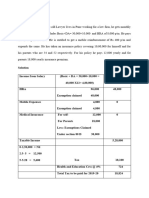

Tax Imposed To Corporation

Tax Imposed To Corporation

You might also like

- Condominium ConceptsDocument7 pagesCondominium ConceptsMarisseAnne Coquilla100% (2)

- Income Tax Banggawan Chapter 10Document18 pagesIncome Tax Banggawan Chapter 10Earth Pirapat100% (5)

- Business Math Lesson1 Week 4Document6 pagesBusiness Math Lesson1 Week 4REBECCA BRIONESNo ratings yet

- Compensation Income Part 1Document7 pagesCompensation Income Part 1Jean Diane JoveloNo ratings yet

- Servsafe CertificationDocument1 pageServsafe Certificationapi-436577767No ratings yet

- MODULE 8.1 - Legal Office ProcedureDocument9 pagesMODULE 8.1 - Legal Office ProcedureIrene Leah C. Romero100% (2)

- Fringe Benefits and Withholding TaxDocument7 pagesFringe Benefits and Withholding TaxXiaoyu KensameNo ratings yet

- Fringe Benefits: Classifications: Employees and Managerial or Supervisory PositionsDocument64 pagesFringe Benefits: Classifications: Employees and Managerial or Supervisory PositionsDempseyNo ratings yet

- Cprefinal - Fringe BenefitsDocument35 pagesCprefinal - Fringe BenefitsRexell DepalacNo ratings yet

- Week 3 Fringe Benefits Part 2 2023Document30 pagesWeek 3 Fringe Benefits Part 2 2023Arellano Rhovic R.No ratings yet

- Tax Planning and Employee RemunerationDocument10 pagesTax Planning and Employee Remunerationabdulraqeeb alareqiNo ratings yet

- Fringe Benefit Tax - Nov 06Document27 pagesFringe Benefit Tax - Nov 06Renievave TorculasNo ratings yet

- Module 11 - Fringe Benefit TaxDocument18 pagesModule 11 - Fringe Benefit TaxJANELLE NUEZNo ratings yet

- ReviewerDocument3 pagesReviewerangel ciiiNo ratings yet

- Theory Questions: Errorless Taxation by Ca Pranav Chandak at Pranav Chandak Academy, PuneDocument10 pagesTheory Questions: Errorless Taxation by Ca Pranav Chandak at Pranav Chandak Academy, PuneSimran MeherNo ratings yet

- IT Part 2Document95 pagesIT Part 2Virgilio E Aranas JrNo ratings yet

- Hussainkhawaja 1177 3641 2 LECTURE-10Document51 pagesHussainkhawaja 1177 3641 2 LECTURE-10Hasnain BhuttoNo ratings yet

- Fringe Benefit TAX: Mr. Mario M. Castro, Cpa, Mba Tax ConsultantDocument19 pagesFringe Benefit TAX: Mr. Mario M. Castro, Cpa, Mba Tax ConsultantKristine Aubrey AlvarezNo ratings yet

- Compensation IncomeDocument8 pagesCompensation IncomeStanley Renz Obaña Dela CruzNo ratings yet

- Chap 10-14: Compensation IncomeDocument44 pagesChap 10-14: Compensation IncomeArna Kaira Kjell DiestraNo ratings yet

- IncomeTax Banggawan2019 Ch10Document10 pagesIncomeTax Banggawan2019 Ch10Noreen Ledda100% (1)

- Module 3.1 Fringe Benefits and de Minimis BenefitsDocument4 pagesModule 3.1 Fringe Benefits and de Minimis BenefitsGabs SolivenNo ratings yet

- Chapter 8 Fringe Benefits 220816140606 B881b1ceDocument37 pagesChapter 8 Fringe Benefits 220816140606 B881b1ceCPAREVIEWNo ratings yet

- Chapter 3 Taxation Part 1Document28 pagesChapter 3 Taxation Part 1Alhysa Rosales CatapangNo ratings yet

- FBT FinalDocument28 pagesFBT Finalmendonesmariza2No ratings yet

- Drill 2 (Employee Benefits) Instruction: Solve and Answer The Following Questions. Please Make A Summary of Your FinalDocument2 pagesDrill 2 (Employee Benefits) Instruction: Solve and Answer The Following Questions. Please Make A Summary of Your FinalYANIII12345No ratings yet

