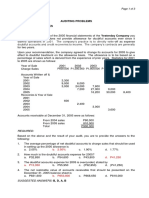

Download as docx, pdf, or txt

You might also like

- Petron-Corporation SwotDocument25 pagesPetron-Corporation SwotAhnJello100% (3)

- Kaizen - The Key To Japan's Competitive SuccesDocument8 pagesKaizen - The Key To Japan's Competitive SuccesHans Siregar67% (3)

- Managing Successful Projects with PRINCE2 2009 EditionFrom EverandManaging Successful Projects with PRINCE2 2009 EditionRating: 4 out of 5 stars4/5 (3)

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Chapters-1-10-Exam-Problem (2) Answer JessaDocument6 pagesChapters-1-10-Exam-Problem (2) Answer JessaLynssej BarbonNo ratings yet

- Problem No. 1: Ap - 1Stpb - 05.07Document10 pagesProblem No. 1: Ap - 1Stpb - 05.07AnnNo ratings yet

- Prac 1 - First Preboard - P2 65th NewDocument12 pagesPrac 1 - First Preboard - P2 65th NewArianne Llorente100% (1)

- AP-5906 ReceivablesDocument5 pagesAP-5906 Receivablesjhouvan100% (1)

- QuizDocument15 pagesQuizMark Domingo Mendoza100% (1)

- Financial AccountingDocument6 pagesFinancial AccountingFernando Alcantara100% (1)

- DocxDocument16 pagesDocxJustin NoladaNo ratings yet

- 5rd Batch - AP - Final Pre-Boards - EditedDocument11 pages5rd Batch - AP - Final Pre-Boards - EditedKim Cristian Maaño100% (1)

- Practical Accounting 2Document4 pagesPractical Accounting 2RajkumariNo ratings yet

- 37 - Income StatementDocument2 pages37 - Income StatementROMAR A. PIGANo ratings yet

- RESA 1st PBDocument9 pagesRESA 1st PBRay Mond0% (1)

- Q4Document10 pagesQ4Miles VicarsNo ratings yet

- This Is RealDocument17 pagesThis Is RealCheemee LiuNo ratings yet

- This Is RealDocument17 pagesThis Is RealCheemee LiuNo ratings yet

- Chapter 8 Audit of Stockholders' EquityDocument19 pagesChapter 8 Audit of Stockholders' EquitySteffany RoqueNo ratings yet

- Prac. 1Document15 pagesPrac. 1Lalaine De JesusNo ratings yet

- Problem No. 1: QuestionsDocument3 pagesProblem No. 1: QuestionsPamela Ledesma SusonNo ratings yet

- This Is RealDocument17 pagesThis Is RealCheemee LiuNo ratings yet

- Cpa Review School of The PhilippinesDocument11 pagesCpa Review School of The PhilippinesKCNo ratings yet

- Cash and Accrual QuizzerDocument5 pagesCash and Accrual QuizzerBabylyn NavarroNo ratings yet

- Practical Accounting 2Document4 pagesPractical Accounting 2James Perater100% (2)

- Morales, Jonalyn M.Document7 pagesMorales, Jonalyn M.Jonalyn MoralesNo ratings yet

- Chapter 9 Cash To Accrual Basis, Single EntryDocument24 pagesChapter 9 Cash To Accrual Basis, Single EntrySteffany RoqueNo ratings yet

- AP - Shareholders Equity PDFDocument5 pagesAP - Shareholders Equity PDFJasmin NgNo ratings yet

- Practical Accounting 2Document4 pagesPractical Accounting 2Steph BorinagaNo ratings yet

- S SdfafdafdafdafDocument8 pagesS SdfafdafdafdafMark Domingo MendozaNo ratings yet

- P2Document7 pagesP2chowchow123No ratings yet

- University of The Visayas Applied Auditing Audit of Liabilities Problem No. 1Document4 pagesUniversity of The Visayas Applied Auditing Audit of Liabilities Problem No. 1stillwinms100% (1)

- P1 2ND Preboard PDFDocument9 pagesP1 2ND Preboard PDFmaria evangelistaNo ratings yet

- Christine Joy Abad AssignmentDocument8 pagesChristine Joy Abad AssignmentEsse ValdezNo ratings yet

- Unit 9 Retained Earnings: Topic 2 - Appropriation and Quasi-ReorganizationDocument4 pagesUnit 9 Retained Earnings: Topic 2 - Appropriation and Quasi-ReorganizationRey HandumonNo ratings yet

- Problem 6Document7 pagesProblem 6Jaylord PidoNo ratings yet

- Audit of ReceivablesDocument3 pagesAudit of ReceivablesPb CunananNo ratings yet

