Download as pdf or txt

You might also like

- Chapter 01Document18 pagesChapter 01Ali Sami Ahmad Faqeeh 160021176No ratings yet

- BlackBook On Role of Banks in International TradeDocument60 pagesBlackBook On Role of Banks in International Tradelakshya katyal100% (3)

- PNB MetLife Guaranteed Income Plan-Brochure - tcm47-63397 PDFDocument6 pagesPNB MetLife Guaranteed Income Plan-Brochure - tcm47-63397 PDFMohit VermaNo ratings yet

- PNB MetLife Guaranteed Income Plan - Brochure - tcm47-63397Document6 pagesPNB MetLife Guaranteed Income Plan - Brochure - tcm47-63397Manisha KumariNo ratings yet

- MetLife Endowment Savings Plan PRINT Brochure - 2016 V2 - tcm47-27873Document4 pagesMetLife Endowment Savings Plan PRINT Brochure - 2016 V2 - tcm47-27873himanshu goyalNo ratings yet

- MetLife Bachat Yojana - Brochure - tcm47-27823Document5 pagesMetLife Bachat Yojana - Brochure - tcm47-27823sarthakNo ratings yet

- Vision Endowment Plus PlanDocument12 pagesVision Endowment Plus PlanRoshith Mele AreekkalNo ratings yet

- MGFP BrochureDocument26 pagesMGFP BrochureAbhinesh KumarNo ratings yet

- RLMMP - BrochureDocument7 pagesRLMMP - BrochureAnjesh KumarNo ratings yet

- MGFP BrochureDocument14 pagesMGFP Brochureankur06e016No ratings yet

- IndiaFirst Smart Save Plan BrochureDocument16 pagesIndiaFirst Smart Save Plan BrochureVishal SharmaNo ratings yet

- Save, Invest & Protect Your FutureDocument2 pagesSave, Invest & Protect Your Futureemaraty khNo ratings yet

- Mahalife Gold: Tata Aia Life InsuranceDocument5 pagesMahalife Gold: Tata Aia Life InsuranceFrancis ReddyNo ratings yet

- Jeevan Nivesh CanarahsbcDocument14 pagesJeevan Nivesh CanarahsbcVinesh ChandraNo ratings yet

- MGFP BrochureDocument23 pagesMGFP BrochureAshwani ChandailNo ratings yet

- Tata AIA Life Insurance MoneyBackPlus BrochureDocument6 pagesTata AIA Life Insurance MoneyBackPlus BrochureasfakpaliwalaNo ratings yet

- Customer's ExpectationsDocument12 pagesCustomer's ExpectationsShail EnternationlNo ratings yet

- One Pager Smart LifestyleDocument2 pagesOne Pager Smart LifestyleSam RamNo ratings yet

- Business Illustration80015109593Document11 pagesBusiness Illustration80015109593Umesh KanaujiyaNo ratings yet

- MGFP BrochureDocument14 pagesMGFP BrochuresarthakNo ratings yet

- ICICI Savings SurakshaDocument8 pagesICICI Savings SurakshaNipun JainNo ratings yet

- ICICI Pru Savings SurakshaDocument8 pagesICICI Pru Savings SurakshabindalmohitNo ratings yet

- Century Plan BrochureDocument28 pagesCentury Plan Brochuresandeepgiri71No ratings yet

- P Nbs JB BrochureDocument5 pagesP Nbs JB BrochureavkashNo ratings yet

- UA SmartLife Brochure-EnglishDocument10 pagesUA SmartLife Brochure-EnglishBuddhika KumarasingheNo ratings yet

- MoneyBackPlus BrochureDocument7 pagesMoneyBackPlus BrochuremanjugnpNo ratings yet

- ManuSecure Brochure - Full - 2023Document17 pagesManuSecure Brochure - Full - 2023L JayNo ratings yet

- IndiaFirst Maha Jeevan Plan - BrochureDocument11 pagesIndiaFirst Maha Jeevan Plan - BrochureBirddoxyNo ratings yet

- Rakshakaran: A Non Linked, Participating, Whole Life Individual Savings PlanDocument6 pagesRakshakaran: A Non Linked, Participating, Whole Life Individual Savings PlanHemant ShakyaNo ratings yet

- ICICI Pru Savings SurakshaDocument8 pagesICICI Pru Savings SurakshaRojan G JosephNo ratings yet

- Wealth Ultima - EnglishDocument2 pagesWealth Ultima - EnglishJagdeesh ShettyNo ratings yet

- Life Insurance BrouchureDocument2 pagesLife Insurance BrouchureGuru9756No ratings yet

