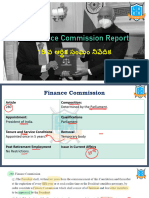

The Finance Commission

The Finance Commission

You might also like

- Back Plan View: Thunderbird ModelDocument1 pageBack Plan View: Thunderbird ModelSEBASSNo ratings yet

- The Seven Pillars of Church Rev - Tom CheyneyDocument87 pagesThe Seven Pillars of Church Rev - Tom CheyneyEmanuel100% (1)

- 15TH Finance CommissionDocument32 pages15TH Finance CommissionSunaina SukumarNo ratings yet

- Current Events 66 BPSCDocument137 pagesCurrent Events 66 BPSCpifaj90517No ratings yet

- 15th Finance Commission RecommendationsDocument4 pages15th Finance Commission RecommendationsVaibhavNo ratings yet

- 14th Finance Commission PDFDocument5 pages14th Finance Commission PDFSudha PandeyNo ratings yet

- 14th Finance Commission VISION IASDocument14 pages14th Finance Commission VISION IASimranNo ratings yet

- 15th Finance Commission: Anuj JindalDocument17 pages15th Finance Commission: Anuj JindalamritNo ratings yet

- 15th Finance Commission ReportDocument26 pages15th Finance Commission ReportLeela KalyaniNo ratings yet

- Lecture 27Document6 pagesLecture 27Vvanshika SinghalNo ratings yet

- Federation, Japan, and Canada. These Data Include CODocument16 pagesFederation, Japan, and Canada. These Data Include COSaif EqbalNo ratings yet

- Deficit Fundamentalism Vs Fiscal Federalism Implications of 13th Finance Commissions RecommendationsDocument8 pagesDeficit Fundamentalism Vs Fiscal Federalism Implications of 13th Finance Commissions RecommendationsShay WaxenNo ratings yet

- FINAL WRITTEN Econ PrsentationDocument4 pagesFINAL WRITTEN Econ PrsentationharrishNo ratings yet

- 15th Finance Commission ReportDocument10 pages15th Finance Commission ReportSaurabh SinghNo ratings yet

- Central Transfers To States: Role of The Finance CommissionDocument2 pagesCentral Transfers To States: Role of The Finance CommissionvikramNo ratings yet

- Fiscal FederalismDocument11 pagesFiscal FederalismPark Seo YoonNo ratings yet

- 15th Finance Commission Upsc Notes 95Document4 pages15th Finance Commission Upsc Notes 95ArshaanNo ratings yet

- Federal FinanceDocument28 pagesFederal Financeadip67436No ratings yet

- 15th Fifteenth Finance CommisionDocument76 pages15th Fifteenth Finance CommisionJaved StylesNo ratings yet

- 14th Finance Commission - Report Summary PDFDocument1 page14th Finance Commission - Report Summary PDFSourav MeenaNo ratings yet

- Fiscal FederalismDocument19 pagesFiscal FederalismPark Seo YoonNo ratings yet

- States' Share in Central Taxes: ISSN (ONLINE) : 2250-0758, ISSN (PRINT) : 2394-6962Document9 pagesStates' Share in Central Taxes: ISSN (ONLINE) : 2250-0758, ISSN (PRINT) : 2394-6962SujayaNo ratings yet

- 15 TH Finance ComissionDocument3 pages15 TH Finance ComissionAnmol RatanNo ratings yet

- PUBLIC, UNIT 2C, Summary of Finance Commission ReportDocument4 pagesPUBLIC, UNIT 2C, Summary of Finance Commission Reportridhijain0102No ratings yet

- PRS Report Summary of 15th Finance Commission For FY 2020-21Document4 pagesPRS Report Summary of 15th Finance Commission For FY 2020-21mansavi bihaniNo ratings yet

- Financial Forecasting in The Budget Preparation ProcessDocument7 pagesFinancial Forecasting in The Budget Preparation Processnmsusarla888No ratings yet

- 15 FC PPT in PDF-2Document40 pages15 FC PPT in PDF-2Ashish SaikiaNo ratings yet

