Write A Note For The Audit File That Evaluated The Company's Business Risks and The Related Inherent Risks

Write A Note For The Audit File That Evaluated The Company's Business Risks and The Related Inherent Risks

You might also like

- Security Plus Solutions-UFEDocument19 pagesSecurity Plus Solutions-UFEDylan MNo ratings yet

- Moodys - Sample Questions 3Document16 pagesMoodys - Sample Questions 3ivaNo ratings yet

- Hyd Gstdata 26052022 6Document5,589 pagesHyd Gstdata 26052022 6PDRK BABIU100% (6)

- ACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDocument3 pagesACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDylan AdrianNo ratings yet

- Solutions of The Audit Process. Principles, Practice and CasesDocument71 pagesSolutions of The Audit Process. Principles, Practice and Casesletuan221290% (10)

- Case 1Document22 pagesCase 1Let it be100% (1)

- Credit PolicyDocument84 pagesCredit PolicyDan John Karikottu100% (6)

- Next 4Document10 pagesNext 4Nurhasanah Asyari100% (1)

- Global Marketing and Advertising Understanding Cultural ParDocument10 pagesGlobal Marketing and Advertising Understanding Cultural ParrakhrasNo ratings yet

- BS EN12079-1999 (Inspection and Testing of Offshore ContainerDocument32 pagesBS EN12079-1999 (Inspection and Testing of Offshore Containerjohnsonpinto100% (3)

- Write A Note For The Audit File That Evaluated The Company's Business Risks and The Related Inherent RisksDocument4 pagesWrite A Note For The Audit File That Evaluated The Company's Business Risks and The Related Inherent RisksRahulNo ratings yet

- Bva 3Document7 pagesBva 3najaneNo ratings yet

- CASE 3 & 4 InggrisDocument22 pagesCASE 3 & 4 InggrisFifke Masyie SiwuNo ratings yet

- Accounting Theory Mid-Exam: By: Rusmian Nuzulul P. / 0910233137Document6 pagesAccounting Theory Mid-Exam: By: Rusmian Nuzulul P. / 0910233137Rusmian Nuzulul PujakaneoNo ratings yet

- Advanced Cost and Management AccountingDocument3 pagesAdvanced Cost and Management AccountingSharvin MoorthyNo ratings yet

- Kieso15e ContinuingCase Sols Vol1Document41 pagesKieso15e ContinuingCase Sols Vol1HảiAnhInviNo ratings yet

- Actuarial Assumptions: 6.1 Sources of DataDocument9 pagesActuarial Assumptions: 6.1 Sources of DataEphilda TatendaMtisiNo ratings yet

- Financial - DictionaryDocument242 pagesFinancial - DictionarySreni VasanNo ratings yet

- CP3 SolutionDocument4 pagesCP3 SolutionWilson ManyongaNo ratings yet

- Request Template: Article Title Purpose/IntentionDocument2 pagesRequest Template: Article Title Purpose/IntentionPhil DubleyNo ratings yet

- Horizontal Analysis - Horizontal Analysis Is Used in Financial Statement Analysis To CompareDocument3 pagesHorizontal Analysis - Horizontal Analysis Is Used in Financial Statement Analysis To CompareShanelle SilmaroNo ratings yet

- FM Unit - IV Accounts Receivables MGT ......Document90 pagesFM Unit - IV Accounts Receivables MGT ......muruganthunaiNo ratings yet

- M&a Facilitators: The Value of Earnouts - StoutDocument8 pagesM&a Facilitators: The Value of Earnouts - StoutadbaNo ratings yet

- C2 Accounts Receivable ManagementDocument7 pagesC2 Accounts Receivable ManagementTENGKU ANIS TENGKU YUSMANo ratings yet

- Session 2 SolutionsDocument11 pagesSession 2 SolutionsAaron ChandlerNo ratings yet