- Fortune Maxima - V3 Brochure (Web)Document14 pagesFortune Maxima - V3 Brochure (Web)KarthikNo ratings yet

- Premier Endowment PlanDocument12 pagesPremier Endowment Planumar zaid khanNo ratings yet

- Future PerfectDocument11 pagesFuture PerfectAditi SinghNo ratings yet

- PP12201710731 HDFC Life ClassicAssure Plus Retail BrochureDocument6 pagesPP12201710731 HDFC Life ClassicAssure Plus Retail BrochureNatuskar pranitNo ratings yet

- Active Income Plan - English PDFDocument2 pagesActive Income Plan - English PDFJagdeesh ShettyNo ratings yet

- Shriram Life Super Income Plan Website VersionDocument24 pagesShriram Life Super Income Plan Website VersionPraveen BabuNo ratings yet

- PNB Metlife MMTPDocument20 pagesPNB Metlife MMTPKiran KumarNo ratings yet

- IDBI Federal Lifesurance Savings Insurance PlanDocument16 pagesIDBI Federal Lifesurance Savings Insurance PlanKumarniksNo ratings yet

- HDFC Life Click 2 InvestDocument7 pagesHDFC Life Click 2 InvestShaik BademiyaNo ratings yet

- HDFC Life Classic Assure Plus PlanDocument6 pagesHDFC Life Classic Assure Plus PlanPrashant ChaudharyNo ratings yet

- Cashflow Protection Plus - EnglishDocument2 pagesCashflow Protection Plus - EnglishJagdeesh ShettyNo ratings yet

- PNB MetLife Aajeevan Suraksha - Brochure - tcm47-69312Document11 pagesPNB MetLife Aajeevan Suraksha - Brochure - tcm47-69312Ashwani ChandailNo ratings yet

- Wealth Gain Insurance Plan Brochure V03Document30 pagesWealth Gain Insurance Plan Brochure V03rajlal88No ratings yet

- A One of Its Kind Plan: For Internal Circulation OnlyDocument18 pagesA One of Its Kind Plan: For Internal Circulation OnlyKunal ShahNo ratings yet

- Iraksha Trop: Protection SolutionsDocument5 pagesIraksha Trop: Protection SolutionsPradeep ShastryNo ratings yet

- Aditya Birla Sun Life Insurance SecurePlus Plan LeafletDocument5 pagesAditya Birla Sun Life Insurance SecurePlus Plan LeafletMohanraj GNo ratings yet

- Future Wealth GainDocument25 pagesFuture Wealth Gainharshad malusareNo ratings yet

- Money Back Advantage Plan Product Brochure NewDocument9 pagesMoney Back Advantage Plan Product Brochure NewSantosh KumarNo ratings yet

- Endowment PolicyDocument25 pagesEndowment PolicyPrateek BindalNo ratings yet

- MMTP Plus BrochureDocument20 pagesMMTP Plus Brochureritesh142No ratings yet

- ICICI Future Perfect - BrochureDocument11 pagesICICI Future Perfect - BrochureChandan Kumar SatyanarayanaNo ratings yet

- Aditya Birla Sun Life Insurance Secureplus Plan: Dear MR Kunjal Uin - 109N102V02Document7 pagesAditya Birla Sun Life Insurance Secureplus Plan: Dear MR Kunjal Uin - 109N102V02kunjal mistryNo ratings yet

- Tata AIA Life Insurance Wealth Maxima: Unit Linked Whole Life Individual Savings PlanDocument14 pagesTata AIA Life Insurance Wealth Maxima: Unit Linked Whole Life Individual Savings PlanShaheryar KhanNo ratings yet

- Fortune Maxima V4 BrochureDocument16 pagesFortune Maxima V4 BrochureSubhadip GhoshNo ratings yet

- Jeevan SafarDocument7 pagesJeevan SafarNishant SinhaNo ratings yet

- Fortune-Maxima-cg RetirementDocument23 pagesFortune-Maxima-cg RetirementSubhadip GhoshNo ratings yet

- Achcha Lagta Hai Na Jab Kuch Jaldi Milta Hai: Tax Benefits Also AvailableDocument10 pagesAchcha Lagta Hai Na Jab Kuch Jaldi Milta Hai: Tax Benefits Also Availabledummy245No ratings yet

- Safe Money First: Your Guidebook to Annuities and Safe Retirement Financial Planning StrategiesFrom EverandSafe Money First: Your Guidebook to Annuities and Safe Retirement Financial Planning StrategiesNo ratings yet

- The Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1From EverandThe Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1No ratings yet

