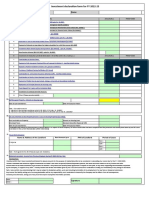

Old Tax Regime of The FY 2019-20 New Tax Regime of FY The 2020-21

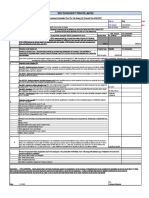

Old Tax Regime of The FY 2019-20 New Tax Regime of FY The 2020-21

You might also like

- Trainors Training On Parent Effectiveness SeminarDocument49 pagesTrainors Training On Parent Effectiveness SeminarBigg Clicks96% (50)

- Investment Declaration Form - 2022-2023Document3 pagesInvestment Declaration Form - 2022-2023Bharathi KNo ratings yet

- F.3 CD Qualico Dev RZDocument96 pagesF.3 CD Qualico Dev RZMiranda GathercoleNo ratings yet

- Gold Experience c1 2nd Edition End of Year Test Main Test ADocument12 pagesGold Experience c1 2nd Edition End of Year Test Main Test APili Hidalgo MoyaNo ratings yet

- A Project Report On Direct TaxDocument53 pagesA Project Report On Direct Taxrani26oct84% (44)

- IT Declaration Form 2020-21Document1 pageIT Declaration Form 2020-21Akshay AcchuNo ratings yet

- The ABC Foundation: Investment Declaration Form For Tax Saving For Financial Year 2018-2019 The Akshaya Patra FoundationDocument1 pageThe ABC Foundation: Investment Declaration Form For Tax Saving For Financial Year 2018-2019 The Akshaya Patra FoundationLantNo ratings yet

- Declaration Form 12BB 2022 23Document4 pagesDeclaration Form 12BB 2022 23S S PradheepanNo ratings yet

- HRA, Chapter VI A - 80CCD, 80C, 80D, Other IncomeDocument9 pagesHRA, Chapter VI A - 80CCD, 80C, 80D, Other Incomefaiyaz432No ratings yet

- Tax Declaration Form 2021 22Document4 pagesTax Declaration Form 2021 22Kasiviswanathan ChinnathambiNo ratings yet

- Income Tax Declaration Form FY 22 23 AY 23 24Document2 pagesIncome Tax Declaration Form FY 22 23 AY 23 24kishoreNo ratings yet

- OLD Income Tax Performa-2021-22Document13 pagesOLD Income Tax Performa-2021-22Research AccountNo ratings yet

- Frequently Asked Questions (Faqs) Tax Deduction at Source On BOB Staff Pension PaymentsDocument4 pagesFrequently Asked Questions (Faqs) Tax Deduction at Source On BOB Staff Pension PaymentsMayur khichiNo ratings yet

- Investment Declaration Form - 1314 - IshitaDocument5 pagesInvestment Declaration Form - 1314 - IshitaIshita AwasthiNo ratings yet

- Employee Tax Declaration - AY 2019-20Document4 pagesEmployee Tax Declaration - AY 2019-20mathuNo ratings yet

- Investment PlanDocument1 pageInvestment PlanNitin AgarwalNo ratings yet

- Employees Proof Submission Form (EPSF) - 2010-11Document1 pageEmployees Proof Submission Form (EPSF) - 2010-11amararenaNo ratings yet

- Portal Investment Proof Verification Guidelines 2022 23Document11 pagesPortal Investment Proof Verification Guidelines 2022 23yfiamataimNo ratings yet

- Declaration Form (22-23)Document4 pagesDeclaration Form (22-23)vasavi kNo ratings yet

- IT Declaration Form 2011-2012Document1 pageIT Declaration Form 2011-2012Shishir RoyNo ratings yet

- BUFIN ITDeclarationFormDocument2 pagesBUFIN ITDeclarationFormdpfsopfopsfhopNo ratings yet

- IT Declaration Form April 2023 To March 2024.Document3 pagesIT Declaration Form April 2023 To March 2024.partha.uneesolutionsNo ratings yet

- O Sec 56 (2) I.E. IOS Clause V, Vi, VII (A & B), Ix, X, XiDocument7 pagesO Sec 56 (2) I.E. IOS Clause V, Vi, VII (A & B), Ix, X, XiRadhika SarawagiNo ratings yet

- Investment Declaration Form (Hemarus)Document4 pagesInvestment Declaration Form (Hemarus)Shashi NaganurNo ratings yet

