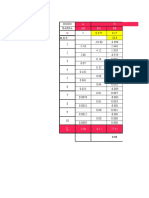

Seasonality Effect On Pakistan Stock Exchnage.: Table 1 Descriptive Analysis

Seasonality Effect On Pakistan Stock Exchnage.: Table 1 Descriptive Analysis

You might also like

- Diffie-Hellman Key Exchange PDFDocument6 pagesDiffie-Hellman Key Exchange PDFZxzxzxz007No ratings yet

- Operations Research ProjectDocument21 pagesOperations Research ProjectDeepak KanojiaNo ratings yet

- Solutions 1Document7 pagesSolutions 1xinyichen121No ratings yet

- Programa de Lineas de InfluenciaDocument7 pagesPrograma de Lineas de Influenciajose pepe pepeNo ratings yet

- Project Write-Up v3Document19 pagesProject Write-Up v3dongn_13No ratings yet

- Análisis de Modos y FrecuenciasDocument1 pageAnálisis de Modos y FrecuenciasIsabelNo ratings yet

- SDOF Undamped Free VibrationDocument3 pagesSDOF Undamped Free VibrationMananNo ratings yet

- SDOF Undamped Free VibrationDocument3 pagesSDOF Undamped Free VibrationyadavameNo ratings yet

- Soil Consolidation TestDocument5 pagesSoil Consolidation Testsatyam agarwalNo ratings yet

- Beta Estimation Illustration PDFDocument4 pagesBeta Estimation Illustration PDFmehar noorNo ratings yet

- Lampiran 6Document6 pagesLampiran 6Ari WijayaNo ratings yet

- Date HP - Price SP500 - Price T-Bills (Adj. Close) (Adj. Close) (%, APR) Stock Return Excess Return HP Market Index HP Market IndexDocument16 pagesDate HP - Price SP500 - Price T-Bills (Adj. Close) (Adj. Close) (%, APR) Stock Return Excess Return HP Market Index HP Market IndexAlfieNo ratings yet

- Controlling Interest Rates - Bank of Russia Monetary Policy EfficiencyDocument5 pagesControlling Interest Rates - Bank of Russia Monetary Policy EfficiencyJ MNo ratings yet

- Blue Bus485 FinalDocument13 pagesBlue Bus485 FinalTamzid Ahmed AnikNo ratings yet

- Nama: Ibnu Muntaha NIM: 19108010113: RissiDocument6 pagesNama: Ibnu Muntaha NIM: 19108010113: RissiIbnu MuntahaNo ratings yet

- TH2Document2 pagesTH2phamleminh248No ratings yet

- #Information: Name: Sizwe Travor Masango Student Number: 4347545 Group 4 Title: Determning The Mass of The BubbleDocument30 pages#Information: Name: Sizwe Travor Masango Student Number: 4347545 Group 4 Title: Determning The Mass of The Bubblemehdube4No ratings yet

- Aws A5.9 - A5.9m-2017 18Document1 pageAws A5.9 - A5.9m-2017 18erick morenoNo ratings yet

- Tugas - Besar - DRAINASE - TAHAP - 2 - KORNELIS LENDEDocument4 pagesTugas - Besar - DRAINASE - TAHAP - 2 - KORNELIS LENDEKornelis LendeNo ratings yet

- Tri Ayuning Sari - 0115030035Document60 pagesTri Ayuning Sari - 0115030035bahrulNo ratings yet

- Hardy CrossDocument6 pagesHardy Crossellen jolandaNo ratings yet

- School of Civil and Chemical Engineering: B.Tech. Civil Engg CLE 2017 - Hydrology Digital AssignmentDocument1 pageSchool of Civil and Chemical Engineering: B.Tech. Civil Engg CLE 2017 - Hydrology Digital AssignmentshubhamNo ratings yet

- Datos Del Ifnorme de Fluidos CPDocument3 pagesDatos Del Ifnorme de Fluidos CPTania CervantesNo ratings yet

- Adanient X P (X) CDF Frequency Abcapital X P (X) CDF FrequencyDocument6 pagesAdanient X P (X) CDF Frequency Abcapital X P (X) CDF FrequencyrohanNo ratings yet

- Tarea 3.4 - Flores Avila.Document21 pagesTarea 3.4 - Flores Avila.Eriick De Jesús PalemónNo ratings yet

