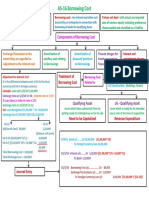

NAS 23 Borrowing Cost

NAS 23 Borrowing Cost

You might also like

- Chapter 1: Base Knowledge Worksheet: Name: - DateDocument370 pagesChapter 1: Base Knowledge Worksheet: Name: - DateMartim Coutinho100% (2)

- Crisis Assessment Intervention and Prevention 2nd Edition Cherry Test BankDocument22 pagesCrisis Assessment Intervention and Prevention 2nd Edition Cherry Test Bankdolium.technic.1i5d67100% (36)

- G.R. No. L-35925. January 22, 1973 DigestDocument3 pagesG.R. No. L-35925. January 22, 1973 DigestMaritoni Roxas100% (1)

- 13.8 AS 16 Borrowing CostsDocument8 pages13.8 AS 16 Borrowing CostsAakshi SharmaNo ratings yet

- Ch2-2 IAS23 Borrowing CostsDocument16 pagesCh2-2 IAS23 Borrowing Costsxu lNo ratings yet

- Chapter 3 - IAS 23Document5 pagesChapter 3 - IAS 23Chandan SamalNo ratings yet

- Topic 4 - Borrowing Cost - MFRS 123Document21 pagesTopic 4 - Borrowing Cost - MFRS 1232023105069No ratings yet

- PCOA Module 6 - PAS 23 and 24Document8 pagesPCOA Module 6 - PAS 23 and 24Jan JanNo ratings yet

- PDF Presentasi SiklusproduksipadaptfapptxDocument27 pagesPDF Presentasi SiklusproduksipadaptfapptxJessica AlodiaNo ratings yet

- PAS 23 Borrowing Costs: Learning ObjectivesDocument5 pagesPAS 23 Borrowing Costs: Learning ObjectivesFhrince Carl CalaquianNo ratings yet

- Module 6 CFAS PAS 23 - BORROWING COSTDocument6 pagesModule 6 CFAS PAS 23 - BORROWING COSTJan JanNo ratings yet

- FInancial ReportingDocument2 pagesFInancial ReportingSuhag PatelNo ratings yet

- LESSON5Document5 pagesLESSON5Ira Charisse BurlaosNo ratings yet

- PF 1-4 2023 - RescheduledDocument240 pagesPF 1-4 2023 - RescheduledZJ XNo ratings yet

- Quiz 1 Far510 MFRS120 123 PDFDocument4 pagesQuiz 1 Far510 MFRS120 123 PDFiirene.ntshNo ratings yet

- UasDocument16 pagesUasAngela BrendaNo ratings yet

- IAS 23 Borrowing Cost F7Document10 pagesIAS 23 Borrowing Cost F7Maria100% (1)

- Financial Accounting 3B Assignment 2Document6 pagesFinancial Accounting 3B Assignment 2NangulaNo ratings yet

- BORROWING COSTS Supplementary Review MaterialDocument2 pagesBORROWING COSTS Supplementary Review MaterialCaseylyn RonquilloNo ratings yet

- LEC03E - BSA 2102 - 012021-Borrowing CostsDocument2 pagesLEC03E - BSA 2102 - 012021-Borrowing CostsKatarame LermanNo ratings yet

- Borrowing CostsDocument12 pagesBorrowing CostsTaimur ShahidNo ratings yet

- IAS 23 Borrowing CostDocument6 pagesIAS 23 Borrowing CostButt ArhamNo ratings yet

- IAS 23 Borrowing CostDocument6 pagesIAS 23 Borrowing CostArm ButtNo ratings yet

- As 16 PDFDocument2 pagesAs 16 PDFRamNo ratings yet

- Module 11 - Borrowing CostsDocument6 pagesModule 11 - Borrowing CostsJehPoyNo ratings yet

- IAS-23 (Borrowing Costs)Document5 pagesIAS-23 (Borrowing Costs)Nazmul HaqueNo ratings yet

- Ind As 23Document6 pagesInd As 23Savin AdhikaryNo ratings yet

- MFRS123Document23 pagesMFRS123Kelvin Leong100% (1)