- Summary of Audit & Assurance Application Level - Worked ExampleDocument22 pagesSummary of Audit & Assurance Application Level - Worked ExampleIQBAL MAHMUDNo ratings yet

- Uts Teori AkuntansiDocument6 pagesUts Teori AkuntansiARYA AZHARI -No ratings yet

- Chapter 10Document23 pagesChapter 10chelintiNo ratings yet

- 10Document8 pages10farhanNo ratings yet

- CombinedDocument47 pagesCombinednsnhemachenaNo ratings yet

- A Letter From PrisonDocument7 pagesA Letter From PrisonFayeeeeNo ratings yet

- Net Credit Sales: August 19, 2017Document10 pagesNet Credit Sales: August 19, 2017Armira Rodriguez ConchaNo ratings yet

- Business Expansion: Example # 1 Overall Analysis of Proposed U.S. ExpansionDocument10 pagesBusiness Expansion: Example # 1 Overall Analysis of Proposed U.S. ExpansionrgaeastindianNo ratings yet

- Accounting For Customer Loyalty Programmes - IFRS PerspectiveDocument5 pagesAccounting For Customer Loyalty Programmes - IFRS PerspectiveFauzi Al-lakadarnyaNo ratings yet

- Case 5.15 Audit 202Document3 pagesCase 5.15 Audit 202DonNo ratings yet

- Accounting T-Research Essay: Total Word Count: 1503 Essay Word Count: 1364Document5 pagesAccounting T-Research Essay: Total Word Count: 1503 Essay Word Count: 1364agamdeepNo ratings yet

- Actuarial AnalysisDocument12 pagesActuarial AnalysisNikita MalhotraNo ratings yet

- A. Questions That Need To Be Addressed IncludeDocument3 pagesA. Questions That Need To Be Addressed IncludeAhmad Zamri OsmanNo ratings yet

- Notes in Fi3Document5 pagesNotes in Fi3Gray JavierNo ratings yet

- Seatwork: PAGE 173 - Case # 2 A. If Gonzales Wants To Provide The Presentation and CPA's Report For General Use byDocument4 pagesSeatwork: PAGE 173 - Case # 2 A. If Gonzales Wants To Provide The Presentation and CPA's Report For General Use byNikky Bless LeonarNo ratings yet

- The Challenges and Opportunities of Customer Profitability AnalysisDocument7 pagesThe Challenges and Opportunities of Customer Profitability AnalysisSarah ChengNo ratings yet

- AUDITINGDocument6 pagesAUDITINGVISAYANA JACQUELINENo ratings yet

- What Is ProfitabilityDocument7 pagesWhat Is ProfitabilityvenkateshNo ratings yet

- Audit On Account ReceivablesDocument7 pagesAudit On Account ReceivablesRonald Ian GoontingNo ratings yet

- Google 10k 2015Document3 pagesGoogle 10k 2015EliasNo ratings yet

- Burget Paints Financial Report Summary and InsightsDocument5 pagesBurget Paints Financial Report Summary and InsightscoolNo ratings yet

- Case 2-1 - Solution: Estimated Time To Complete This Case Is 1 To 1.5 HrsDocument10 pagesCase 2-1 - Solution: Estimated Time To Complete This Case Is 1 To 1.5 HrsUsman GorayaNo ratings yet

- Assignment June 15Document3 pagesAssignment June 15BlackChemistry GuipetacioNo ratings yet

- LenovoDocument5 pagesLenovoamin233No ratings yet

- Module-III Analytical Tools in Sourcing, Pricing Analysis: Foreign Exchange Currency ManagementDocument10 pagesModule-III Analytical Tools in Sourcing, Pricing Analysis: Foreign Exchange Currency ManagementumeshNo ratings yet

- Notes On Weighted-Average Cost of Capital (WACC) : Finance 422Document5 pagesNotes On Weighted-Average Cost of Capital (WACC) : Finance 422Dan MaloneyNo ratings yet

