Section A Multiple Choice Questions 25 Marks (Answer in Multiple Choice Answer Sheet Provided) (Suggested Time: 36 Minutes)

Section A Multiple Choice Questions 25 Marks (Answer in Multiple Choice Answer Sheet Provided) (Suggested Time: 36 Minutes)

You might also like

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)No ratings yet

- Pilot TestDocument4 pagesPilot TestTrang Nguyễn QuỳnhNo ratings yet

- Exercise 1-1 To 1-5Document5 pagesExercise 1-1 To 1-5Jennette ToNo ratings yet

- Quiz - Chapter 1 - The Accounting ProcessDocument4 pagesQuiz - Chapter 1 - The Accounting ProcessJoseph Docto100% (2)

- CFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)From EverandCFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- ACC 3rd QuizDocument12 pagesACC 3rd QuizJazzy Mercado55% (11)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Agreement To Terminate LeaseDocument54 pagesAgreement To Terminate LeaseFerdinand Villanueva100% (1)

- Loans and Receivables - PresentationDocument71 pagesLoans and Receivables - PresentationIvy RosalesNo ratings yet

- Notes PayableDocument8 pagesNotes Payablechamie143No ratings yet

- Philippine Oblicon Articles 1231-1260Document22 pagesPhilippine Oblicon Articles 1231-1260Danielle Alessandra T. Calpo100% (1)

- Af101 MST S1 2019Document12 pagesAf101 MST S1 2019Malia i Lutu Leonia Kueva Losalu100% (2)

- Midterm 2022 - v2Document6 pagesMidterm 2022 - v2JF FNo ratings yet

- Pilot Test 2023Document6 pagesPilot Test 2023bapeboiz1510No ratings yet

- Quiz Chapter 4 - Chapter 8Document11 pagesQuiz Chapter 4 - Chapter 8Fäb RiceNo ratings yet

- Pilot TestDocument5 pagesPilot Testkhanhhung1112004No ratings yet

- Pilot Test 2023Document7 pagesPilot Test 2023trthuytrang004No ratings yet

- Chapter 4: Adjusting The Accounts and Preparing Financial StatementsDocument8 pagesChapter 4: Adjusting The Accounts and Preparing Financial StatementsDanh PhanNo ratings yet

- Midterm 2022 - v1Document6 pagesMidterm 2022 - v1JF FNo ratings yet

- F 2019092615474369290942Document12 pagesF 2019092615474369290942Deta BenedictaNo ratings yet

- PACE Sample ExamDocument13 pagesPACE Sample ExamjhouvanNo ratings yet

- Compre 2 - Far1Document5 pagesCompre 2 - Far1Mary Alyssa Claire Capate IINo ratings yet

- C. Identification, Recording, Communication.: ExceptDocument9 pagesC. Identification, Recording, Communication.: ExceptSylvia Al-a'maNo ratings yet

- Af101 MST - 2017 - F2FDocument10 pagesAf101 MST - 2017 - F2FŁøuiša Ņøinñøi100% (1)

- BSMM 8110 First Quiz Winter 2020 SolutionsDocument4 pagesBSMM 8110 First Quiz Winter 2020 SolutionsHibibiNo ratings yet

- Quiz Financial Accounting NTTDocument34 pagesQuiz Financial Accounting NTTdatdo1105No ratings yet

- Revision QnsDocument9 pagesRevision Qnspratibha jaggan martinNo ratings yet

- Fsa Questions FBNDocument34 pagesFsa Questions FBNsprykizyNo ratings yet

- Review Questions Financial Accounting 1 StudentsDocument5 pagesReview Questions Financial Accounting 1 StudentsNancy VõNo ratings yet

- Acc. P 2 2021 RevisionDocument8 pagesAcc. P 2 2021 RevisionSowda AhmedNo ratings yet

- Accounting Hawk - FAR - Incoming 3rd and 4th YearDocument27 pagesAccounting Hawk - FAR - Incoming 3rd and 4th YearClaire BarbaNo ratings yet

- Chapt 1,2,3,5,6 MCQDocument24 pagesChapt 1,2,3,5,6 MCQbritzNo ratings yet

- Soal UTS SMT 1 AkP (12-10-21)Document22 pagesSoal UTS SMT 1 AkP (12-10-21)Bayu PrasetyoNo ratings yet

- Abm 2 Summative TestDocument1 pageAbm 2 Summative TestSarah Mae Aventurado100% (1)

- FAR First Grading ExaminationDocument9 pagesFAR First Grading ExaminationRoldan ManganipNo ratings yet