- Module 3 - Borrowing CostsDocument3 pagesModule 3 - Borrowing CostsLui100% (1)

- Intacc 2Document22 pagesIntacc 2AngelKate MicabaniNo ratings yet

- CA Inter Accounts Suggested Ans Nov23 Castudynotes ComDocument31 pagesCA Inter Accounts Suggested Ans Nov23 Castudynotes ComShivaram ShivaramNo ratings yet

- Pas 23Document11 pagesPas 23Justine VeralloNo ratings yet

- Common Loan Appln Upto Rs 2 CroreDocument7 pagesCommon Loan Appln Upto Rs 2 CroreAashish DabhadeNo ratings yet

- Citn & Icag-11Document1 pageCitn & Icag-11AKINROYEJE TEMITOPENo ratings yet

- Annual Budget For The Operating Costs: Page 1 of 4Document4 pagesAnnual Budget For The Operating Costs: Page 1 of 4swarna dasNo ratings yet

- 05 Handout 1Document18 pages05 Handout 1Jay PinedaNo ratings yet

- Ias 23Document18 pagesIas 23Shah KamalNo ratings yet

- Material of As 16Document21 pagesMaterial of As 16emmanuel JohnyNo ratings yet

- As 16Document10 pagesAs 16RAJASHEKARNo ratings yet

- Borrowing Costs IAS 23Document10 pagesBorrowing Costs IAS 23Tinashe ZhouNo ratings yet

- Ind As 23 - SolutionsDocument10 pagesInd As 23 - Solutionssoumya saswatNo ratings yet

- CM All AS SummaryDocument64 pagesCM All AS SummaryP KarthikeyanNo ratings yet

- 5.IAS 23 .Borrowing Cost Q&ADocument12 pages5.IAS 23 .Borrowing Cost Q&AAbdulkarim Hamisi KufakunogaNo ratings yet

- FR Session 2 - 8th July 2023Document40 pagesFR Session 2 - 8th July 2023irmaya.safitraNo ratings yet

- Ias: 23 Barrowing Cost: What Are Qualifying Assets?Document4 pagesIas: 23 Barrowing Cost: What Are Qualifying Assets?nishanthanNo ratings yet

- Review Material - ACCE 411Document5 pagesReview Material - ACCE 411zee abadillaNo ratings yet

- Chapter13 HKAS23Document9 pagesChapter13 HKAS23Kelviw02 WuuoqwoNo ratings yet

- Accounting Standard (AS) - 16 Borrowing Costs: Vinod JainDocument29 pagesAccounting Standard (AS) - 16 Borrowing Costs: Vinod Jainpriyajas303No ratings yet

- Borrowing CostsDocument4 pagesBorrowing CostsNoella Marie BaronNo ratings yet

- IC 1928-2020union MudraDocument11 pagesIC 1928-2020union Mudraamit_200619No ratings yet

- Model DPR For End Borrower DIDF Scheme 05 Jan2018Document52 pagesModel DPR For End Borrower DIDF Scheme 05 Jan2018muthukrishnanNo ratings yet

- To Complete This Workbook, Answer The Questions On Each WorksheetDocument12 pagesTo Complete This Workbook, Answer The Questions On Each WorksheetRizza L. MacarandanNo ratings yet

- CA-365 190117-AsDocument5 pagesCA-365 190117-AsGmt HspNo ratings yet

- International Accounting Standard 23Document4 pagesInternational Accounting Standard 23sami ullahNo ratings yet

- IPSAS 25 Borrowing CostsDocument24 pagesIPSAS 25 Borrowing CostsKibromWeldegiyorgisNo ratings yet

- Indv FINNANCEDocument7 pagesIndv FINNANCEMuhammad Aiezaqul Haikal bin ZainuriNo ratings yet

- AS 16 Borrowing CostsDocument16 pagesAS 16 Borrowing CostsRENU PALINo ratings yet

- EdgeReport UTKARSHBNK IPONotes 11 07 2023 599Document21 pagesEdgeReport UTKARSHBNK IPONotes 11 07 2023 599prashant_natureNo ratings yet