- Deductions On Section 80CDocument12 pagesDeductions On Section 80CViraja GuruNo ratings yet

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Document5 pages1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiNo ratings yet

- Investment GuidelineDocument3 pagesInvestment GuidelineBuchi YarraNo ratings yet

- Income Tax Declaration Form - F.Y. 2020-21Document8 pagesIncome Tax Declaration Form - F.Y. 2020-21LTelford RudraprayagNo ratings yet

- Investment Declaration Form - 2021-22Document3 pagesInvestment Declaration Form - 2021-22rajamani balajiNo ratings yet

- Investment Declaration Form For The Financial Year 2014 - 15Document7 pagesInvestment Declaration Form For The Financial Year 2014 - 15devanyaNo ratings yet

- Indian Institute of Technology Madras: CircularDocument5 pagesIndian Institute of Technology Madras: CircularAravinthram R am18m002No ratings yet

- Provident FundDocument5 pagesProvident FundG MadhuriNo ratings yet

- Declaration For Proposed Tax Saving Investment and Expenditures For F.Y. 2011 12Document11 pagesDeclaration For Proposed Tax Saving Investment and Expenditures For F.Y. 2011 12nikhiljain17No ratings yet

- Income Decleration PDFDocument2 pagesIncome Decleration PDFvijay dabhiNo ratings yet

- Investment Declaration Form F.Y 2023-24Document4 pagesInvestment Declaration Form F.Y 2023-24Aditi Suryavanshi100% (2)

- 1 .Income Tax On Salaries - (01.06.2015)Document57 pages1 .Income Tax On Salaries - (01.06.2015)yvNo ratings yet

- Tax Proof Submission FY 2021-22Document10 pagesTax Proof Submission FY 2021-22cutieedivyaNo ratings yet

- IT Declaration Form 2019-20Document1 pageIT Declaration Form 2019-20KarunaNo ratings yet

- IT Declaration Form FY 2018-19Document3 pagesIT Declaration Form FY 2018-19sgshekar3050% (2)

- Individual-Txation-FY-2018-19-with - JJDocument64 pagesIndividual-Txation-FY-2018-19-with - JJCOMPLETE ACADEMYNo ratings yet

- For Tds On SalaryDocument40 pagesFor Tds On SalarykshitijsaxenaNo ratings yet

- DownloadDocument6 pagesDownloadpankhewalegNo ratings yet

- Arrina Education Services Pvt. LTD.: Investment Declaration Form (FY 2012-2013)Document2 pagesArrina Education Services Pvt. LTD.: Investment Declaration Form (FY 2012-2013)JITEN2050No ratings yet

- Salaries PresentationDocument21 pagesSalaries PresentationDipika PandaNo ratings yet

- Tax Savings Declarations GuidelinesDocument13 pagesTax Savings Declarations GuidelinesAditya DasNo ratings yet

- DeductionsDocument11 pagesDeductionsguest1No ratings yet

- FAQ On Budget FY 2020-21Document9 pagesFAQ On Budget FY 2020-21GUNANo ratings yet

- Direct TaxesDocument9 pagesDirect TaxesPuneet JindalNo ratings yet

- Income Tax NitDocument6 pagesIncome Tax NitrensisamNo ratings yet

- Deductions From Gross Total Income: Deductions Allowable Under Various Sections of Chapter VIA of Income Tax ActDocument8 pagesDeductions From Gross Total Income: Deductions Allowable Under Various Sections of Chapter VIA of Income Tax ActalisagasaNo ratings yet

- Employee Tax Declaration - AY 2019-20Document1 pageEmployee Tax Declaration - AY 2019-20mathuNo ratings yet

- PPP Loan Forgiveness Application (Revised 6.16.2020)Document5 pagesPPP Loan Forgiveness Application (Revised 6.16.2020)LaurenNo ratings yet

- Guidelines For Income Tax DeclarationDocument9 pagesGuidelines For Income Tax Declarationapoorva1801No ratings yet

- Tax Rebate Claim Form-2019Document2 pagesTax Rebate Claim Form-2019Muhammad Hanif SuchwaniNo ratings yet

- Investment Declaration Form11-12Document2 pagesInvestment Declaration Form11-12girijasankar11No ratings yet

- Income Tax Ready Reckoner 2011-12Document28 pagesIncome Tax Ready Reckoner 2011-12kpksscribdNo ratings yet