- Ppe ApDocument5 pagesPpe ApGrace A. Manalo0% (1)

- Local Media3172437425380563588Document20 pagesLocal Media3172437425380563588Candy SchrendiNo ratings yet

- 5th Year Exam APMIDTERMDocument11 pages5th Year Exam APMIDTERMMark Domingo MendozaNo ratings yet

- AP 2007 (Shareholder's Equity) v.20Document4 pagesAP 2007 (Shareholder's Equity) v.20jalrestauroNo ratings yet

- Test Bank Chapter 3 Cost Volume Profit ADocument4 pagesTest Bank Chapter 3 Cost Volume Profit AKarlo D. ReclaNo ratings yet

- Cash Flow AnalysisDocument4 pagesCash Flow AnalysisMargin Pason RanjoNo ratings yet

- AP2 Quiz1 02112017Document3 pagesAP2 Quiz1 02112017PatOcampoNo ratings yet

- Cebu CPAR Center: C.C.P.A.R. Practical Accounting Problems 1 - PreweekDocument23 pagesCebu CPAR Center: C.C.P.A.R. Practical Accounting Problems 1 - PreweekIzzy BNo ratings yet

- AP 2006 (Liabilities) v2.0Document8 pagesAP 2006 (Liabilities) v2.0jalrestauroNo ratings yet

- College of Accountancy Final Examination Acctg 207A InstructionsDocument5 pagesCollege of Accountancy Final Examination Acctg 207A InstructionsCarmela TolinganNo ratings yet

- Chapter 7 Audit of LiabilitiesDocument26 pagesChapter 7 Audit of LiabilitiesSteffany Roque67% (3)

- MASDocument11 pagesMASgray downeyNo ratings yet

- Pre2 Module-Intangible Assets: Learning ObjectivesDocument9 pagesPre2 Module-Intangible Assets: Learning ObjectivesCyrine Grace DucogNo ratings yet

- ProblemsDocument46 pagesProblemsDan Andrei BongoNo ratings yet

- Auditing Theory and Problems (Qualifying Round) : Answer: DDocument15 pagesAuditing Theory and Problems (Qualifying Round) : Answer: DJohn Paulo SamonteNo ratings yet

- AP 5902 LiabilitiesDocument11 pagesAP 5902 LiabilitiesAnonymous Cd5GS3GM100% (1)

- Principles of Cash Flow Valuation: An Integrated Market-Based ApproachFrom EverandPrinciples of Cash Flow Valuation: An Integrated Market-Based ApproachRating: 3 out of 5 stars3/5 (3)

- The Valuation of Digital Intangibles: Technology, Marketing and InternetFrom EverandThe Valuation of Digital Intangibles: Technology, Marketing and InternetNo ratings yet

- Project Management Accounting: Budgeting, Tracking, and Reporting Costs and ProfitabilityFrom EverandProject Management Accounting: Budgeting, Tracking, and Reporting Costs and ProfitabilityRating: 4 out of 5 stars4/5 (2)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsFrom EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsNo ratings yet

- Wiley Practitioner's Guide to GAAS 2006: Covering all SASs, SSAEs, SSARSs, and InterpretationsFrom EverandWiley Practitioner's Guide to GAAS 2006: Covering all SASs, SSAEs, SSARSs, and InterpretationsRating: 2 out of 5 stars2/5 (2)

- Account-Based Marketing: How to Target and Engage the Companies That Will Grow Your RevenueFrom EverandAccount-Based Marketing: How to Target and Engage the Companies That Will Grow Your RevenueRating: 1 out of 5 stars1/5 (1)

- Forex PDFDocument5 pagesForex PDFErika LanezNo ratings yet

- Auditing Problems SummaryDocument16 pagesAuditing Problems SummaryErika LanezNo ratings yet

- MCQ - Corporation Law PDFDocument6 pagesMCQ - Corporation Law PDFErika LanezNo ratings yet

- MCQ - Negotiable Instruments PDFDocument9 pagesMCQ - Negotiable Instruments PDFErika LanezNo ratings yet

- Buss CombiDocument2 pagesBuss CombiErika LanezNo ratings yet

- Cost Accounting: Job Order Costing SystemDocument6 pagesCost Accounting: Job Order Costing SystemErika LanezNo ratings yet

- AudPW Theo PDFDocument18 pagesAudPW Theo PDFErika LanezNo ratings yet

- Business Combi 2Document1 pageBusiness Combi 2Erika LanezNo ratings yet

- AudPW ProbSln PDFDocument10 pagesAudPW ProbSln PDFErika LanezNo ratings yet

- AudPW Prob PDFDocument24 pagesAudPW Prob PDFErika LanezNo ratings yet

- AP 8507 Receivables PDFDocument6 pagesAP 8507 Receivables PDFErika LanezNo ratings yet