- De Minimis Benefits: Taxability: Excluded From Gross Income Up To The Extent of 90,000 PesosDocument3 pagesDe Minimis Benefits: Taxability: Excluded From Gross Income Up To The Extent of 90,000 PesosKathNo ratings yet

- Fringe Benefits TaxDocument11 pagesFringe Benefits Taxkenshin sclanimirNo ratings yet

- De Minimis and Fringe BenefitsDocument14 pagesDe Minimis and Fringe BenefitsCza PeñaNo ratings yet

- Tax43-013-Compensation IncomeDocument22 pagesTax43-013-Compensation Incomelowi shooNo ratings yet

- 2nd Semester Income Taxation Module 9 Exercises On Fringe Benefits TaxDocument9 pages2nd Semester Income Taxation Module 9 Exercises On Fringe Benefits Taxnicole tolaybaNo ratings yet

- Fringe Benefit ExercisesDocument6 pagesFringe Benefit ExercisesGet BurnNo ratings yet

- Problem 1 Write The Letter As Well As The Entire AnswerDocument2 pagesProblem 1 Write The Letter As Well As The Entire AnswerStephanie DesembranaNo ratings yet

- 05M Fringe BenefitDocument4 pages05M Fringe BenefitMarko IllustrisimoNo ratings yet

- Taxation - Direct & Indirect JUNE 2022Document10 pagesTaxation - Direct & Indirect JUNE 2022Rajni KumariNo ratings yet

- Acctax1 - Chapter 6 ReviewerDocument4 pagesAcctax1 - Chapter 6 ReviewerEirene Joy VillanuevaNo ratings yet

- Fringe BenefitsDocument22 pagesFringe BenefitsMariel BerdigayNo ratings yet

- Compensation IncomeDocument34 pagesCompensation IncomeAdelade MaryosaNo ratings yet

- Module+7+ +Fringe+Benefits+and+de+Minimis+BenefitsDocument5 pagesModule+7+ +Fringe+Benefits+and+de+Minimis+Benefitskrisha milloNo ratings yet

- Taxation - Direct and Indirect 2022Document10 pagesTaxation - Direct and Indirect 2022Sagar JindalNo ratings yet

- Assignment No. 4Document3 pagesAssignment No. 4Paula VillarubiaNo ratings yet

- Notes On SalariesDocument18 pagesNotes On SalariesParul KansariaNo ratings yet

- Work Book of Corporate Financial Accounting 23-04-2022Document33 pagesWork Book of Corporate Financial Accounting 23-04-2022SWAPNIL JADHAVNo ratings yet

- Employee Benefits: Cruz, Jerica May A. CBET-01-501EDocument21 pagesEmployee Benefits: Cruz, Jerica May A. CBET-01-501Eclara san miguelNo ratings yet

- 6 Employment Income Taxation 2021Document91 pages6 Employment Income Taxation 2021siyad ahmedNo ratings yet

- Specified Sources of IncomeDocument15 pagesSpecified Sources of Incomebrian karuNo ratings yet

- TAXATION - Direct & IndirectDocument7 pagesTAXATION - Direct & IndirectSubhana NasimNo ratings yet

- Excel Professional Services, Inc.: Cpa ReviewDocument11 pagesExcel Professional Services, Inc.: Cpa ReviewKuro HanabusaNo ratings yet

- Excel Professional Services, Inc.: Classification of EmployeesDocument12 pagesExcel Professional Services, Inc.: Classification of Employeesvane rondinaNo ratings yet

- Chapter 3 Part 2Document22 pagesChapter 3 Part 2ISLAM KHALED ZSCNo ratings yet

- PDF Document E64dfec87bb0 1Document75 pagesPDF Document E64dfec87bb0 120BRM051 Sukant SNo ratings yet

- BUS. MATH Q2 - Week4Document5 pagesBUS. MATH Q2 - Week4DARLENE MARTIN100% (1)

- Employment IncomeDocument12 pagesEmployment Incomemusobya godfreyNo ratings yet