- Dissertation On Revenue RecognitionDocument7 pagesDissertation On Revenue RecognitionCollegePaperGhostWriterSterlingHeights100% (1)

- Dmp3e Ch06 Solutions 01.26.10 FinalDocument39 pagesDmp3e Ch06 Solutions 01.26.10 Finalmichaelkwok1No ratings yet

- Aaa 5Document3 pagesAaa 5Hamza ZahidNo ratings yet

- How To Value A Company by Analyzing Its CustomersDocument10 pagesHow To Value A Company by Analyzing Its CustomersAnkit AgrawalNo ratings yet

- CH 4 Solved Exercises Focusing - On - CustomersDocument8 pagesCH 4 Solved Exercises Focusing - On - Customersanumshahzad_16No ratings yet

- At The End of This Chapter, You Will Be Able ToDocument29 pagesAt The End of This Chapter, You Will Be Able ToAki GirmNo ratings yet

- ACC 111 Assessment 2 - Project: Adam MuhammadDocument7 pagesACC 111 Assessment 2 - Project: Adam Muhammadmuhammad raqibNo ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18From EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18No ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments 2018/19From EverandAudit Risk Alert: General Accounting and Auditing Developments 2018/19No ratings yet

- Theoretical Question 2 - Nana PDFDocument1 pageTheoretical Question 2 - Nana PDFRahulNo ratings yet

- One Line Rent Roll (April 17, 2020)Document24 pagesOne Line Rent Roll (April 17, 2020)RahulNo ratings yet

- Theoretical Question 1 - Company Do SeaDocument1 pageTheoretical Question 1 - Company Do SeaRahulNo ratings yet

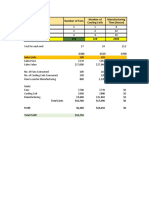

- Model Number of Fans Number of Cooling Coils Manufacturing Time (Hours)Document5 pagesModel Number of Fans Number of Cooling Coils Manufacturing Time (Hours)RahulNo ratings yet

- Purchasing Power Parity (PPP)Document3 pagesPurchasing Power Parity (PPP)RahulNo ratings yet

- Write A Note For The Audit File That Evaluated The Company's Business Risks and The Related Inherent RisksDocument4 pagesWrite A Note For The Audit File That Evaluated The Company's Business Risks and The Related Inherent RisksRahulNo ratings yet

- Vortex Bladeless Wind TurbineDocument3 pagesVortex Bladeless Wind TurbineLokesh Kumar GuptaNo ratings yet

- D093/D094 Service ManualDocument779 pagesD093/D094 Service ManualMr DungNo ratings yet

- Chapter 6Document34 pagesChapter 6Nguyễn Nhật SangNo ratings yet

- Fitsum Kelilie PDFDocument84 pagesFitsum Kelilie PDFYeabsera DemelashNo ratings yet

- Lecture 4Document48 pagesLecture 4mohsinNo ratings yet

- RFC3227 - Guidelines For Evidence Collection and ArchivingDocument10 pagesRFC3227 - Guidelines For Evidence Collection and ArchivingPyroargerNo ratings yet

- Data Transmission Over Inmarsat in TCP/IP EnvironmentDocument7 pagesData Transmission Over Inmarsat in TCP/IP EnvironmentpankajlangadeNo ratings yet

- FMD 2022 Half Year Activity Report - FinalDocument78 pagesFMD 2022 Half Year Activity Report - FinalPaul WaltersNo ratings yet

- Sbi Life EshieldDocument6 pagesSbi Life EshieldAnkit VyasNo ratings yet

- 21BCS11102 - Prashant Kumar C++ 1.3Document13 pages21BCS11102 - Prashant Kumar C++ 1.3AswinNo ratings yet

- Week 1Document3 pagesWeek 1Jemalyn Mina100% (1)

- Abstract On Honey PotsDocument18 pagesAbstract On Honey PotsBen Garcia100% (3)

