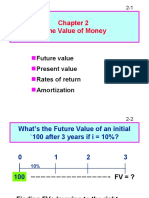

#Pvofguaranteedpaymentof10,000In5Years: PV PV

#Pvofguaranteedpaymentof10,000In5Years: PV PV

You might also like

- Chapter 2 CircuitDocument37 pagesChapter 2 CircuitKemal Selman Altun100% (1)

- Actuarial Notation: AnnuitiesDocument12 pagesActuarial Notation: AnnuitiesCallum Thain BlackNo ratings yet

- FNCE401v7 Assignment 1Document8 pagesFNCE401v7 Assignment 1David Eaton50% (2)

- ALMF March 2021 - SolutionsDocument11 pagesALMF March 2021 - Solutionssaad ansariNo ratings yet

- Time Value of MoneyDocument35 pagesTime Value of MoneyChimmy ParkNo ratings yet

- The Term Structure of Interest Rates: Denitsa StefanovaDocument41 pagesThe Term Structure of Interest Rates: Denitsa StefanovathofkampNo ratings yet

- Time Value of Money ConceptsDocument76 pagesTime Value of Money ConceptsAmit KaushikNo ratings yet

- 644 - Corporate Finance SolutionDocument7 pages644 - Corporate Finance Solutionrayan.wydouwNo ratings yet

- E136l7 Bond PricingDocument21 pagesE136l7 Bond PricingRahul PatelNo ratings yet

- Time Value For Money (Compatibility Mode)Document87 pagesTime Value For Money (Compatibility Mode)Azman ScxNo ratings yet

- Present ValueDocument38 pagesPresent Valuemarjannaseri77100% (1)

- Present Value Annuity Tables: What Is An Annuity Table?Document8 pagesPresent Value Annuity Tables: What Is An Annuity Table?Sharmin ReulaNo ratings yet

- Valuation of SecuritiesDocument71 pagesValuation of Securitieskuruvillaj2217No ratings yet

- Cfa CalculatorDocument33 pagesCfa CalculatorTanvir Ahmed Syed100% (2)

- Chap 002Document63 pagesChap 002محمد عقابنةNo ratings yet

- FPSB India - Retirement Module Sample Paper - Simplified Solution Using Calculator - March 2013Document9 pagesFPSB India - Retirement Module Sample Paper - Simplified Solution Using Calculator - March 2013Krupa VoraNo ratings yet

- FINA 2303 Chapter 4 Spring 2023Document37 pagesFINA 2303 Chapter 4 Spring 2023kalam huiNo ratings yet

- Mortgage MathDocument40 pagesMortgage MathAmit KumarNo ratings yet

- 2019 CorrigeDocument7 pages2019 Corrigeadrien.graffNo ratings yet

- 06 - Time Value of Money - 2Document77 pages06 - Time Value of Money - 2Salsabila AufaNo ratings yet

- Advanced Risk Mathematics Exam 21 - 22Document6 pagesAdvanced Risk Mathematics Exam 21 - 22Martin KasukuNo ratings yet

- 03 Assessing RiskDocument10 pages03 Assessing RiskKhalid WaheedNo ratings yet

- Financial Mathematics For Actuaries: Bond Yields and The Term StructureDocument55 pagesFinancial Mathematics For Actuaries: Bond Yields and The Term StructurephitoengNo ratings yet

- A Time Value of Money Primer: by David B. Hamm, MBA, CPA For Finance and Quantitative Methods ModulesDocument28 pagesA Time Value of Money Primer: by David B. Hamm, MBA, CPA For Finance and Quantitative Methods ModulesMSA-ACCA100% (2)

- Ch3 Time Value of MoneyDocument60 pagesCh3 Time Value of MoneyNiazi MustafaNo ratings yet

- Macro Questionss12Document8 pagesMacro Questionss12paripi99No ratings yet

- Financial ManagementDocument9 pagesFinancial Managementfirankisan1313No ratings yet

- Finc600 Chapter 2 PPTDocument41 pagesFinc600 Chapter 2 PPTmnh2006No ratings yet

