Download as docx, pdf, or txt

You might also like

- Gitman Chapter 3 SolutionDocument21 pagesGitman Chapter 3 SolutionNauman Iqbal75% (4)

- New HR Strategy Makes Lloyd's A "Best Company"Document4 pagesNew HR Strategy Makes Lloyd's A "Best Company"Rob3332No ratings yet

- Confined Spaces: Job Safety AnalysisDocument2 pagesConfined Spaces: Job Safety Analysismalimsaidi_160040895No ratings yet

- Anne Aylor, Inc.: Determination of Planning Materiality and Tolerable MisstatementDocument14 pagesAnne Aylor, Inc.: Determination of Planning Materiality and Tolerable MisstatementAlrac GarciaNo ratings yet

- Final Assessment S1, 2021Document5 pagesFinal Assessment S1, 2021Dilrukshi Wanasinghe100% (1)

- Case Study Week 5 AnswerDocument8 pagesCase Study Week 5 AnswerAlrac GarciaNo ratings yet

- Citibank CFO PresentationDocument29 pagesCitibank CFO PresentationDiego de AragãoNo ratings yet

- Larsen and Toubro FRA AssignmentDocument11 pagesLarsen and Toubro FRA AssignmentZenish KhumujamNo ratings yet

- List of Key Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Profitability Ratios and the Other Most Important Financial RatiosFrom EverandList of Key Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Profitability Ratios and the Other Most Important Financial RatiosNo ratings yet

- GQ Magazine August 2011Document2 pagesGQ Magazine August 2011RamkumarNo ratings yet

- Gujarat State Petronet LimitedDocument13 pagesGujarat State Petronet LimitedAmrita Rao Bhatt100% (1)

- 234invuf AnnualReport2021-22Document169 pages234invuf AnnualReport2021-22Pathan IkhlaqueNo ratings yet

- BEGA ELECTROMOTOR SA Financial Condition Analysis PDFDocument16 pagesBEGA ELECTROMOTOR SA Financial Condition Analysis PDFVirgo AeliusNo ratings yet

- ACC314 Business Finance Management Resit Answers (SEPT) R 19-20Document8 pagesACC314 Business Finance Management Resit Answers (SEPT) R 19-20Rukshani RefaiNo ratings yet

- Main Project - Accounting and Finance - Jan2023Document5 pagesMain Project - Accounting and Finance - Jan2023Farai BlessedWithout Measure MukamuraNo ratings yet

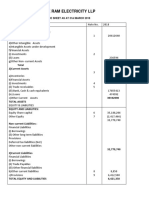

- Shree Ram Electricity LLP: 1) Non-Current AssetsDocument5 pagesShree Ram Electricity LLP: 1) Non-Current AssetsSaba MullaNo ratings yet

- Basel Ii and Its ImplicationsDocument24 pagesBasel Ii and Its ImplicationsMon SethNo ratings yet

- F2 Sept 2013 QPDocument20 pagesF2 Sept 2013 QPFahadNo ratings yet

- AUDIT PROCESS SolutionsDocument21 pagesAUDIT PROCESS SolutionsTazlyn MarillierNo ratings yet

- Corporate GovernanceDocument19 pagesCorporate GovernancehNo ratings yet

- CSG Ar 2018 enDocument452 pagesCSG Ar 2018 enHaitham FathiNo ratings yet

- Review On Financial Standing of Saiddi AgriDocument3 pagesReview On Financial Standing of Saiddi AgriBilling ZamboecozoneNo ratings yet

- 2020 GR 10 Revision Activities Final ENGeDocument21 pages2020 GR 10 Revision Activities Final ENGeAmahle NgidiNo ratings yet

- Midsem Exams Fin Accting WeekendDocument4 pagesMidsem Exams Fin Accting WeekendMichael LastNo ratings yet

- S5. Accounting AnalysisDocument18 pagesS5. Accounting AnalysisJoão Maria VigárioNo ratings yet

- Royal Dutch Shell PLCDocument20 pagesRoyal Dutch Shell PLCstefan.kovar.financeNo ratings yet

- Financial Analysis - HomeworkDocument7 pagesFinancial Analysis - HomeworkTuan Anh LeeNo ratings yet

- Assessment-3b-2 (1) (AutoRecovered)Document6 pagesAssessment-3b-2 (1) (AutoRecovered)Trúc NguyễnNo ratings yet

- Tutorial 6 On RatiosDocument6 pagesTutorial 6 On RatiosKrrish BosamiaNo ratings yet

- 2020 July 301 Financial Reporting enDocument16 pages2020 July 301 Financial Reporting enimabrar190No ratings yet

- Assignment Gilbert LumbertDocument6 pagesAssignment Gilbert LumbertHenri De sloovereNo ratings yet