- Scope of SupplyDocument12 pagesScope of Supplyreza39No ratings yet

- Sub Order LabelsDocument4 pagesSub Order LabelsLubhNo ratings yet

- PCR Measur Tektronix PDFDocument24 pagesPCR Measur Tektronix PDFGrzegorz ZissNo ratings yet

- Introduction To Auto CadDocument31 pagesIntroduction To Auto CadazhiNo ratings yet

- Survey of Termites in Forests of Punjab PakistanDocument8 pagesSurvey of Termites in Forests of Punjab Pakistan2039123No ratings yet

- Sample Skillshare Class Outline - Dylan MierzwinskiDocument4 pagesSample Skillshare Class Outline - Dylan MierzwinskiBBMS ResearcherNo ratings yet

- Yahoo Business StrategyDocument9 pagesYahoo Business Strategytanvir7650% (2)

- MQTT VulneribilitiesDocument6 pagesMQTT VulneribilitiesAbdul HadiNo ratings yet

- AE211 Final ExamDocument10 pagesAE211 Final ExamMariette Alex AgbanlogNo ratings yet

- PyQt For Autodesk Maya 2015 64bitDocument9 pagesPyQt For Autodesk Maya 2015 64bitJadTahhanNo ratings yet

- Machines 07 00042 PDFDocument21 pagesMachines 07 00042 PDFguterresNo ratings yet

- Case Digest: Atty Ricafort V Atty BansilDocument3 pagesCase Digest: Atty Ricafort V Atty BansilmavslastimozaNo ratings yet

- Construction Inc - QTN3255Document1 pageConstruction Inc - QTN3255denciopo61No ratings yet

- FIBRS Incident Report: Pembroke Pines Police Department 9500 Pines BLVD Pembroke Pines, FLDocument5 pagesFIBRS Incident Report: Pembroke Pines Police Department 9500 Pines BLVD Pembroke Pines, FLbrianna sahibdeenNo ratings yet

- Apparel ManufacturingDocument13 pagesApparel ManufacturingBoier Sesh Pata100% (1)

Download as docx, pdf, or txt

You might also like

- Security Plus Solutions-UFEDocument19 pagesSecurity Plus Solutions-UFEDylan MNo ratings yet

- Moodys - Sample Questions 3Document16 pagesMoodys - Sample Questions 3ivaNo ratings yet

- Hyd Gstdata 26052022 6Document5,589 pagesHyd Gstdata 26052022 6PDRK BABIU100% (6)

- ACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDocument3 pagesACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDylan AdrianNo ratings yet

- Solutions of The Audit Process. Principles, Practice and CasesDocument71 pagesSolutions of The Audit Process. Principles, Practice and Casesletuan221290% (10)

- Case 1Document22 pagesCase 1Let it be100% (1)

- Credit PolicyDocument84 pagesCredit PolicyDan John Karikottu100% (6)

- Next 4Document10 pagesNext 4Nurhasanah Asyari100% (1)

- Global Marketing and Advertising Understanding Cultural ParDocument10 pagesGlobal Marketing and Advertising Understanding Cultural ParrakhrasNo ratings yet

- BS EN12079-1999 (Inspection and Testing of Offshore ContainerDocument32 pagesBS EN12079-1999 (Inspection and Testing of Offshore Containerjohnsonpinto100% (3)

- Write A Note For The Audit File That Evaluated The Company's Business Risks and The Related Inherent RisksDocument4 pagesWrite A Note For The Audit File That Evaluated The Company's Business Risks and The Related Inherent RisksRahulNo ratings yet

- Bva 3Document7 pagesBva 3najaneNo ratings yet

- CASE 3 & 4 InggrisDocument22 pagesCASE 3 & 4 InggrisFifke Masyie SiwuNo ratings yet

- Accounting Theory Mid-Exam: By: Rusmian Nuzulul P. / 0910233137Document6 pagesAccounting Theory Mid-Exam: By: Rusmian Nuzulul P. / 0910233137Rusmian Nuzulul PujakaneoNo ratings yet