- 6 - As-16 Borrowing CostsDocument15 pages6 - As-16 Borrowing CostsKrishna JhaNo ratings yet

- Case 7.3 and 8Document24 pagesCase 7.3 and 8Bertha Muhammad SyahNo ratings yet

- Exrcises and Topics For Discussions DB 2024Document6 pagesExrcises and Topics For Discussions DB 2024Nguyễn Hồng HạnhNo ratings yet

- Investment Climate Reforms: An Independent Evaluation of World Bank Group Support to Reforms of Business RegulationsFrom EverandInvestment Climate Reforms: An Independent Evaluation of World Bank Group Support to Reforms of Business RegulationsNo ratings yet

- NAS 37 Provision, Contingent Asset and Contingent LiabilitiesDocument5 pagesNAS 37 Provision, Contingent Asset and Contingent LiabilitiesPrashant TamangNo ratings yet

- NAS 37 Provision, Contingent Asset and Contingent LiabilitiesDocument5 pagesNAS 37 Provision, Contingent Asset and Contingent LiabilitiesPrashant TamangNo ratings yet

- Advanced Financial Reporting Marks WeightageDocument3 pagesAdvanced Financial Reporting Marks WeightagePrashant TamangNo ratings yet

- Unit Overview:: NAS 17 Lease Revision Note Relevant For CAP-II StudentsDocument11 pagesUnit Overview:: NAS 17 Lease Revision Note Relevant For CAP-II StudentsPrashant TamangNo ratings yet

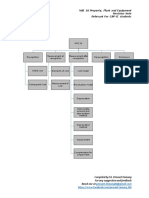

- NAS 16-Property, Plant and EquipmentDocument10 pagesNAS 16-Property, Plant and EquipmentPrashant TamangNo ratings yet

- Unit Overview:: NAS 2 Inventories Revision Note Relevant For CAP-II StudentsDocument13 pagesUnit Overview:: NAS 2 Inventories Revision Note Relevant For CAP-II StudentsPrashant TamangNo ratings yet

- NAS 2 InventoriesDocument12 pagesNAS 2 InventoriesPrashant TamangNo ratings yet

- Importance of The Marketing Environment Analysis IDocument9 pagesImportance of The Marketing Environment Analysis IkatieNo ratings yet

- Ivylorainepenriquez: Page1of4 248brgymaahas 0 9 1 9 - 2 8 2 5 - 1 7 Lagunalosbanos 4 0 3 0Document4 pagesIvylorainepenriquez: Page1of4 248brgymaahas 0 9 1 9 - 2 8 2 5 - 1 7 Lagunalosbanos 4 0 3 0ivy loraine enriquezNo ratings yet

- Brief History Jeep. 22Document2 pagesBrief History Jeep. 22Crystal Jane Tic-ing100% (1)

- Banking SWOT Analysis v2Document29 pagesBanking SWOT Analysis v2Chiraroj AngsumaleeNo ratings yet

- N-23-05 Republic V EquitableDocument1 pageN-23-05 Republic V EquitableAndrew GallardoNo ratings yet

- Appearance and Non-Appearance of The PartyDocument16 pagesAppearance and Non-Appearance of The PartySlim ShadyNo ratings yet

- 1 - Prosodic Features of Speech-COMPLETEDocument39 pages1 - Prosodic Features of Speech-COMPLETEMendoza EmmaNo ratings yet

- Jerome Littles NewspaperDocument14 pagesJerome Littles NewspaperJerome LittlesNo ratings yet

- Pag Ibig FundDocument5 pagesPag Ibig FundeyNo ratings yet

- MUH 2512 Exam 2 Study GuideDocument14 pagesMUH 2512 Exam 2 Study GuideAlan DeVall100% (1)

- ISFIF Programme Schedule - 08 12 2017Document31 pagesISFIF Programme Schedule - 08 12 2017Saurav DashNo ratings yet

- Assemblage Art Shadow Box Eller's ArtistsDocument1 pageAssemblage Art Shadow Box Eller's ArtistsRadu CiurariuNo ratings yet

- Financial Results, Limited Review Report For December 31, 2015 (Result)Document4 pagesFinancial Results, Limited Review Report For December 31, 2015 (Result)Shyam SunderNo ratings yet

