Download as pdf or txt

You might also like

- Search For The Graf SpeeDocument5 pagesSearch For The Graf SpeeChristina Chavez Clinton0% (1)

- Annex Table 38. Export Volumes of Goods and Services: Source: OECD Economic Outlook 88 DatabaseDocument17 pagesAnnex Table 38. Export Volumes of Goods and Services: Source: OECD Economic Outlook 88 DatabaseRaghvendra NarayanNo ratings yet

- Forecast Tables EN PDFDocument2 pagesForecast Tables EN PDFSyed Maratab AliNo ratings yet

- Ip183 - en - Statistical AnnexDocument3 pagesIp183 - en - Statistical AnnexPeter DerdakNo ratings yet

- Trouble in The AirDocument19 pagesTrouble in The AirAmiranNo ratings yet

- Table 1: Health Expenditure in OECD Countries, 2000 To 2006Document8 pagesTable 1: Health Expenditure in OECD Countries, 2000 To 2006snamicampaniaNo ratings yet

- Berenberg Global ForecastsDocument15 pagesBerenberg Global ForecastsbobmezzNo ratings yet

- File 0081 PDFDocument1 pageFile 0081 PDFEd ZNo ratings yet

- CREDIT SUISSE ECONOMICS - Global Economics Quarterly - The Worst Is Yet To Come (28sep2022)Document45 pagesCREDIT SUISSE ECONOMICS - Global Economics Quarterly - The Worst Is Yet To Come (28sep2022)ikaNo ratings yet

- Table 53: Taxes On Capital As % of GDP - TotalDocument30 pagesTable 53: Taxes On Capital As % of GDP - TotalRalwkwtza NykoNo ratings yet

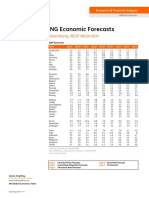

- October 2022 INGF 3Document7 pagesOctober 2022 INGF 3Daniel SbizzaroNo ratings yet

- IMF - WEO - 202004 - Statistical Appendix - Tables B PDFDocument8 pagesIMF - WEO - 202004 - Statistical Appendix - Tables B PDFAnna VassilovskiNo ratings yet

- 161/2009 - 13 November 2009Document2 pages161/2009 - 13 November 2009Dennik SMENo ratings yet

- Euro Area and EU27 GDP Up by 1.0%Document6 pagesEuro Area and EU27 GDP Up by 1.0%qtipxNo ratings yet

- 22/2010 - 12 February 2010Document2 pages22/2010 - 12 February 2010Dennik SMENo ratings yet

- Note On Stock of Liabilities of Trade Credits and AdvancesDocument2 pagesNote On Stock of Liabilities of Trade Credits and Advancesathanasios_syrakisNo ratings yet

- GDP Up by 0.6% in Both The Euro Area and The EU28: Flash Estimate For The Second Quarter of 2017Document3 pagesGDP Up by 0.6% in Both The Euro Area and The EU28: Flash Estimate For The Second Quarter of 2017loginxscribdNo ratings yet

- HDP EuDocument2 pagesHDP EuDennik SMENo ratings yet

- 2 13112020 Ap enDocument1 page2 13112020 Ap enWeb AdevarulNo ratings yet

- CPI 2009 Regional Highlights EU WE en - Corruption Perceptions Index 2009 - Regional Highlights For The European Union and Western EuropeDocument2 pagesCPI 2009 Regional Highlights EU WE en - Corruption Perceptions Index 2009 - Regional Highlights For The European Union and Western EuropeJon C.No ratings yet

- TED GrowthAccountingTotalFactorProductivity1990 2014Document136 pagesTED GrowthAccountingTotalFactorProductivity1990 2014Alejandro Alfaro AcoNo ratings yet

- BP Statistical ReviewDocument158 pagesBP Statistical Reviewbrayan7uribeNo ratings yet

- Corruption Percepttion IndexDocument9 pagesCorruption Percepttion IndexKalvin AmosNo ratings yet

- BP Stats Review 2018 All DataDocument111 pagesBP Stats Review 2018 All DataNeeraj YadavNo ratings yet

- Business Investment: Recent Performance and Some Implications For Policy Robert Ford and Pierre PoretDocument53 pagesBusiness Investment: Recent Performance and Some Implications For Policy Robert Ford and Pierre PoretAbdena GutuNo ratings yet

- Annual Percent Change, Unless Noted OtherwiseDocument1 pageAnnual Percent Change, Unless Noted OtherwiseFz DNo ratings yet

- Measles 2019 AerDocument9 pagesMeasles 2019 AerJose BritesNo ratings yet

- Economic Update and Outlook: Key Issues For 2011Document21 pagesEconomic Update and Outlook: Key Issues For 2011TrevorCrouchNo ratings yet

- The European Foundry Industry 2019 Annual Statistics and National Reports 1Document112 pagesThe European Foundry Industry 2019 Annual Statistics and National Reports 1Ryan KnightNo ratings yet

