Download as pdf or txt

You might also like

- Project On Retail BankingDocument74 pagesProject On Retail BankingManasvi Darshan Tolia80% (5)

- Pooja MishraDocument7 pagesPooja MishrasmsmbaNo ratings yet

- Consumer Perception Towards HDFC BankDocument55 pagesConsumer Perception Towards HDFC BankMajid Ali0% (3)

- Small & Payment Banks PPT FinalDocument12 pagesSmall & Payment Banks PPT FinalAakash JainNo ratings yet

- Sikkim Manipal University: "Comparative Study On Customer's Loyalty inDocument8 pagesSikkim Manipal University: "Comparative Study On Customer's Loyalty inSubrat PatnaikNo ratings yet

- Awareness and Satisfaction Level of Financial Products Offered by ICICI Bank and HDFC BankDocument13 pagesAwareness and Satisfaction Level of Financial Products Offered by ICICI Bank and HDFC BankPankaj AhujaNo ratings yet

- Literature ReviewDocument10 pagesLiterature Reviewridhiarora2378% (9)

- Wjarr 2024 0993Document7 pagesWjarr 2024 0993mcvallespinNo ratings yet

- Research Proposal ReportDocument5 pagesResearch Proposal ReportMEERA JOSHY 1927436No ratings yet

- A Project Report On HDFC and SbiDocument47 pagesA Project Report On HDFC and SbiMminu CharaniaNo ratings yet

- Service Quality Perceptions: A Case Study of Banking ServicesDocument19 pagesService Quality Perceptions: A Case Study of Banking ServicesLaurent GelyNo ratings yet

- Customer Satisfaction and Reasons For Using Value Added Services Offered by Selected Commercial Banks in Thoothukudi DistrictDocument16 pagesCustomer Satisfaction and Reasons For Using Value Added Services Offered by Selected Commercial Banks in Thoothukudi DistrictPeter HeinNo ratings yet

- A Study On Customer Satisfaction Towards Banking Services of The State Bank of IndiaDocument45 pagesA Study On Customer Satisfaction Towards Banking Services of The State Bank of IndiaArchana YadavNo ratings yet

- Excutive SummaryDocument42 pagesExcutive SummaryRiya TomarNo ratings yet

- An Analytical Study of Various Policies Related To Personal Financing Services of Icici Bank With Special Reference To Western Uttar PradeshDocument11 pagesAn Analytical Study of Various Policies Related To Personal Financing Services of Icici Bank With Special Reference To Western Uttar PradeshAnubhav SonyNo ratings yet

- Summer Internships 2011 MBA 2010-12: Role of IT in The Banking IndustryDocument71 pagesSummer Internships 2011 MBA 2010-12: Role of IT in The Banking IndustrySakshi DuaNo ratings yet

- Objective of The StudyDocument13 pagesObjective of The StudyYogendra Kumar Jain100% (1)

- Internet Banking: by Cheguri AkshithaDocument18 pagesInternet Banking: by Cheguri Akshithacheguri akshithaNo ratings yet

- A Study On Innovation in Banking and Its Impact On Customer SatisfactionDocument5 pagesA Study On Innovation in Banking and Its Impact On Customer SatisfactionMaulik patelNo ratings yet

- Devendra Tiwari Mba MRPDocument26 pagesDevendra Tiwari Mba MRPambrishgpt9360% (1)

- Deepali Project ReportDocument34 pagesDeepali Project ReportAshish MOHARENo ratings yet

- A Study On Customer Perception Towards Online Banking Services of State Bank of India in Jalna DistrictDocument7 pagesA Study On Customer Perception Towards Online Banking Services of State Bank of India in Jalna DistrictIJAR JOURNALNo ratings yet

- A Study On Customers Satisfaction-1102-With-cover-page-V2 Ex ProjectDocument16 pagesA Study On Customers Satisfaction-1102-With-cover-page-V2 Ex ProjectFelix ChristoferNo ratings yet

- Customer Relationship Management in Banking Sector (With Special Reference To ICICI Bank)Document7 pagesCustomer Relationship Management in Banking Sector (With Special Reference To ICICI Bank)Sufiyan JugariNo ratings yet

- A Study On Services Quality of SBI In: P.RoselinDocument4 pagesA Study On Services Quality of SBI In: P.RoselinSanchit ParnamiNo ratings yet