- 14.02 Principles of Macroeconomics Fall 2009: Quiz 1 Thursday, October 8 7:30 PM - 9 PMDocument17 pages14.02 Principles of Macroeconomics Fall 2009: Quiz 1 Thursday, October 8 7:30 PM - 9 PMHenry CisnerosNo ratings yet

- UntitledDocument6 pagesUntitledShuHao ShiNo ratings yet

- CH 03Document86 pagesCH 03Ahsan AliNo ratings yet

- Reading 2 The Time Value of Money in Finance - AnswersDocument20 pagesReading 2 The Time Value of Money in Finance - Answersmenexe9137No ratings yet

- Feasibility Assignment 1&2 AnswersDocument12 pagesFeasibility Assignment 1&2 AnswersSouliman MuhammadNo ratings yet

- KWK 4th Append DDocument6 pagesKWK 4th Append DAnonymous O5asZmNo ratings yet

- Time Value of Money: Future Value Present Value Rates of Return AmortizationDocument47 pagesTime Value of Money: Future Value Present Value Rates of Return AmortizationJasprit DuggalNo ratings yet

- TVM 2021Document58 pagesTVM 2021mahendra pratap singhNo ratings yet

- FM 1 at MasiDocument7 pagesFM 1 at Masifirankisan1313No ratings yet

- Time Value of MoneyDocument29 pagesTime Value of Moneyrohan angelNo ratings yet

- Annuities Modeling With R: Giorgio Alfredo Spedicato, PH.D C.Stat ACASDocument34 pagesAnnuities Modeling With R: Giorgio Alfredo Spedicato, PH.D C.Stat ACAScyrine rienNo ratings yet

- 01-Problem Set Unit 02Document19 pages01-Problem Set Unit 02Tatiana BuruianaNo ratings yet

- EC303 Lecture Notes Part1Document14 pagesEC303 Lecture Notes Part1alamchowdhuryNo ratings yet

- Simple and Compound InterestDocument43 pagesSimple and Compound InterestAnne BergoniaNo ratings yet

- Macroeconomic Analysis 2003: ConsumptionDocument20 pagesMacroeconomic Analysis 2003: ConsumptionDeep Narayan MukhopadhyayNo ratings yet

- Basic 5Document2 pagesBasic 5Venky DNo ratings yet

- Annuities 2023Document70 pagesAnnuities 2023oceanflow.lrNo ratings yet

- Introduction To Financial Mathematics 2Document16 pagesIntroduction To Financial Mathematics 2Hedy Wenyan CenNo ratings yet

- Sample QuestionsDocument10 pagesSample QuestionsduongcamnhoNo ratings yet

- Financial Management 1Document20 pagesFinancial Management 1Sriram_VNo ratings yet

- Time Value of Money: Future Value Present Value Rates of Return AmortizationDocument83 pagesTime Value of Money: Future Value Present Value Rates of Return Amortizationbh5029No ratings yet

- AppcDocument47 pagesAppcdianNo ratings yet

- Q2 Quarterly Assessment Gen MathDocument5 pagesQ2 Quarterly Assessment Gen Mathrayanthony.tagadiadNo ratings yet

- CM1A - 221 - EXAM - Final CleanDocument6 pagesCM1A - 221 - EXAM - Final CleanShuvrajyoti BhattacharjeeNo ratings yet

- Corporate FinanceDocument87 pagesCorporate FinanceXiao PoNo ratings yet

- Exercises - Lecture 7 (A)Document7 pagesExercises - Lecture 7 (A)Samuel ChunNo ratings yet

- The Valuation of Long-Term SecuritiesDocument83 pagesThe Valuation of Long-Term SecuritiesJennyModiNo ratings yet

- Chapter 6Document132 pagesChapter 6Salim MattarNo ratings yet

- Financial Management ExercisesDocument11 pagesFinancial Management ExercisesDonat NabahunguNo ratings yet

- Financial Mathematics Course FIN 118 Unit Course 10 Number Unit Ordinary Annuity Annuity Due Unit SubjectDocument26 pagesFinancial Mathematics Course FIN 118 Unit Course 10 Number Unit Ordinary Annuity Annuity Due Unit Subjectayadi_ezer6795No ratings yet