- Acctg1 MidtermDocument6 pagesAcctg1 MidtermKevin Elrey Arce50% (4)

- AC 1 2 Final Exam 1Document7 pagesAC 1 2 Final Exam 1christine anglaNo ratings yet

- Final Exam AC 1 2 Answer KeyDocument7 pagesFinal Exam AC 1 2 Answer KeyBill VilladolidNo ratings yet

- Chapter 4 Question ReviewDocument11 pagesChapter 4 Question ReviewNayan SahaNo ratings yet

- Mid Term POA - Test 01Document8 pagesMid Term POA - Test 01Trang Ca CaNo ratings yet

- PA Sample MCQs 2Document15 pagesPA Sample MCQs 2ANH PHẠM QUỲNHNo ratings yet

- Basic Accounting Crash CourseDocument5 pagesBasic Accounting Crash CourseJolo RomanNo ratings yet

- Midterm Examination Suggested AnswersDocument9 pagesMidterm Examination Suggested AnswersJoshua CaraldeNo ratings yet

- WORKSHOP 2 Prior To Workshop AssignmentDocument5 pagesWORKSHOP 2 Prior To Workshop AssignmentMagnus Blicker LarsenNo ratings yet

- D PDF Sample Exam 2Document29 pagesD PDF Sample Exam 2seatow6No ratings yet

- Soal Cash ArDocument10 pagesSoal Cash ArmfreakthingNo ratings yet

- Acc SampleexamDocument12 pagesAcc SampleexamAmber AJNo ratings yet

- HT Cau Hoi on Tap KTQTE K19 Ko Bản DịchDocument10 pagesHT Cau Hoi on Tap KTQTE K19 Ko Bản Dịchdthien1602No ratings yet

- Tong Hop Cau HoiDocument44 pagesTong Hop Cau HoiVu Truc Ngan (K17 HCM)No ratings yet

- Xy95lywmi - Midterm Exam FarDocument12 pagesXy95lywmi - Midterm Exam FarLyra Mae De BotonNo ratings yet

- 1Document21 pages1DrGeorge Saad AbdallaNo ratings yet

- Level 4 ThoeryDocument25 pagesLevel 4 ThoeryEdomNo ratings yet

- NAU Accounting Skills Assessment Practice Exam Revised 0416Document11 pagesNAU Accounting Skills Assessment Practice Exam Revised 0416Danica VetuzNo ratings yet

- ACC 122 General Review - AKDocument11 pagesACC 122 General Review - AKJaselle SanchezNo ratings yet

- Final Exam - TemplateDocument7 pagesFinal Exam - TemplateKristine Esplana ToraldeNo ratings yet

- Abs3 TheoryDocument31 pagesAbs3 TheoryHassenNo ratings yet

- Tai Lieu Ke Toan - Docx Khanh.Document20 pagesTai Lieu Ke Toan - Docx Khanh.copmuopNo ratings yet

- Quiz On RizalDocument14 pagesQuiz On RizalYorinNo ratings yet

- Theory (1) 1Document18 pagesTheory (1) 1Debela RegasaNo ratings yet

- Acchievement Test Fabm2Document5 pagesAcchievement Test Fabm2Carmelo John Delacruz100% (1)

- Business Finance ExamDocument3 pagesBusiness Finance ExamChristian Joy ReyesNo ratings yet

- PA - T NG H P TestbankDocument86 pagesPA - T NG H P TestbankBích Phan Ngô NgọcNo ratings yet

- November 2019Document4 pagesNovember 2019Astrid MeloNo ratings yet

- SPS REYES v. BPI FAMILY SAVINGS BANKDocument2 pagesSPS REYES v. BPI FAMILY SAVINGS BANKAngelNo ratings yet

- 13-G.R. No. 160466 - Spouses Ong v. Philippine Commercial InternationalDocument4 pages13-G.R. No. 160466 - Spouses Ong v. Philippine Commercial InternationalPat EspinozaNo ratings yet

- Basic Accounting Principles and ProcessDocument14 pagesBasic Accounting Principles and ProcessAlex VillarosaNo ratings yet

- Credit Appraisal and Project Finance: Module No 4 & 5 by Mr. Navneet SaxenaDocument217 pagesCredit Appraisal and Project Finance: Module No 4 & 5 by Mr. Navneet SaxenaWedi TassewNo ratings yet

- Opr 0004 YDocument1 pageOpr 0004 YsrgaurNo ratings yet

- Hoover vs. FDR: Reactions To The Great DepressionDocument3 pagesHoover vs. FDR: Reactions To The Great Depressionirregularflowers100% (1)