- Illustration 1 and 2 Salary - 21-22 Nov 2023Document5 pagesIllustration 1 and 2 Salary - 21-22 Nov 2023Chinmay HarshNo ratings yet

- Deferred Income Tax and Employee BenefitsDocument35 pagesDeferred Income Tax and Employee BenefitsHello HiNo ratings yet

- Postemployment BenefitsDocument22 pagesPostemployment BenefitsChoco ButternutNo ratings yet

- Compensation Income and Fringe Benefit Tax. ReviewerDocument4 pagesCompensation Income and Fringe Benefit Tax. RevieweryzaNo ratings yet

- Income Tax Group AssignmentDocument8 pagesIncome Tax Group AssignmentFozle Rabby 182-11-5893No ratings yet

- Quiz 6 - Fringe BenefitsDocument7 pagesQuiz 6 - Fringe BenefitsCarlo manejaNo ratings yet

- Contributions TDocument6 pagesContributions TRena Jocelle NalzaroNo ratings yet

- 18 - IND AS 19 - Employee Benefit - Final (R)Document28 pages18 - IND AS 19 - Employee Benefit - Final (R)S Bharhath kumarNo ratings yet

- What Is A PerquisiteDocument8 pagesWhat Is A PerquisitesoujnyNo ratings yet

- Ramos-Randolph MM3 HRM Module-1Document7 pagesRamos-Randolph MM3 HRM Module-1Randz RamosNo ratings yet

- Chapter 13Document6 pagesChapter 13Randz RamosNo ratings yet

- AssignmentDocument6 pagesAssignmentRandz RamosNo ratings yet

- Korea The Criminal Code Does Not Criminalize Sodomy or Same Sex Sexual Conduct1Document9 pagesKorea The Criminal Code Does Not Criminalize Sodomy or Same Sex Sexual Conduct1Randz RamosNo ratings yet

- IS-700.A Instructor GuideDocument216 pagesIS-700.A Instructor GuideTherleDreganskyNo ratings yet

- Graduated Income Tax Rates Under Section 24 (A) (2) of The Tax Code of 1997, As Amended by RepublicDocument10 pagesGraduated Income Tax Rates Under Section 24 (A) (2) of The Tax Code of 1997, As Amended by RepublicMohammad Nowaiser MaruhomNo ratings yet

- Change of Land Use (Clu) Application and Scrutiny Form: DD MM Yyyy DD MM Yyyy ADocument4 pagesChange of Land Use (Clu) Application and Scrutiny Form: DD MM Yyyy DD MM Yyyy ATàmìļ Přïñčé0% (1)

- Our Global Neighborhood: A Summary Analysis by Henry LambDocument16 pagesOur Global Neighborhood: A Summary Analysis by Henry LambGreensparrow01No ratings yet

- GMAT RescheduleDocument3 pagesGMAT RescheduleMANOUJ GOELNo ratings yet

- APPENDIX2Document2 pagesAPPENDIX2Lavanya GoleNo ratings yet

- Petition For MilaDocument16 pagesPetition For MilacindyjdumasNo ratings yet

- A Petition For Divorce by Mutual Consent Us 13 (B) of The Hindu Marriage AcDocument2 pagesA Petition For Divorce by Mutual Consent Us 13 (B) of The Hindu Marriage AcDeepak100% (1)

- United States v. Sokolow, 490 U.S. 1 (1989)Document14 pagesUnited States v. Sokolow, 490 U.S. 1 (1989)Scribd Government DocsNo ratings yet

- Introduction To Comparative Politics 6th Edition Kesselman Test BankDocument12 pagesIntroduction To Comparative Politics 6th Edition Kesselman Test Bankmymaximiliandwo100% (22)

- Immaculata V Navarro, GR L-42230, November 26, 1986 (Per J. Paras, Second Division)Document2 pagesImmaculata V Navarro, GR L-42230, November 26, 1986 (Per J. Paras, Second Division)Steve UyNo ratings yet

- Edward Mandell HouseDocument8 pagesEdward Mandell HouseSLAVEFATHERNo ratings yet

- Peaceful Settlement of DisputesDocument51 pagesPeaceful Settlement of DisputesVivek MenonNo ratings yet

