Download as pdf or txt

You might also like

- Trading Implied Volatility: Extrinsiq Advanced Options Trading Guides, #4From EverandTrading Implied Volatility: Extrinsiq Advanced Options Trading Guides, #4Rating: 4 out of 5 stars4/5 (1)

- FY021 Introducttion To Business StudiesDocument13 pagesFY021 Introducttion To Business StudiesKamrul Islam SakibNo ratings yet

- Value Investing: The Buffett Techniques Of Accumulating Wealth With Practical Strategies To Always Choose The Intelligent InvestmentFrom EverandValue Investing: The Buffett Techniques Of Accumulating Wealth With Practical Strategies To Always Choose The Intelligent InvestmentRating: 4.5 out of 5 stars4.5/5 (39)

- Semis Examination BDocument12 pagesSemis Examination BCHENG50% (2)

- Forecasting VolatilityDocument132 pagesForecasting VolatilityPeter Pank100% (1)

- Question SetDocument2 pagesQuestion Setbando007No ratings yet

- Class 19Document5 pagesClass 19bando007No ratings yet

- 4BS1 01R Que 20190517Document16 pages4BS1 01R Que 20190517ilovefettuccine0% (1)

- Introduction To ValuationDocument5 pagesIntroduction To ValuationRG VergaraNo ratings yet

- Valuation Concepts and Methods Introduction To ValuationDocument18 pagesValuation Concepts and Methods Introduction To ValuationPatricia Nicole BarriosNo ratings yet

- Session 2 (CH 1 - Introduction To Valuation)Document27 pagesSession 2 (CH 1 - Introduction To Valuation)Arun KumarNo ratings yet

- An Introduction To Valuation: Aswath DamodaranDocument29 pagesAn Introduction To Valuation: Aswath Damodaranaditya_jain1188No ratings yet

- Mauboussin - The Importance of ExpectationsDocument17 pagesMauboussin - The Importance of Expectationsjockxyz100% (1)

- A Philosophical Basis For ValuationDocument1 pageA Philosophical Basis For ValuationAbhishek ChakrabortyNo ratings yet

- Jieya Kylah D. Casiple BSMA 4-BDocument4 pagesJieya Kylah D. Casiple BSMA 4-BJieya Kylah CasipleNo ratings yet

- Thoughts On Valuation - Part 2 - An Epistemological ViewDocument8 pagesThoughts On Valuation - Part 2 - An Epistemological Viewpjs15No ratings yet

- Business Valuation1Document288 pagesBusiness Valuation1Kapil Bhopatkar100% (1)

- Final Project ReportDocument51 pagesFinal Project ReportmadhumdkNo ratings yet

- 2012.08.21 - The Importance of Expectations - That Question That Bears Repeating - What's Priced in PDFDocument17 pages2012.08.21 - The Importance of Expectations - That Question That Bears Repeating - What's Priced in PDFbrineshrimpNo ratings yet

- Chap 8 Lecture NoteDocument4 pagesChap 8 Lecture NoteCloudSpireNo ratings yet

- Don Fishback The 3 Proven KeyDocument30 pagesDon Fishback The 3 Proven KeyCristinaNo ratings yet

- Everything Is A DCF ModelDocument13 pagesEverything Is A DCF ModelSajjad HossainNo ratings yet

- Everything Is A DCF Model: Counterpoint Global InsightsDocument12 pagesEverything Is A DCF Model: Counterpoint Global InsightsAnonymous kgSMlxNo ratings yet

- Penman 5ed Chap007Document22 pagesPenman 5ed Chap007Hirastikanah HKNo ratings yet

- Methods Estimate Value by Luca CapitalDocument24 pagesMethods Estimate Value by Luca CapitalDũng NguyễnNo ratings yet

- Business SolutionDocument7 pagesBusiness SolutionYogesh PanwarNo ratings yet

- Investment Valuation: Learn Proven Methods For Determining Asset Value And Taking The Right Investing DecisionsFrom EverandInvestment Valuation: Learn Proven Methods For Determining Asset Value And Taking The Right Investing DecisionsNo ratings yet

- An Introduction To ValuationDocument27 pagesAn Introduction To ValuationBhaskar SmithNo ratings yet

- C 18 PDFDocument288 pagesC 18 PDFBKS SannyasiNo ratings yet

- Val Closing PropositionsDocument7 pagesVal Closing PropositionsHadi P.No ratings yet

- Bruce 2Document62 pagesBruce 2vhueves77No ratings yet

- Fundamental AnalysisDocument40 pagesFundamental AnalysisKhialani RohitNo ratings yet

- It's All A Big Mistake - 06!20!12.unlockedDocument10 pagesIt's All A Big Mistake - 06!20!12.unlockeddpbasicNo ratings yet

- Relative ValuationDocument4 pagesRelative Valuationjiteshjacob439No ratings yet