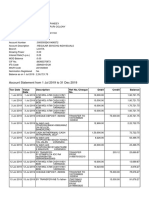

- Account Statement From 1 Jul 2019 To 31 Dec 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Jul 2019 To 31 Dec 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancepratibha guptaNo ratings yet

- Far 05 - Prelim ExamsDocument5 pagesFar 05 - Prelim ExamsMark Domingo MendozaNo ratings yet

- CPNREIT - Report (Official)Document21 pagesCPNREIT - Report (Official)Arty MagartyNo ratings yet

- Credit FunctionDocument19 pagesCredit FunctionPrincess Di BaykingNo ratings yet

- Credit ManualDocument106 pagesCredit ManualTony Green100% (2)

- CSC Saln Base FormDocument3 pagesCSC Saln Base Formjocansino4496No ratings yet

- Chapter06 ProblemsDocument2 pagesChapter06 ProblemsJesús Saracho Aguirre0% (1)

- Reaction Paper On GRP 12Document2 pagesReaction Paper On GRP 12Ayen YambaoNo ratings yet

- Lee v. CADocument2 pagesLee v. CAReymart-Vin Maguliano100% (1)

- 101 - Lizarraga Hermanos V Abada - LASDocument3 pages101 - Lizarraga Hermanos V Abada - LASLoren SeñeresNo ratings yet

- Minnesota Rental Application FormDocument2 pagesMinnesota Rental Application FormJonathan McNallyNo ratings yet

- Axis Bank - Initiating Coverage (Keynote Capitals)Document22 pagesAxis Bank - Initiating Coverage (Keynote Capitals)DenilNo ratings yet

- Bar Lecture in Banking, SPCL & FRIADocument93 pagesBar Lecture in Banking, SPCL & FRIAEstrell VanguardiaNo ratings yet

- Collecting BankerDocument15 pagesCollecting Bankeranusaya1988100% (2)

- Budget - Reply Final PDFDocument28 pagesBudget - Reply Final PDFBernewsAdmin100% (1)

- MCQ On Passive TaxesDocument7 pagesMCQ On Passive TaxesRandy ManzanoNo ratings yet

- Presentation 5 - Credit Risk ManagementDocument6 pagesPresentation 5 - Credit Risk ManagementMai ChiNo ratings yet

- Documents During Property SaleDocument12 pagesDocuments During Property SaleParas ShardaNo ratings yet

Download as pdf or txt

You might also like

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)No ratings yet

- Pilot TestDocument4 pagesPilot TestTrang Nguyễn QuỳnhNo ratings yet

- Exercise 1-1 To 1-5Document5 pagesExercise 1-1 To 1-5Jennette ToNo ratings yet

- Quiz - Chapter 1 - The Accounting ProcessDocument4 pagesQuiz - Chapter 1 - The Accounting ProcessJoseph Docto100% (2)

- CFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)From EverandCFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- ACC 3rd QuizDocument12 pagesACC 3rd QuizJazzy Mercado55% (11)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Agreement To Terminate LeaseDocument54 pagesAgreement To Terminate LeaseFerdinand Villanueva100% (1)

- Loans and Receivables - PresentationDocument71 pagesLoans and Receivables - PresentationIvy RosalesNo ratings yet

- Notes PayableDocument8 pagesNotes Payablechamie143No ratings yet

- Philippine Oblicon Articles 1231-1260Document22 pagesPhilippine Oblicon Articles 1231-1260Danielle Alessandra T. Calpo100% (1)

- Af101 MST S1 2019Document12 pagesAf101 MST S1 2019Malia i Lutu Leonia Kueva Losalu100% (2)

- Midterm 2022 - v2Document6 pagesMidterm 2022 - v2JF FNo ratings yet

- Pilot Test 2023Document6 pagesPilot Test 2023bapeboiz1510No ratings yet

- Quiz Chapter 4 - Chapter 8Document11 pagesQuiz Chapter 4 - Chapter 8Fäb RiceNo ratings yet

- Pilot TestDocument5 pagesPilot Testkhanhhung1112004No ratings yet

- Pilot Test 2023Document7 pagesPilot Test 2023trthuytrang004No ratings yet

- Chapter 4: Adjusting The Accounts and Preparing Financial StatementsDocument8 pagesChapter 4: Adjusting The Accounts and Preparing Financial StatementsDanh PhanNo ratings yet