- AP 8505 Investments PDFDocument6 pagesAP 8505 Investments PDFErika LanezNo ratings yet

- AT.M-1405 Risk Assessment and Responses To RiskDocument10 pagesAT.M-1405 Risk Assessment and Responses To RiskErika LanezNo ratings yet

- AP 8502 LiabilitiesDocument8 pagesAP 8502 LiabilitiesErika LanezNo ratings yet

- Question 98 Exam KitDocument3 pagesQuestion 98 Exam KitGoi Cai EnNo ratings yet

- 1 MSA Syllabus Summer 2021Document6 pages1 MSA Syllabus Summer 2021Javed AnwarNo ratings yet

- Olson Harris LTDDocument7 pagesOlson Harris LTDthuanv2511No ratings yet

- What Factors Affect The EntrepreneurialDocument23 pagesWhat Factors Affect The Entrepreneurial02 Andrew Edwin yNo ratings yet

- CAA Finance Internship ReportDocument20 pagesCAA Finance Internship ReportNabeel Raja100% (4)

- How We Can Establish Good Relationship With Our SupplierDocument5 pagesHow We Can Establish Good Relationship With Our Supplierpatricia navasNo ratings yet

- Ugd Completion ReportDocument2 pagesUgd Completion Reportyadagirireddy bolluNo ratings yet

- Atrex ManualDocument455 pagesAtrex Manualblufoot36100% (1)

- Part 1 - Section D Cost Management 1.1 Cost Drivers and Cost FlowsDocument114 pagesPart 1 - Section D Cost Management 1.1 Cost Drivers and Cost FlowsGaleli PascualNo ratings yet

- JLL Jakarta Property Market Review 2q 2023 enDocument22 pagesJLL Jakarta Property Market Review 2q 2023 enSatrioMWibowoNo ratings yet

- Module AkmenDocument14 pagesModule AkmenNeshaNo ratings yet

- The Rajasthan State Cooperative Bank LTD.: (RSCB)Document61 pagesThe Rajasthan State Cooperative Bank LTD.: (RSCB)Bullzeye StrategyNo ratings yet

- 50 Procurement Formulas!Document9 pages50 Procurement Formulas!ebnugroho123No ratings yet

- PM Deck RentomojoDocument14 pagesPM Deck RentomojoAkshay Kumar SinghNo ratings yet

- Tugas Inggris Chapter 2Document5 pagesTugas Inggris Chapter 2Alam MahardikaNo ratings yet

- Mpu 22012 - Online Business Report - Jun2020Document2 pagesMpu 22012 - Online Business Report - Jun2020Linesh 2021No ratings yet

- National Internal Revenue Code of 1997Document95 pagesNational Internal Revenue Code of 1997Jocel Rose TorresNo ratings yet

- Arbitration Notice Prior To The Filing of Execution Petition Card No - XXXXXXXXXXXXXXX1709Document1 pageArbitration Notice Prior To The Filing of Execution Petition Card No - XXXXXXXXXXXXXXX1709Sanjay SandhuNo ratings yet

- 6183-FMDQ DQL - February 8, 2024 (Extended)Document4 pages6183-FMDQ DQL - February 8, 2024 (Extended)Matilda AdefalujoNo ratings yet

- What Is ERP? Guide To Enterprise Resource Planning SoftwareDocument23 pagesWhat Is ERP? Guide To Enterprise Resource Planning SoftwareAlex Muhwezi100% (1)

- 3-1 Additional Practice: NameDocument2 pages3-1 Additional Practice: NameProf. David G.No ratings yet

- Footwear Sectoral Report - 20032017Document49 pagesFootwear Sectoral Report - 20032017Gamer zoneNo ratings yet

- MAS 2PB Oct 2014Document12 pagesMAS 2PB Oct 2014Rhad Estoque100% (1)

- The Enterprise Software PlaybookDocument27 pagesThe Enterprise Software PlaybookTom LowNo ratings yet

- Michelin Case StudyDocument9 pagesMichelin Case StudyDivesh Mehta100% (1)

- 4th MA Organization and MangementDocument3 pages4th MA Organization and MangementLily Mar VinluanNo ratings yet

- Problem Set 2 - IFMPS2 (19SP) BKCDocument17 pagesProblem Set 2 - IFMPS2 (19SP) BKCLaurenNo ratings yet

- Swot Analysis Strengths 1. Quick ServiceDocument2 pagesSwot Analysis Strengths 1. Quick ServiceMigs MigsyNo ratings yet