- Synopsis On:a Study of The Banking Sector in India - With Reference To Net BankingDocument7 pagesSynopsis On:a Study of The Banking Sector in India - With Reference To Net BankingSaurabh SinghNo ratings yet

- Consumer Perception Towards Public SectoDocument24 pagesConsumer Perception Towards Public SectojayNo ratings yet

- Customer's Perception Towards Internet Banking: A Study of Sirsa CityDocument8 pagesCustomer's Perception Towards Internet Banking: A Study of Sirsa Cityਅਮਨਦੀਪ ਸਿੰਘ ਰੋਗਲਾNo ratings yet

- Customer Perception Project - 075845Document7 pagesCustomer Perception Project - 075845Karthik NNo ratings yet

- HDFC BankDocument20 pagesHDFC Bankmohd.irfanNo ratings yet

- Customer Satisfaction Regarding Consumer Loan With Specialreference To PUNJAB AND SIND BANKDocument60 pagesCustomer Satisfaction Regarding Consumer Loan With Specialreference To PUNJAB AND SIND BANKSaurabh Mehta0% (1)

- Chapter 1 PDFDocument26 pagesChapter 1 PDFPriyanka KanseNo ratings yet

- Literature Review of Retail Banking in IndiaDocument5 pagesLiterature Review of Retail Banking in Indiac5qfb5v5100% (1)

- Customers Perception On Banking ServicesDocument96 pagesCustomers Perception On Banking ServicesAnonymous 1Ij456aNo ratings yet

- Master of Business Administration Rajasthan Technical University, KOTADocument70 pagesMaster of Business Administration Rajasthan Technical University, KOTAHatim AliNo ratings yet

- 08 Chapter 1Document9 pages08 Chapter 157 SHIVANI KANOJIYANo ratings yet

- E Banking - HDFCDocument7 pagesE Banking - HDFCmohammed khayyumNo ratings yet

- SIP PresentationDocument24 pagesSIP PresentationGorang MuthaNo ratings yet

- Impact of Technological Changes On Customer: Experience in Banking Sector-A Study of Select Banks in Madhya PradeshDocument12 pagesImpact of Technological Changes On Customer: Experience in Banking Sector-A Study of Select Banks in Madhya PradeshSiddharthJainNo ratings yet

- Mohammad Fazal-1Document81 pagesMohammad Fazal-1Norma SanfordNo ratings yet

- A3Document17 pagesA3Varsha VarshaNo ratings yet

- Project Report (AutoRecovered)Document34 pagesProject Report (AutoRecovered)Ashish MOHARENo ratings yet

- Project ReportDocument38 pagesProject Reportsunidhimishra2375No ratings yet

- Neha Kumari MahatoDocument50 pagesNeha Kumari MahatoIshaan JaiswalNo ratings yet

- SaranyaDocument24 pagesSaranyaSachin chinnuNo ratings yet

- Customer Satisfaction and Awarness On Public Sector Bank Sectors in TiruchirappalliDocument8 pagesCustomer Satisfaction and Awarness On Public Sector Bank Sectors in TiruchirappalliIAEME PublicationNo ratings yet

- Impact of E-Banking in India: Presented By-Shouvik Maji PGDM - 75Document11 pagesImpact of E-Banking in India: Presented By-Shouvik Maji PGDM - 75Nilanjan GhoshNo ratings yet

- Ankitha - Ret BankDocument25 pagesAnkitha - Ret BankMOHAMMED KHAYYUMNo ratings yet

- Customer Satisfaction in BanksDocument20 pagesCustomer Satisfaction in Banksp_chopra1010957088% (48)

- A Project Report On Online BankingDocument18 pagesA Project Report On Online BankingSourav PaulNo ratings yet

- A Study On CustomerDocument24 pagesA Study On CustomerROHITNo ratings yet

- Project Report OnDocument91 pagesProject Report OnSurajNo ratings yet

- Retail Banking Issues and Concerns in India: Madhvi JulkaDocument8 pagesRetail Banking Issues and Concerns in India: Madhvi JulkadeepakpinksuratNo ratings yet

- Online BankingDocument46 pagesOnline BankingNazmulHasanNo ratings yet

- Final Report of Vijaya Bank Part 2Document49 pagesFinal Report of Vijaya Bank Part 2shivangi shawNo ratings yet

- Online BankingDocument31 pagesOnline BankingRavi Kashyap506No ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- Marketing of Consumer Financial Products: Insights From Service MarketingFrom EverandMarketing of Consumer Financial Products: Insights From Service MarketingNo ratings yet