- Chapter 01Document117 pagesChapter 01Sadi SonmezNo ratings yet

- 6fc55141 enDocument2 pages6fc55141 enTalila SidaNo ratings yet

- Statistica EurostatDocument5 pagesStatistica Eurostatrezeanumaria22No ratings yet

- 2 13052011 Ap enDocument2 pages2 13052011 Ap enShruthi JayaramNo ratings yet

- Ae8c39ec enDocument22 pagesAe8c39ec enStathis MetsovitisNo ratings yet

- Laju Pertumbuhan Produk Domestik Bruto Per Kapita Beberapa Negara Menurut Harga Konstan (Persen), 2000-2015Document4 pagesLaju Pertumbuhan Produk Domestik Bruto Per Kapita Beberapa Negara Menurut Harga Konstan (Persen), 2000-2015Rahayu SetianingsihNo ratings yet

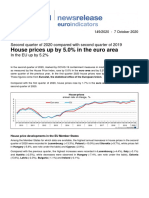

- House Prices Up by 5.0% in The Euro Area: Second Quarter of 2020 Compared With Second Quarter of 2019 Intheeuupby5.2%Document3 pagesHouse Prices Up by 5.0% in The Euro Area: Second Quarter of 2020 Compared With Second Quarter of 2019 Intheeuupby5.2%PapasimaNo ratings yet

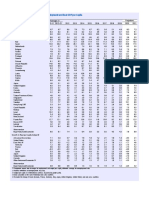

- (Percent Change, Unless Otherwise Noted) : Table 1.1. Overview of The World Economic Outlook ProjectionsDocument3 pages(Percent Change, Unless Otherwise Noted) : Table 1.1. Overview of The World Economic Outlook ProjectionsSathish KumarNo ratings yet

- C Cêu KH CH Quèc Tõ ®õn Viöt Nam Tõ N M 2000 ®õn N M 2010Document3 pagesC Cêu KH CH Quèc Tõ ®õn Viöt Nam Tõ N M 2000 ®õn N M 2010Thuận TrầnNo ratings yet

- 2023-03-01 - ESRB - 2023 EBA Real GVA by Sector (Updated 1 March 2023)Document16 pages2023-03-01 - ESRB - 2023 EBA Real GVA by Sector (Updated 1 March 2023)krisNiswanderNo ratings yet

- GDP ProjectDocument2 pagesGDP Projectnghiah5No ratings yet

- CH1 The National EconomyDocument40 pagesCH1 The National EconomyCollège YvemarcelNo ratings yet

- European Economy European EconomyDocument17 pagesEuropean Economy European EconomyChandrashekhara V GNo ratings yet

- 2021 06 22 Merelli Macro ScenarioDocument66 pages2021 06 22 Merelli Macro ScenarioVito GiacovelliNo ratings yet

- EO PresentationDocument23 pagesEO PresentationjrmiztliNo ratings yet

- Hiv and Aids: Surveillance ReportDocument7 pagesHiv and Aids: Surveillance ReportFrancisca BallesterosNo ratings yet

- Table 1.1. Overview of The World Economic Outlook Projections (Percent Change, Unless Noted Otherwise)Document2 pagesTable 1.1. Overview of The World Economic Outlook Projections (Percent Change, Unless Noted Otherwise)sy yusufNo ratings yet

- Práctica KNNDocument2 pagesPráctica KNNCarlos CanoNo ratings yet

- BP Statistical Review of World Energy 2017 Underpinning DataDocument69 pagesBP Statistical Review of World Energy 2017 Underpinning DatadairandexNo ratings yet

- 2 31072023 BP enDocument3 pages2 31072023 BP enDaniel AyresNo ratings yet

- Euro Area GDP Stable and EU27 GDP Up by 0.1%Document10 pagesEuro Area GDP Stable and EU27 GDP Up by 0.1%qtipxNo ratings yet

- Saldo Publico: Spain - 1 - 0,6 - 0,5 - 0,2 - 0,4 1 2 1,9 - 4,1Document3 pagesSaldo Publico: Spain - 1 - 0,6 - 0,5 - 0,2 - 0,4 1 2 1,9 - 4,1Ernest YouverNo ratings yet

- Economic Out Look 190603Document14 pagesEconomic Out Look 190603sirdquantsNo ratings yet

- EBRDDocument1 pageEBRDDennik SME100% (1)

- BP Statistical Review of World Energy 2017 Underpinning DataDocument70 pagesBP Statistical Review of World Energy 2017 Underpinning DataThales MacêdoNo ratings yet

- Dengue: Surveillance ReportDocument7 pagesDengue: Surveillance Reportramona donisaNo ratings yet

- Unprecedented Fall in OECD GDP by 9.8% in Q2 2020Document2 pagesUnprecedented Fall in OECD GDP by 9.8% in Q2 2020Βασίλης ΒήτταςNo ratings yet

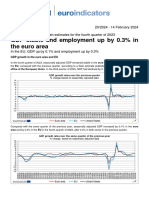

- GDP Stable and Employment Up by 0.3% in The Euro AreaDocument4 pagesGDP Stable and Employment Up by 0.3% in The Euro Areagustavo.kahilNo ratings yet