- CASO Crecimiento PlantasDocument17 pagesCASO Crecimiento PlantasGreysiNo ratings yet

- Cross HedgingDocument3 pagesCross HedgingAnupam G. RatheeNo ratings yet

- Data Mining AssignmentDocument4 pagesData Mining AssignmentMusa KhanNo ratings yet

- HelloDocument42 pagesHelloLídia EldianaNo ratings yet

- LinearityDocument4 pagesLinearityll vvNo ratings yet

- Investment Analysis and Portfolio Management: Submitted By, Amal George FK 3463 PGDM 29: FinanceDocument7 pagesInvestment Analysis and Portfolio Management: Submitted By, Amal George FK 3463 PGDM 29: FinanceAnanthasankar SNairNo ratings yet

- Number 3Document2 pagesNumber 3Mhiamar AbelladaNo ratings yet

- MMult Function and Demo of ROIDocument6 pagesMMult Function and Demo of ROIJITESHNo ratings yet

- Simulation Final ProjectDocument10 pagesSimulation Final ProjectSalman SheikhNo ratings yet

- CCATDocument19 pagesCCATgemmangbnNo ratings yet

- Metodo NewmarkDocument137 pagesMetodo NewmarkMateoAriasPerezNo ratings yet

- Chapter Four 4.0 Data AnalysisDocument6 pagesChapter Four 4.0 Data AnalysisSMART ROBITONo ratings yet

- Ilide - Info Aplicacion Del Metodo Smith and Ichiyen en Balance de Tesis PRDocument23 pagesIlide - Info Aplicacion Del Metodo Smith and Ichiyen en Balance de Tesis PRjhonatangenarobernuyarteagaNo ratings yet

- Table 3Document2 pagesTable 3Soumya MukhopadhyayNo ratings yet

- Jadual Waktu Pelaksanaan Rekonstruksi Jalan Sengkol - Kuta T.A 2017Document9 pagesJadual Waktu Pelaksanaan Rekonstruksi Jalan Sengkol - Kuta T.A 2017Ian MancisNo ratings yet

- ECE494 Lab 5 DiscussionDocument3 pagesECE494 Lab 5 DiscussionpanmanNo ratings yet

- FIN604 - HW 02 - 18164052 - Farhan ZubairDocument4 pagesFIN604 - HW 02 - 18164052 - Farhan ZubairZNo ratings yet

- CASO Crecimiento PlantasDocument12 pagesCASO Crecimiento PlantasCynthia Falcón FloresNo ratings yet

- Assignment 2 Solution PDFDocument15 pagesAssignment 2 Solution PDFabimalainNo ratings yet

- Saluran Bandara HitungDocument5 pagesSaluran Bandara HitungRESKI SESANo ratings yet

- Lincoln 2Document2 pagesLincoln 2kien phamNo ratings yet

- Sample Size & Portfolio in ConstructionDocument7 pagesSample Size & Portfolio in ConstructionArshad HussainNo ratings yet

- Vier Cylinders 2022Document2 pagesVier Cylinders 2022sobheysaidNo ratings yet

- Kirby South East Asia: Aisc 2005 AsdDocument3 pagesKirby South East Asia: Aisc 2005 AsdthiệnNo ratings yet

- Vanna LyDocument5 pagesVanna LynonaNo ratings yet

- Undamped Single Degree of Freedom ResponseDocument5 pagesUndamped Single Degree of Freedom ResponsenonaNo ratings yet

- X-R Chart LabDocument7 pagesX-R Chart Labarslan shahidNo ratings yet

- Repairable Non RepairableDocument33 pagesRepairable Non Repairablemobile legendNo ratings yet

- Appendix B: Correlation Tables and Dimensionless FunctionsDocument10 pagesAppendix B: Correlation Tables and Dimensionless FunctionsmisterkoroNo ratings yet

- BacktestDocument26 pagesBacktestNejma SaidiNo ratings yet

- Asme BPVC - Ii.c-2015 Sfa-5.9/sfa-5.9mDocument1 pageAsme BPVC - Ii.c-2015 Sfa-5.9/sfa-5.9mpuwarin najaNo ratings yet

- Car Parking Shade Design ReportDocument28 pagesCar Parking Shade Design Reportsiso hego100% (1)

- Newton Raphson Submission FileDocument9 pagesNewton Raphson Submission Fileshailesh upadhyayNo ratings yet