- Case 4 Written Report - Third DraftDocument5 pagesCase 4 Written Report - Third DraftMarc MoralesNo ratings yet

- Financial Anaylsis 1Document27 pagesFinancial Anaylsis 1Nitika DhatwaliaNo ratings yet

- Project 2Document8 pagesProject 2krinilu802No ratings yet

- 2 Ratio Analysis Financial Statement Analysis 1652097843303Document8 pages2 Ratio Analysis Financial Statement Analysis 1652097843303vroommNo ratings yet

- Can Press Release Jun 2008Document5 pagesCan Press Release Jun 2008pranav5950No ratings yet

- Solutions - Chapter 8Document16 pagesSolutions - Chapter 8Dre ThathipNo ratings yet

- Touch StoneDocument45 pagesTouch StoneSubba RamaNo ratings yet

- SM CHDocument53 pagesSM CHInderjeet JeedNo ratings yet

- Project Profile ON: Baby Feeding BottlesDocument6 pagesProject Profile ON: Baby Feeding BottlesRekha KuttappanNo ratings yet

- Goldstar Example of Ratio AnalysisDocument13 pagesGoldstar Example of Ratio AnalysisRoshan SomaruNo ratings yet

- L&T Press Release: Performance For The Quarter Ended March 31, 2012Document6 pagesL&T Press Release: Performance For The Quarter Ended March 31, 2012blazegloryNo ratings yet

- San Narciso Executive Summary 2012Document4 pagesSan Narciso Executive Summary 2012Janedel ValderamaNo ratings yet

- FXCM Q3 Slide DeckDocument20 pagesFXCM Q3 Slide DeckRon FinbergNo ratings yet

- Intern Hiring Process TGP 2024 - Management ControlDocument9 pagesIntern Hiring Process TGP 2024 - Management Controlra.manriquedNo ratings yet

- Financial Feasibility Study For Investment Projects Case 2: The NCF and The Pay-Back Period of Project PE1 of CUCODocument3 pagesFinancial Feasibility Study For Investment Projects Case 2: The NCF and The Pay-Back Period of Project PE1 of CUCOMariam YasserNo ratings yet

- Basic Energy Corporation SEC Form 17 A April172023Document245 pagesBasic Energy Corporation SEC Form 17 A April172023SSGNo ratings yet

- Chapter 5Document56 pagesChapter 5yedinkachaw shferawNo ratings yet

- Lebanese Association of Certified Public Accountants KEY - IFRS February Exam 2020 - Extra SessionDocument6 pagesLebanese Association of Certified Public Accountants KEY - IFRS February Exam 2020 - Extra Sessionjad NasserNo ratings yet

- FRPA-Supple-2-QP - FINALDocument3 pagesFRPA-Supple-2-QP - FINALSenthil KumarNo ratings yet

- Alkali Metals Limited - R - 26112020Document7 pagesAlkali Metals Limited - R - 26112020Yogi173No ratings yet

- Project Financial Accounting For Managers Company: Godfrey Phillips India LimitedDocument8 pagesProject Financial Accounting For Managers Company: Godfrey Phillips India LimitedSOURAV ACHARJEENo ratings yet

- Lesson 9 - Analysis of Financial StatementDocument26 pagesLesson 9 - Analysis of Financial StatementJannah FrancineNo ratings yet

- Prashanth VivaDocument22 pagesPrashanth Vivabest video of every timeNo ratings yet

- Online Presentation 11-1-11Document18 pagesOnline Presentation 11-1-11Hari HaranNo ratings yet

- San Vicente Executive Summary 2012Document6 pagesSan Vicente Executive Summary 2012Maria CharessaNo ratings yet

- GenSantosCity SoCot ES2015Document5 pagesGenSantosCity SoCot ES2015J JaNo ratings yet

- Makerere University Business School Jinja CampusDocument54 pagesMakerere University Business School Jinja CampusIanNo ratings yet

- Practice QuestionsDocument10 pagesPractice QuestionsDana El SakkaNo ratings yet

- GP FINNANCEDocument12 pagesGP FINNANCEMuhammad Aiezaqul Haikal bin ZainuriNo ratings yet

- Performance Highlights: NeutralDocument11 pagesPerformance Highlights: NeutralAngel BrokingNo ratings yet

- Moody's Adjustments To Vattenfall's Accounts: ObjectiveDocument4 pagesMoody's Adjustments To Vattenfall's Accounts: ObjectiveSunny VohraNo ratings yet

- List of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosFrom EverandList of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosNo ratings yet

- Brief History of The Systems Approach PrincipleDocument2 pagesBrief History of The Systems Approach PrincipleVladuț KistrugaNo ratings yet

- The Key Ideas of The Quantitative and Cybernetic Approaches To International Management. Quantitative ApproachDocument2 pagesThe Key Ideas of The Quantitative and Cybernetic Approaches To International Management. Quantitative ApproachVladuț KistrugaNo ratings yet

