Download as pdf or txt

You might also like

- Ame1501 101 2023Document2 pagesAme1501 101 2023Kwazi MalazaNo ratings yet

- Assignment 1Document9 pagesAssignment 1Celsozeca2011No ratings yet

- Industry Report AutomobileDocument14 pagesIndustry Report AutomobileASHISH AGARWALNo ratings yet

- Revenue Estimation: Sponsored byDocument53 pagesRevenue Estimation: Sponsored byMirna CachayNo ratings yet

- Reservation AgreementDocument1 pageReservation AgreementMerwin S. ManucumNo ratings yet

- Group Presentation Feb 2022Document52 pagesGroup Presentation Feb 2022Sayali StoriesNo ratings yet

- Group Presentation Feb 2023Document56 pagesGroup Presentation Feb 2023Jay PrajapatiNo ratings yet

- Group Presentation Feb 2023Document56 pagesGroup Presentation Feb 2023Nishit VermaNo ratings yet

- GCMDocument22 pagesGCMIda MaharaniNo ratings yet

- 14 - Learning From Accidents - tcm153-367867 PDFDocument18 pages14 - Learning From Accidents - tcm153-367867 PDFVipin SomasekharanNo ratings yet

- OPEX-Monthly Reports-YTD SeptemberDocument39 pagesOPEX-Monthly Reports-YTD SeptemberNEZNo ratings yet

- Post-Mock Revision Set 2 - Marking SchemeDocument12 pagesPost-Mock Revision Set 2 - Marking Schemetitle subNo ratings yet

- Group Presentation July 2021Document52 pagesGroup Presentation July 2021raghunandhan.cvNo ratings yet

- Mining ProductivityDocument176 pagesMining Productivityykharchi88% (8)

- Lean Six Sigma 2022 - Nitrogen Improvement - AnalyseDocument80 pagesLean Six Sigma 2022 - Nitrogen Improvement - AnalyseSalman CnNo ratings yet

- Lean Six Sigma 2022 - Nitrogen Improvement - D&MDocument71 pagesLean Six Sigma 2022 - Nitrogen Improvement - D&MSalman CnNo ratings yet

- Assignment-2 (Cost Accounting)Document24 pagesAssignment-2 (Cost Accounting)Iqra AbbasNo ratings yet

- Why Is Inventory Important? Why Is Inventory Required?Document14 pagesWhy Is Inventory Important? Why Is Inventory Required?Dương DươngNo ratings yet

- 1 Graad 12: National Senior CertificateDocument22 pages1 Graad 12: National Senior CertificateSphiwenhle MbheleNo ratings yet

- Presentation-1 Improving Energy Efficiency - Muhammad Farooq - FFCDocument26 pagesPresentation-1 Improving Energy Efficiency - Muhammad Farooq - FFCUmar AslamNo ratings yet

- 1 Tata Steel 02jan24 Kotak InstDocument12 pages1 Tata Steel 02jan24 Kotak Instraghavanseshu.seshathriNo ratings yet

- Policy On Environmental ProtectionDocument18 pagesPolicy On Environmental ProtectionYOGA SAGITA HNNo ratings yet

- Cyclical Forecasting 2018Document17 pagesCyclical Forecasting 2018mweng407No ratings yet

- PH Zero Loss Journey For CashDocument2 pagesPH Zero Loss Journey For CashBhupinder SinghNo ratings yet

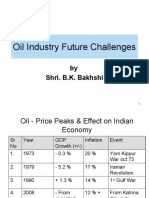

- Oil Industry Future Challenges: by Shri. B.K. BakhshiDocument21 pagesOil Industry Future Challenges: by Shri. B.K. BakhshiGirish1412No ratings yet

- Consolidated Monthly Bulletins: January-December 2019Document25 pagesConsolidated Monthly Bulletins: January-December 2019Rahul ChoudharyNo ratings yet

- Condensed Consolidated Interim Results (Reviewed) : For The Six Months Ended 31 December 2020Document50 pagesCondensed Consolidated Interim Results (Reviewed) : For The Six Months Ended 31 December 2020Serkan BirolNo ratings yet

- Bahodopi SMEDY FinalDocument26 pagesBahodopi SMEDY FinalSamuel samuelNo ratings yet

- Premier Oil Falkland Islands Sea Lion Development Offshore Oil Spill StrategyDocument78 pagesPremier Oil Falkland Islands Sea Lion Development Offshore Oil Spill Strategyjanemcniven505No ratings yet

- Sample MRU Global Fire Retardant Plywood Market - PDF 1 52Document92 pagesSample MRU Global Fire Retardant Plywood Market - PDF 1 52zbignevtvNo ratings yet

- National Senior Certificate: Grade 12Document9 pagesNational Senior Certificate: Grade 12Khathutshelo KharivheNo ratings yet

- Fly Ash S Type F Data SheetDocument1 pageFly Ash S Type F Data SheetUdhayakumar VenkataramanNo ratings yet

- Jun-2017-Consolidated-Bulletins-3-08-2017 TRINIDAD Y TOBAGODocument24 pagesJun-2017-Consolidated-Bulletins-3-08-2017 TRINIDAD Y TOBAGOrubenpeNo ratings yet