- TVM-Practical QuestionsDocument6 pagesTVM-Practical Questionsparag nimjeNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Rakesh Khosla: Career HighlightsDocument3 pagesRakesh Khosla: Career HighlightsMuthu Srinivasan Muthu SelvamNo ratings yet

- Act Roi WebsitepayDocument2 pagesAct Roi Websitepaynagendra reddy panyamNo ratings yet

- SBI SME CAForm - New PDFDocument20 pagesSBI SME CAForm - New PDFBang Manish BangNo ratings yet

- Print DigestsDocument42 pagesPrint DigestsMirellaNo ratings yet

- HLS PON FR12 TheNewConflictMgmt 102021 EdsDocument10 pagesHLS PON FR12 TheNewConflictMgmt 102021 Edskarishma PradhanNo ratings yet

- F0606 Application For EmploymentDocument3 pagesF0606 Application For EmploymentIhwan AsrulNo ratings yet

- Astro InvasionDocument41 pagesAstro InvasionJohnNo ratings yet

- Sample Ws Chap 4Document52 pagesSample Ws Chap 4Thanh UyênNo ratings yet

- NYSDOT-Safety Information Management System: Average Accident Costs/Severity Distribution State Highways 2018Document4 pagesNYSDOT-Safety Information Management System: Average Accident Costs/Severity Distribution State Highways 2018jamcoso3240No ratings yet

- FULL TEXT - President Duterte's 2018 State of The Nation Address PDFDocument37 pagesFULL TEXT - President Duterte's 2018 State of The Nation Address PDFDarlene VenturaNo ratings yet

- Nano Ganesh (1) SadDocument2 pagesNano Ganesh (1) SadYaser ShaikhNo ratings yet

- Scott Cooley Lyric and Chord Songbook Volume OneDocument272 pagesScott Cooley Lyric and Chord Songbook Volume OneScott CooleyNo ratings yet

- FX2N-16DNET Devicenet User ManualDocument126 pagesFX2N-16DNET Devicenet User ManualNguyen QuanNo ratings yet

- Media ProjectDocument8 pagesMedia Projectruchika singhNo ratings yet

- Acrysol rm-8w 3Document4 pagesAcrysol rm-8w 3Forever0% (1)

- Judiciary: Structure, Organization and FunctioningDocument5 pagesJudiciary: Structure, Organization and FunctioningGaurav SinghNo ratings yet

- Dodge Charger 69 RT BlueDocument1 pageDodge Charger 69 RT BluekevinNo ratings yet

- Social Entrepeneurship Bootcamp SyllabusDocument7 pagesSocial Entrepeneurship Bootcamp SyllabusIsraelllNo ratings yet

- BC LetterDocument10 pagesBC LetterMehnoor SiddiquiNo ratings yet

- Machine Learning Primer 108796Document15 pagesMachine Learning Primer 108796Vinay Nagnath JokareNo ratings yet

- Chapter 5 Health Information SystemDocument36 pagesChapter 5 Health Information SystemAirishNo ratings yet

- InterviewDocument15 pagesInterviewRMRE UETNo ratings yet

- Special Continuous Probability DistributionsDocument11 pagesSpecial Continuous Probability DistributionsnofacejackNo ratings yet

- How Venture Capitalists Evaluate Potential Venture OpportunitiesDocument4 pagesHow Venture Capitalists Evaluate Potential Venture OpportunitiesARSHAD QAYUMNo ratings yet

- Talisic Vs Atty. Rinen Feb. 12,2014Document3 pagesTalisic Vs Atty. Rinen Feb. 12,2014Katharina CantaNo ratings yet

- Infosys: Case StudyDocument6 pagesInfosys: Case StudyShivam KhandelwalNo ratings yet

- I3 Marketing AspectDocument9 pagesI3 Marketing AspectJulliena BakersNo ratings yet

- List of NFPA Codes and StandardsDocument28 pagesList of NFPA Codes and StandardsjteranlavillaNo ratings yet