- Rubrica Rectangular Corte 2. Manuel RoblesDocument28 pagesRubrica Rectangular Corte 2. Manuel RoblesAlex Robles PimientaNo ratings yet

- Quality Assurance: QP 7.2 S03 Form 7 Capability of Measurement Processes Procedure 2 程序2 (Gauge R&R)Document20 pagesQuality Assurance: QP 7.2 S03 Form 7 Capability of Measurement Processes Procedure 2 程序2 (Gauge R&R)cong daNo ratings yet

- NETS NYPS (68 Bus System) ANAREDE PacDyn ANATEM Study ReportDocument48 pagesNETS NYPS (68 Bus System) ANAREDE PacDyn ANATEM Study Reportflywheel2006No ratings yet

- Endterm Examination (Assessment) Summer 2020 Name: - Reg #Document1 pageEndterm Examination (Assessment) Summer 2020 Name: - Reg #HassanRazaNo ratings yet

- Moody's Puts Top 5 Pakistani Banks' Ratings Under ReviewDocument2 pagesMoody's Puts Top 5 Pakistani Banks' Ratings Under ReviewHassanRazaNo ratings yet

- Descriptive Analysis: Dr. Hassan RazaDocument3 pagesDescriptive Analysis: Dr. Hassan RazaHassanRazaNo ratings yet

- Shows Significance at The .05 Level: Pairwise CorrelationsDocument2 pagesShows Significance at The .05 Level: Pairwise CorrelationsHassanRazaNo ratings yet

- Moderation Interpretation Write UpDocument2 pagesModeration Interpretation Write UpHassanRazaNo ratings yet

- Statement of Purpose To Pursue Higher StudiesDocument1 pageStatement of Purpose To Pursue Higher StudiesHassanRazaNo ratings yet

- Statistical Modeling of Extreme Values PDFDocument28 pagesStatistical Modeling of Extreme Values PDFHassanRazaNo ratings yet

- Market Microstructure TheoryDocument3 pagesMarket Microstructure TheoryHassanRazaNo ratings yet

- Cost Accounting QuestionsDocument5 pagesCost Accounting QuestionsAdilHayatNo ratings yet

- Descriptor GDP M2 TBR LR CPI Employ GFCF PC Export: Sheet1Document4 pagesDescriptor GDP M2 TBR LR CPI Employ GFCF PC Export: Sheet1HassanRazaNo ratings yet

- Divide and ConqureDocument114 pagesDivide and ConqureREENIENo ratings yet

- Third Law of ThermodynamicsDocument4 pagesThird Law of Thermodynamicsandres arizaNo ratings yet

- Advance LPDocument3 pagesAdvance LPSubrataTalapatraNo ratings yet

- Intelligent System: Lecture Notes For Chapter 7Document25 pagesIntelligent System: Lecture Notes For Chapter 7Priti YadavNo ratings yet

- Bayesian NonparametricsDocument60 pagesBayesian NonparametricsZeferinixNo ratings yet

- V. L. Balakin, A. V. DoroshinDocument69 pagesV. L. Balakin, A. V. DoroshinFiras ZekiNo ratings yet

- Group 6Document34 pagesGroup 6Naveen KumarNo ratings yet

- Indiraswari, Setiyowati - 2023 - Moderasi Financial Attitude Pada Financial Literacy Dan Risk Tolerance Terhadap Keputusan InvestasiDocument11 pagesIndiraswari, Setiyowati - 2023 - Moderasi Financial Attitude Pada Financial Literacy Dan Risk Tolerance Terhadap Keputusan Investasirizki romadhaniNo ratings yet

- Logistic Regression Using SASDocument22 pagesLogistic Regression Using SASSubhashish SarkarNo ratings yet

- MUCLecture 2021 112940914Document26 pagesMUCLecture 2021 112940914Noor FarhanNo ratings yet

- Worksheet 2.1 (1) SPSSDocument11 pagesWorksheet 2.1 (1) SPSSDoo - WopNo ratings yet

- Hardy CrossDocument13 pagesHardy CrossNeyman Ezer Zuniga RiveraNo ratings yet

- CryptographyDocument4 pagesCryptographyrajivkurjeeNo ratings yet

- Nominal and Effective InterestDocument31 pagesNominal and Effective InterestAnas OdehNo ratings yet