- Advanced Cost and Management AccountingDocument3 pagesAdvanced Cost and Management AccountingSharvin MoorthyNo ratings yet

- Kieso15e ContinuingCase Sols Vol1Document41 pagesKieso15e ContinuingCase Sols Vol1HảiAnhInviNo ratings yet

- Actuarial Assumptions: 6.1 Sources of DataDocument9 pagesActuarial Assumptions: 6.1 Sources of DataEphilda TatendaMtisiNo ratings yet

- Financial - DictionaryDocument242 pagesFinancial - DictionarySreni VasanNo ratings yet

- CP3 SolutionDocument4 pagesCP3 SolutionWilson ManyongaNo ratings yet

- Request Template: Article Title Purpose/IntentionDocument2 pagesRequest Template: Article Title Purpose/IntentionPhil DubleyNo ratings yet

- Horizontal Analysis - Horizontal Analysis Is Used in Financial Statement Analysis To CompareDocument3 pagesHorizontal Analysis - Horizontal Analysis Is Used in Financial Statement Analysis To CompareShanelle SilmaroNo ratings yet

- FM Unit - IV Accounts Receivables MGT ......Document90 pagesFM Unit - IV Accounts Receivables MGT ......muruganthunaiNo ratings yet

- M&a Facilitators: The Value of Earnouts - StoutDocument8 pagesM&a Facilitators: The Value of Earnouts - StoutadbaNo ratings yet

- C2 Accounts Receivable ManagementDocument7 pagesC2 Accounts Receivable ManagementTENGKU ANIS TENGKU YUSMANo ratings yet

- Session 2 SolutionsDocument11 pagesSession 2 SolutionsAaron ChandlerNo ratings yet

- Summary of Audit & Assurance Application Level - Worked ExampleDocument22 pagesSummary of Audit & Assurance Application Level - Worked ExampleIQBAL MAHMUDNo ratings yet

- Uts Teori AkuntansiDocument6 pagesUts Teori AkuntansiARYA AZHARI -No ratings yet

- Chapter 10Document23 pagesChapter 10chelintiNo ratings yet

- 10Document8 pages10farhanNo ratings yet

- CombinedDocument47 pagesCombinednsnhemachenaNo ratings yet

- A Letter From PrisonDocument7 pagesA Letter From PrisonFayeeeeNo ratings yet

- Net Credit Sales: August 19, 2017Document10 pagesNet Credit Sales: August 19, 2017Armira Rodriguez ConchaNo ratings yet

- Business Expansion: Example # 1 Overall Analysis of Proposed U.S. ExpansionDocument10 pagesBusiness Expansion: Example # 1 Overall Analysis of Proposed U.S. ExpansionrgaeastindianNo ratings yet

- Accounting For Customer Loyalty Programmes - IFRS PerspectiveDocument5 pagesAccounting For Customer Loyalty Programmes - IFRS PerspectiveFauzi Al-lakadarnyaNo ratings yet

- Case 5.15 Audit 202Document3 pagesCase 5.15 Audit 202DonNo ratings yet

- Accounting T-Research Essay: Total Word Count: 1503 Essay Word Count: 1364Document5 pagesAccounting T-Research Essay: Total Word Count: 1503 Essay Word Count: 1364agamdeepNo ratings yet

- Actuarial AnalysisDocument12 pagesActuarial AnalysisNikita MalhotraNo ratings yet

- A. Questions That Need To Be Addressed IncludeDocument3 pagesA. Questions That Need To Be Addressed IncludeAhmad Zamri OsmanNo ratings yet

- Notes in Fi3Document5 pagesNotes in Fi3Gray JavierNo ratings yet

- Seatwork: PAGE 173 - Case # 2 A. If Gonzales Wants To Provide The Presentation and CPA's Report For General Use byDocument4 pagesSeatwork: PAGE 173 - Case # 2 A. If Gonzales Wants To Provide The Presentation and CPA's Report For General Use byNikky Bless LeonarNo ratings yet