- Lis Pendens NoticeDocument2 pagesLis Pendens Noticemarc47No ratings yet

Download as pdf or txt

You might also like

- Chapter 2 CircuitDocument37 pagesChapter 2 CircuitKemal Selman Altun100% (1)

- Actuarial Notation: AnnuitiesDocument12 pagesActuarial Notation: AnnuitiesCallum Thain BlackNo ratings yet

- FNCE401v7 Assignment 1Document8 pagesFNCE401v7 Assignment 1David Eaton50% (2)

- ALMF March 2021 - SolutionsDocument11 pagesALMF March 2021 - Solutionssaad ansariNo ratings yet

- Time Value of MoneyDocument35 pagesTime Value of MoneyChimmy ParkNo ratings yet

- The Term Structure of Interest Rates: Denitsa StefanovaDocument41 pagesThe Term Structure of Interest Rates: Denitsa StefanovathofkampNo ratings yet

- Time Value of Money ConceptsDocument76 pagesTime Value of Money ConceptsAmit KaushikNo ratings yet

- 644 - Corporate Finance SolutionDocument7 pages644 - Corporate Finance Solutionrayan.wydouwNo ratings yet

- E136l7 Bond PricingDocument21 pagesE136l7 Bond PricingRahul PatelNo ratings yet

- Time Value For Money (Compatibility Mode)Document87 pagesTime Value For Money (Compatibility Mode)Azman ScxNo ratings yet

- Present ValueDocument38 pagesPresent Valuemarjannaseri77100% (1)

- Present Value Annuity Tables: What Is An Annuity Table?Document8 pagesPresent Value Annuity Tables: What Is An Annuity Table?Sharmin ReulaNo ratings yet

- Valuation of SecuritiesDocument71 pagesValuation of Securitieskuruvillaj2217No ratings yet

- Cfa CalculatorDocument33 pagesCfa CalculatorTanvir Ahmed Syed100% (2)

- Chap 002Document63 pagesChap 002محمد عقابنةNo ratings yet

- FPSB India - Retirement Module Sample Paper - Simplified Solution Using Calculator - March 2013Document9 pagesFPSB India - Retirement Module Sample Paper - Simplified Solution Using Calculator - March 2013Krupa VoraNo ratings yet

- FINA 2303 Chapter 4 Spring 2023Document37 pagesFINA 2303 Chapter 4 Spring 2023kalam huiNo ratings yet

- Mortgage MathDocument40 pagesMortgage MathAmit KumarNo ratings yet

- 2019 CorrigeDocument7 pages2019 Corrigeadrien.graffNo ratings yet

- 06 - Time Value of Money - 2Document77 pages06 - Time Value of Money - 2Salsabila AufaNo ratings yet

- Advanced Risk Mathematics Exam 21 - 22Document6 pagesAdvanced Risk Mathematics Exam 21 - 22Martin KasukuNo ratings yet

- 03 Assessing RiskDocument10 pages03 Assessing RiskKhalid WaheedNo ratings yet

- Financial Mathematics For Actuaries: Bond Yields and The Term StructureDocument55 pagesFinancial Mathematics For Actuaries: Bond Yields and The Term StructurephitoengNo ratings yet

- A Time Value of Money Primer: by David B. Hamm, MBA, CPA For Finance and Quantitative Methods ModulesDocument28 pagesA Time Value of Money Primer: by David B. Hamm, MBA, CPA For Finance and Quantitative Methods ModulesMSA-ACCA100% (2)

- Ch3 Time Value of MoneyDocument60 pagesCh3 Time Value of MoneyNiazi MustafaNo ratings yet

- Macro Questionss12Document8 pagesMacro Questionss12paripi99No ratings yet

- Financial ManagementDocument9 pagesFinancial Managementfirankisan1313No ratings yet

- Finc600 Chapter 2 PPTDocument41 pagesFinc600 Chapter 2 PPTmnh2006No ratings yet