- Nama: Anissa Asyahra NIM: 20.05.51.0253 Mata Kulah: Manajemen Keuangan 2 Tugas Diskusi 2 Manajemen Keuangan 2 SoalDocument15 pagesNama: Anissa Asyahra NIM: 20.05.51.0253 Mata Kulah: Manajemen Keuangan 2 Tugas Diskusi 2 Manajemen Keuangan 2 SoalAnissa AsyahraNo ratings yet

- DualityDocument26 pagesDualityNavneet RaiNo ratings yet

- Amplitude Modulation Techniques in SimulinkMatlabDocument11 pagesAmplitude Modulation Techniques in SimulinkMatlabEysha qureshiNo ratings yet

- Cryptography MCQDocument4 pagesCryptography MCQShesh Narayan MishraNo ratings yet

- Association Rules FP GrowthDocument32 pagesAssociation Rules FP GrowthMuhammad TalhaNo ratings yet

- Iterative Linear EquationsDocument30 pagesIterative Linear EquationsJORGE FREJA MACIASNo ratings yet

- Btech NC 3 Sem Python Programming knc302 2022Document2 pagesBtech NC 3 Sem Python Programming knc302 2022Anushka ChaudharyNo ratings yet

- Addition and Subtraction of PolynomialsDocument23 pagesAddition and Subtraction of PolynomialsRonz de Borja100% (1)

- Mathematics: Pearson EdexcelDocument20 pagesMathematics: Pearson EdexcelHaroon Aslam100% (1)

- McdeconDocument38 pagesMcdeconAlejandro Garza JuárezNo ratings yet

- Solution To Question No. 1Document2 pagesSolution To Question No. 1Kashif NiaziNo ratings yet

- LR (0) ParsingDocument14 pagesLR (0) ParsingOmaima Musarat100% (1)

- Businessfinance12 - q3 - Mod6.1 - Basic-Long-Term-Financial-Concepts - Simple-and-Compound-InterestDocument27 pagesBusinessfinance12 - q3 - Mod6.1 - Basic-Long-Term-Financial-Concepts - Simple-and-Compound-InterestMarilyn Tamayo0% (1)

- Sofiplus 2020: Interpolation of Cross SectionsDocument2 pagesSofiplus 2020: Interpolation of Cross Sectionsnepoznati1111No ratings yet

Download as docx, pdf, or txt

You might also like

- Diffie-Hellman Key Exchange PDFDocument6 pagesDiffie-Hellman Key Exchange PDFZxzxzxz007No ratings yet

- Operations Research ProjectDocument21 pagesOperations Research ProjectDeepak KanojiaNo ratings yet

- Solutions 1Document7 pagesSolutions 1xinyichen121No ratings yet

- Programa de Lineas de InfluenciaDocument7 pagesPrograma de Lineas de Influenciajose pepe pepeNo ratings yet

- Project Write-Up v3Document19 pagesProject Write-Up v3dongn_13No ratings yet

- Análisis de Modos y FrecuenciasDocument1 pageAnálisis de Modos y FrecuenciasIsabelNo ratings yet

- SDOF Undamped Free VibrationDocument3 pagesSDOF Undamped Free VibrationMananNo ratings yet

- SDOF Undamped Free VibrationDocument3 pagesSDOF Undamped Free VibrationyadavameNo ratings yet

- Soil Consolidation TestDocument5 pagesSoil Consolidation Testsatyam agarwalNo ratings yet

- Beta Estimation Illustration PDFDocument4 pagesBeta Estimation Illustration PDFmehar noorNo ratings yet

- Lampiran 6Document6 pagesLampiran 6Ari WijayaNo ratings yet

- Date HP - Price SP500 - Price T-Bills (Adj. Close) (Adj. Close) (%, APR) Stock Return Excess Return HP Market Index HP Market IndexDocument16 pagesDate HP - Price SP500 - Price T-Bills (Adj. Close) (Adj. Close) (%, APR) Stock Return Excess Return HP Market Index HP Market IndexAlfieNo ratings yet

- Controlling Interest Rates - Bank of Russia Monetary Policy EfficiencyDocument5 pagesControlling Interest Rates - Bank of Russia Monetary Policy EfficiencyJ MNo ratings yet

- Blue Bus485 FinalDocument13 pagesBlue Bus485 FinalTamzid Ahmed AnikNo ratings yet