- KZN Economics Grade 12 September 2023 P2 and MemoDocument30 pagesKZN Economics Grade 12 September 2023 P2 and Memonkatekodawn72No ratings yet

- 2016 Trinidad y TobagoDocument25 pages2016 Trinidad y TobagorubenpeNo ratings yet

- SUG 1-Year Mine Plan Presentation - FINALE6Document64 pagesSUG 1-Year Mine Plan Presentation - FINALE6Christian TewodrosNo ratings yet

- Profile On Boric AcidDocument18 pagesProfile On Boric AcidKaramara Training & ConsultancyNo ratings yet

- Rio - Tube CP 2015Document16 pagesRio - Tube CP 2015Ioannis ZNo ratings yet

- BHP Billiton Base Metals: India On The Global Map?Document14 pagesBHP Billiton Base Metals: India On The Global Map?miningnovaNo ratings yet

- Military Budget 1999 - HologramsDocument8 pagesMilitary Budget 1999 - HologramsChiodo72No ratings yet

- Lab 1Document6 pagesLab 1Gwen Ibarra SuaybaguioNo ratings yet

- Group 4 SC-Acid Analysis PresentationDocument20 pagesGroup 4 SC-Acid Analysis PresentationYanbin CaoNo ratings yet

- Putting The Market Togethere: Aggregate Demand and Aggregate SupplyDocument21 pagesPutting The Market Togethere: Aggregate Demand and Aggregate SupplyKatherine Asis NatinoNo ratings yet

- Biomass Power Generation Plant Installation Project ReportDocument30 pagesBiomass Power Generation Plant Installation Project ReportRavi JainNo ratings yet

- CFC Supervisory Committee 21st Feb 2022 Final Version 2Document11 pagesCFC Supervisory Committee 21st Feb 2022 Final Version 2Htoo Htoo KyawNo ratings yet

- Weir Capital Markets Day 17 June 2014Document83 pagesWeir Capital Markets Day 17 June 2014iman_pumpNo ratings yet

- 1Q 2020 Earnings Call: Rick Muncrief, Chairman & CeoDocument18 pages1Q 2020 Earnings Call: Rick Muncrief, Chairman & CeoValue InvestorNo ratings yet

- Jean-Raymond Boulle, Titanium Resources GroupDocument30 pagesJean-Raymond Boulle, Titanium Resources Groupinvestorseurope offshore stockbrokersNo ratings yet

- CommoditiesDaily 080317Document2 pagesCommoditiesDaily 080317Dominic TsuiNo ratings yet

- 3-Energy Narrative - Guyana NG Feasibility Study - Revised Final Report - Appendix C - Final - 0 - 0Document90 pages3-Energy Narrative - Guyana NG Feasibility Study - Revised Final Report - Appendix C - Final - 0 - 0Olusegun OyebanjiNo ratings yet

- Grade 9 Provincial Examination Economics Management and Sciences P2 (English) June 2022 Possible AnswersDocument6 pagesGrade 9 Provincial Examination Economics Management and Sciences P2 (English) June 2022 Possible AnswersTererai Lalelani Masikati HoveNo ratings yet

- Economic Effects of Indonesia's Mineral-Processing Requirment For ExportDocument70 pagesEconomic Effects of Indonesia's Mineral-Processing Requirment For Exportblue100% (1)

- Case Study: Round - 1Document9 pagesCase Study: Round - 1Rajat RanjanNo ratings yet

- FMC ExpenditureDocument1 pageFMC Expenditureshamb2001No ratings yet

- RFP-01353 - Price Update 2Document69 pagesRFP-01353 - Price Update 2the next miamiNo ratings yet

- Test Che323Document3 pagesTest Che323nurulNo ratings yet

- Market Reports 1613989542Document2 pagesMarket Reports 1613989542Ankit AgarwalNo ratings yet

- Calcium ChlorideDocument18 pagesCalcium ChlorideyenealemNo ratings yet

- 42A06SW0013Document50 pages42A06SW0013thanikachalam.cNo ratings yet

- Cma Assignment 1 PDFDocument1 pageCma Assignment 1 PDFThomas nyadeNo ratings yet

- IMO ES Enero 2022 Los BroncesDocument133 pagesIMO ES Enero 2022 Los BroncesDarling JallasNo ratings yet

- Light Manufacturing in Zambia: Job Creation and Prosperity in a Resource-Based EconomyFrom EverandLight Manufacturing in Zambia: Job Creation and Prosperity in a Resource-Based EconomyNo ratings yet

- Sean Darby - JefferiesDocument18 pagesSean Darby - JefferiesKurnia NindyoNo ratings yet

- M Chatib BasriDocument15 pagesM Chatib BasriKurnia NindyoNo ratings yet

- Macroscope: Huge Drop On Imports Likely Not SustainableDocument5 pagesMacroscope: Huge Drop On Imports Likely Not SustainableKurnia NindyoNo ratings yet