- Notes To Investment Proof SubmissionDocument10 pagesNotes To Investment Proof SubmissionVinayak DhotreNo ratings yet

- National Institute of Technology CalicutDocument7 pagesNational Institute of Technology CalicutraghuramaNo ratings yet

- Employee Investment Declaration Form For The Financial Year 2019-2020Document2 pagesEmployee Investment Declaration Form For The Financial Year 2019-2020Hinglaj SinghNo ratings yet

- IT Declaration 2011-12Document2 pagesIT Declaration 2011-12Vijaya Saradhi PeddiNo ratings yet

- IT AmendmentDocument13 pagesIT AmendmentMs Geethanjali MNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Old Exam AEDocument12 pagesOld Exam AEaaaaaNo ratings yet

- 00 - King Lear AnalysisDocument11 pages00 - King Lear AnalysisViki VankaNo ratings yet

- Gas Spot Market: How Does It Work and Who Are The Players?Document16 pagesGas Spot Market: How Does It Work and Who Are The Players?lupoderi100% (1)

- 4 - Liber NVDocument8 pages4 - Liber NVIsmael I. VelazquezNo ratings yet

- Cblo DRDocument28 pagesCblo DRPrerna BhardwajNo ratings yet

- Legal Terminology - Ders 1Document27 pagesLegal Terminology - Ders 1simberkis12No ratings yet

- (Chris Horrocks, Zoran Jevtic) Introducing Foucaul PDFDocument91 pages(Chris Horrocks, Zoran Jevtic) Introducing Foucaul PDFJeronimo Amaral de CarvalhoNo ratings yet

- Aff - Human Germline Genetic Engineering - MSDI 2022Document97 pagesAff - Human Germline Genetic Engineering - MSDI 2022HyperrealHNo ratings yet

- T. Daryaee and Kh. Rezakhani The SasaniaDocument51 pagesT. Daryaee and Kh. Rezakhani The Sasaniaejc1717No ratings yet

- Mulund College of CommerceDocument20 pagesMulund College of CommerceAashay DagdeNo ratings yet

- PDFDocument6 pagesPDFHarshada AhirraoNo ratings yet

- Week 13 15Document14 pagesWeek 13 15Marjorie QuitorNo ratings yet

- Pancard Clubs NCLT OrderDocument31 pagesPancard Clubs NCLT OrderMr. AbhirBhandary NMAMIT ISNo ratings yet

- CRIMINAL SOCIOLOGY - ETHICS AND HUMAN RELATIONS 200 Item - KeyDocument7 pagesCRIMINAL SOCIOLOGY - ETHICS AND HUMAN RELATIONS 200 Item - Keymark patalinghugNo ratings yet

- Luke Gromen Slide Deck For Parts 3 and 4Document47 pagesLuke Gromen Slide Deck For Parts 3 and 4riazuddin1985No ratings yet

- Salazar vs. Achacoso, 183 SCRA 145Document7 pagesSalazar vs. Achacoso, 183 SCRA 145Inez PadsNo ratings yet

- QATAR: Major ChangesDocument11 pagesQATAR: Major ChangesVivekanandNo ratings yet

- Philisophy of EducationDocument35 pagesPhilisophy of EducationHilux23100% (1)

- EnglishFile4e Upp-Int TG PCM Vocab 3ADocument1 pageEnglishFile4e Upp-Int TG PCM Vocab 3AღDaff ღNo ratings yet

- Personal Brand PaperDocument9 pagesPersonal Brand PaperAntonio BonansingaNo ratings yet

- Week 1: BBDM3404 Case StudyDocument15 pagesWeek 1: BBDM3404 Case StudyWEN RONG TEOHNo ratings yet

- CC Unit 3, Replies To Enquiries - To StsDocument21 pagesCC Unit 3, Replies To Enquiries - To StsNhật LinhNo ratings yet

- GLOBAL PRACTICE OF ARCHITECTURE The Impacts of Globalization of The Architectural PracticeDocument1 pageGLOBAL PRACTICE OF ARCHITECTURE The Impacts of Globalization of The Architectural PracticeMark Russell DimayugaNo ratings yet

- Market StructureDocument65 pagesMarket StructureDhanya Das100% (1)

- FORD Final SlideDocument12 pagesFORD Final SlideJubayed Hossain ChowdhuryNo ratings yet