- Nama: Ibnu Muntaha NIM: 19108010113: RissiDocument6 pagesNama: Ibnu Muntaha NIM: 19108010113: RissiIbnu MuntahaNo ratings yet

- TH2Document2 pagesTH2phamleminh248No ratings yet

- #Information: Name: Sizwe Travor Masango Student Number: 4347545 Group 4 Title: Determning The Mass of The BubbleDocument30 pages#Information: Name: Sizwe Travor Masango Student Number: 4347545 Group 4 Title: Determning The Mass of The Bubblemehdube4No ratings yet

- Aws A5.9 - A5.9m-2017 18Document1 pageAws A5.9 - A5.9m-2017 18erick morenoNo ratings yet

- Tugas - Besar - DRAINASE - TAHAP - 2 - KORNELIS LENDEDocument4 pagesTugas - Besar - DRAINASE - TAHAP - 2 - KORNELIS LENDEKornelis LendeNo ratings yet

- Tri Ayuning Sari - 0115030035Document60 pagesTri Ayuning Sari - 0115030035bahrulNo ratings yet

- Hardy CrossDocument6 pagesHardy Crossellen jolandaNo ratings yet

- School of Civil and Chemical Engineering: B.Tech. Civil Engg CLE 2017 - Hydrology Digital AssignmentDocument1 pageSchool of Civil and Chemical Engineering: B.Tech. Civil Engg CLE 2017 - Hydrology Digital AssignmentshubhamNo ratings yet

- Datos Del Ifnorme de Fluidos CPDocument3 pagesDatos Del Ifnorme de Fluidos CPTania CervantesNo ratings yet

- Adanient X P (X) CDF Frequency Abcapital X P (X) CDF FrequencyDocument6 pagesAdanient X P (X) CDF Frequency Abcapital X P (X) CDF FrequencyrohanNo ratings yet

- Tarea 3.4 - Flores Avila.Document21 pagesTarea 3.4 - Flores Avila.Eriick De Jesús PalemónNo ratings yet

- CASO Crecimiento PlantasDocument17 pagesCASO Crecimiento PlantasGreysiNo ratings yet

- Cross HedgingDocument3 pagesCross HedgingAnupam G. RatheeNo ratings yet

- Data Mining AssignmentDocument4 pagesData Mining AssignmentMusa KhanNo ratings yet

- HelloDocument42 pagesHelloLídia EldianaNo ratings yet

- LinearityDocument4 pagesLinearityll vvNo ratings yet

- Investment Analysis and Portfolio Management: Submitted By, Amal George FK 3463 PGDM 29: FinanceDocument7 pagesInvestment Analysis and Portfolio Management: Submitted By, Amal George FK 3463 PGDM 29: FinanceAnanthasankar SNairNo ratings yet

- Number 3Document2 pagesNumber 3Mhiamar AbelladaNo ratings yet

- MMult Function and Demo of ROIDocument6 pagesMMult Function and Demo of ROIJITESHNo ratings yet

- Simulation Final ProjectDocument10 pagesSimulation Final ProjectSalman SheikhNo ratings yet

- CCATDocument19 pagesCCATgemmangbnNo ratings yet

- Metodo NewmarkDocument137 pagesMetodo NewmarkMateoAriasPerezNo ratings yet

- Chapter Four 4.0 Data AnalysisDocument6 pagesChapter Four 4.0 Data AnalysisSMART ROBITONo ratings yet

- Ilide - Info Aplicacion Del Metodo Smith and Ichiyen en Balance de Tesis PRDocument23 pagesIlide - Info Aplicacion Del Metodo Smith and Ichiyen en Balance de Tesis PRjhonatangenarobernuyarteagaNo ratings yet

- Table 3Document2 pagesTable 3Soumya MukhopadhyayNo ratings yet

- Jadual Waktu Pelaksanaan Rekonstruksi Jalan Sengkol - Kuta T.A 2017Document9 pagesJadual Waktu Pelaksanaan Rekonstruksi Jalan Sengkol - Kuta T.A 2017Ian MancisNo ratings yet

- ECE494 Lab 5 DiscussionDocument3 pagesECE494 Lab 5 DiscussionpanmanNo ratings yet

- FIN604 - HW 02 - 18164052 - Farhan ZubairDocument4 pagesFIN604 - HW 02 - 18164052 - Farhan ZubairZNo ratings yet