- Dole GuidelineDocument34 pagesDole GuidelineLovely GuevarraNo ratings yet

- Whether One Slap Would Consitute As A Ground For Divorce?Document4 pagesWhether One Slap Would Consitute As A Ground For Divorce?Rohan VijayNo ratings yet

- Rules For Member's MeetingDocument3 pagesRules For Member's MeetingMichele ColesNo ratings yet

- Respondent.: Soliman M. Santos, JR., Complainant, vs. Atty. Francisco R. LlamasDocument8 pagesRespondent.: Soliman M. Santos, JR., Complainant, vs. Atty. Francisco R. LlamasCaitlin KintanarNo ratings yet

- INZ 1199 - Partnership-Based Temporary Visa Guide (INZ 1199) - March 2015Document9 pagesINZ 1199 - Partnership-Based Temporary Visa Guide (INZ 1199) - March 2015Dragoslav DzolicNo ratings yet

- Biagtan v. Insular LifeDocument2 pagesBiagtan v. Insular LifeIldefonso Hernaez100% (2)

- COA Disallowance: Module VI. Disposal ManagementDocument34 pagesCOA Disallowance: Module VI. Disposal ManagementCirilo CabadaNo ratings yet

- Divorce Petition Assignment No. 7Document4 pagesDivorce Petition Assignment No. 7sanjana sethNo ratings yet

- Tax Appeal E026 of 2020Document8 pagesTax Appeal E026 of 2020Meru CityNo ratings yet

- Odchigue-Bondoc vs. TanDocument1 pageOdchigue-Bondoc vs. TanCarlota Nicolas VillaromanNo ratings yet

- Duecker's Testimony For Kathleen Kane HearingDocument11 pagesDuecker's Testimony For Kathleen Kane HearingPennLiveNo ratings yet

- TCS & TPSDocument3 pagesTCS & TPSGeorge Khris DebbarmaNo ratings yet

- II.3.a.a Umaguing V de VeraDocument2 pagesII.3.a.a Umaguing V de Veraclarisse lyka hattonNo ratings yet

- 50 Beyond The States System ?: Hedley BullDocument4 pages50 Beyond The States System ?: Hedley BullmaLEna_88No ratings yet

Download as docx, pdf, or txt

You might also like

- Condominium ConceptsDocument7 pagesCondominium ConceptsMarisseAnne Coquilla100% (2)

- Income Tax Banggawan Chapter 10Document18 pagesIncome Tax Banggawan Chapter 10Earth Pirapat100% (5)

- Business Math Lesson1 Week 4Document6 pagesBusiness Math Lesson1 Week 4REBECCA BRIONESNo ratings yet

- Compensation Income Part 1Document7 pagesCompensation Income Part 1Jean Diane JoveloNo ratings yet

- Servsafe CertificationDocument1 pageServsafe Certificationapi-436577767No ratings yet

- MODULE 8.1 - Legal Office ProcedureDocument9 pagesMODULE 8.1 - Legal Office ProcedureIrene Leah C. Romero100% (2)

- Fringe Benefits and Withholding TaxDocument7 pagesFringe Benefits and Withholding TaxXiaoyu KensameNo ratings yet

- Fringe Benefits: Classifications: Employees and Managerial or Supervisory PositionsDocument64 pagesFringe Benefits: Classifications: Employees and Managerial or Supervisory PositionsDempseyNo ratings yet

- Cprefinal - Fringe BenefitsDocument35 pagesCprefinal - Fringe BenefitsRexell DepalacNo ratings yet

- Week 3 Fringe Benefits Part 2 2023Document30 pagesWeek 3 Fringe Benefits Part 2 2023Arellano Rhovic R.No ratings yet

- Tax Planning and Employee RemunerationDocument10 pagesTax Planning and Employee Remunerationabdulraqeeb alareqiNo ratings yet

- Fringe Benefit Tax - Nov 06Document27 pagesFringe Benefit Tax - Nov 06Renievave TorculasNo ratings yet

- Module 11 - Fringe Benefit TaxDocument18 pagesModule 11 - Fringe Benefit TaxJANELLE NUEZNo ratings yet