- " Digitalisation of Banks " PDFDocument74 pages" Digitalisation of Banks " PDFHIMANI GERANo ratings yet

- List of Payment Banks & Small Finance Banks: For Bank and Government ExamsDocument7 pagesList of Payment Banks & Small Finance Banks: For Bank and Government Examsjiby georgeNo ratings yet

- The Evolution of Banking in IndiaDocument5 pagesThe Evolution of Banking in IndiaCyril ChettiarNo ratings yet

- PPB Module 1Document42 pagesPPB Module 1RAJNo ratings yet

- Banking Awareness August Set 2: Dr. Gaurav GargDocument3 pagesBanking Awareness August Set 2: Dr. Gaurav Gargkarunakaran09No ratings yet

- L15 Scheduled BANKS PDFDocument14 pagesL15 Scheduled BANKS PDFakshita raoNo ratings yet

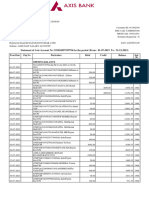

- Account STMT XX9794 31122023Document16 pagesAccount STMT XX9794 31122023shubhamkasyap443No ratings yet

- APB CSP Enrollment Form - Dec'18Document3 pagesAPB CSP Enrollment Form - Dec'18Smart CalligraphyNo ratings yet

- C12 Bank Audit Complete NotesDocument42 pagesC12 Bank Audit Complete Noteschananakartik1No ratings yet

- Shyamal Money & BankingDocument95 pagesShyamal Money & BankingSHYAMAL BANERJEENo ratings yet

- Recent Weeks Clients Payment: Transfer DetailsDocument23 pagesRecent Weeks Clients Payment: Transfer DetailsPreasia WilfredNo ratings yet

- Overview of Banking IndustryDocument12 pagesOverview of Banking Industrybeena antuNo ratings yet

- Financial Institutions PYQ Lyst4152Document47 pagesFinancial Institutions PYQ Lyst4152pallavchhawan0910No ratings yet

- Iare Birm Lecture NotesDocument188 pagesIare Birm Lecture NotesSumit Kumar GautamNo ratings yet

- Current Affairs Q&A PDF May 25 2023 by Affairscloud New 1Document19 pagesCurrent Affairs Q&A PDF May 25 2023 by Affairscloud New 1Atish PandaNo ratings yet

- Summary Sheet - Rural Banking and Financial Institutes in India Lyst2962Document20 pagesSummary Sheet - Rural Banking and Financial Institutes in India Lyst2962swasat duttaNo ratings yet

- Paytm BankDocument10 pagesPaytm BankGobind SinghNo ratings yet

- Payment Bank Impact On Digital BankingDocument78 pagesPayment Bank Impact On Digital BankingSudharshan Reddy P0% (1)

- PPB - Complete PDFDocument185 pagesPPB - Complete PDFishantkathuriaNo ratings yet

- RBI Grade B 16 August 2018 Memory Based (English)Document50 pagesRBI Grade B 16 August 2018 Memory Based (English)VinayRajNo ratings yet

- Final GK Power Capsule For Rbi Assistant Mains 2017 by Gopal Sir and TeamDocument66 pagesFinal GK Power Capsule For Rbi Assistant Mains 2017 by Gopal Sir and TeamJagannath JagguNo ratings yet

- Aditya ChavanDocument87 pagesAditya ChavanAditya ChavanNo ratings yet

- May Q&ADocument169 pagesMay Q&AEliteNo ratings yet

- Banking Awareness QuizDocument23 pagesBanking Awareness Quizjay meskaNo ratings yet

- Bank Quest October - December 2022Document68 pagesBank Quest October - December 2022Naveen Kumar PoosalaNo ratings yet

- Banking & Economy PDF - March 2021 by AffairsCloud 1Document218 pagesBanking & Economy PDF - March 2021 by AffairsCloud 1most funny videoNo ratings yet

- BSC Magazine Exclusive July Monthly GA MCQs FinalDocument50 pagesBSC Magazine Exclusive July Monthly GA MCQs Finalshikharv90No ratings yet

- Current Affairs of February 2024Document36 pagesCurrent Affairs of February 2024imrankhan872019No ratings yet

- Payments BankDocument3 pagesPayments BankSwagata GhoshNo ratings yet