- Sumangal Ghosh 0122200100002473Document7 pagesSumangal Ghosh 0122200100002473Sumangal GhoshNo ratings yet

- Quiz 1 Just in Time SystemDocument5 pagesQuiz 1 Just in Time SystemMicah CarpioNo ratings yet

- Check Book Register: Account InfoDocument3 pagesCheck Book Register: Account InfodlkfaNo ratings yet

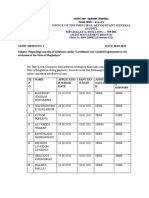

- Office of The Principal Accountant General (AUDIT), Meghalaya, Shillong - 793 001Document11 pagesOffice of The Principal Accountant General (AUDIT), Meghalaya, Shillong - 793 001ronald reaganNo ratings yet

- Conso NotesDocument17 pagesConso NotesShalini GazulaNo ratings yet

- Account Statement For Account:0114002101107545: Branch DetailsDocument4 pagesAccount Statement For Account:0114002101107545: Branch DetailsHappy JainNo ratings yet

- 2023 - Q1 Press Release BAM - FDocument9 pages2023 - Q1 Press Release BAM - FJ Pierre RicherNo ratings yet

- Acs 304. Financial Mathematics IiDocument5 pagesAcs 304. Financial Mathematics IiKimondo KingNo ratings yet

- Payment Receipt 12thDocument2 pagesPayment Receipt 12thMrunal WaghchaureNo ratings yet

- Mac Trading Company Comparative Balance Sheet For The Year Ended December 20CY 20CY 20PYDocument8 pagesMac Trading Company Comparative Balance Sheet For The Year Ended December 20CY 20CY 20PYJoymee BigorniaNo ratings yet

- S N A P - 3 4 0 4 3: CashbackDocument6 pagesS N A P - 3 4 0 4 3: CashbackNS financeNo ratings yet

- Basic Accounting QuestionnaireDocument5 pagesBasic Accounting Questionnaireangeline bulacanNo ratings yet

- Mobile Money - Investment Opportunities For SACCOsDocument20 pagesMobile Money - Investment Opportunities For SACCOsKivumbi WilliamNo ratings yet

- 10 V3 - 20201026 - CFA一级押题 - 组合管理 - 泽才教育Document29 pages10 V3 - 20201026 - CFA一级押题 - 组合管理 - 泽才教育Bowen ZhangNo ratings yet

- Live Better Savings Account Statement: Capitec B AnkDocument1 pageLive Better Savings Account Statement: Capitec B AnkManzini MlebogengNo ratings yet

- (BANKING LAWS) Classification of BanksDocument3 pages(BANKING LAWS) Classification of BanksZyril MarchanNo ratings yet

- Measuring and Evaluate Bank PerformanceDocument1 pageMeasuring and Evaluate Bank PerformanceNguyen Hoai HuongNo ratings yet

- Principles of Sound Lending: SafetyDocument3 pagesPrinciples of Sound Lending: Safety18UCOM040 Saravanakumar ANo ratings yet

- Control Account Reconciliations ExamplesDocument3 pagesControl Account Reconciliations ExamplesRameen FatimaNo ratings yet

- Notes Compiled - 230218 - 135429Document125 pagesNotes Compiled - 230218 - 135429Bidhan SapkotaNo ratings yet

- e-StatementBRImo 023801082631503 Jan2024 20240325 104605Document2 pagese-StatementBRImo 023801082631503 Jan2024 20240325 104605nda658915No ratings yet

- Whats Really Going On in CourtDocument632 pagesWhats Really Going On in CourtCarla DiCapriNo ratings yet

- Đoạn văn câu hỏiDocument51 pagesĐoạn văn câu hỏiMinh MinhNo ratings yet

- Co Opbanksfinal PDFDocument13 pagesCo Opbanksfinal PDFAJAY SHAHNo ratings yet

- Accounts Receivables: To Mr. ZulfiqarDocument14 pagesAccounts Receivables: To Mr. ZulfiqarJM LangamanNo ratings yet

- Jarvis Money Market Fund DESEMBER 2022Document4 pagesJarvis Money Market Fund DESEMBER 2022Dhanik JayantiNo ratings yet

- Health Insurance Presentation. (Fn-26)Document19 pagesHealth Insurance Presentation. (Fn-26)m_dattaiasNo ratings yet

- VII-ADJUSTING Answer ENTRIES-DOUBTFUL ACCOUNTSDocument4 pagesVII-ADJUSTING Answer ENTRIES-DOUBTFUL ACCOUNTSHassanhor Guro BacolodNo ratings yet