- Chapter 1 Fundamental Principles of ValuationDocument15 pagesChapter 1 Fundamental Principles of ValuationMonica MangobaNo ratings yet

- VCM Chapter 1Document12 pagesVCM Chapter 1AMNo ratings yet

- The Greater Fool TheoryDocument4 pagesThe Greater Fool TheoryElvie'Inanod Sumayang delaCruz'BaqueroNo ratings yet

- Model Risk ManagementDocument13 pagesModel Risk ManagementayzlimNo ratings yet

- Valuation of StocksDocument47 pagesValuation of Stocksojasd1100% (1)

- (Article) Stock Valuation Models (Prudential Financial 2003)Document31 pages(Article) Stock Valuation Models (Prudential Financial 2003)trungvt2111No ratings yet

- Financial Management - A Random Walk Down Wall Street Case StudyDocument7 pagesFinancial Management - A Random Walk Down Wall Street Case StudyjanelleNo ratings yet

- Value Premium and Value InvestingDocument41 pagesValue Premium and Value InvestingSreyas SudarsanNo ratings yet

- Liquidity Trading and Price Determination in EquitDocument29 pagesLiquidity Trading and Price Determination in EquitsayyadnagarbarsandaNo ratings yet

- Approach For DCF and Multiple ValuationDocument21 pagesApproach For DCF and Multiple Valuationmodi4uk100% (1)

- Methods of Estimating Value - LucaCAP PDFDocument24 pagesMethods of Estimating Value - LucaCAP PDFAndré ksNo ratings yet

- Classical Finance Vs Behavoiral FinanceDocument5 pagesClassical Finance Vs Behavoiral FinancePurnendu SinghNo ratings yet

- Price AnomaliesDocument24 pagesPrice AnomaliesTodd W. SigetyNo ratings yet

- Value InterviewsDocument31 pagesValue InterviewsAmit Rana100% (1)

- Pitfalls To Avoid: OutputDocument7 pagesPitfalls To Avoid: OutputSrivastava MukulNo ratings yet

- Booksummary Priceless The Hidden Value of PsychologyDocument3 pagesBooksummary Priceless The Hidden Value of PsychologyVaishnaviRavipatiNo ratings yet

- Little Book FINALDocument17 pagesLittle Book FINALquelthalas100% (5)

- Interviews For Intelligent Investors Toby Carlisle Wes GrayDocument20 pagesInterviews For Intelligent Investors Toby Carlisle Wes GraySylvester MalapasNo ratings yet

- 08 LasherIM Ch08Document20 pages08 LasherIM Ch08Ed Donaldy100% (2)

- Common Errors in DCF ModelsDocument12 pagesCommon Errors in DCF Modelsrslamba1100% (2)

- Common DCF Errors - LeggMasonDocument12 pagesCommon DCF Errors - LeggMasonBob JonesNo ratings yet

- Notes Chapter WiseDocument55 pagesNotes Chapter WiseBitan SahaNo ratings yet

- Valuation and TradingDocument22 pagesValuation and TradingKathryn FlemingNo ratings yet

- Order FlowDocument184 pagesOrder Flowvaclarush100% (11)

- My Notes of BG's Value Investing SeminaryDocument12 pagesMy Notes of BG's Value Investing SeminarysilviocastNo ratings yet

- Chapter 1: Fundamental Principles of Valuation Fundamentals Principles of ValuationDocument15 pagesChapter 1: Fundamental Principles of Valuation Fundamentals Principles of ValuationJoyce Dela CruzNo ratings yet

- Investment Philosophies: Successful Strategies and the Investors Who Made Them WorkFrom EverandInvestment Philosophies: Successful Strategies and the Investors Who Made Them WorkRating: 4.5 out of 5 stars4.5/5 (2)

- Mdim - Icbit Brochure 2020Document6 pagesMdim - Icbit Brochure 2020bando007No ratings yet

- Mait Mba - FDP - July 2021Document7 pagesMait Mba - FDP - July 2021bando007No ratings yet

- Understanding The Concept of Corporate Social ResponsibilityDocument18 pagesUnderstanding The Concept of Corporate Social Responsibilitybando007No ratings yet

- Ir Fy 2017 18 PDFDocument412 pagesIr Fy 2017 18 PDFbando007No ratings yet

- International Webinar: Resurgence of Business Growth Post Covid-19: Challenges and StrategiesDocument1 pageInternational Webinar: Resurgence of Business Growth Post Covid-19: Challenges and Strategiesbando007No ratings yet

- Test 3Document1 pageTest 3bando007No ratings yet

- 1Document4 pages1bando007No ratings yet

- Time Value of MoneyDocument11 pagesTime Value of Moneybando007No ratings yet

- Dividend Discount ModelDocument12 pagesDividend Discount Modelbando007No ratings yet

- Japan Funds Fillip To East-West Metro - Agency Inspects Sites Where Work Has Started After Years of DelayDocument2 pagesJapan Funds Fillip To East-West Metro - Agency Inspects Sites Where Work Has Started After Years of Delaybando007No ratings yet