- Fiscal Planning and The New Maintenance of Effort Law: Companion Document For Council PresentationDocument39 pagesFiscal Planning and The New Maintenance of Effort Law: Companion Document For Council PresentationParents' Coalition of Montgomery County, MarylandNo ratings yet

- 5 - Chapter 5 - Financial Plan - FINALDocument22 pages5 - Chapter 5 - Financial Plan - FINALnickmorara4No ratings yet

- February 2021 24Document1 pageFebruary 2021 24Raghav SharmaNo ratings yet

- State-Ordered Report Completed by PFM GroupDocument26 pagesState-Ordered Report Completed by PFM GroupAnonymous L5EiMKJ50% (2)

- 16th Finance CommissionDocument4 pages16th Finance CommissionSanthosh KumarNo ratings yet

- 14th Finance CommissionDocument6 pages14th Finance CommissionPartha SurveNo ratings yet

- 14th Finance Commission PDFDocument6 pages14th Finance Commission PDFRavu ArunNo ratings yet

- CFC - SFCDocument22 pagesCFC - SFCAuna SandoNo ratings yet

- Ijsrmjournal, Journal Manager, 30 IjsrmDocument9 pagesIjsrmjournal, Journal Manager, 30 IjsrmZahidNo ratings yet

- 15th Finance CommissionDocument6 pages15th Finance CommissionSingh JagdishNo ratings yet

- Fiscal Federalism in IndiaDocument32 pagesFiscal Federalism in IndiaZaisha KhanNo ratings yet

- Fiscal Policy 1-Resource Mobilization TaxationDocument22 pagesFiscal Policy 1-Resource Mobilization TaxationumairzafarNo ratings yet

- 016 SD 01Document17 pages016 SD 01JOSE EPHRAIM MAGLAQUENo ratings yet

- Rbi Report On Finances of PanchayatsDocument8 pagesRbi Report On Finances of PanchayatsSKNo ratings yet

- Punjab: 604.2 Billion USD Sindh: 291.5 Billion USD KPK: 85 Billion USD Balochistan: 32 Billion USDDocument4 pagesPunjab: 604.2 Billion USD Sindh: 291.5 Billion USD KPK: 85 Billion USD Balochistan: 32 Billion USDzakria yahyaNo ratings yet

- Grant Thornton Report - Local Government A Financial SnapshotDocument22 pagesGrant Thornton Report - Local Government A Financial SnapshotNew Zealand Taxpayers' UnionNo ratings yet

- Issues and Challenges For The 14Th Finance Commission: Career in GeophysicsDocument2 pagesIssues and Challenges For The 14Th Finance Commission: Career in GeophysicsCandyCrüshSagaNo ratings yet

- Economics ProjectDocument10 pagesEconomics ProjectbhavikNo ratings yet

- Commission Shall Use The Population Data of 2011 While Making Its RecommendationsDocument2 pagesCommission Shall Use The Population Data of 2011 While Making Its RecommendationsTajNo ratings yet

- Darshini Gayithri 2023 An Econometric Analysis of Revenue Diversification Among Selected Indian StatesDocument23 pagesDarshini Gayithri 2023 An Econometric Analysis of Revenue Diversification Among Selected Indian StatessushilNo ratings yet

- BVCSD Statler Report Final BVCSD Five Year Fiscal Forecast 2-11-13-1Document31 pagesBVCSD Statler Report Final BVCSD Five Year Fiscal Forecast 2-11-13-1Faith GreenNo ratings yet

- Media Statement - How Much It Costs To Run County Governments - Final FinalDocument2 pagesMedia Statement - How Much It Costs To Run County Governments - Final FinalInternational Budget Partnership KenyaNo ratings yet

- Analysis of Municipality TernateDocument14 pagesAnalysis of Municipality TernateSuleman S Al-QalbyNo ratings yet

- Kitchener 2013 Budget Preview Nov 5 2012Document52 pagesKitchener 2013 Budget Preview Nov 5 2012WR_RecordNo ratings yet

- Acct 260 Cafr 3-15Document6 pagesAcct 260 Cafr 3-15StephanieNo ratings yet

- Beyond Every Child Matters: Local Area Agreements and Your OutcomesDocument14 pagesBeyond Every Child Matters: Local Area Agreements and Your OutcomesodalindNo ratings yet

