Forms Involeved in ACCA T9 F6 and There After

Forms Involeved in ACCA T9 F6 and There After

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Eo No. 8b-Tourism Assistance DeskDocument2 pagesEo No. 8b-Tourism Assistance Deskcheryl ann100% (2)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Transfer Letter For Cars Registrartion Pakistan PunjabDocument1 pageTransfer Letter For Cars Registrartion Pakistan PunjabM Muneeb Saeed58% (12)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Cost Accounting Past PapersDocument66 pagesCost Accounting Past Paperssalamankhana100% (2)

- Killer TechnologyDocument2 pagesKiller TechnologyJuan Carlos VinascoNo ratings yet

- Education: Oxford English DictionaryDocument6 pagesEducation: Oxford English DictionaryM Muneeb SaeedNo ratings yet

- CIA HandbookDocument42 pagesCIA HandbookMuhammad UsmanNo ratings yet

- F9 Practice Question Sassone PLC INVESTMENT APPRAISALDocument3 pagesF9 Practice Question Sassone PLC INVESTMENT APPRAISALM Muneeb Saeed0% (1)

- Objective: Sr. # Degree Subjects Institution Board Year Marks DivisionDocument2 pagesObjective: Sr. # Degree Subjects Institution Board Year Marks DivisionM Muneeb SaeedNo ratings yet

- Acca Approved EmployersDocument2 pagesAcca Approved EmployersAsim Khalil100% (1)

- Please Choose One of The Topics Below:: History Categories of ComputersDocument32 pagesPlease Choose One of The Topics Below:: History Categories of ComputersM Muneeb SaeedNo ratings yet

- How To Check Your MobileDocument3 pagesHow To Check Your MobileM Muneeb SaeedNo ratings yet

- British Council Report Pakistan: The Next GenerationDocument45 pagesBritish Council Report Pakistan: The Next GenerationM Muneeb SaeedNo ratings yet

- Purchase Serial Number: VS13RNL-EDC8H6P-8BDD4MR-UVWU5UJ Activation Code:646F-AD6B-EDBE-0900-C4A9Document1 pagePurchase Serial Number: VS13RNL-EDC8H6P-8BDD4MR-UVWU5UJ Activation Code:646F-AD6B-EDBE-0900-C4A9M Muneeb SaeedNo ratings yet

- Standard Costing ACCA t4 t7 f5Document6 pagesStandard Costing ACCA t4 t7 f5M Muneeb SaeedNo ratings yet

- Ion Onl Y: Copy For HM Revenue & CustomsDocument4 pagesIon Onl Y: Copy For HM Revenue & CustomsM Muneeb SaeedNo ratings yet

- ACCA Answer BookletDocument1 pageACCA Answer BookletM Muneeb Saeed0% (1)

- Struggle For DemocracyDocument2 pagesStruggle For DemocracyM Muneeb SaeedNo ratings yet

- Organizing ProductionDocument50 pagesOrganizing ProductionMohammad Raihanul HasanNo ratings yet

- Currency OverlayDocument6 pagesCurrency OverlayprankyaquariusNo ratings yet

- 2.0 FIN Plan & Forecasting v1Document62 pages2.0 FIN Plan & Forecasting v1Omer CrestianiNo ratings yet

- Contract DocumentDocument45 pagesContract DocumentEngineeri TadiyosNo ratings yet

- The Second Wave Resilient Inclusive Exponential FintechsDocument70 pagesThe Second Wave Resilient Inclusive Exponential FintechsjlknspceppuqowxxtaNo ratings yet

- Staple Food Prices in Ethiopia: Shahidur RashidDocument15 pagesStaple Food Prices in Ethiopia: Shahidur RashidNebiyu SamuelNo ratings yet

- IAS 10 Events After The Reporting Period: 02/15/2022 Delight Training &consulting CenterDocument11 pagesIAS 10 Events After The Reporting Period: 02/15/2022 Delight Training &consulting CenterNimona BeyeneNo ratings yet

- Alexa Ilagan Report For SRGGDocument31 pagesAlexa Ilagan Report For SRGGALEXA MAE ILAGANNo ratings yet

- Competitiveness in Global Trade: The Case of The Automobile IndustryDocument25 pagesCompetitiveness in Global Trade: The Case of The Automobile IndustryKhánh Nguyễn NgHNo ratings yet

- C7 Problem 13Document2 pagesC7 Problem 13Erica CastroNo ratings yet

- Basta Ayun Na YunDocument2 pagesBasta Ayun Na YunAngelo ReyesNo ratings yet

- Reviewer in GE 113Document14 pagesReviewer in GE 113John Rafael Monteverde AcuñaNo ratings yet

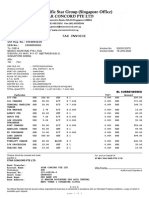

- Invoice SII22012979Document2 pagesInvoice SII22012979Summersky9333No ratings yet