- Midterm 2022 - v1Document6 pagesMidterm 2022 - v1JF FNo ratings yet

- F 2019092615474369290942Document12 pagesF 2019092615474369290942Deta BenedictaNo ratings yet

- PACE Sample ExamDocument13 pagesPACE Sample ExamjhouvanNo ratings yet

- Compre 2 - Far1Document5 pagesCompre 2 - Far1Mary Alyssa Claire Capate IINo ratings yet

- C. Identification, Recording, Communication.: ExceptDocument9 pagesC. Identification, Recording, Communication.: ExceptSylvia Al-a'maNo ratings yet

- Af101 MST - 2017 - F2FDocument10 pagesAf101 MST - 2017 - F2FŁøuiša Ņøinñøi100% (1)

- BSMM 8110 First Quiz Winter 2020 SolutionsDocument4 pagesBSMM 8110 First Quiz Winter 2020 SolutionsHibibiNo ratings yet

- Quiz Financial Accounting NTTDocument34 pagesQuiz Financial Accounting NTTdatdo1105No ratings yet

- Revision QnsDocument9 pagesRevision Qnspratibha jaggan martinNo ratings yet

- Fsa Questions FBNDocument34 pagesFsa Questions FBNsprykizyNo ratings yet

- Review Questions Financial Accounting 1 StudentsDocument5 pagesReview Questions Financial Accounting 1 StudentsNancy VõNo ratings yet

- Acc. P 2 2021 RevisionDocument8 pagesAcc. P 2 2021 RevisionSowda AhmedNo ratings yet

- Accounting Hawk - FAR - Incoming 3rd and 4th YearDocument27 pagesAccounting Hawk - FAR - Incoming 3rd and 4th YearClaire BarbaNo ratings yet

- Chapt 1,2,3,5,6 MCQDocument24 pagesChapt 1,2,3,5,6 MCQbritzNo ratings yet

- Soal UTS SMT 1 AkP (12-10-21)Document22 pagesSoal UTS SMT 1 AkP (12-10-21)Bayu PrasetyoNo ratings yet

- Abm 2 Summative TestDocument1 pageAbm 2 Summative TestSarah Mae Aventurado100% (1)

- FAR First Grading ExaminationDocument9 pagesFAR First Grading ExaminationRoldan ManganipNo ratings yet

- Acctg1 MidtermDocument6 pagesAcctg1 MidtermKevin Elrey Arce50% (4)

- AC 1 2 Final Exam 1Document7 pagesAC 1 2 Final Exam 1christine anglaNo ratings yet

- Final Exam AC 1 2 Answer KeyDocument7 pagesFinal Exam AC 1 2 Answer KeyBill VilladolidNo ratings yet

- Chapter 4 Question ReviewDocument11 pagesChapter 4 Question ReviewNayan SahaNo ratings yet

- Mid Term POA - Test 01Document8 pagesMid Term POA - Test 01Trang Ca CaNo ratings yet

- PA Sample MCQs 2Document15 pagesPA Sample MCQs 2ANH PHẠM QUỲNHNo ratings yet

- Basic Accounting Crash CourseDocument5 pagesBasic Accounting Crash CourseJolo RomanNo ratings yet

- Midterm Examination Suggested AnswersDocument9 pagesMidterm Examination Suggested AnswersJoshua CaraldeNo ratings yet

- WORKSHOP 2 Prior To Workshop AssignmentDocument5 pagesWORKSHOP 2 Prior To Workshop AssignmentMagnus Blicker LarsenNo ratings yet

- D PDF Sample Exam 2Document29 pagesD PDF Sample Exam 2seatow6No ratings yet

- Soal Cash ArDocument10 pagesSoal Cash ArmfreakthingNo ratings yet

- Acc SampleexamDocument12 pagesAcc SampleexamAmber AJNo ratings yet

- HT Cau Hoi on Tap KTQTE K19 Ko Bản DịchDocument10 pagesHT Cau Hoi on Tap KTQTE K19 Ko Bản Dịchdthien1602No ratings yet

- Tong Hop Cau HoiDocument44 pagesTong Hop Cau HoiVu Truc Ngan (K17 HCM)No ratings yet

- Xy95lywmi - Midterm Exam FarDocument12 pagesXy95lywmi - Midterm Exam FarLyra Mae De BotonNo ratings yet

- 1Document21 pages1DrGeorge Saad AbdallaNo ratings yet

- Level 4 ThoeryDocument25 pagesLevel 4 ThoeryEdomNo ratings yet

- NAU Accounting Skills Assessment Practice Exam Revised 0416Document11 pagesNAU Accounting Skills Assessment Practice Exam Revised 0416Danica VetuzNo ratings yet