- State Comptroller's Audit of The The Hendrick Hudson School District's Financial ConditionDocument11 pagesState Comptroller's Audit of The The Hendrick Hudson School District's Financial ConditionCara MatthewsNo ratings yet

- 201002ThematicPaper LocalServiceDelivery FinalDocument39 pages201002ThematicPaper LocalServiceDelivery FinalLham DorjiNo ratings yet

- Gadgil FormulaDocument6 pagesGadgil FormulaHemant ShivakumarNo ratings yet

- Chapter-Iv An Analysis of The Recommendations of Recent Finance Commissions of India A Descriptive TreatiseDocument18 pagesChapter-Iv An Analysis of The Recommendations of Recent Finance Commissions of India A Descriptive TreatiseRaja SimmanNo ratings yet

- Highlights 14thfinance Commission Report PDFDocument2 pagesHighlights 14thfinance Commission Report PDFtanyaa90No ratings yet

- 15th Finance CommissionDocument20 pages15th Finance CommissiontqncsqnsvoqzulkeaaNo ratings yet

- Dutchess County AuditDocument15 pagesDutchess County AuditDaily FreemanNo ratings yet

- Report Summary: Report of The 15 Finance Commission For FY 2020-21Document4 pagesReport Summary: Report of The 15 Finance Commission For FY 2020-21Adithya Sharma SalagramNo ratings yet

- Local Public Finance Management in the People's Republic of China: Challenges and OpportunitiesFrom EverandLocal Public Finance Management in the People's Republic of China: Challenges and OpportunitiesNo ratings yet

- Scanned With CamscannerDocument8 pagesScanned With Camscannershivam kumarNo ratings yet

- Custom Search: Law Articles - India's Most Authentice Free Legal Source OnlineDocument4 pagesCustom Search: Law Articles - India's Most Authentice Free Legal Source Onlineshivam kumarNo ratings yet

- Trips and TrimsDocument2 pagesTrips and Trimsshivam kumarNo ratings yet

- History ProjectDocument9 pagesHistory Projectshivam kumarNo ratings yet

- Indian Democracy - Role of Election CommDocument84 pagesIndian Democracy - Role of Election Commshivam kumarNo ratings yet

- 10 Eng ExerDocument17 pages10 Eng ExerGuruNo ratings yet

- Environmental Governance Programme (EGP)Document2 pagesEnvironmental Governance Programme (EGP)Francisco SilvaNo ratings yet

- Dentate PDIDocument5 pagesDentate PDIkelompok cNo ratings yet

- Vocab 8b Cee - b1 - RB - TB - A19 - Resource-16Document1 pageVocab 8b Cee - b1 - RB - TB - A19 - Resource-16Freddy Flores VilcaNo ratings yet

- Assignment N° 1: Connected Speech: Assimilation-Coalescence - Elision - LiaisonDocument5 pagesAssignment N° 1: Connected Speech: Assimilation-Coalescence - Elision - LiaisonRoxana AguirreNo ratings yet

- Analisis Preferensi Konsumen Terhadap Bu Dfe22138Document6 pagesAnalisis Preferensi Konsumen Terhadap Bu Dfe22138CERITA SEROJANo ratings yet

- Ching V DigestDocument2 pagesChing V DigestAthena Venice MercadoNo ratings yet

- Directions:: Criteria 5 4 2 1Document3 pagesDirections:: Criteria 5 4 2 1Ha KDOGNo ratings yet

- محاضره 1 انسجهDocument32 pagesمحاضره 1 انسجهYahya Daham Zafeer SakhrNo ratings yet

- James Cameron - Original Screenplay For AvatarDocument152 pagesJames Cameron - Original Screenplay For AvatarAngelSuicide67% (3)

- Negro y AzulDocument3 pagesNegro y AzulDado TopicNo ratings yet

- GCSE MATH Past Papers Mark Schemes Standard MayJune Series 2013 12709Document6 pagesGCSE MATH Past Papers Mark Schemes Standard MayJune Series 2013 12709Назар ГущікNo ratings yet

