Download as docx, pdf, or txt

You might also like

- The Star Mobile Marketing PlanDocument32 pagesThe Star Mobile Marketing Planweiyee_130% (1)

- A. Review Activity: B. Springboard/MotivationDocument3 pagesA. Review Activity: B. Springboard/MotivationsweetzelNo ratings yet

- Business Finance - 12 - Third - Week 4Document10 pagesBusiness Finance - 12 - Third - Week 4AngelicaHermoParasNo ratings yet

- Week 2Document5 pagesWeek 2Jemar Alipio100% (1)

- Daily Lesson Log: I. ObjectivesDocument4 pagesDaily Lesson Log: I. ObjectivesAngelicaHermoParasNo ratings yet

- Week 5 SCEDocument4 pagesWeek 5 SCEAngelicaHermoParas100% (1)

- Entrepreneurship Lesson 1Document46 pagesEntrepreneurship Lesson 1Mark Nelson A. MontemayorNo ratings yet

- September 2 2019Document3 pagesSeptember 2 2019Vinza AcobNo ratings yet

- DLL Fabm2Document2 pagesDLL Fabm2Dimple Grace AstorgaNo ratings yet

- FABM 2 - WEEK 2 - Louise Peralta - 11 - FairnessDocument3 pagesFABM 2 - WEEK 2 - Louise Peralta - 11 - FairnessLouise Joseph PeraltaNo ratings yet

- Grades 1 To 12 Daily Lesson Log School Franklin Delano Roosevelt Memorial School Grade Level Teacher Roman L. Espera Learning AreaDocument3 pagesGrades 1 To 12 Daily Lesson Log School Franklin Delano Roosevelt Memorial School Grade Level Teacher Roman L. Espera Learning AreaRoman EsperaNo ratings yet

- First Quarter Test Grade 12: Fundamental of ABM-2Document2 pagesFirst Quarter Test Grade 12: Fundamental of ABM-2manuel hipolitoNo ratings yet

- Fabm1 LPDocument2 pagesFabm1 LPRaul Soriano CabantingNo ratings yet

- Department of Education: Republic of The PhilippinesDocument2 pagesDepartment of Education: Republic of The PhilippinesCharly Mint Atamosa IsraelNo ratings yet

- Daily-Lesson LogDocument3 pagesDaily-Lesson LogFaith Tulmo De Dios100% (1)

- Bus Ethics and Responsbility Dll1Document18 pagesBus Ethics and Responsbility Dll1ClaireSobredilla-Juarez100% (3)

- Orgmngmt DLL Week 9Document4 pagesOrgmngmt DLL Week 9Rizalyn AbilaNo ratings yet

- Session 1 Session 2 Session 3 Session 4 Session 5: I. ObjectivesDocument3 pagesSession 1 Session 2 Session 3 Session 4 Session 5: I. ObjectivesLeighyo An MegastinoNo ratings yet

- Two-Way Table of SpecificationDocument2 pagesTwo-Way Table of SpecificationAngelicaHermoParasNo ratings yet

- Lesson Plan in FABM2Document2 pagesLesson Plan in FABM2Dimple Grace Astorga100% (1)

- DLL #6 ACCTNG. EquationDocument2 pagesDLL #6 ACCTNG. EquationCab VicNo ratings yet

- Daily Lesson Log/Plan: Monday Tuesday Wednesday ThursdayDocument2 pagesDaily Lesson Log/Plan: Monday Tuesday Wednesday ThursdayJovelyn Ignacio VinluanNo ratings yet

- Business Enterprise Simulation Bus PlanDocument24 pagesBusiness Enterprise Simulation Bus Planchristine j.No ratings yet

- Tos in FABM2 Second QuarterDocument2 pagesTos in FABM2 Second QuarterLAARNI REBONGNo ratings yet

- DLL Abm 1 Week 7-8Document4 pagesDLL Abm 1 Week 7-8Christopher Selebio100% (1)

- ABM - FABM11-IIIg - J - 28Document2 pagesABM - FABM11-IIIg - J - 28Mary Grace Pagalan Ladaran0% (1)

- DLL FABM Week17Document3 pagesDLL FABM Week17sweetzelNo ratings yet

- DLL Fundamentals May 2 - 6Document6 pagesDLL Fundamentals May 2 - 6Ma. Grace HermogenesNo ratings yet

- DLL-FABM2-ANALYSIS AND INTERPRETATION OF FINANCIAL ANALYSIS W2 LiquidityDocument4 pagesDLL-FABM2-ANALYSIS AND INTERPRETATION OF FINANCIAL ANALYSIS W2 LiquidityArianne Kay Javier-WabanNo ratings yet

- OM 5kkkDocument2 pagesOM 5kkkjcNo ratings yet

- 3FABM1 DLL Nov 20-23Document5 pages3FABM1 DLL Nov 20-23Marilyn Nelmida TamayoNo ratings yet

- Week 6 SCEDocument3 pagesWeek 6 SCEAngelicaHermoParasNo ratings yet

- LP in ABMDocument4 pagesLP in ABMGLICER MANGARON100% (1)