- How To Be Courageous & BraveDocument1 pageHow To Be Courageous & BraveElias FungNo ratings yet

- CA 110 Owners ManualDocument10 pagesCA 110 Owners ManualJury FigueroaNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Trainors Training On Parent Effectiveness SeminarDocument49 pagesTrainors Training On Parent Effectiveness SeminarBigg Clicks96% (50)

- Investment Declaration Form - 2022-2023Document3 pagesInvestment Declaration Form - 2022-2023Bharathi KNo ratings yet

- F.3 CD Qualico Dev RZDocument96 pagesF.3 CD Qualico Dev RZMiranda GathercoleNo ratings yet

- Gold Experience c1 2nd Edition End of Year Test Main Test ADocument12 pagesGold Experience c1 2nd Edition End of Year Test Main Test APili Hidalgo MoyaNo ratings yet

- A Project Report On Direct TaxDocument53 pagesA Project Report On Direct Taxrani26oct84% (44)

- IT Declaration Form 2020-21Document1 pageIT Declaration Form 2020-21Akshay AcchuNo ratings yet

- The ABC Foundation: Investment Declaration Form For Tax Saving For Financial Year 2018-2019 The Akshaya Patra FoundationDocument1 pageThe ABC Foundation: Investment Declaration Form For Tax Saving For Financial Year 2018-2019 The Akshaya Patra FoundationLantNo ratings yet

- Declaration Form 12BB 2022 23Document4 pagesDeclaration Form 12BB 2022 23S S PradheepanNo ratings yet

- HRA, Chapter VI A - 80CCD, 80C, 80D, Other IncomeDocument9 pagesHRA, Chapter VI A - 80CCD, 80C, 80D, Other Incomefaiyaz432No ratings yet

- Tax Declaration Form 2021 22Document4 pagesTax Declaration Form 2021 22Kasiviswanathan ChinnathambiNo ratings yet

- Income Tax Declaration Form FY 22 23 AY 23 24Document2 pagesIncome Tax Declaration Form FY 22 23 AY 23 24kishoreNo ratings yet

- OLD Income Tax Performa-2021-22Document13 pagesOLD Income Tax Performa-2021-22Research AccountNo ratings yet

- Frequently Asked Questions (Faqs) Tax Deduction at Source On BOB Staff Pension PaymentsDocument4 pagesFrequently Asked Questions (Faqs) Tax Deduction at Source On BOB Staff Pension PaymentsMayur khichiNo ratings yet

- Investment Declaration Form - 1314 - IshitaDocument5 pagesInvestment Declaration Form - 1314 - IshitaIshita AwasthiNo ratings yet

- Employee Tax Declaration - AY 2019-20Document4 pagesEmployee Tax Declaration - AY 2019-20mathuNo ratings yet

- Investment PlanDocument1 pageInvestment PlanNitin AgarwalNo ratings yet

- Employees Proof Submission Form (EPSF) - 2010-11Document1 pageEmployees Proof Submission Form (EPSF) - 2010-11amararenaNo ratings yet

- Portal Investment Proof Verification Guidelines 2022 23Document11 pagesPortal Investment Proof Verification Guidelines 2022 23yfiamataimNo ratings yet

- Declaration Form (22-23)Document4 pagesDeclaration Form (22-23)vasavi kNo ratings yet

- IT Declaration Form 2011-2012Document1 pageIT Declaration Form 2011-2012Shishir RoyNo ratings yet

- BUFIN ITDeclarationFormDocument2 pagesBUFIN ITDeclarationFormdpfsopfopsfhopNo ratings yet

- IT Declaration Form April 2023 To March 2024.Document3 pagesIT Declaration Form April 2023 To March 2024.partha.uneesolutionsNo ratings yet

- O Sec 56 (2) I.E. IOS Clause V, Vi, VII (A & B), Ix, X, XiDocument7 pagesO Sec 56 (2) I.E. IOS Clause V, Vi, VII (A & B), Ix, X, XiRadhika SarawagiNo ratings yet

- Investment Declaration Form (Hemarus)Document4 pagesInvestment Declaration Form (Hemarus)Shashi NaganurNo ratings yet

- Deductions On Section 80CDocument12 pagesDeductions On Section 80CViraja GuruNo ratings yet

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Document5 pages1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiNo ratings yet

- Investment GuidelineDocument3 pagesInvestment GuidelineBuchi YarraNo ratings yet