- The Challenges and Opportunities of Customer Profitability AnalysisDocument7 pagesThe Challenges and Opportunities of Customer Profitability AnalysisSarah ChengNo ratings yet

- AUDITINGDocument6 pagesAUDITINGVISAYANA JACQUELINENo ratings yet

- What Is ProfitabilityDocument7 pagesWhat Is ProfitabilityvenkateshNo ratings yet

- Audit On Account ReceivablesDocument7 pagesAudit On Account ReceivablesRonald Ian GoontingNo ratings yet

- Google 10k 2015Document3 pagesGoogle 10k 2015EliasNo ratings yet

- Burget Paints Financial Report Summary and InsightsDocument5 pagesBurget Paints Financial Report Summary and InsightscoolNo ratings yet

- Case 2-1 - Solution: Estimated Time To Complete This Case Is 1 To 1.5 HrsDocument10 pagesCase 2-1 - Solution: Estimated Time To Complete This Case Is 1 To 1.5 HrsUsman GorayaNo ratings yet

- Assignment June 15Document3 pagesAssignment June 15BlackChemistry GuipetacioNo ratings yet

- LenovoDocument5 pagesLenovoamin233No ratings yet

- Module-III Analytical Tools in Sourcing, Pricing Analysis: Foreign Exchange Currency ManagementDocument10 pagesModule-III Analytical Tools in Sourcing, Pricing Analysis: Foreign Exchange Currency ManagementumeshNo ratings yet

- Notes On Weighted-Average Cost of Capital (WACC) : Finance 422Document5 pagesNotes On Weighted-Average Cost of Capital (WACC) : Finance 422Dan MaloneyNo ratings yet

- Dissertation On Revenue RecognitionDocument7 pagesDissertation On Revenue RecognitionCollegePaperGhostWriterSterlingHeights100% (1)

- Dmp3e Ch06 Solutions 01.26.10 FinalDocument39 pagesDmp3e Ch06 Solutions 01.26.10 Finalmichaelkwok1No ratings yet

- Aaa 5Document3 pagesAaa 5Hamza ZahidNo ratings yet

- How To Value A Company by Analyzing Its CustomersDocument10 pagesHow To Value A Company by Analyzing Its CustomersAnkit AgrawalNo ratings yet

- CH 4 Solved Exercises Focusing - On - CustomersDocument8 pagesCH 4 Solved Exercises Focusing - On - Customersanumshahzad_16No ratings yet

- At The End of This Chapter, You Will Be Able ToDocument29 pagesAt The End of This Chapter, You Will Be Able ToAki GirmNo ratings yet

- ACC 111 Assessment 2 - Project: Adam MuhammadDocument7 pagesACC 111 Assessment 2 - Project: Adam Muhammadmuhammad raqibNo ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments, 2017/18From EverandAudit Risk Alert: General Accounting and Auditing Developments, 2017/18No ratings yet

- Audit Risk Alert: General Accounting and Auditing Developments 2018/19From EverandAudit Risk Alert: General Accounting and Auditing Developments 2018/19No ratings yet

- Theoretical Question 2 - Nana PDFDocument1 pageTheoretical Question 2 - Nana PDFRahulNo ratings yet

- One Line Rent Roll (April 17, 2020)Document24 pagesOne Line Rent Roll (April 17, 2020)RahulNo ratings yet

- Theoretical Question 1 - Company Do SeaDocument1 pageTheoretical Question 1 - Company Do SeaRahulNo ratings yet

- Model Number of Fans Number of Cooling Coils Manufacturing Time (Hours)Document5 pagesModel Number of Fans Number of Cooling Coils Manufacturing Time (Hours)RahulNo ratings yet

- Purchasing Power Parity (PPP)Document3 pagesPurchasing Power Parity (PPP)RahulNo ratings yet