- ReviewerDocument3 pagesReviewerangel ciiiNo ratings yet

- Theory Questions: Errorless Taxation by Ca Pranav Chandak at Pranav Chandak Academy, PuneDocument10 pagesTheory Questions: Errorless Taxation by Ca Pranav Chandak at Pranav Chandak Academy, PuneSimran MeherNo ratings yet

- IT Part 2Document95 pagesIT Part 2Virgilio E Aranas JrNo ratings yet

- Hussainkhawaja 1177 3641 2 LECTURE-10Document51 pagesHussainkhawaja 1177 3641 2 LECTURE-10Hasnain BhuttoNo ratings yet

- Fringe Benefit TAX: Mr. Mario M. Castro, Cpa, Mba Tax ConsultantDocument19 pagesFringe Benefit TAX: Mr. Mario M. Castro, Cpa, Mba Tax ConsultantKristine Aubrey AlvarezNo ratings yet

- Compensation IncomeDocument8 pagesCompensation IncomeStanley Renz Obaña Dela CruzNo ratings yet

- Chap 10-14: Compensation IncomeDocument44 pagesChap 10-14: Compensation IncomeArna Kaira Kjell DiestraNo ratings yet

- IncomeTax Banggawan2019 Ch10Document10 pagesIncomeTax Banggawan2019 Ch10Noreen Ledda100% (1)

- Module 3.1 Fringe Benefits and de Minimis BenefitsDocument4 pagesModule 3.1 Fringe Benefits and de Minimis BenefitsGabs SolivenNo ratings yet

- Chapter 8 Fringe Benefits 220816140606 B881b1ceDocument37 pagesChapter 8 Fringe Benefits 220816140606 B881b1ceCPAREVIEWNo ratings yet

- Chapter 3 Taxation Part 1Document28 pagesChapter 3 Taxation Part 1Alhysa Rosales CatapangNo ratings yet

- FBT FinalDocument28 pagesFBT Finalmendonesmariza2No ratings yet

- Drill 2 (Employee Benefits) Instruction: Solve and Answer The Following Questions. Please Make A Summary of Your FinalDocument2 pagesDrill 2 (Employee Benefits) Instruction: Solve and Answer The Following Questions. Please Make A Summary of Your FinalYANIII12345No ratings yet

- De Minimis Benefits: Taxability: Excluded From Gross Income Up To The Extent of 90,000 PesosDocument3 pagesDe Minimis Benefits: Taxability: Excluded From Gross Income Up To The Extent of 90,000 PesosKathNo ratings yet

- Fringe Benefits TaxDocument11 pagesFringe Benefits Taxkenshin sclanimirNo ratings yet

- De Minimis and Fringe BenefitsDocument14 pagesDe Minimis and Fringe BenefitsCza PeñaNo ratings yet

- Tax43-013-Compensation IncomeDocument22 pagesTax43-013-Compensation Incomelowi shooNo ratings yet

- 2nd Semester Income Taxation Module 9 Exercises On Fringe Benefits TaxDocument9 pages2nd Semester Income Taxation Module 9 Exercises On Fringe Benefits Taxnicole tolaybaNo ratings yet

- Fringe Benefit ExercisesDocument6 pagesFringe Benefit ExercisesGet BurnNo ratings yet

- Problem 1 Write The Letter As Well As The Entire AnswerDocument2 pagesProblem 1 Write The Letter As Well As The Entire AnswerStephanie DesembranaNo ratings yet

- 05M Fringe BenefitDocument4 pages05M Fringe BenefitMarko IllustrisimoNo ratings yet

- Taxation - Direct & Indirect JUNE 2022Document10 pagesTaxation - Direct & Indirect JUNE 2022Rajni KumariNo ratings yet

- Acctax1 - Chapter 6 ReviewerDocument4 pagesAcctax1 - Chapter 6 ReviewerEirene Joy VillanuevaNo ratings yet

- Fringe BenefitsDocument22 pagesFringe BenefitsMariel BerdigayNo ratings yet

- Compensation IncomeDocument34 pagesCompensation IncomeAdelade MaryosaNo ratings yet

- Module+7+ +Fringe+Benefits+and+de+Minimis+BenefitsDocument5 pagesModule+7+ +Fringe+Benefits+and+de+Minimis+Benefitskrisha milloNo ratings yet