- Thrift Banks and Rural BanksDocument14 pagesThrift Banks and Rural BanksrowelmanigbasNo ratings yet

- Week No. 2 (2 Quarter) Information Sheet: Baybay City DivisionDocument5 pagesWeek No. 2 (2 Quarter) Information Sheet: Baybay City DivisionDeona FayeNo ratings yet

- 2.05 AssignmentDocument3 pages2.05 Assignmentthethingsidoformyfriends6No ratings yet

- Cost of Living Project-1Document3 pagesCost of Living Project-1Eric MendozaNo ratings yet

- Jadwa Tugas OKTOBER-1Document1 pageJadwa Tugas OKTOBER-1Syahreza FahleviNo ratings yet

- T3 - Salient Features and ContractsDocument49 pagesT3 - Salient Features and Contractsmichael musillaNo ratings yet

- 1-B Inventory of LGU Functions, Services and Facilities For Barangays (Annex E-2)Document41 pages1-B Inventory of LGU Functions, Services and Facilities For Barangays (Annex E-2)Barangay Poblacion NaawanNo ratings yet

- Lista Contribuabililor Mari 2014Document57 pagesLista Contribuabililor Mari 2014szeni_csNo ratings yet

- Elasticity Practice Sheet: Micro Topics 2.3, 2.4 and 2.5Document1 pageElasticity Practice Sheet: Micro Topics 2.3, 2.4 and 2.5Evelyn Hsu徐御庭No ratings yet

- Free School Supplies For Indigent Elementary Pupils of Barangay Libertad Every SummerDocument5 pagesFree School Supplies For Indigent Elementary Pupils of Barangay Libertad Every SummerÃrtçhïè Ømápöy VīllâflørNo ratings yet

- TCS Express CentersDocument1 pageTCS Express CentersMuzammilNo ratings yet

- Sentence CorrectionDocument21 pagesSentence CorrectionSrinivasan Saai Mahesh 16BCE0559No ratings yet

- Business Environment Quality Model in The SME SegmentDocument23 pagesBusiness Environment Quality Model in The SME SegmentRubenAmarilleMedinaJr.No ratings yet

- Midterm1 ECON122 DDocument5 pagesMidterm1 ECON122 DyanabudaghyanNo ratings yet

- Legal Form:: Brief Description of The Project Name of BusinessDocument20 pagesLegal Form:: Brief Description of The Project Name of BusinessMuktar jiboNo ratings yet

Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Eo No. 8b-Tourism Assistance DeskDocument2 pagesEo No. 8b-Tourism Assistance Deskcheryl ann100% (2)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Transfer Letter For Cars Registrartion Pakistan PunjabDocument1 pageTransfer Letter For Cars Registrartion Pakistan PunjabM Muneeb Saeed58% (12)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Cost Accounting Past PapersDocument66 pagesCost Accounting Past Paperssalamankhana100% (2)

- Killer TechnologyDocument2 pagesKiller TechnologyJuan Carlos VinascoNo ratings yet

- Education: Oxford English DictionaryDocument6 pagesEducation: Oxford English DictionaryM Muneeb SaeedNo ratings yet

- CIA HandbookDocument42 pagesCIA HandbookMuhammad UsmanNo ratings yet

- F9 Practice Question Sassone PLC INVESTMENT APPRAISALDocument3 pagesF9 Practice Question Sassone PLC INVESTMENT APPRAISALM Muneeb Saeed0% (1)

- Objective: Sr. # Degree Subjects Institution Board Year Marks DivisionDocument2 pagesObjective: Sr. # Degree Subjects Institution Board Year Marks DivisionM Muneeb SaeedNo ratings yet

- Acca Approved EmployersDocument2 pagesAcca Approved EmployersAsim Khalil100% (1)

- Please Choose One of The Topics Below:: History Categories of ComputersDocument32 pagesPlease Choose One of The Topics Below:: History Categories of ComputersM Muneeb SaeedNo ratings yet

- How To Check Your MobileDocument3 pagesHow To Check Your MobileM Muneeb SaeedNo ratings yet

- British Council Report Pakistan: The Next GenerationDocument45 pagesBritish Council Report Pakistan: The Next GenerationM Muneeb SaeedNo ratings yet

- Purchase Serial Number: VS13RNL-EDC8H6P-8BDD4MR-UVWU5UJ Activation Code:646F-AD6B-EDBE-0900-C4A9Document1 pagePurchase Serial Number: VS13RNL-EDC8H6P-8BDD4MR-UVWU5UJ Activation Code:646F-AD6B-EDBE-0900-C4A9M Muneeb SaeedNo ratings yet

- Standard Costing ACCA t4 t7 f5Document6 pagesStandard Costing ACCA t4 t7 f5M Muneeb SaeedNo ratings yet