- FFG Star Wars RPG EquipmentDocument44 pagesFFG Star Wars RPG EquipmentguiloNo ratings yet

- YCMOU Study Center Submission Slip: Application No: Distance EducationDocument4 pagesYCMOU Study Center Submission Slip: Application No: Distance Educationvaibhavpardeshi55No ratings yet

- Inglés Ix: Dra. Mercy Noelia Páliza ChampiDocument30 pagesInglés Ix: Dra. Mercy Noelia Páliza ChampiEdwin Christian Laurente HuertasNo ratings yet

- Cadenas Drives USA PDFDocument238 pagesCadenas Drives USA PDFCamilo Araya ArayaNo ratings yet

- Company Information: 32nd Street Corner 7th Avenue, Bonifacio Global City @globemybusiness Taguig, PhilippinesDocument3 pagesCompany Information: 32nd Street Corner 7th Avenue, Bonifacio Global City @globemybusiness Taguig, PhilippinesTequila Mhae LopezNo ratings yet

- PF Enomination Job AidDocument9 pagesPF Enomination Job Aidashritha prakashNo ratings yet

- Https Ecf - Njb.uscourts - Gov Cgi-Bin DKTRPTDocument2 pagesHttps Ecf - Njb.uscourts - Gov Cgi-Bin DKTRPTBill Singh100% (1)

- Rowan AtkinsonDocument5 pagesRowan AtkinsonDelia AndreeaNo ratings yet

- Daniel Burnham in The PhilippinesDocument6 pagesDaniel Burnham in The PhilippinesJanelleNo ratings yet

- SpaceHulk Death AngelDocument5 pagesSpaceHulk Death Angelfuffa02No ratings yet

- Possessive Adjectives: Interchange 1Document4 pagesPossessive Adjectives: Interchange 1Islam MohammadNo ratings yet

- Current Affairs of February 2024Document36 pagesCurrent Affairs of February 2024imrankhan872019No ratings yet

- BH Eu 05 SensepostDocument37 pagesBH Eu 05 SensepostblwztrainingNo ratings yet

- Tese - Cristiana AlmeidaDocument257 pagesTese - Cristiana AlmeidaDeia AlmeidaNo ratings yet

Download as pdf or txt

You might also like

- Chapter 1: Base Knowledge Worksheet: Name: - DateDocument370 pagesChapter 1: Base Knowledge Worksheet: Name: - DateMartim Coutinho100% (2)

- Crisis Assessment Intervention and Prevention 2nd Edition Cherry Test BankDocument22 pagesCrisis Assessment Intervention and Prevention 2nd Edition Cherry Test Bankdolium.technic.1i5d67100% (36)

- G.R. No. L-35925. January 22, 1973 DigestDocument3 pagesG.R. No. L-35925. January 22, 1973 DigestMaritoni Roxas100% (1)

- 13.8 AS 16 Borrowing CostsDocument8 pages13.8 AS 16 Borrowing CostsAakshi SharmaNo ratings yet

- Ch2-2 IAS23 Borrowing CostsDocument16 pagesCh2-2 IAS23 Borrowing Costsxu lNo ratings yet

- Chapter 3 - IAS 23Document5 pagesChapter 3 - IAS 23Chandan SamalNo ratings yet

- Topic 4 - Borrowing Cost - MFRS 123Document21 pagesTopic 4 - Borrowing Cost - MFRS 1232023105069No ratings yet

- PCOA Module 6 - PAS 23 and 24Document8 pagesPCOA Module 6 - PAS 23 and 24Jan JanNo ratings yet

- PDF Presentasi SiklusproduksipadaptfapptxDocument27 pagesPDF Presentasi SiklusproduksipadaptfapptxJessica AlodiaNo ratings yet

- PAS 23 Borrowing Costs: Learning ObjectivesDocument5 pagesPAS 23 Borrowing Costs: Learning ObjectivesFhrince Carl CalaquianNo ratings yet

- Module 6 CFAS PAS 23 - BORROWING COSTDocument6 pagesModule 6 CFAS PAS 23 - BORROWING COSTJan JanNo ratings yet