- DATA6211 EaDocument9 pagesDATA6211 Eanzfpbte564No ratings yet

- An Introduction of Computer Programming - g10Document20 pagesAn Introduction of Computer Programming - g10zimran dave epelipciaNo ratings yet

- Hoover vs. FDR: Reactions To The Great DepressionDocument3 pagesHoover vs. FDR: Reactions To The Great Depressionirregularflowers100% (1)

- 2 - PrimusLine - flyer-water-GBDocument4 pages2 - PrimusLine - flyer-water-GBzeroicesnowNo ratings yet

- WFWEDocument30 pagesWFWEEstiven Gier50% (4)

- Trust PATDocument211 pagesTrust PATfergieNo ratings yet

- Radio IsotopesDocument10 pagesRadio IsotopesPG ChemistryNo ratings yet

- FemaleAccountant 1 To 271 14 02 2020Document67 pagesFemaleAccountant 1 To 271 14 02 2020Stigan India100% (1)

- Reading and Math Online Resources - 2017-18Document3 pagesReading and Math Online Resources - 2017-18api-32237090No ratings yet

- History of Fashion - Indus VallyDocument3 pagesHistory of Fashion - Indus VallyShAiShahNo ratings yet

- Persuasive Speech Analysis InstructionsDocument2 pagesPersuasive Speech Analysis Instructionsapi-552410496No ratings yet

- PHD Thesis Dahle PDFDocument190 pagesPHD Thesis Dahle PDFJessNo ratings yet

- Arroyo Vs YuDocument4 pagesArroyo Vs YuAlean Fueconcillo-EvangelistaNo ratings yet

- Shear Connections Notes: (1) The Beams Considered With Coped ConditionDocument9 pagesShear Connections Notes: (1) The Beams Considered With Coped ConditionSrikanth SikhaNo ratings yet

- Henry Schein Orthodontics Catalog - General SuppliesDocument8 pagesHenry Schein Orthodontics Catalog - General SuppliesOrtho OrganizersNo ratings yet

- Sustainable Biodegradable Solutions Reshaping The Food Packaging IndustryDocument65 pagesSustainable Biodegradable Solutions Reshaping The Food Packaging Industrypot poteNo ratings yet

Download as docx, pdf, or txt

You might also like

- Back Plan View: Thunderbird ModelDocument1 pageBack Plan View: Thunderbird ModelSEBASSNo ratings yet

- The Seven Pillars of Church Rev - Tom CheyneyDocument87 pagesThe Seven Pillars of Church Rev - Tom CheyneyEmanuel100% (1)

- 15TH Finance CommissionDocument32 pages15TH Finance CommissionSunaina SukumarNo ratings yet

- Current Events 66 BPSCDocument137 pagesCurrent Events 66 BPSCpifaj90517No ratings yet

- 15th Finance Commission RecommendationsDocument4 pages15th Finance Commission RecommendationsVaibhavNo ratings yet

- 14th Finance Commission PDFDocument5 pages14th Finance Commission PDFSudha PandeyNo ratings yet

- 14th Finance Commission VISION IASDocument14 pages14th Finance Commission VISION IASimranNo ratings yet

- 15th Finance Commission: Anuj JindalDocument17 pages15th Finance Commission: Anuj JindalamritNo ratings yet

- 15th Finance Commission ReportDocument26 pages15th Finance Commission ReportLeela KalyaniNo ratings yet

- Lecture 27Document6 pagesLecture 27Vvanshika SinghalNo ratings yet

- Federation, Japan, and Canada. These Data Include CODocument16 pagesFederation, Japan, and Canada. These Data Include COSaif EqbalNo ratings yet

- Deficit Fundamentalism Vs Fiscal Federalism Implications of 13th Finance Commissions RecommendationsDocument8 pagesDeficit Fundamentalism Vs Fiscal Federalism Implications of 13th Finance Commissions RecommendationsShay WaxenNo ratings yet

- FINAL WRITTEN Econ PrsentationDocument4 pagesFINAL WRITTEN Econ PrsentationharrishNo ratings yet

- 15th Finance Commission ReportDocument10 pages15th Finance Commission ReportSaurabh SinghNo ratings yet