- CASO Crecimiento PlantasDocument12 pagesCASO Crecimiento PlantasCynthia Falcón FloresNo ratings yet

- Assignment 2 Solution PDFDocument15 pagesAssignment 2 Solution PDFabimalainNo ratings yet

- Saluran Bandara HitungDocument5 pagesSaluran Bandara HitungRESKI SESANo ratings yet

- Lincoln 2Document2 pagesLincoln 2kien phamNo ratings yet

- Sample Size & Portfolio in ConstructionDocument7 pagesSample Size & Portfolio in ConstructionArshad HussainNo ratings yet

- Vier Cylinders 2022Document2 pagesVier Cylinders 2022sobheysaidNo ratings yet

- Kirby South East Asia: Aisc 2005 AsdDocument3 pagesKirby South East Asia: Aisc 2005 AsdthiệnNo ratings yet

- Vanna LyDocument5 pagesVanna LynonaNo ratings yet

- Undamped Single Degree of Freedom ResponseDocument5 pagesUndamped Single Degree of Freedom ResponsenonaNo ratings yet

- X-R Chart LabDocument7 pagesX-R Chart Labarslan shahidNo ratings yet

- Repairable Non RepairableDocument33 pagesRepairable Non Repairablemobile legendNo ratings yet

- Appendix B: Correlation Tables and Dimensionless FunctionsDocument10 pagesAppendix B: Correlation Tables and Dimensionless FunctionsmisterkoroNo ratings yet

- BacktestDocument26 pagesBacktestNejma SaidiNo ratings yet

- Asme BPVC - Ii.c-2015 Sfa-5.9/sfa-5.9mDocument1 pageAsme BPVC - Ii.c-2015 Sfa-5.9/sfa-5.9mpuwarin najaNo ratings yet

- Car Parking Shade Design ReportDocument28 pagesCar Parking Shade Design Reportsiso hego100% (1)

- Newton Raphson Submission FileDocument9 pagesNewton Raphson Submission Fileshailesh upadhyayNo ratings yet

- Rubrica Rectangular Corte 2. Manuel RoblesDocument28 pagesRubrica Rectangular Corte 2. Manuel RoblesAlex Robles PimientaNo ratings yet

- Quality Assurance: QP 7.2 S03 Form 7 Capability of Measurement Processes Procedure 2 程序2 (Gauge R&R)Document20 pagesQuality Assurance: QP 7.2 S03 Form 7 Capability of Measurement Processes Procedure 2 程序2 (Gauge R&R)cong daNo ratings yet

- NETS NYPS (68 Bus System) ANAREDE PacDyn ANATEM Study ReportDocument48 pagesNETS NYPS (68 Bus System) ANAREDE PacDyn ANATEM Study Reportflywheel2006No ratings yet

- Endterm Examination (Assessment) Summer 2020 Name: - Reg #Document1 pageEndterm Examination (Assessment) Summer 2020 Name: - Reg #HassanRazaNo ratings yet

- Moody's Puts Top 5 Pakistani Banks' Ratings Under ReviewDocument2 pagesMoody's Puts Top 5 Pakistani Banks' Ratings Under ReviewHassanRazaNo ratings yet

- Descriptive Analysis: Dr. Hassan RazaDocument3 pagesDescriptive Analysis: Dr. Hassan RazaHassanRazaNo ratings yet

- Shows Significance at The .05 Level: Pairwise CorrelationsDocument2 pagesShows Significance at The .05 Level: Pairwise CorrelationsHassanRazaNo ratings yet

- Moderation Interpretation Write UpDocument2 pagesModeration Interpretation Write UpHassanRazaNo ratings yet

- Statement of Purpose To Pursue Higher StudiesDocument1 pageStatement of Purpose To Pursue Higher StudiesHassanRazaNo ratings yet

- Statistical Modeling of Extreme Values PDFDocument28 pagesStatistical Modeling of Extreme Values PDFHassanRazaNo ratings yet

- Market Microstructure TheoryDocument3 pagesMarket Microstructure TheoryHassanRazaNo ratings yet

- Cost Accounting QuestionsDocument5 pagesCost Accounting QuestionsAdilHayatNo ratings yet

- Descriptor GDP M2 TBR LR CPI Employ GFCF PC Export: Sheet1Document4 pagesDescriptor GDP M2 TBR LR CPI Employ GFCF PC Export: Sheet1HassanRazaNo ratings yet