- FInancial ReportingDocument2 pagesFInancial ReportingSuhag PatelNo ratings yet

- LESSON5Document5 pagesLESSON5Ira Charisse BurlaosNo ratings yet

- PF 1-4 2023 - RescheduledDocument240 pagesPF 1-4 2023 - RescheduledZJ XNo ratings yet

- Quiz 1 Far510 MFRS120 123 PDFDocument4 pagesQuiz 1 Far510 MFRS120 123 PDFiirene.ntshNo ratings yet

- UasDocument16 pagesUasAngela BrendaNo ratings yet

- IAS 23 Borrowing Cost F7Document10 pagesIAS 23 Borrowing Cost F7Maria100% (1)

- Financial Accounting 3B Assignment 2Document6 pagesFinancial Accounting 3B Assignment 2NangulaNo ratings yet

- BORROWING COSTS Supplementary Review MaterialDocument2 pagesBORROWING COSTS Supplementary Review MaterialCaseylyn RonquilloNo ratings yet

- LEC03E - BSA 2102 - 012021-Borrowing CostsDocument2 pagesLEC03E - BSA 2102 - 012021-Borrowing CostsKatarame LermanNo ratings yet

- Borrowing CostsDocument12 pagesBorrowing CostsTaimur ShahidNo ratings yet

- IAS 23 Borrowing CostDocument6 pagesIAS 23 Borrowing CostButt ArhamNo ratings yet

- IAS 23 Borrowing CostDocument6 pagesIAS 23 Borrowing CostArm ButtNo ratings yet

- As 16 PDFDocument2 pagesAs 16 PDFRamNo ratings yet

- Module 11 - Borrowing CostsDocument6 pagesModule 11 - Borrowing CostsJehPoyNo ratings yet

- IAS-23 (Borrowing Costs)Document5 pagesIAS-23 (Borrowing Costs)Nazmul HaqueNo ratings yet

- Ind As 23Document6 pagesInd As 23Savin AdhikaryNo ratings yet

- MFRS123Document23 pagesMFRS123Kelvin Leong100% (1)

- Module 3 - Borrowing CostsDocument3 pagesModule 3 - Borrowing CostsLui100% (1)

- Intacc 2Document22 pagesIntacc 2AngelKate MicabaniNo ratings yet

- CA Inter Accounts Suggested Ans Nov23 Castudynotes ComDocument31 pagesCA Inter Accounts Suggested Ans Nov23 Castudynotes ComShivaram ShivaramNo ratings yet

- Pas 23Document11 pagesPas 23Justine VeralloNo ratings yet

- Common Loan Appln Upto Rs 2 CroreDocument7 pagesCommon Loan Appln Upto Rs 2 CroreAashish DabhadeNo ratings yet

- Citn & Icag-11Document1 pageCitn & Icag-11AKINROYEJE TEMITOPENo ratings yet

- Annual Budget For The Operating Costs: Page 1 of 4Document4 pagesAnnual Budget For The Operating Costs: Page 1 of 4swarna dasNo ratings yet

- 05 Handout 1Document18 pages05 Handout 1Jay PinedaNo ratings yet

- Ias 23Document18 pagesIas 23Shah KamalNo ratings yet

- Material of As 16Document21 pagesMaterial of As 16emmanuel JohnyNo ratings yet

- As 16Document10 pagesAs 16RAJASHEKARNo ratings yet

- Borrowing Costs IAS 23Document10 pagesBorrowing Costs IAS 23Tinashe ZhouNo ratings yet

- Ind As 23 - SolutionsDocument10 pagesInd As 23 - Solutionssoumya saswatNo ratings yet

- CM All AS SummaryDocument64 pagesCM All AS SummaryP KarthikeyanNo ratings yet

- 5.IAS 23 .Borrowing Cost Q&ADocument12 pages5.IAS 23 .Borrowing Cost Q&AAbdulkarim Hamisi KufakunogaNo ratings yet

- FR Session 2 - 8th July 2023Document40 pagesFR Session 2 - 8th July 2023irmaya.safitraNo ratings yet

- Ias: 23 Barrowing Cost: What Are Qualifying Assets?Document4 pagesIas: 23 Barrowing Cost: What Are Qualifying Assets?nishanthanNo ratings yet