- Macroscope: Inflation Preview: Tame NovemberDocument4 pagesMacroscope: Inflation Preview: Tame NovemberKurnia NindyoNo ratings yet

- Macroscope: Nov18 Trade Result Could Trigger (Another) Front-Loaded Rate HikeDocument5 pagesMacroscope: Nov18 Trade Result Could Trigger (Another) Front-Loaded Rate HikeKurnia NindyoNo ratings yet

- Peralatan Industri Kimia: Arif Rahman, ST MTDocument80 pagesPeralatan Industri Kimia: Arif Rahman, ST MTKurnia NindyoNo ratings yet

- Te U/ Home Loan: Subsequent InstalmentsDocument1 pageTe U/ Home Loan: Subsequent InstalmentsShatvik MishraNo ratings yet

- Financial StatementDocument19 pagesFinancial StatementCS SNo ratings yet

- VAT Invoice - 2024-01-31 - 00000007031318-2401-18359960Document2 pagesVAT Invoice - 2024-01-31 - 00000007031318-2401-18359960mhzp4ckj47No ratings yet

- Econ Paper 2 - Sample For ClassDocument2 pagesEcon Paper 2 - Sample For ClassDanishNo ratings yet

- Consumer and Producer Theory - Falvio ToxvaerdDocument188 pagesConsumer and Producer Theory - Falvio ToxvaerdNimra AhmedNo ratings yet

- Board Resolution of Smart Iaq Technologies Inc. Number - 1 - Series of 2017Document1 pageBoard Resolution of Smart Iaq Technologies Inc. Number - 1 - Series of 2017Marnel DaluyenNo ratings yet

- Promise To PayDocument3 pagesPromise To PayDaraire OlowokereNo ratings yet

- Cattleya Tent Events: Event Planning BusinessDocument8 pagesCattleya Tent Events: Event Planning BusinessRobert StefanNo ratings yet

- HR/ Management GamesDocument39 pagesHR/ Management Gameskamdica100% (6)

- Quantitative Chapter 4 - SI and CIDocument11 pagesQuantitative Chapter 4 - SI and CISWAGATAM BAZNo ratings yet

- Tutorial MSDocument4 pagesTutorial MSVidhya NairNo ratings yet

- Swarovski Components Collection 2023 LowResDocument450 pagesSwarovski Components Collection 2023 LowResjuliabalbi01No ratings yet

- Rfaq PDFDocument69 pagesRfaq PDFsaurabh yadavNo ratings yet

- MECH REC69 Magnetic Particle Dye Penetrant ReportDocument1 pageMECH REC69 Magnetic Particle Dye Penetrant ReporttinzarmoeNo ratings yet

- Joe Grad Has Just Arrived at The Big U HeDocument2 pagesJoe Grad Has Just Arrived at The Big U Hetrilocksp SinghNo ratings yet

- Examiner's Report: MA/FMA Management AccountingDocument9 pagesExaminer's Report: MA/FMA Management AccountingFayaz AhmedNo ratings yet

- (English (Auto-Generated) ) 04 - Drilling Economics and The AFE - FLV (DownSub - Com)Document5 pages(English (Auto-Generated) ) 04 - Drilling Economics and The AFE - FLV (DownSub - Com)Nasser JNo ratings yet

- 12th Commerce B.K Practice Book Smart NotesDocument20 pages12th Commerce B.K Practice Book Smart NotesSiddhi Kabadi 130 11th Com BNo ratings yet

- RDO No. 100 - Ozamis City, Misamis OccidentalDocument206 pagesRDO No. 100 - Ozamis City, Misamis OccidentalBahay PuyatNo ratings yet

- Design and Construction of A Manual Food GrinderDocument10 pagesDesign and Construction of A Manual Food GrinderAlvin S Soriano Jr.No ratings yet

- CDCS Case StudyDocument4 pagesCDCS Case StudyPangoea Pangoea100% (1)

- Power Feed-Thru Systems & ConnectorsDocument2 pagesPower Feed-Thru Systems & Connectorsclaudio godinezNo ratings yet

- Price List 22042013 National CablesDocument8 pagesPrice List 22042013 National CablesSukhirthan SenthilkumarNo ratings yet

- Summary MAS291Document9 pagesSummary MAS291Hiếu PhạmNo ratings yet

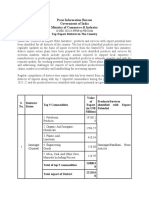

- District Wise Exports of India - 2021Document13 pagesDistrict Wise Exports of India - 2021MNo ratings yet

- Chapter Four Data Presentation, Analysis and Interpretation: 4.0 PreambleDocument60 pagesChapter Four Data Presentation, Analysis and Interpretation: 4.0 PreambleADAMNo ratings yet

- 3 - Frank - Chapter03 - Rational Consumer ChoiceDocument40 pages3 - Frank - Chapter03 - Rational Consumer ChoiceNOPPHANUT NGAMVITROJENo ratings yet

- ISQ - ECO102 - Summer 2022 - Course OutlineDocument4 pagesISQ - ECO102 - Summer 2022 - Course OutlineRakibul HasanNo ratings yet