Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Quiz#1 - Accounting and FinanceDocument19 pagesQuiz#1 - Accounting and Financehakimuh91No ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Chapter 04 AnsDocument38 pagesChapter 04 AnsLuisLoNo ratings yet

- FAR Module (Partnership Dissolution & Liquidation)Document38 pagesFAR Module (Partnership Dissolution & Liquidation)Angelo Bagolboc60% (5)

- Problem SetDocument2 pagesProblem SetABDUL RAHIM G. ACOONNo ratings yet

- PrelimsDocument2 pagesPrelimsABDUL RAHIM G. ACOONNo ratings yet

- Cost AccountingDocument3 pagesCost AccountingABDUL RAHIM G. ACOONNo ratings yet

- Cases For Negotiable Instruments LawDocument1 pageCases For Negotiable Instruments LawABDUL RAHIM G. ACOONNo ratings yet

- Administrative Proceedings Case Digests ABSDocument22 pagesAdministrative Proceedings Case Digests ABSABDUL RAHIM G. ACOONNo ratings yet

- Election Offenses: Section 27. Election Offenses. - in Addition To The Prohibited Acts and Election OffensesDocument4 pagesElection Offenses: Section 27. Election Offenses. - in Addition To The Prohibited Acts and Election OffensesABDUL RAHIM G. ACOONNo ratings yet

- Director, LMB V. Ca and Aquilino L. Carino G.R. No. 112567 February 7, 2000Document6 pagesDirector, LMB V. Ca and Aquilino L. Carino G.R. No. 112567 February 7, 2000ABDUL RAHIM G. ACOONNo ratings yet

- Cases For Digest LTDDocument1 pageCases For Digest LTDABDUL RAHIM G. ACOONNo ratings yet

- Activity #1: Naming of Words: ST THDocument15 pagesActivity #1: Naming of Words: ST THABDUL RAHIM G. ACOONNo ratings yet

- Corporate Tax - UAEDocument48 pagesCorporate Tax - UAEUmair BaigNo ratings yet

- Chapter 18 QuizDocument2 pagesChapter 18 QuizJamaica DavidNo ratings yet

- The Year: Add: Non-Allowable Depreciation 12,497Document23 pagesThe Year: Add: Non-Allowable Depreciation 12,497peter richNo ratings yet

- Business Association OutlineDocument134 pagesBusiness Association OutlineSean BarlowNo ratings yet

- IAS 12 BinderDocument20 pagesIAS 12 BinderUmer Shah100% (1)

- L&T Detailed Policy - SMB - Credit Norms - DSA-DST - July 2022Document15 pagesL&T Detailed Policy - SMB - Credit Norms - DSA-DST - July 2022Tejas GaubaNo ratings yet

- Managerial Accounting 13th Edition by Warren Reeve and Duchac Solution ManualDocument16 pagesManagerial Accounting 13th Edition by Warren Reeve and Duchac Solution Manualroger100% (39)

- Assessment 3 Tax 1Document5 pagesAssessment 3 Tax 1Judy Ann GacetaNo ratings yet

- 7.9.15 MPAC SlidesDocument100 pages7.9.15 MPAC SlidesNhorelajne ManaogNo ratings yet

- ACG5175-Problem 7.5Document3 pagesACG5175-Problem 7.5Justine JacksonNo ratings yet

- P K Jain Surendra S Yadav Alok Dixit Derrivative Markets in IndiaDocument211 pagesP K Jain Surendra S Yadav Alok Dixit Derrivative Markets in Indiaadv mishraNo ratings yet

- PartnershipDocument24 pagesPartnershipEthan75% (4)

- Assets, Liabilities and The Balance SheetDocument13 pagesAssets, Liabilities and The Balance SheetMARIA-MIRUNA IVĂNESCUNo ratings yet

- 2023 CMCI LDCS Annex A & B - TemplateDocument4 pages2023 CMCI LDCS Annex A & B - TemplateLanie LeiNo ratings yet

- Vue Cinema FSDocument168 pagesVue Cinema FSYeshwanth LeoNo ratings yet

- SOLUTION MAF503 - JUN 2015 AmmendDocument8 pagesSOLUTION MAF503 - JUN 2015 Ammendanis izzatiNo ratings yet

- Nur Amaliyah - 041811333032 AKLDocument5 pagesNur Amaliyah - 041811333032 AKLNur AmaliyahNo ratings yet

- Key Information Memorandum & Common Application Form: Equity FundDocument11 pagesKey Information Memorandum & Common Application Form: Equity FundbapisroyNo ratings yet

- Accounting Question Paper Co Operative Accounting of Campus3 1Document5 pagesAccounting Question Paper Co Operative Accounting of Campus3 1Mengsteab GebreslassieNo ratings yet

- Module 4 - 7 - Different Ways of Calculating WACCDocument10 pagesModule 4 - 7 - Different Ways of Calculating WACCBaher WilliamNo ratings yet

- AP DLSA 05 PPE For DistributionDocument10 pagesAP DLSA 05 PPE For DistributionStela Marie CarandangNo ratings yet

- Methods of Valuation of FirmsDocument90 pagesMethods of Valuation of Firmsmuskaan bhadadaNo ratings yet

- XBRL Financial Statements Duly Authenticated As Per Section 134 (Including BoardDocument84 pagesXBRL Financial Statements Duly Authenticated As Per Section 134 (Including BoardBhavik SaliaNo ratings yet

- DSC, SEC & DSE (III & IV Sem)Document21 pagesDSC, SEC & DSE (III & IV Sem)Shakti S SarvadeNo ratings yet

- Nawaz - My India ProjectDocument23 pagesNawaz - My India ProjectriyaNo ratings yet

- Equitas SFB Initial (Geojit)Document11 pagesEquitas SFB Initial (Geojit)beza manojNo ratings yet

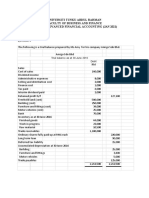

- Universiti Tunku Abdul Rahman Faculty of Business and Finance Ubaf 2113 Advanced Financial Accounting (Jan 2021) Tutorial 1Document5 pagesUniversiti Tunku Abdul Rahman Faculty of Business and Finance Ubaf 2113 Advanced Financial Accounting (Jan 2021) Tutorial 1KAY PHINE NGNo ratings yet