- Central Transfers To States: Role of The Finance CommissionDocument2 pagesCentral Transfers To States: Role of The Finance CommissionvikramNo ratings yet

- Fiscal FederalismDocument11 pagesFiscal FederalismPark Seo YoonNo ratings yet

- 15th Finance Commission Upsc Notes 95Document4 pages15th Finance Commission Upsc Notes 95ArshaanNo ratings yet

- Federal FinanceDocument28 pagesFederal Financeadip67436No ratings yet

- 15th Fifteenth Finance CommisionDocument76 pages15th Fifteenth Finance CommisionJaved StylesNo ratings yet

- 14th Finance Commission - Report Summary PDFDocument1 page14th Finance Commission - Report Summary PDFSourav MeenaNo ratings yet

- Fiscal FederalismDocument19 pagesFiscal FederalismPark Seo YoonNo ratings yet

- States' Share in Central Taxes: ISSN (ONLINE) : 2250-0758, ISSN (PRINT) : 2394-6962Document9 pagesStates' Share in Central Taxes: ISSN (ONLINE) : 2250-0758, ISSN (PRINT) : 2394-6962SujayaNo ratings yet

- 15 TH Finance ComissionDocument3 pages15 TH Finance ComissionAnmol RatanNo ratings yet

- PUBLIC, UNIT 2C, Summary of Finance Commission ReportDocument4 pagesPUBLIC, UNIT 2C, Summary of Finance Commission Reportridhijain0102No ratings yet

- PRS Report Summary of 15th Finance Commission For FY 2020-21Document4 pagesPRS Report Summary of 15th Finance Commission For FY 2020-21mansavi bihaniNo ratings yet

- Financial Forecasting in The Budget Preparation ProcessDocument7 pagesFinancial Forecasting in The Budget Preparation Processnmsusarla888No ratings yet

- 15 FC PPT in PDF-2Document40 pages15 FC PPT in PDF-2Ashish SaikiaNo ratings yet

- Fiscal Planning and The New Maintenance of Effort Law: Companion Document For Council PresentationDocument39 pagesFiscal Planning and The New Maintenance of Effort Law: Companion Document For Council PresentationParents' Coalition of Montgomery County, MarylandNo ratings yet

- 5 - Chapter 5 - Financial Plan - FINALDocument22 pages5 - Chapter 5 - Financial Plan - FINALnickmorara4No ratings yet

- February 2021 24Document1 pageFebruary 2021 24Raghav SharmaNo ratings yet

- State-Ordered Report Completed by PFM GroupDocument26 pagesState-Ordered Report Completed by PFM GroupAnonymous L5EiMKJ50% (2)

- 16th Finance CommissionDocument4 pages16th Finance CommissionSanthosh KumarNo ratings yet

- 14th Finance CommissionDocument6 pages14th Finance CommissionPartha SurveNo ratings yet

- 14th Finance Commission PDFDocument6 pages14th Finance Commission PDFRavu ArunNo ratings yet

- CFC - SFCDocument22 pagesCFC - SFCAuna SandoNo ratings yet

- Ijsrmjournal, Journal Manager, 30 IjsrmDocument9 pagesIjsrmjournal, Journal Manager, 30 IjsrmZahidNo ratings yet

- 15th Finance CommissionDocument6 pages15th Finance CommissionSingh JagdishNo ratings yet

- Fiscal Federalism in IndiaDocument32 pagesFiscal Federalism in IndiaZaisha KhanNo ratings yet

- Fiscal Policy 1-Resource Mobilization TaxationDocument22 pagesFiscal Policy 1-Resource Mobilization TaxationumairzafarNo ratings yet

- 016 SD 01Document17 pages016 SD 01JOSE EPHRAIM MAGLAQUENo ratings yet

- Rbi Report On Finances of PanchayatsDocument8 pagesRbi Report On Finances of PanchayatsSKNo ratings yet

- Punjab: 604.2 Billion USD Sindh: 291.5 Billion USD KPK: 85 Billion USD Balochistan: 32 Billion USDDocument4 pagesPunjab: 604.2 Billion USD Sindh: 291.5 Billion USD KPK: 85 Billion USD Balochistan: 32 Billion USDzakria yahyaNo ratings yet