- Divide and ConqureDocument114 pagesDivide and ConqureREENIENo ratings yet

- Third Law of ThermodynamicsDocument4 pagesThird Law of Thermodynamicsandres arizaNo ratings yet

- Advance LPDocument3 pagesAdvance LPSubrataTalapatraNo ratings yet

- Intelligent System: Lecture Notes For Chapter 7Document25 pagesIntelligent System: Lecture Notes For Chapter 7Priti YadavNo ratings yet

- Bayesian NonparametricsDocument60 pagesBayesian NonparametricsZeferinixNo ratings yet

- V. L. Balakin, A. V. DoroshinDocument69 pagesV. L. Balakin, A. V. DoroshinFiras ZekiNo ratings yet

- Group 6Document34 pagesGroup 6Naveen KumarNo ratings yet

- Indiraswari, Setiyowati - 2023 - Moderasi Financial Attitude Pada Financial Literacy Dan Risk Tolerance Terhadap Keputusan InvestasiDocument11 pagesIndiraswari, Setiyowati - 2023 - Moderasi Financial Attitude Pada Financial Literacy Dan Risk Tolerance Terhadap Keputusan Investasirizki romadhaniNo ratings yet

- Logistic Regression Using SASDocument22 pagesLogistic Regression Using SASSubhashish SarkarNo ratings yet

- MUCLecture 2021 112940914Document26 pagesMUCLecture 2021 112940914Noor FarhanNo ratings yet

- Worksheet 2.1 (1) SPSSDocument11 pagesWorksheet 2.1 (1) SPSSDoo - WopNo ratings yet

- Hardy CrossDocument13 pagesHardy CrossNeyman Ezer Zuniga RiveraNo ratings yet

- CryptographyDocument4 pagesCryptographyrajivkurjeeNo ratings yet

- Nominal and Effective InterestDocument31 pagesNominal and Effective InterestAnas OdehNo ratings yet

- Nama: Anissa Asyahra NIM: 20.05.51.0253 Mata Kulah: Manajemen Keuangan 2 Tugas Diskusi 2 Manajemen Keuangan 2 SoalDocument15 pagesNama: Anissa Asyahra NIM: 20.05.51.0253 Mata Kulah: Manajemen Keuangan 2 Tugas Diskusi 2 Manajemen Keuangan 2 SoalAnissa AsyahraNo ratings yet

- DualityDocument26 pagesDualityNavneet RaiNo ratings yet

- Amplitude Modulation Techniques in SimulinkMatlabDocument11 pagesAmplitude Modulation Techniques in SimulinkMatlabEysha qureshiNo ratings yet

- Cryptography MCQDocument4 pagesCryptography MCQShesh Narayan MishraNo ratings yet

- Association Rules FP GrowthDocument32 pagesAssociation Rules FP GrowthMuhammad TalhaNo ratings yet

- Iterative Linear EquationsDocument30 pagesIterative Linear EquationsJORGE FREJA MACIASNo ratings yet

- Btech NC 3 Sem Python Programming knc302 2022Document2 pagesBtech NC 3 Sem Python Programming knc302 2022Anushka ChaudharyNo ratings yet

- Addition and Subtraction of PolynomialsDocument23 pagesAddition and Subtraction of PolynomialsRonz de Borja100% (1)

- Mathematics: Pearson EdexcelDocument20 pagesMathematics: Pearson EdexcelHaroon Aslam100% (1)

- McdeconDocument38 pagesMcdeconAlejandro Garza JuárezNo ratings yet

- Solution To Question No. 1Document2 pagesSolution To Question No. 1Kashif NiaziNo ratings yet

- LR (0) ParsingDocument14 pagesLR (0) ParsingOmaima Musarat100% (1)

- Businessfinance12 - q3 - Mod6.1 - Basic-Long-Term-Financial-Concepts - Simple-and-Compound-InterestDocument27 pagesBusinessfinance12 - q3 - Mod6.1 - Basic-Long-Term-Financial-Concepts - Simple-and-Compound-InterestMarilyn Tamayo0% (1)

- Sofiplus 2020: Interpolation of Cross SectionsDocument2 pagesSofiplus 2020: Interpolation of Cross Sectionsnepoznati1111No ratings yet