- 14.02 Principles of Macroeconomics Fall 2009: Quiz 1 Thursday, October 8 7:30 PM - 9 PMDocument17 pages14.02 Principles of Macroeconomics Fall 2009: Quiz 1 Thursday, October 8 7:30 PM - 9 PMHenry CisnerosNo ratings yet

- UntitledDocument6 pagesUntitledShuHao ShiNo ratings yet

- CH 03Document86 pagesCH 03Ahsan AliNo ratings yet

- Reading 2 The Time Value of Money in Finance - AnswersDocument20 pagesReading 2 The Time Value of Money in Finance - Answersmenexe9137No ratings yet

- Feasibility Assignment 1&2 AnswersDocument12 pagesFeasibility Assignment 1&2 AnswersSouliman MuhammadNo ratings yet

- KWK 4th Append DDocument6 pagesKWK 4th Append DAnonymous O5asZmNo ratings yet

- Time Value of Money: Future Value Present Value Rates of Return AmortizationDocument47 pagesTime Value of Money: Future Value Present Value Rates of Return AmortizationJasprit DuggalNo ratings yet

- TVM 2021Document58 pagesTVM 2021mahendra pratap singhNo ratings yet

- FM 1 at MasiDocument7 pagesFM 1 at Masifirankisan1313No ratings yet

- Time Value of MoneyDocument29 pagesTime Value of Moneyrohan angelNo ratings yet

- Annuities Modeling With R: Giorgio Alfredo Spedicato, PH.D C.Stat ACASDocument34 pagesAnnuities Modeling With R: Giorgio Alfredo Spedicato, PH.D C.Stat ACAScyrine rienNo ratings yet

- 01-Problem Set Unit 02Document19 pages01-Problem Set Unit 02Tatiana BuruianaNo ratings yet

- EC303 Lecture Notes Part1Document14 pagesEC303 Lecture Notes Part1alamchowdhuryNo ratings yet

- Simple and Compound InterestDocument43 pagesSimple and Compound InterestAnne BergoniaNo ratings yet

- Macroeconomic Analysis 2003: ConsumptionDocument20 pagesMacroeconomic Analysis 2003: ConsumptionDeep Narayan MukhopadhyayNo ratings yet

- Basic 5Document2 pagesBasic 5Venky DNo ratings yet

- Annuities 2023Document70 pagesAnnuities 2023oceanflow.lrNo ratings yet

- Introduction To Financial Mathematics 2Document16 pagesIntroduction To Financial Mathematics 2Hedy Wenyan CenNo ratings yet

- Sample QuestionsDocument10 pagesSample QuestionsduongcamnhoNo ratings yet

- Financial Management 1Document20 pagesFinancial Management 1Sriram_VNo ratings yet

- Time Value of Money: Future Value Present Value Rates of Return AmortizationDocument83 pagesTime Value of Money: Future Value Present Value Rates of Return Amortizationbh5029No ratings yet

- AppcDocument47 pagesAppcdianNo ratings yet

- Q2 Quarterly Assessment Gen MathDocument5 pagesQ2 Quarterly Assessment Gen Mathrayanthony.tagadiadNo ratings yet

- CM1A - 221 - EXAM - Final CleanDocument6 pagesCM1A - 221 - EXAM - Final CleanShuvrajyoti BhattacharjeeNo ratings yet

- Corporate FinanceDocument87 pagesCorporate FinanceXiao PoNo ratings yet

- Exercises - Lecture 7 (A)Document7 pagesExercises - Lecture 7 (A)Samuel ChunNo ratings yet

- The Valuation of Long-Term SecuritiesDocument83 pagesThe Valuation of Long-Term SecuritiesJennyModiNo ratings yet

- Chapter 6Document132 pagesChapter 6Salim MattarNo ratings yet

- Financial Management ExercisesDocument11 pagesFinancial Management ExercisesDonat NabahunguNo ratings yet

- Financial Mathematics Course FIN 118 Unit Course 10 Number Unit Ordinary Annuity Annuity Due Unit SubjectDocument26 pagesFinancial Mathematics Course FIN 118 Unit Course 10 Number Unit Ordinary Annuity Annuity Due Unit Subjectayadi_ezer6795No ratings yet