- Business Finance - 12 - Third - Week 5Document11 pagesBusiness Finance - 12 - Third - Week 5AngelicaHermoParasNo ratings yet

- Chapter 2 July 15-19Document3 pagesChapter 2 July 15-19Francesnova B. Dela PeñaNo ratings yet

- DLL 5 Di Pa TaposDocument3 pagesDLL 5 Di Pa TaposMay-Ann S. Cahilig0% (1)

- Detailed Lesson Plan in Fundamentals of AccountancyDocument5 pagesDetailed Lesson Plan in Fundamentals of AccountancyKrisha Joy CofinoNo ratings yet

- DLP EaaDocument6 pagesDLP EaaEmily A. AneñonNo ratings yet

- Fundamentals of Accountancy Business and Management 1 11 3 QuarterDocument4 pagesFundamentals of Accountancy Business and Management 1 11 3 QuarterPaulo Amposta CarpioNo ratings yet

- ABM 1 LP COT Aug 29Document6 pagesABM 1 LP COT Aug 29ßella DC Reponoya100% (1)

- 4 A'S Procedure:: Instructional PlanningDocument4 pages4 A'S Procedure:: Instructional PlanningMJ BenedictoNo ratings yet

- Lesson Plan in FABM2Document2 pagesLesson Plan in FABM2Dimple Grace AstorgaNo ratings yet

- Segmentation, Targeting, Positioning (STP)Document6 pagesSegmentation, Targeting, Positioning (STP)Surbhit SinhaNo ratings yet

- DLL Elective2 (Accounting)Document133 pagesDLL Elective2 (Accounting)Ythess NotcoidNo ratings yet

- Week 3 DLL Jan 15-19 XXXDocument7 pagesWeek 3 DLL Jan 15-19 XXXChristian TonogbanuaNo ratings yet

- DLL #5 Acctng.Document2 pagesDLL #5 Acctng.Cab VicNo ratings yet

- DLL #9 ACCTG. - Trial BalanceDocument3 pagesDLL #9 ACCTG. - Trial BalanceCab Vic100% (1)

- Dll. Business Finance Week 1Document9 pagesDll. Business Finance Week 1Mariz Bolongaita AñiroNo ratings yet

- DEMODocument27 pagesDEMORamil TabanaoNo ratings yet

- Budget of Lessons AccountingDocument2 pagesBudget of Lessons Accountingrhio amor100% (1)

- Detailed Lesson Plan EDITEDDocument6 pagesDetailed Lesson Plan EDITEDJoylen AcopNo ratings yet

- Daily Lesson Log: Abm - Fabm11-Ilib-C-17 Abm - Fabm11-Ilid-E-19 Abm - Fabm11-Iilb-C-17Document7 pagesDaily Lesson Log: Abm - Fabm11-Ilib-C-17 Abm - Fabm11-Ilid-E-19 Abm - Fabm11-Iilb-C-17Abegail PanangNo ratings yet

- Final Exam in Fundamental of Accounting, Business and Management 2 Grade 12 Name: - Date: - Section: - ScoreDocument2 pagesFinal Exam in Fundamental of Accounting, Business and Management 2 Grade 12 Name: - Date: - Section: - ScoreLeylaNo ratings yet

- ABM1 Week 3Document54 pagesABM1 Week 3Gladzangel LoricabvNo ratings yet

- Pre and Post of Accounting 2Document14 pagesPre and Post of Accounting 2Nancy AtentarNo ratings yet

- DLP 7 The Accounting EquationDocument13 pagesDLP 7 The Accounting EquationBela MationgNo ratings yet

- DLL - Abm Aug 21 - 25Document2 pagesDLL - Abm Aug 21 - 25Michelle Vinoray PascualNo ratings yet

- Abm Aom11 Iic e 28 AgcopraDocument5 pagesAbm Aom11 Iic e 28 AgcopraJarven SaguinNo ratings yet

- First Periodical ExaminationDocument1 pageFirst Periodical ExaminationJennyvee Motol HernandezNo ratings yet

- DLL Fabm1 Week1Document5 pagesDLL Fabm1 Week1Agatha AlcidNo ratings yet

- Lesson Plan in Accounting 2.3Document3 pagesLesson Plan in Accounting 2.3Jevie GibertasNo ratings yet

- E-Tech DLL Session 7 and 8Document4 pagesE-Tech DLL Session 7 and 8Jevie GibertasNo ratings yet

- Lesson Plan in Oral Com 1.6Document3 pagesLesson Plan in Oral Com 1.6Jevie Gibertas67% (3)

- E-Tech DLL Session 3 and 4Document4 pagesE-Tech DLL Session 3 and 4Jevie GibertasNo ratings yet

- Platform Plan FormatDocument6 pagesPlatform Plan FormatJevie GibertasNo ratings yet

- Lesson Plan in Oral Com 1.9Document2 pagesLesson Plan in Oral Com 1.9Jevie GibertasNo ratings yet

- Lesson Plan in Oral Communication 1.1Document3 pagesLesson Plan in Oral Communication 1.1Jevie GibertasNo ratings yet

- Lesson Plan in Oral Communication 1.3Document2 pagesLesson Plan in Oral Communication 1.3Jevie GibertasNo ratings yet