- Write A Note For The Audit File That Evaluated The Company's Business Risks and The Related Inherent RisksDocument4 pagesWrite A Note For The Audit File That Evaluated The Company's Business Risks and The Related Inherent RisksRahulNo ratings yet

- Vortex Bladeless Wind TurbineDocument3 pagesVortex Bladeless Wind TurbineLokesh Kumar GuptaNo ratings yet

- D093/D094 Service ManualDocument779 pagesD093/D094 Service ManualMr DungNo ratings yet

- Chapter 6Document34 pagesChapter 6Nguyễn Nhật SangNo ratings yet

- Fitsum Kelilie PDFDocument84 pagesFitsum Kelilie PDFYeabsera DemelashNo ratings yet

- Lecture 4Document48 pagesLecture 4mohsinNo ratings yet

- RFC3227 - Guidelines For Evidence Collection and ArchivingDocument10 pagesRFC3227 - Guidelines For Evidence Collection and ArchivingPyroargerNo ratings yet

- Data Transmission Over Inmarsat in TCP/IP EnvironmentDocument7 pagesData Transmission Over Inmarsat in TCP/IP EnvironmentpankajlangadeNo ratings yet

- FMD 2022 Half Year Activity Report - FinalDocument78 pagesFMD 2022 Half Year Activity Report - FinalPaul WaltersNo ratings yet

- Sbi Life EshieldDocument6 pagesSbi Life EshieldAnkit VyasNo ratings yet

- 21BCS11102 - Prashant Kumar C++ 1.3Document13 pages21BCS11102 - Prashant Kumar C++ 1.3AswinNo ratings yet

- Week 1Document3 pagesWeek 1Jemalyn Mina100% (1)

- Abstract On Honey PotsDocument18 pagesAbstract On Honey PotsBen Garcia100% (3)

- Scope of SupplyDocument12 pagesScope of Supplyreza39No ratings yet

- Sub Order LabelsDocument4 pagesSub Order LabelsLubhNo ratings yet

- PCR Measur Tektronix PDFDocument24 pagesPCR Measur Tektronix PDFGrzegorz ZissNo ratings yet

- Introduction To Auto CadDocument31 pagesIntroduction To Auto CadazhiNo ratings yet

- Survey of Termites in Forests of Punjab PakistanDocument8 pagesSurvey of Termites in Forests of Punjab Pakistan2039123No ratings yet

- Sample Skillshare Class Outline - Dylan MierzwinskiDocument4 pagesSample Skillshare Class Outline - Dylan MierzwinskiBBMS ResearcherNo ratings yet

- Yahoo Business StrategyDocument9 pagesYahoo Business Strategytanvir7650% (2)

- MQTT VulneribilitiesDocument6 pagesMQTT VulneribilitiesAbdul HadiNo ratings yet

- AE211 Final ExamDocument10 pagesAE211 Final ExamMariette Alex AgbanlogNo ratings yet

- PyQt For Autodesk Maya 2015 64bitDocument9 pagesPyQt For Autodesk Maya 2015 64bitJadTahhanNo ratings yet

- Machines 07 00042 PDFDocument21 pagesMachines 07 00042 PDFguterresNo ratings yet

- Case Digest: Atty Ricafort V Atty BansilDocument3 pagesCase Digest: Atty Ricafort V Atty BansilmavslastimozaNo ratings yet

- Construction Inc - QTN3255Document1 pageConstruction Inc - QTN3255denciopo61No ratings yet

- FIBRS Incident Report: Pembroke Pines Police Department 9500 Pines BLVD Pembroke Pines, FLDocument5 pagesFIBRS Incident Report: Pembroke Pines Police Department 9500 Pines BLVD Pembroke Pines, FLbrianna sahibdeenNo ratings yet

- Apparel ManufacturingDocument13 pagesApparel ManufacturingBoier Sesh Pata100% (1)