- Review Material - ACCE 411Document5 pagesReview Material - ACCE 411zee abadillaNo ratings yet

- Chapter13 HKAS23Document9 pagesChapter13 HKAS23Kelviw02 WuuoqwoNo ratings yet

- Accounting Standard (AS) - 16 Borrowing Costs: Vinod JainDocument29 pagesAccounting Standard (AS) - 16 Borrowing Costs: Vinod Jainpriyajas303No ratings yet

- Borrowing CostsDocument4 pagesBorrowing CostsNoella Marie BaronNo ratings yet

- IC 1928-2020union MudraDocument11 pagesIC 1928-2020union Mudraamit_200619No ratings yet

- Model DPR For End Borrower DIDF Scheme 05 Jan2018Document52 pagesModel DPR For End Borrower DIDF Scheme 05 Jan2018muthukrishnanNo ratings yet

- To Complete This Workbook, Answer The Questions On Each WorksheetDocument12 pagesTo Complete This Workbook, Answer The Questions On Each WorksheetRizza L. MacarandanNo ratings yet

- CA-365 190117-AsDocument5 pagesCA-365 190117-AsGmt HspNo ratings yet

- International Accounting Standard 23Document4 pagesInternational Accounting Standard 23sami ullahNo ratings yet

- IPSAS 25 Borrowing CostsDocument24 pagesIPSAS 25 Borrowing CostsKibromWeldegiyorgisNo ratings yet

- Indv FINNANCEDocument7 pagesIndv FINNANCEMuhammad Aiezaqul Haikal bin ZainuriNo ratings yet

- AS 16 Borrowing CostsDocument16 pagesAS 16 Borrowing CostsRENU PALINo ratings yet

- EdgeReport UTKARSHBNK IPONotes 11 07 2023 599Document21 pagesEdgeReport UTKARSHBNK IPONotes 11 07 2023 599prashant_natureNo ratings yet

- 6 - As-16 Borrowing CostsDocument15 pages6 - As-16 Borrowing CostsKrishna JhaNo ratings yet

- Case 7.3 and 8Document24 pagesCase 7.3 and 8Bertha Muhammad SyahNo ratings yet

- Exrcises and Topics For Discussions DB 2024Document6 pagesExrcises and Topics For Discussions DB 2024Nguyễn Hồng HạnhNo ratings yet

- Investment Climate Reforms: An Independent Evaluation of World Bank Group Support to Reforms of Business RegulationsFrom EverandInvestment Climate Reforms: An Independent Evaluation of World Bank Group Support to Reforms of Business RegulationsNo ratings yet

- NAS 37 Provision, Contingent Asset and Contingent LiabilitiesDocument5 pagesNAS 37 Provision, Contingent Asset and Contingent LiabilitiesPrashant TamangNo ratings yet

- NAS 37 Provision, Contingent Asset and Contingent LiabilitiesDocument5 pagesNAS 37 Provision, Contingent Asset and Contingent LiabilitiesPrashant TamangNo ratings yet

- Advanced Financial Reporting Marks WeightageDocument3 pagesAdvanced Financial Reporting Marks WeightagePrashant TamangNo ratings yet

- Unit Overview:: NAS 17 Lease Revision Note Relevant For CAP-II StudentsDocument11 pagesUnit Overview:: NAS 17 Lease Revision Note Relevant For CAP-II StudentsPrashant TamangNo ratings yet

- NAS 16-Property, Plant and EquipmentDocument10 pagesNAS 16-Property, Plant and EquipmentPrashant TamangNo ratings yet

- Unit Overview:: NAS 2 Inventories Revision Note Relevant For CAP-II StudentsDocument13 pagesUnit Overview:: NAS 2 Inventories Revision Note Relevant For CAP-II StudentsPrashant TamangNo ratings yet

- NAS 2 InventoriesDocument12 pagesNAS 2 InventoriesPrashant TamangNo ratings yet

- Importance of The Marketing Environment Analysis IDocument9 pagesImportance of The Marketing Environment Analysis IkatieNo ratings yet