- Grant Thornton Report - Local Government A Financial SnapshotDocument22 pagesGrant Thornton Report - Local Government A Financial SnapshotNew Zealand Taxpayers' UnionNo ratings yet

- Issues and Challenges For The 14Th Finance Commission: Career in GeophysicsDocument2 pagesIssues and Challenges For The 14Th Finance Commission: Career in GeophysicsCandyCrüshSagaNo ratings yet

- Economics ProjectDocument10 pagesEconomics ProjectbhavikNo ratings yet

- Commission Shall Use The Population Data of 2011 While Making Its RecommendationsDocument2 pagesCommission Shall Use The Population Data of 2011 While Making Its RecommendationsTajNo ratings yet

- Darshini Gayithri 2023 An Econometric Analysis of Revenue Diversification Among Selected Indian StatesDocument23 pagesDarshini Gayithri 2023 An Econometric Analysis of Revenue Diversification Among Selected Indian StatessushilNo ratings yet

- BVCSD Statler Report Final BVCSD Five Year Fiscal Forecast 2-11-13-1Document31 pagesBVCSD Statler Report Final BVCSD Five Year Fiscal Forecast 2-11-13-1Faith GreenNo ratings yet

- Media Statement - How Much It Costs To Run County Governments - Final FinalDocument2 pagesMedia Statement - How Much It Costs To Run County Governments - Final FinalInternational Budget Partnership KenyaNo ratings yet

- Analysis of Municipality TernateDocument14 pagesAnalysis of Municipality TernateSuleman S Al-QalbyNo ratings yet

- Kitchener 2013 Budget Preview Nov 5 2012Document52 pagesKitchener 2013 Budget Preview Nov 5 2012WR_RecordNo ratings yet

- Acct 260 Cafr 3-15Document6 pagesAcct 260 Cafr 3-15StephanieNo ratings yet

- Beyond Every Child Matters: Local Area Agreements and Your OutcomesDocument14 pagesBeyond Every Child Matters: Local Area Agreements and Your OutcomesodalindNo ratings yet

- State Comptroller's Audit of The The Hendrick Hudson School District's Financial ConditionDocument11 pagesState Comptroller's Audit of The The Hendrick Hudson School District's Financial ConditionCara MatthewsNo ratings yet

- 201002ThematicPaper LocalServiceDelivery FinalDocument39 pages201002ThematicPaper LocalServiceDelivery FinalLham DorjiNo ratings yet

- Gadgil FormulaDocument6 pagesGadgil FormulaHemant ShivakumarNo ratings yet

- Chapter-Iv An Analysis of The Recommendations of Recent Finance Commissions of India A Descriptive TreatiseDocument18 pagesChapter-Iv An Analysis of The Recommendations of Recent Finance Commissions of India A Descriptive TreatiseRaja SimmanNo ratings yet

- Highlights 14thfinance Commission Report PDFDocument2 pagesHighlights 14thfinance Commission Report PDFtanyaa90No ratings yet

- 15th Finance CommissionDocument20 pages15th Finance CommissiontqncsqnsvoqzulkeaaNo ratings yet

- Dutchess County AuditDocument15 pagesDutchess County AuditDaily FreemanNo ratings yet

- Report Summary: Report of The 15 Finance Commission For FY 2020-21Document4 pagesReport Summary: Report of The 15 Finance Commission For FY 2020-21Adithya Sharma SalagramNo ratings yet

- Local Public Finance Management in the People's Republic of China: Challenges and OpportunitiesFrom EverandLocal Public Finance Management in the People's Republic of China: Challenges and OpportunitiesNo ratings yet

- Scanned With CamscannerDocument8 pagesScanned With Camscannershivam kumarNo ratings yet

- Custom Search: Law Articles - India's Most Authentice Free Legal Source OnlineDocument4 pagesCustom Search: Law Articles - India's Most Authentice Free Legal Source Onlineshivam kumarNo ratings yet

- Trips and TrimsDocument2 pagesTrips and Trimsshivam kumarNo ratings yet

- History ProjectDocument9 pagesHistory Projectshivam kumarNo ratings yet

- Indian Democracy - Role of Election CommDocument84 pagesIndian Democracy - Role of Election Commshivam kumarNo ratings yet