- ACC 122 General Review - AKDocument11 pagesACC 122 General Review - AKJaselle SanchezNo ratings yet

- Final Exam - TemplateDocument7 pagesFinal Exam - TemplateKristine Esplana ToraldeNo ratings yet

- Abs3 TheoryDocument31 pagesAbs3 TheoryHassenNo ratings yet

- Tai Lieu Ke Toan - Docx Khanh.Document20 pagesTai Lieu Ke Toan - Docx Khanh.copmuopNo ratings yet

- Quiz On RizalDocument14 pagesQuiz On RizalYorinNo ratings yet

- Theory (1) 1Document18 pagesTheory (1) 1Debela RegasaNo ratings yet

- Acchievement Test Fabm2Document5 pagesAcchievement Test Fabm2Carmelo John Delacruz100% (1)

- Business Finance ExamDocument3 pagesBusiness Finance ExamChristian Joy ReyesNo ratings yet

- PA - T NG H P TestbankDocument86 pagesPA - T NG H P TestbankBích Phan Ngô NgọcNo ratings yet

- November 2019Document4 pagesNovember 2019Astrid MeloNo ratings yet

- SPS REYES v. BPI FAMILY SAVINGS BANKDocument2 pagesSPS REYES v. BPI FAMILY SAVINGS BANKAngelNo ratings yet

- 13-G.R. No. 160466 - Spouses Ong v. Philippine Commercial InternationalDocument4 pages13-G.R. No. 160466 - Spouses Ong v. Philippine Commercial InternationalPat EspinozaNo ratings yet

- Basic Accounting Principles and ProcessDocument14 pagesBasic Accounting Principles and ProcessAlex VillarosaNo ratings yet

- Credit Appraisal and Project Finance: Module No 4 & 5 by Mr. Navneet SaxenaDocument217 pagesCredit Appraisal and Project Finance: Module No 4 & 5 by Mr. Navneet SaxenaWedi TassewNo ratings yet

- Opr 0004 YDocument1 pageOpr 0004 YsrgaurNo ratings yet

- Hoover vs. FDR: Reactions To The Great DepressionDocument3 pagesHoover vs. FDR: Reactions To The Great Depressionirregularflowers100% (1)

- Account Statement From 1 Jul 2019 To 31 Dec 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Jul 2019 To 31 Dec 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancepratibha guptaNo ratings yet

- Far 05 - Prelim ExamsDocument5 pagesFar 05 - Prelim ExamsMark Domingo MendozaNo ratings yet

- CPNREIT - Report (Official)Document21 pagesCPNREIT - Report (Official)Arty MagartyNo ratings yet

- Credit FunctionDocument19 pagesCredit FunctionPrincess Di BaykingNo ratings yet

- Credit ManualDocument106 pagesCredit ManualTony Green100% (2)

- CSC Saln Base FormDocument3 pagesCSC Saln Base Formjocansino4496No ratings yet

- Chapter06 ProblemsDocument2 pagesChapter06 ProblemsJesús Saracho Aguirre0% (1)

- Reaction Paper On GRP 12Document2 pagesReaction Paper On GRP 12Ayen YambaoNo ratings yet

- Lee v. CADocument2 pagesLee v. CAReymart-Vin Maguliano100% (1)

- 101 - Lizarraga Hermanos V Abada - LASDocument3 pages101 - Lizarraga Hermanos V Abada - LASLoren SeñeresNo ratings yet

- Minnesota Rental Application FormDocument2 pagesMinnesota Rental Application FormJonathan McNallyNo ratings yet

- Axis Bank - Initiating Coverage (Keynote Capitals)Document22 pagesAxis Bank - Initiating Coverage (Keynote Capitals)DenilNo ratings yet

- Bar Lecture in Banking, SPCL & FRIADocument93 pagesBar Lecture in Banking, SPCL & FRIAEstrell VanguardiaNo ratings yet

- Collecting BankerDocument15 pagesCollecting Bankeranusaya1988100% (2)

- Budget - Reply Final PDFDocument28 pagesBudget - Reply Final PDFBernewsAdmin100% (1)

- MCQ On Passive TaxesDocument7 pagesMCQ On Passive TaxesRandy ManzanoNo ratings yet

- Presentation 5 - Credit Risk ManagementDocument6 pagesPresentation 5 - Credit Risk ManagementMai ChiNo ratings yet

- Documents During Property SaleDocument12 pagesDocuments During Property SaleParas ShardaNo ratings yet