- Inflació 1Document2 pagesInflació 1Maria José RodríguezNo ratings yet

- Seasonally Adjusted Unemployment, Totals:: Data Not Available January 2021Document6 pagesSeasonally Adjusted Unemployment, Totals:: Data Not Available January 2021Robert SzymańskiNo ratings yet

- BP Stats Review 2018 Renewable EnergyDocument11 pagesBP Stats Review 2018 Renewable EnergyANA PAULA MODESTONo ratings yet

- Autumn Woods Bylaws15 12 9Document7 pagesAutumn Woods Bylaws15 12 9api-284745372No ratings yet

- Brief: SDG Priorities For BangladeshDocument3 pagesBrief: SDG Priorities For BangladeshMrz AshikNo ratings yet

- Lawrence Connell v. Linda Ammons - Court Opinion Denying Motion To Change VenueDocument3 pagesLawrence Connell v. Linda Ammons - Court Opinion Denying Motion To Change VenueLegal InsurrectionNo ratings yet

- As 3711.1-2000 Freight Containers Classification Dimensions and RatingsDocument8 pagesAs 3711.1-2000 Freight Containers Classification Dimensions and RatingsSAI Global - APACNo ratings yet

- Post DevelopmentDocument35 pagesPost DevelopmentAminul QuayyumNo ratings yet

- UntitledDocument2 pagesUntitledapi-1549565660% (1)

- UntitledDocument617 pagesUntitledMihaela SanduNo ratings yet

- Learning Module For Grade 11 Introduction To The World Religions and Belief SystemsDocument10 pagesLearning Module For Grade 11 Introduction To The World Religions and Belief SystemsJaypee DaliasenNo ratings yet

- Inclusive Education in JapanDocument12 pagesInclusive Education in JapanRominaNo ratings yet

- Grade Five 2nd Assessment 2023Document5 pagesGrade Five 2nd Assessment 2023Chisom NwekeNo ratings yet

- DOH-HHRDB Healthcare Workers (Physicians)Document41 pagesDOH-HHRDB Healthcare Workers (Physicians)VERA FilesNo ratings yet

- Ictk MCQ PDFDocument24 pagesIctk MCQ PDFExtra Account100% (1)

- Computer AssociatesDocument18 pagesComputer AssociatesRosel RicafortNo ratings yet

- Robert Kuttner On The Aftermath of Debt Bubbles and Restructuring DebtsDocument1 pageRobert Kuttner On The Aftermath of Debt Bubbles and Restructuring DebtsmrwonkishNo ratings yet

- Data InterpretationDocument44 pagesData InterpretationSwati Choudhary100% (2)

- A Development Bank Is A Polygonal Development Finance Institution Devoted To Improving The Social and Monetary Development of Its Associate NationsDocument2 pagesA Development Bank Is A Polygonal Development Finance Institution Devoted To Improving The Social and Monetary Development of Its Associate NationsAjay SolankiNo ratings yet

- Un Mundo Donde Quepan Muchos Mundos A Po PDFDocument42 pagesUn Mundo Donde Quepan Muchos Mundos A Po PDFJorge Acosta Jr.No ratings yet

- Feb 05 InprocDocument740 pagesFeb 05 InprocaptureincNo ratings yet

- CSE40419 - Ethics (Cases)Document16 pagesCSE40419 - Ethics (Cases)Gabriel WongNo ratings yet

- 65 Royale Homes Mktg. Corp. v. Fidel P. Alcantara, G.R. No. 195190, July 28, 2014Document30 pages65 Royale Homes Mktg. Corp. v. Fidel P. Alcantara, G.R. No. 195190, July 28, 2014joyeduardoNo ratings yet

- Environment Position PaperDocument6 pagesEnvironment Position PaperJenlisa KimanobanNo ratings yet

- Spes Reviewer 2023Document3 pagesSpes Reviewer 2023moneciaashleycate100% (2)

- FINALLY DTOT Matrix KindergartenDocument3 pagesFINALLY DTOT Matrix KindergartenJaymar Kevin PadayaoNo ratings yet

- The Romantic Movement As ADocument7 pagesThe Romantic Movement As ATANBIR RAHAMANNo ratings yet

- ContractDocument3 pagesContractrodelyn ubalubaoNo ratings yet

- Zahir Hse OfficerDocument20 pagesZahir Hse Officerimdadullahkhan151No ratings yet

- JAAF Camouflage Markings World War II PDFDocument208 pagesJAAF Camouflage Markings World War II PDFVali Vali100% (10)

- 09 U.S. v. Bonifacio, G.R. No. L-10563, 2 March 1916Document4 pages09 U.S. v. Bonifacio, G.R. No. L-10563, 2 March 1916Andrei Da JoseNo ratings yet

- Drupal DevOpsDocument2 pagesDrupal DevOpsIon ArseneNo ratings yet