- 10 Eng ExerDocument17 pages10 Eng ExerGuruNo ratings yet

- Environmental Governance Programme (EGP)Document2 pagesEnvironmental Governance Programme (EGP)Francisco SilvaNo ratings yet

- Dentate PDIDocument5 pagesDentate PDIkelompok cNo ratings yet

- Vocab 8b Cee - b1 - RB - TB - A19 - Resource-16Document1 pageVocab 8b Cee - b1 - RB - TB - A19 - Resource-16Freddy Flores VilcaNo ratings yet

- Assignment N° 1: Connected Speech: Assimilation-Coalescence - Elision - LiaisonDocument5 pagesAssignment N° 1: Connected Speech: Assimilation-Coalescence - Elision - LiaisonRoxana AguirreNo ratings yet

- Analisis Preferensi Konsumen Terhadap Bu Dfe22138Document6 pagesAnalisis Preferensi Konsumen Terhadap Bu Dfe22138CERITA SEROJANo ratings yet

- Ching V DigestDocument2 pagesChing V DigestAthena Venice MercadoNo ratings yet

- Directions:: Criteria 5 4 2 1Document3 pagesDirections:: Criteria 5 4 2 1Ha KDOGNo ratings yet

- محاضره 1 انسجهDocument32 pagesمحاضره 1 انسجهYahya Daham Zafeer SakhrNo ratings yet

- James Cameron - Original Screenplay For AvatarDocument152 pagesJames Cameron - Original Screenplay For AvatarAngelSuicide67% (3)

- Negro y AzulDocument3 pagesNegro y AzulDado TopicNo ratings yet

- GCSE MATH Past Papers Mark Schemes Standard MayJune Series 2013 12709Document6 pagesGCSE MATH Past Papers Mark Schemes Standard MayJune Series 2013 12709Назар ГущікNo ratings yet

- DATA6211 EaDocument9 pagesDATA6211 Eanzfpbte564No ratings yet

- An Introduction of Computer Programming - g10Document20 pagesAn Introduction of Computer Programming - g10zimran dave epelipciaNo ratings yet

- Hoover vs. FDR: Reactions To The Great DepressionDocument3 pagesHoover vs. FDR: Reactions To The Great Depressionirregularflowers100% (1)

- 2 - PrimusLine - flyer-water-GBDocument4 pages2 - PrimusLine - flyer-water-GBzeroicesnowNo ratings yet

- WFWEDocument30 pagesWFWEEstiven Gier50% (4)

- Trust PATDocument211 pagesTrust PATfergieNo ratings yet

- Radio IsotopesDocument10 pagesRadio IsotopesPG ChemistryNo ratings yet

- FemaleAccountant 1 To 271 14 02 2020Document67 pagesFemaleAccountant 1 To 271 14 02 2020Stigan India100% (1)

- Reading and Math Online Resources - 2017-18Document3 pagesReading and Math Online Resources - 2017-18api-32237090No ratings yet

- History of Fashion - Indus VallyDocument3 pagesHistory of Fashion - Indus VallyShAiShahNo ratings yet

- Persuasive Speech Analysis InstructionsDocument2 pagesPersuasive Speech Analysis Instructionsapi-552410496No ratings yet

- PHD Thesis Dahle PDFDocument190 pagesPHD Thesis Dahle PDFJessNo ratings yet

- Arroyo Vs YuDocument4 pagesArroyo Vs YuAlean Fueconcillo-EvangelistaNo ratings yet

- Shear Connections Notes: (1) The Beams Considered With Coped ConditionDocument9 pagesShear Connections Notes: (1) The Beams Considered With Coped ConditionSrikanth SikhaNo ratings yet

- Henry Schein Orthodontics Catalog - General SuppliesDocument8 pagesHenry Schein Orthodontics Catalog - General SuppliesOrtho OrganizersNo ratings yet

- Sustainable Biodegradable Solutions Reshaping The Food Packaging IndustryDocument65 pagesSustainable Biodegradable Solutions Reshaping The Food Packaging Industrypot poteNo ratings yet