- IBA Journal July Dec 2016Document104 pagesIBA Journal July Dec 2016bando007No ratings yet

- Registration FormDocument1 pageRegistration Formbando007No ratings yet

- List of Funding Agencies For Research Proposals: Department of Science and Technology (DST)Document13 pagesList of Funding Agencies For Research Proposals: Department of Science and Technology (DST)ParamasivamKuppusamyNo ratings yet

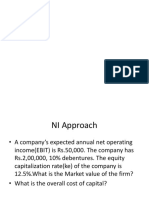

- NI NOI ApproachDocument14 pagesNI NOI Approachbando007No ratings yet

- XimeDocument24 pagesXimebando007No ratings yet

- Bhruti NewDocument2 pagesBhruti Newbando007No ratings yet

- Problem 2: RequiredDocument3 pagesProblem 2: RequiredJohn Lester C AlagNo ratings yet

- SalaryDocument42 pagesSalaryNidhi LathNo ratings yet

- Template M/S Laxmi Enterprises Dabur: Gross Profit (Income)Document10 pagesTemplate M/S Laxmi Enterprises Dabur: Gross Profit (Income)trisanka banikNo ratings yet

- Odev - Cash - Flow - and - Financial - Planning (1) - Fatih EkerDocument16 pagesOdev - Cash - Flow - and - Financial - Planning (1) - Fatih EkerfurkanNo ratings yet

- Macro Class Exercises Sem 1 2020-2021Document27 pagesMacro Class Exercises Sem 1 2020-2021Imran UmarNo ratings yet

- This Is FreedomDocument31 pagesThis Is FreedomNurhussein RaopanNo ratings yet

- Entrep Q2 Module 3 Week 5Document8 pagesEntrep Q2 Module 3 Week 5Some DudeNo ratings yet

- Essentials of Accounting For Governmental and Not-For-Profit Organizations 12th Edition Copley Solutions Manual 1Document36 pagesEssentials of Accounting For Governmental and Not-For-Profit Organizations 12th Edition Copley Solutions Manual 1timothyaliqjtkomaegr100% (35)

- April - 20223Document1 pageApril - 20223Gadhavi JitudanNo ratings yet

- Fiverr ProjectDocument12 pagesFiverr ProjectAryan ZiaNo ratings yet

- Better Pililla Transport Service Cooperative Better Pililla Transport Service CooperativeDocument1 pageBetter Pililla Transport Service Cooperative Better Pililla Transport Service CooperativeHellen DeaNo ratings yet

- EFHDocument50 pagesEFHNeng GeulisNo ratings yet

- Decision Tree (Withholding Tax)Document1 pageDecision Tree (Withholding Tax)Loudie Ann MarcosNo ratings yet

- Appendices: Pasa Guwahali Puch: Bachat Tatha Reen Sahakari Sanstha LTDDocument5 pagesAppendices: Pasa Guwahali Puch: Bachat Tatha Reen Sahakari Sanstha LTDAnu ThapaNo ratings yet

- ILPA Best Practices Capital Calls and Distribution NoticeDocument23 pagesILPA Best Practices Capital Calls and Distribution NoticeMcAlpine PLLCNo ratings yet

- Business Terminology For Beginners 3.0 PDFDocument3 pagesBusiness Terminology For Beginners 3.0 PDFmacskafogoNo ratings yet

- IA3 Chapter 14 Problem 31Document3 pagesIA3 Chapter 14 Problem 31Bea TumulakNo ratings yet

- Cash Flow Analysis: ReviewDocument50 pagesCash Flow Analysis: ReviewDiich Tiari RachmadaniNo ratings yet

- Blank Scholarship Application Form PDFDocument4 pagesBlank Scholarship Application Form PDFRendi Pratama WNo ratings yet

- Ac PaperDocument6 pagesAc PaperAshwini SakpalNo ratings yet

- Group 7 - FPT - Financial AnalysisDocument2 pagesGroup 7 - FPT - Financial AnalysisNgọcAnhNo ratings yet

- Latest 2020 Budgeting-Calculator-Spreadsheet-with-Guidelines-ver-1-61Document4 pagesLatest 2020 Budgeting-Calculator-Spreadsheet-with-Guidelines-ver-1-61BhushanNo ratings yet

- Entrep 12Document4 pagesEntrep 12Rene Rulete MapaladNo ratings yet

- De - Fundamentals of AccountingDocument16 pagesDe - Fundamentals of Accountingcamilla100% (1)

- NCH Customer Support Services, Inc. PayslipDocument1 pageNCH Customer Support Services, Inc. PayslipTrainer EntainNo ratings yet

- Bir Ruling No. 108-93Document2 pagesBir Ruling No. 108-93saintkarriNo ratings yet

- Cash Flow ExampleDocument2 pagesCash Flow ExampleAlhassan ShakirNo ratings yet