- Essay Title: Common Agrliculture Policy Problems and BenefitsDocument5 pagesEssay Title: Common Agrliculture Policy Problems and BenefitsVladuț KistrugaNo ratings yet

- Common Agrliculture Policy Problems and BenefitsDocument4 pagesCommon Agrliculture Policy Problems and BenefitsVladuț KistrugaNo ratings yet

- Презентация Microsoft PowerPointDocument7 pagesПрезентация Microsoft PowerPointVladuț KistrugaNo ratings yet

- Презентация Microsoft PowerPointDocument7 pagesПрезентация Microsoft PowerPointVladuț KistrugaNo ratings yet

- Презентация Microsoft PowerPointDocument7 pagesПрезентация Microsoft PowerPointVladuț KistrugaNo ratings yet

- Classification of MenusDocument12 pagesClassification of Menusliewin langiNo ratings yet

- Risk and Return Analysis of Selected: October 2018Document5 pagesRisk and Return Analysis of Selected: October 2018BHARATHITHASAN S 20PHD0413No ratings yet

- Adobe Scan 8 Nov 2021Document10 pagesAdobe Scan 8 Nov 2021AstarothNo ratings yet

- Liderazgo en Enfermería y Burnout (Pucheu, 2010)Document8 pagesLiderazgo en Enfermería y Burnout (Pucheu, 2010)Carolina Oyarzún PérezNo ratings yet

- Energy Conversions Se GizmoDocument4 pagesEnergy Conversions Se Gizmoapi-279264664No ratings yet

- Indian Society (Unit-3)Document37 pagesIndian Society (Unit-3)Debadutta NayakNo ratings yet

- AWS Real Exam QuestionsDocument6 pagesAWS Real Exam Questionslolo100% (1)

- Data Engineer - Insightin Technology BangladeshDocument6 pagesData Engineer - Insightin Technology BangladeshJahidul IslamNo ratings yet

- LIT 1 Module 3Document14 pagesLIT 1 Module 3ALL ABOUT PAGEANTARYNo ratings yet

- Template Business PlanDocument12 pagesTemplate Business PlanReghie SantosNo ratings yet

- Rosenthal Decorating Inc Is A Commercial Painting and Decorating ContractorDocument1 pageRosenthal Decorating Inc Is A Commercial Painting and Decorating ContractorFreelance WorkerNo ratings yet

- NO. Course's NameDocument33 pagesNO. Course's NameBillionaireka0% (1)

- NHAI Safety Manual PDFDocument239 pagesNHAI Safety Manual PDFgk_kishoree8167% (3)

- NBD AuthorityDocument23 pagesNBD Authoritysharpshooter0999100% (1)

- Essential Teacher TESOLDocument68 pagesEssential Teacher TESOLAlifFajriNo ratings yet

- CNR Company ProfileDocument6 pagesCNR Company ProfilejhonNo ratings yet

- RK13AR12ING01PTS 5904717eDocument2 pagesRK13AR12ING01PTS 5904717epatma siswantiNo ratings yet

- London College of Legal Studies (South)Document3 pagesLondon College of Legal Studies (South)Saadat Bin SiddiqueNo ratings yet

- Bodies and Gender: Understanding Biological Sex As Continuum, Not A Dichotomy of Male and FemaleDocument13 pagesBodies and Gender: Understanding Biological Sex As Continuum, Not A Dichotomy of Male and FemaleRosalie AlitaoNo ratings yet

- Nilai Syair Sayed Idrus Bin Salim Aljufri (Guru Tua) Dan Implikasinya Pada Pendidikan KarakterDocument11 pagesNilai Syair Sayed Idrus Bin Salim Aljufri (Guru Tua) Dan Implikasinya Pada Pendidikan KarakterMuhammad ArmansyahNo ratings yet

- Case Investigation of Natuzza EvoloDocument13 pagesCase Investigation of Natuzza EvoloMichael Nanko100% (2)

- Trik Memeras SusuDocument80 pagesTrik Memeras SusuM.a safarNo ratings yet

- Belief in Divine Decree in IslamDocument2 pagesBelief in Divine Decree in IslamahmadnaiemNo ratings yet

- Test 1 For Unit 6Document3 pagesTest 1 For Unit 6Hang TruongNo ratings yet

- Term-Ii Summary and Important Questions For Revision Class - Ix PackingDocument9 pagesTerm-Ii Summary and Important Questions For Revision Class - Ix PackingAditya NarayanNo ratings yet

- Churton T. - The Gnostics PDFDocument217 pagesChurton T. - The Gnostics PDFmoalvey7128100% (5)

- Initial Conversation Scripts by Tanya AlizaDocument6 pagesInitial Conversation Scripts by Tanya AlizaIan Salazar100% (1)