- Taxation - Direct and Indirect 2022Document10 pagesTaxation - Direct and Indirect 2022Sagar JindalNo ratings yet

- Assignment No. 4Document3 pagesAssignment No. 4Paula VillarubiaNo ratings yet

- Notes On SalariesDocument18 pagesNotes On SalariesParul KansariaNo ratings yet

- Work Book of Corporate Financial Accounting 23-04-2022Document33 pagesWork Book of Corporate Financial Accounting 23-04-2022SWAPNIL JADHAVNo ratings yet

- Employee Benefits: Cruz, Jerica May A. CBET-01-501EDocument21 pagesEmployee Benefits: Cruz, Jerica May A. CBET-01-501Eclara san miguelNo ratings yet

- 6 Employment Income Taxation 2021Document91 pages6 Employment Income Taxation 2021siyad ahmedNo ratings yet

- Specified Sources of IncomeDocument15 pagesSpecified Sources of Incomebrian karuNo ratings yet

- TAXATION - Direct & IndirectDocument7 pagesTAXATION - Direct & IndirectSubhana NasimNo ratings yet

- Excel Professional Services, Inc.: Cpa ReviewDocument11 pagesExcel Professional Services, Inc.: Cpa ReviewKuro HanabusaNo ratings yet

- Excel Professional Services, Inc.: Classification of EmployeesDocument12 pagesExcel Professional Services, Inc.: Classification of Employeesvane rondinaNo ratings yet

- Chapter 3 Part 2Document22 pagesChapter 3 Part 2ISLAM KHALED ZSCNo ratings yet

- PDF Document E64dfec87bb0 1Document75 pagesPDF Document E64dfec87bb0 120BRM051 Sukant SNo ratings yet

- BUS. MATH Q2 - Week4Document5 pagesBUS. MATH Q2 - Week4DARLENE MARTIN100% (1)

- Employment IncomeDocument12 pagesEmployment Incomemusobya godfreyNo ratings yet

- Illustration 1 and 2 Salary - 21-22 Nov 2023Document5 pagesIllustration 1 and 2 Salary - 21-22 Nov 2023Chinmay HarshNo ratings yet

- Deferred Income Tax and Employee BenefitsDocument35 pagesDeferred Income Tax and Employee BenefitsHello HiNo ratings yet

- Postemployment BenefitsDocument22 pagesPostemployment BenefitsChoco ButternutNo ratings yet

- Compensation Income and Fringe Benefit Tax. ReviewerDocument4 pagesCompensation Income and Fringe Benefit Tax. RevieweryzaNo ratings yet

- Income Tax Group AssignmentDocument8 pagesIncome Tax Group AssignmentFozle Rabby 182-11-5893No ratings yet

- Quiz 6 - Fringe BenefitsDocument7 pagesQuiz 6 - Fringe BenefitsCarlo manejaNo ratings yet

- Contributions TDocument6 pagesContributions TRena Jocelle NalzaroNo ratings yet

- 18 - IND AS 19 - Employee Benefit - Final (R)Document28 pages18 - IND AS 19 - Employee Benefit - Final (R)S Bharhath kumarNo ratings yet

- What Is A PerquisiteDocument8 pagesWhat Is A PerquisitesoujnyNo ratings yet

- Ramos-Randolph MM3 HRM Module-1Document7 pagesRamos-Randolph MM3 HRM Module-1Randz RamosNo ratings yet

- Chapter 13Document6 pagesChapter 13Randz RamosNo ratings yet

- AssignmentDocument6 pagesAssignmentRandz RamosNo ratings yet

- Korea The Criminal Code Does Not Criminalize Sodomy or Same Sex Sexual Conduct1Document9 pagesKorea The Criminal Code Does Not Criminalize Sodomy or Same Sex Sexual Conduct1Randz RamosNo ratings yet

- IS-700.A Instructor GuideDocument216 pagesIS-700.A Instructor GuideTherleDreganskyNo ratings yet

- Graduated Income Tax Rates Under Section 24 (A) (2) of The Tax Code of 1997, As Amended by RepublicDocument10 pagesGraduated Income Tax Rates Under Section 24 (A) (2) of The Tax Code of 1997, As Amended by RepublicMohammad Nowaiser MaruhomNo ratings yet