- Income Tax Declaration Form - F.Y. 2020-21Document8 pagesIncome Tax Declaration Form - F.Y. 2020-21LTelford RudraprayagNo ratings yet

- Investment Declaration Form - 2021-22Document3 pagesInvestment Declaration Form - 2021-22rajamani balajiNo ratings yet

- Investment Declaration Form For The Financial Year 2014 - 15Document7 pagesInvestment Declaration Form For The Financial Year 2014 - 15devanyaNo ratings yet

- Indian Institute of Technology Madras: CircularDocument5 pagesIndian Institute of Technology Madras: CircularAravinthram R am18m002No ratings yet

- Provident FundDocument5 pagesProvident FundG MadhuriNo ratings yet

- Declaration For Proposed Tax Saving Investment and Expenditures For F.Y. 2011 12Document11 pagesDeclaration For Proposed Tax Saving Investment and Expenditures For F.Y. 2011 12nikhiljain17No ratings yet

- Income Decleration PDFDocument2 pagesIncome Decleration PDFvijay dabhiNo ratings yet

- Investment Declaration Form F.Y 2023-24Document4 pagesInvestment Declaration Form F.Y 2023-24Aditi Suryavanshi100% (2)

- 1 .Income Tax On Salaries - (01.06.2015)Document57 pages1 .Income Tax On Salaries - (01.06.2015)yvNo ratings yet

- Tax Proof Submission FY 2021-22Document10 pagesTax Proof Submission FY 2021-22cutieedivyaNo ratings yet

- IT Declaration Form 2019-20Document1 pageIT Declaration Form 2019-20KarunaNo ratings yet

- IT Declaration Form FY 2018-19Document3 pagesIT Declaration Form FY 2018-19sgshekar3050% (2)

- Individual-Txation-FY-2018-19-with - JJDocument64 pagesIndividual-Txation-FY-2018-19-with - JJCOMPLETE ACADEMYNo ratings yet

- For Tds On SalaryDocument40 pagesFor Tds On SalarykshitijsaxenaNo ratings yet

- DownloadDocument6 pagesDownloadpankhewalegNo ratings yet

- Arrina Education Services Pvt. LTD.: Investment Declaration Form (FY 2012-2013)Document2 pagesArrina Education Services Pvt. LTD.: Investment Declaration Form (FY 2012-2013)JITEN2050No ratings yet

- Salaries PresentationDocument21 pagesSalaries PresentationDipika PandaNo ratings yet

- Tax Savings Declarations GuidelinesDocument13 pagesTax Savings Declarations GuidelinesAditya DasNo ratings yet

- DeductionsDocument11 pagesDeductionsguest1No ratings yet

- FAQ On Budget FY 2020-21Document9 pagesFAQ On Budget FY 2020-21GUNANo ratings yet

- Direct TaxesDocument9 pagesDirect TaxesPuneet JindalNo ratings yet

- Income Tax NitDocument6 pagesIncome Tax NitrensisamNo ratings yet

- Deductions From Gross Total Income: Deductions Allowable Under Various Sections of Chapter VIA of Income Tax ActDocument8 pagesDeductions From Gross Total Income: Deductions Allowable Under Various Sections of Chapter VIA of Income Tax ActalisagasaNo ratings yet

- Employee Tax Declaration - AY 2019-20Document1 pageEmployee Tax Declaration - AY 2019-20mathuNo ratings yet

- PPP Loan Forgiveness Application (Revised 6.16.2020)Document5 pagesPPP Loan Forgiveness Application (Revised 6.16.2020)LaurenNo ratings yet

- Guidelines For Income Tax DeclarationDocument9 pagesGuidelines For Income Tax Declarationapoorva1801No ratings yet

- Tax Rebate Claim Form-2019Document2 pagesTax Rebate Claim Form-2019Muhammad Hanif SuchwaniNo ratings yet

- Investment Declaration Form11-12Document2 pagesInvestment Declaration Form11-12girijasankar11No ratings yet

- Income Tax Ready Reckoner 2011-12Document28 pagesIncome Tax Ready Reckoner 2011-12kpksscribdNo ratings yet

- Notes To Investment Proof SubmissionDocument10 pagesNotes To Investment Proof SubmissionVinayak DhotreNo ratings yet