- TVM-Practical QuestionsDocument6 pagesTVM-Practical Questionsparag nimjeNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Rakesh Khosla: Career HighlightsDocument3 pagesRakesh Khosla: Career HighlightsMuthu Srinivasan Muthu SelvamNo ratings yet

- Act Roi WebsitepayDocument2 pagesAct Roi Websitepaynagendra reddy panyamNo ratings yet

- SBI SME CAForm - New PDFDocument20 pagesSBI SME CAForm - New PDFBang Manish BangNo ratings yet

- Print DigestsDocument42 pagesPrint DigestsMirellaNo ratings yet

- HLS PON FR12 TheNewConflictMgmt 102021 EdsDocument10 pagesHLS PON FR12 TheNewConflictMgmt 102021 Edskarishma PradhanNo ratings yet

- F0606 Application For EmploymentDocument3 pagesF0606 Application For EmploymentIhwan AsrulNo ratings yet

- Astro InvasionDocument41 pagesAstro InvasionJohnNo ratings yet

- Sample Ws Chap 4Document52 pagesSample Ws Chap 4Thanh UyênNo ratings yet

- NYSDOT-Safety Information Management System: Average Accident Costs/Severity Distribution State Highways 2018Document4 pagesNYSDOT-Safety Information Management System: Average Accident Costs/Severity Distribution State Highways 2018jamcoso3240No ratings yet

- FULL TEXT - President Duterte's 2018 State of The Nation Address PDFDocument37 pagesFULL TEXT - President Duterte's 2018 State of The Nation Address PDFDarlene VenturaNo ratings yet

- Nano Ganesh (1) SadDocument2 pagesNano Ganesh (1) SadYaser ShaikhNo ratings yet

- Scott Cooley Lyric and Chord Songbook Volume OneDocument272 pagesScott Cooley Lyric and Chord Songbook Volume OneScott CooleyNo ratings yet

- FX2N-16DNET Devicenet User ManualDocument126 pagesFX2N-16DNET Devicenet User ManualNguyen QuanNo ratings yet

- Media ProjectDocument8 pagesMedia Projectruchika singhNo ratings yet

- Acrysol rm-8w 3Document4 pagesAcrysol rm-8w 3Forever0% (1)

- Judiciary: Structure, Organization and FunctioningDocument5 pagesJudiciary: Structure, Organization and FunctioningGaurav SinghNo ratings yet

- Dodge Charger 69 RT BlueDocument1 pageDodge Charger 69 RT BluekevinNo ratings yet

- Social Entrepeneurship Bootcamp SyllabusDocument7 pagesSocial Entrepeneurship Bootcamp SyllabusIsraelllNo ratings yet

- BC LetterDocument10 pagesBC LetterMehnoor SiddiquiNo ratings yet

- Machine Learning Primer 108796Document15 pagesMachine Learning Primer 108796Vinay Nagnath JokareNo ratings yet

- Chapter 5 Health Information SystemDocument36 pagesChapter 5 Health Information SystemAirishNo ratings yet

- InterviewDocument15 pagesInterviewRMRE UETNo ratings yet

- Special Continuous Probability DistributionsDocument11 pagesSpecial Continuous Probability DistributionsnofacejackNo ratings yet

- How Venture Capitalists Evaluate Potential Venture OpportunitiesDocument4 pagesHow Venture Capitalists Evaluate Potential Venture OpportunitiesARSHAD QAYUMNo ratings yet

- Talisic Vs Atty. Rinen Feb. 12,2014Document3 pagesTalisic Vs Atty. Rinen Feb. 12,2014Katharina CantaNo ratings yet

- Infosys: Case StudyDocument6 pagesInfosys: Case StudyShivam KhandelwalNo ratings yet

- I3 Marketing AspectDocument9 pagesI3 Marketing AspectJulliena BakersNo ratings yet

- List of NFPA Codes and StandardsDocument28 pagesList of NFPA Codes and StandardsjteranlavillaNo ratings yet

- Lis Pendens NoticeDocument2 pagesLis Pendens Noticemarc47No ratings yet