- Change of Land Use (Clu) Application and Scrutiny Form: DD MM Yyyy DD MM Yyyy ADocument4 pagesChange of Land Use (Clu) Application and Scrutiny Form: DD MM Yyyy DD MM Yyyy ATàmìļ Přïñčé0% (1)

- Our Global Neighborhood: A Summary Analysis by Henry LambDocument16 pagesOur Global Neighborhood: A Summary Analysis by Henry LambGreensparrow01No ratings yet

- GMAT RescheduleDocument3 pagesGMAT RescheduleMANOUJ GOELNo ratings yet

- APPENDIX2Document2 pagesAPPENDIX2Lavanya GoleNo ratings yet

- Petition For MilaDocument16 pagesPetition For MilacindyjdumasNo ratings yet

- A Petition For Divorce by Mutual Consent Us 13 (B) of The Hindu Marriage AcDocument2 pagesA Petition For Divorce by Mutual Consent Us 13 (B) of The Hindu Marriage AcDeepak100% (1)

- United States v. Sokolow, 490 U.S. 1 (1989)Document14 pagesUnited States v. Sokolow, 490 U.S. 1 (1989)Scribd Government DocsNo ratings yet

- Introduction To Comparative Politics 6th Edition Kesselman Test BankDocument12 pagesIntroduction To Comparative Politics 6th Edition Kesselman Test Bankmymaximiliandwo100% (22)

- Immaculata V Navarro, GR L-42230, November 26, 1986 (Per J. Paras, Second Division)Document2 pagesImmaculata V Navarro, GR L-42230, November 26, 1986 (Per J. Paras, Second Division)Steve UyNo ratings yet

- Edward Mandell HouseDocument8 pagesEdward Mandell HouseSLAVEFATHERNo ratings yet

- Peaceful Settlement of DisputesDocument51 pagesPeaceful Settlement of DisputesVivek MenonNo ratings yet

- Dole GuidelineDocument34 pagesDole GuidelineLovely GuevarraNo ratings yet

- Whether One Slap Would Consitute As A Ground For Divorce?Document4 pagesWhether One Slap Would Consitute As A Ground For Divorce?Rohan VijayNo ratings yet

- Rules For Member's MeetingDocument3 pagesRules For Member's MeetingMichele ColesNo ratings yet

- Respondent.: Soliman M. Santos, JR., Complainant, vs. Atty. Francisco R. LlamasDocument8 pagesRespondent.: Soliman M. Santos, JR., Complainant, vs. Atty. Francisco R. LlamasCaitlin KintanarNo ratings yet

- INZ 1199 - Partnership-Based Temporary Visa Guide (INZ 1199) - March 2015Document9 pagesINZ 1199 - Partnership-Based Temporary Visa Guide (INZ 1199) - March 2015Dragoslav DzolicNo ratings yet

- Biagtan v. Insular LifeDocument2 pagesBiagtan v. Insular LifeIldefonso Hernaez100% (2)

- COA Disallowance: Module VI. Disposal ManagementDocument34 pagesCOA Disallowance: Module VI. Disposal ManagementCirilo CabadaNo ratings yet

- Divorce Petition Assignment No. 7Document4 pagesDivorce Petition Assignment No. 7sanjana sethNo ratings yet

- Tax Appeal E026 of 2020Document8 pagesTax Appeal E026 of 2020Meru CityNo ratings yet

- Odchigue-Bondoc vs. TanDocument1 pageOdchigue-Bondoc vs. TanCarlota Nicolas VillaromanNo ratings yet

- Duecker's Testimony For Kathleen Kane HearingDocument11 pagesDuecker's Testimony For Kathleen Kane HearingPennLiveNo ratings yet

- TCS & TPSDocument3 pagesTCS & TPSGeorge Khris DebbarmaNo ratings yet

- II.3.a.a Umaguing V de VeraDocument2 pagesII.3.a.a Umaguing V de Veraclarisse lyka hattonNo ratings yet

- 50 Beyond The States System ?: Hedley BullDocument4 pages50 Beyond The States System ?: Hedley BullmaLEna_88No ratings yet