- Ivylorainepenriquez: Page1of4 248brgymaahas 0 9 1 9 - 2 8 2 5 - 1 7 Lagunalosbanos 4 0 3 0Document4 pagesIvylorainepenriquez: Page1of4 248brgymaahas 0 9 1 9 - 2 8 2 5 - 1 7 Lagunalosbanos 4 0 3 0ivy loraine enriquezNo ratings yet

- Brief History Jeep. 22Document2 pagesBrief History Jeep. 22Crystal Jane Tic-ing100% (1)

- Banking SWOT Analysis v2Document29 pagesBanking SWOT Analysis v2Chiraroj AngsumaleeNo ratings yet

- N-23-05 Republic V EquitableDocument1 pageN-23-05 Republic V EquitableAndrew GallardoNo ratings yet

- Appearance and Non-Appearance of The PartyDocument16 pagesAppearance and Non-Appearance of The PartySlim ShadyNo ratings yet

- 1 - Prosodic Features of Speech-COMPLETEDocument39 pages1 - Prosodic Features of Speech-COMPLETEMendoza EmmaNo ratings yet

- Jerome Littles NewspaperDocument14 pagesJerome Littles NewspaperJerome LittlesNo ratings yet

- Pag Ibig FundDocument5 pagesPag Ibig FundeyNo ratings yet

- MUH 2512 Exam 2 Study GuideDocument14 pagesMUH 2512 Exam 2 Study GuideAlan DeVall100% (1)

- ISFIF Programme Schedule - 08 12 2017Document31 pagesISFIF Programme Schedule - 08 12 2017Saurav DashNo ratings yet

- Assemblage Art Shadow Box Eller's ArtistsDocument1 pageAssemblage Art Shadow Box Eller's ArtistsRadu CiurariuNo ratings yet

- Financial Results, Limited Review Report For December 31, 2015 (Result)Document4 pagesFinancial Results, Limited Review Report For December 31, 2015 (Result)Shyam SunderNo ratings yet

- FFG Star Wars RPG EquipmentDocument44 pagesFFG Star Wars RPG EquipmentguiloNo ratings yet

- YCMOU Study Center Submission Slip: Application No: Distance EducationDocument4 pagesYCMOU Study Center Submission Slip: Application No: Distance Educationvaibhavpardeshi55No ratings yet

- Inglés Ix: Dra. Mercy Noelia Páliza ChampiDocument30 pagesInglés Ix: Dra. Mercy Noelia Páliza ChampiEdwin Christian Laurente HuertasNo ratings yet

- Cadenas Drives USA PDFDocument238 pagesCadenas Drives USA PDFCamilo Araya ArayaNo ratings yet

- Company Information: 32nd Street Corner 7th Avenue, Bonifacio Global City @globemybusiness Taguig, PhilippinesDocument3 pagesCompany Information: 32nd Street Corner 7th Avenue, Bonifacio Global City @globemybusiness Taguig, PhilippinesTequila Mhae LopezNo ratings yet

- PF Enomination Job AidDocument9 pagesPF Enomination Job Aidashritha prakashNo ratings yet

- Https Ecf - Njb.uscourts - Gov Cgi-Bin DKTRPTDocument2 pagesHttps Ecf - Njb.uscourts - Gov Cgi-Bin DKTRPTBill Singh100% (1)

- Rowan AtkinsonDocument5 pagesRowan AtkinsonDelia AndreeaNo ratings yet

- Daniel Burnham in The PhilippinesDocument6 pagesDaniel Burnham in The PhilippinesJanelleNo ratings yet

- SpaceHulk Death AngelDocument5 pagesSpaceHulk Death Angelfuffa02No ratings yet

- Possessive Adjectives: Interchange 1Document4 pagesPossessive Adjectives: Interchange 1Islam MohammadNo ratings yet

- Current Affairs of February 2024Document36 pagesCurrent Affairs of February 2024imrankhan872019No ratings yet

- BH Eu 05 SensepostDocument37 pagesBH Eu 05 SensepostblwztrainingNo ratings yet

- Tese - Cristiana AlmeidaDocument257 pagesTese - Cristiana AlmeidaDeia AlmeidaNo ratings yet