- Lesson Plan in Oral Com 1.5Document2 pagesLesson Plan in Oral Com 1.5Jevie GibertasNo ratings yet

- Lesson Plan in Accounting 2.3Document3 pagesLesson Plan in Accounting 2.3Jevie GibertasNo ratings yet

- Lesson Plan in Accounting 1.2Document3 pagesLesson Plan in Accounting 1.2Jevie GibertasNo ratings yet

- Lesson Plan in Accounting 1.1Document13 pagesLesson Plan in Accounting 1.1Jevie GibertasNo ratings yet

- Blended Learning-PHD EM-EDUC TECHDocument1 pageBlended Learning-PHD EM-EDUC TECHJevie GibertasNo ratings yet

- Blended Learning - PHD EM: Requirements For PortfolioDocument1 pageBlended Learning - PHD EM: Requirements For PortfolioJevie GibertasNo ratings yet

- Sample Contents of A Completed Feasibility StudyDocument4 pagesSample Contents of A Completed Feasibility StudyMatthew DasigNo ratings yet

- 2ND SEM ENTREPRENEURSHIP 4th GRADINGDocument13 pages2ND SEM ENTREPRENEURSHIP 4th GRADINGAnne Clarette MaligayaNo ratings yet

- InternationalStudentHealthFee Ish Ish X37003194374 Invoice 2024 01 05Document2 pagesInternationalStudentHealthFee Ish Ish X37003194374 Invoice 2024 01 05manmeetbirring2344No ratings yet

- Basel II and Banks in PakistanDocument67 pagesBasel II and Banks in PakistanSadaf FayyazNo ratings yet

- Liber8 Your BusinessDocument7 pagesLiber8 Your BusinessLaura HumphreysNo ratings yet

- Top North American 3PLs 2012Document40 pagesTop North American 3PLs 2012Đoàn Duy Tân100% (1)

- Test Bank For Management 10th Canadian Edition RobbinsDocument48 pagesTest Bank For Management 10th Canadian Edition RobbinsSuzanne Washington100% (38)

- Guideline CharterDocument5 pagesGuideline CharterNguyễn Tấn DũngNo ratings yet

- ADL Digital Bancassurance Sales 2023Document12 pagesADL Digital Bancassurance Sales 2023shohaebbNo ratings yet

- Modigliani and Miller (1958) - Assumptions: PerfectDocument27 pagesModigliani and Miller (1958) - Assumptions: PerfectCharlotte CaiNo ratings yet

- Peso Starter Fund Product Highlight Sheet - 082321Document11 pagesPeso Starter Fund Product Highlight Sheet - 082321Frost ByteNo ratings yet

- Priority Work Try To Find The PersonDocument47 pagesPriority Work Try To Find The PersonThủy Tiên NguyễnNo ratings yet

- Accountant S Ramshad CVDocument2 pagesAccountant S Ramshad CVramshadNo ratings yet

- Perjanjian Rakan Kongsi ExnessDocument3 pagesPerjanjian Rakan Kongsi ExnessmyexnessfxNo ratings yet

- CHAPTER 1. Multinational Finance Management OverviewDocument7 pagesCHAPTER 1. Multinational Finance Management OverviewTuấn LêNo ratings yet

- Using Assurance Models in IT Audit EngagementsDocument24 pagesUsing Assurance Models in IT Audit Engagementspreeti singhNo ratings yet

- CNCS Organization Assessment Tool Final 082517 508 0Document29 pagesCNCS Organization Assessment Tool Final 082517 508 0Nicole TaylorNo ratings yet

- TESDA Circular No. 007-2022Document11 pagesTESDA Circular No. 007-2022shellaNo ratings yet

- Iso 9001 1987Document9 pagesIso 9001 1987siti sarahNo ratings yet

- Sem 3 Managerial Economics Module 2 DEMAND FORCASTING TECHNIQUESDocument9 pagesSem 3 Managerial Economics Module 2 DEMAND FORCASTING TECHNIQUESAmos33No ratings yet

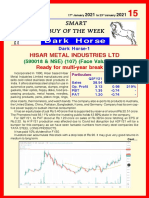

- Dark Horse-3Document2 pagesDark Horse-3kavin photosNo ratings yet

- Motorola: Making Quality A PriorityDocument19 pagesMotorola: Making Quality A PriorityKatya Avdieienko100% (1)

- JKT PVT LTDDocument8 pagesJKT PVT LTDSathiya YorathNo ratings yet

- SALN Form BlankDocument3 pagesSALN Form BlankIrish GarciaNo ratings yet

- Project Scope StatementDocument4 pagesProject Scope StatementAlan FirminoNo ratings yet

- Chapter 23Document21 pagesChapter 23RanDy JunaedyNo ratings yet

- Research FinalDocument18 pagesResearch FinalErwin Carl MendozaNo ratings yet

- C Khushi Agarwal 28Document15 pagesC Khushi Agarwal 28Khushi AgarwalNo ratings yet

- Enterprise Unified Process 1233990371415931 3Document14 pagesEnterprise Unified Process 1233990371415931 3jemaldaNo ratings yet