- Ion Onl Y: Copy For HM Revenue & CustomsDocument4 pagesIon Onl Y: Copy For HM Revenue & CustomsM Muneeb SaeedNo ratings yet

- ACCA Answer BookletDocument1 pageACCA Answer BookletM Muneeb Saeed0% (1)

- Struggle For DemocracyDocument2 pagesStruggle For DemocracyM Muneeb SaeedNo ratings yet

- Organizing ProductionDocument50 pagesOrganizing ProductionMohammad Raihanul HasanNo ratings yet

- Currency OverlayDocument6 pagesCurrency OverlayprankyaquariusNo ratings yet

- 2.0 FIN Plan & Forecasting v1Document62 pages2.0 FIN Plan & Forecasting v1Omer CrestianiNo ratings yet

- Contract DocumentDocument45 pagesContract DocumentEngineeri TadiyosNo ratings yet

- The Second Wave Resilient Inclusive Exponential FintechsDocument70 pagesThe Second Wave Resilient Inclusive Exponential FintechsjlknspceppuqowxxtaNo ratings yet

- Staple Food Prices in Ethiopia: Shahidur RashidDocument15 pagesStaple Food Prices in Ethiopia: Shahidur RashidNebiyu SamuelNo ratings yet

- IAS 10 Events After The Reporting Period: 02/15/2022 Delight Training &consulting CenterDocument11 pagesIAS 10 Events After The Reporting Period: 02/15/2022 Delight Training &consulting CenterNimona BeyeneNo ratings yet

- Alexa Ilagan Report For SRGGDocument31 pagesAlexa Ilagan Report For SRGGALEXA MAE ILAGANNo ratings yet

- Competitiveness in Global Trade: The Case of The Automobile IndustryDocument25 pagesCompetitiveness in Global Trade: The Case of The Automobile IndustryKhánh Nguyễn NgHNo ratings yet

- C7 Problem 13Document2 pagesC7 Problem 13Erica CastroNo ratings yet

- Basta Ayun Na YunDocument2 pagesBasta Ayun Na YunAngelo ReyesNo ratings yet

- Reviewer in GE 113Document14 pagesReviewer in GE 113John Rafael Monteverde AcuñaNo ratings yet

- Invoice SII22012979Document2 pagesInvoice SII22012979Summersky9333No ratings yet

- Thrift Banks and Rural BanksDocument14 pagesThrift Banks and Rural BanksrowelmanigbasNo ratings yet

- Week No. 2 (2 Quarter) Information Sheet: Baybay City DivisionDocument5 pagesWeek No. 2 (2 Quarter) Information Sheet: Baybay City DivisionDeona FayeNo ratings yet

- 2.05 AssignmentDocument3 pages2.05 Assignmentthethingsidoformyfriends6No ratings yet

- Cost of Living Project-1Document3 pagesCost of Living Project-1Eric MendozaNo ratings yet

- Jadwa Tugas OKTOBER-1Document1 pageJadwa Tugas OKTOBER-1Syahreza FahleviNo ratings yet

- T3 - Salient Features and ContractsDocument49 pagesT3 - Salient Features and Contractsmichael musillaNo ratings yet

- 1-B Inventory of LGU Functions, Services and Facilities For Barangays (Annex E-2)Document41 pages1-B Inventory of LGU Functions, Services and Facilities For Barangays (Annex E-2)Barangay Poblacion NaawanNo ratings yet

- Lista Contribuabililor Mari 2014Document57 pagesLista Contribuabililor Mari 2014szeni_csNo ratings yet

- Elasticity Practice Sheet: Micro Topics 2.3, 2.4 and 2.5Document1 pageElasticity Practice Sheet: Micro Topics 2.3, 2.4 and 2.5Evelyn Hsu徐御庭No ratings yet

- Free School Supplies For Indigent Elementary Pupils of Barangay Libertad Every SummerDocument5 pagesFree School Supplies For Indigent Elementary Pupils of Barangay Libertad Every SummerÃrtçhïè Ømápöy VīllâflørNo ratings yet

- TCS Express CentersDocument1 pageTCS Express CentersMuzammilNo ratings yet

- Sentence CorrectionDocument21 pagesSentence CorrectionSrinivasan Saai Mahesh 16BCE0559No ratings yet

- Business Environment Quality Model in The SME SegmentDocument23 pagesBusiness Environment Quality Model in The SME SegmentRubenAmarilleMedinaJr.No ratings yet

- Midterm1 ECON122 DDocument5 pagesMidterm1 ECON122 DyanabudaghyanNo ratings yet

- Legal Form:: Brief Description of The Project Name of BusinessDocument20 pagesLegal Form:: Brief Description of The Project Name of BusinessMuktar jiboNo ratings yet