- National Institute of Technology CalicutDocument7 pagesNational Institute of Technology CalicutraghuramaNo ratings yet

- Employee Investment Declaration Form For The Financial Year 2019-2020Document2 pagesEmployee Investment Declaration Form For The Financial Year 2019-2020Hinglaj SinghNo ratings yet

- IT Declaration 2011-12Document2 pagesIT Declaration 2011-12Vijaya Saradhi PeddiNo ratings yet

- IT AmendmentDocument13 pagesIT AmendmentMs Geethanjali MNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Old Exam AEDocument12 pagesOld Exam AEaaaaaNo ratings yet

- 00 - King Lear AnalysisDocument11 pages00 - King Lear AnalysisViki VankaNo ratings yet

- Gas Spot Market: How Does It Work and Who Are The Players?Document16 pagesGas Spot Market: How Does It Work and Who Are The Players?lupoderi100% (1)

- 4 - Liber NVDocument8 pages4 - Liber NVIsmael I. VelazquezNo ratings yet

- Cblo DRDocument28 pagesCblo DRPrerna BhardwajNo ratings yet

- Legal Terminology - Ders 1Document27 pagesLegal Terminology - Ders 1simberkis12No ratings yet

- (Chris Horrocks, Zoran Jevtic) Introducing Foucaul PDFDocument91 pages(Chris Horrocks, Zoran Jevtic) Introducing Foucaul PDFJeronimo Amaral de CarvalhoNo ratings yet

- Aff - Human Germline Genetic Engineering - MSDI 2022Document97 pagesAff - Human Germline Genetic Engineering - MSDI 2022HyperrealHNo ratings yet

- T. Daryaee and Kh. Rezakhani The SasaniaDocument51 pagesT. Daryaee and Kh. Rezakhani The Sasaniaejc1717No ratings yet

- Mulund College of CommerceDocument20 pagesMulund College of CommerceAashay DagdeNo ratings yet

- PDFDocument6 pagesPDFHarshada AhirraoNo ratings yet

- Week 13 15Document14 pagesWeek 13 15Marjorie QuitorNo ratings yet

- Pancard Clubs NCLT OrderDocument31 pagesPancard Clubs NCLT OrderMr. AbhirBhandary NMAMIT ISNo ratings yet

- CRIMINAL SOCIOLOGY - ETHICS AND HUMAN RELATIONS 200 Item - KeyDocument7 pagesCRIMINAL SOCIOLOGY - ETHICS AND HUMAN RELATIONS 200 Item - Keymark patalinghugNo ratings yet

- Luke Gromen Slide Deck For Parts 3 and 4Document47 pagesLuke Gromen Slide Deck For Parts 3 and 4riazuddin1985No ratings yet

- Salazar vs. Achacoso, 183 SCRA 145Document7 pagesSalazar vs. Achacoso, 183 SCRA 145Inez PadsNo ratings yet

- QATAR: Major ChangesDocument11 pagesQATAR: Major ChangesVivekanandNo ratings yet

- Philisophy of EducationDocument35 pagesPhilisophy of EducationHilux23100% (1)

- EnglishFile4e Upp-Int TG PCM Vocab 3ADocument1 pageEnglishFile4e Upp-Int TG PCM Vocab 3AღDaff ღNo ratings yet

- Personal Brand PaperDocument9 pagesPersonal Brand PaperAntonio BonansingaNo ratings yet

- Week 1: BBDM3404 Case StudyDocument15 pagesWeek 1: BBDM3404 Case StudyWEN RONG TEOHNo ratings yet

- CC Unit 3, Replies To Enquiries - To StsDocument21 pagesCC Unit 3, Replies To Enquiries - To StsNhật LinhNo ratings yet

- GLOBAL PRACTICE OF ARCHITECTURE The Impacts of Globalization of The Architectural PracticeDocument1 pageGLOBAL PRACTICE OF ARCHITECTURE The Impacts of Globalization of The Architectural PracticeMark Russell DimayugaNo ratings yet

- Market StructureDocument65 pagesMarket StructureDhanya Das100% (1)

- FORD Final SlideDocument12 pagesFORD Final SlideJubayed Hossain ChowdhuryNo ratings yet

- How To Be Courageous & BraveDocument1 pageHow To Be Courageous & BraveElias FungNo ratings yet

- CA 110 Owners ManualDocument10 pagesCA 110 Owners ManualJury FigueroaNo ratings yet