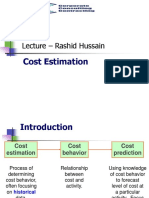

AMD2019s2 Topic 8

AMD2019s2 Topic 8

You might also like

- Job Order Costing: Learning ObjectivesDocument50 pagesJob Order Costing: Learning ObjectivesTNo ratings yet

- Acc311 Excel Week3 Project 1Document3 pagesAcc311 Excel Week3 Project 1Lilian LNo ratings yet

- Sample Solution Manual For Management Accounting 2nd Edition by Leslie G. EldenburgDocument40 pagesSample Solution Manual For Management Accounting 2nd Edition by Leslie G. EldenburgAshwin Thiyagarajan100% (1)

- Chapter 6 Solutions Comm 305Document31 pagesChapter 6 Solutions Comm 305mike0% (5)

- 3.1 Definition and Application of Cost Behaviour ConceptDocument6 pages3.1 Definition and Application of Cost Behaviour ConceptPrince PierreNo ratings yet

- Cost Concepts and Classifications: Fixed Vs Direct Vs Variable Indirect Functional Vs BehavioralDocument20 pagesCost Concepts and Classifications: Fixed Vs Direct Vs Variable Indirect Functional Vs BehavioralNur Hidayah Yusof LatifNo ratings yet

- Cost Concept and SegregationDocument1 pageCost Concept and SegregationsatyaNo ratings yet

- ACC202 SU6 Jan2020Document31 pagesACC202 SU6 Jan2020hashtagjxNo ratings yet

- Cost Classification Based On Cost BehaviorDocument38 pagesCost Classification Based On Cost Behaviorshriya2413No ratings yet

- Mixed CostDocument4 pagesMixed CostPeter WagdyNo ratings yet

- Cost BehaviorDocument29 pagesCost BehaviorLucy UnNo ratings yet

- Introduction To Cost ManagementDocument31 pagesIntroduction To Cost ManagementVINCENT GAYRAMONNo ratings yet

- COST ESTIMATION A Class Lecture by Rashid Hussain 1657763473Document55 pagesCOST ESTIMATION A Class Lecture by Rashid Hussain 1657763473HiteshSandhalNo ratings yet

- Chap 022Document42 pagesChap 022Mohamed AlyNo ratings yet

- CMA Part 2 Financial Decision Making: Study Unit 8 - CVP Analysis and Marginal AnalysisDocument85 pagesCMA Part 2 Financial Decision Making: Study Unit 8 - CVP Analysis and Marginal AnalysisNEERAJ GUPTANo ratings yet

- Managerial Accounting: Dr. Zubair AhmadDocument24 pagesManagerial Accounting: Dr. Zubair AhmadCaylessNo ratings yet

- (Semi-Variable) Total Variable) Cost As Production Unit Fixed Costs) As Production IncreaseDocument4 pages(Semi-Variable) Total Variable) Cost As Production Unit Fixed Costs) As Production IncreaseClint AbenojaNo ratings yet

- 02 Cost Behavior With Regression AnalysisDocument6 pages02 Cost Behavior With Regression Analysisrandomlungs121223No ratings yet

- MAC Summary of FormulasDocument25 pagesMAC Summary of FormulasRuNo ratings yet

- Cost AccountingDocument3 pagesCost AccountingABDUL RAHIM G. ACOONNo ratings yet

- Chapter 18 Slides MSREDocument43 pagesChapter 18 Slides MSREMichael CorreaNo ratings yet

- Chapter 3 - Cost Volume and Cost Volume Profit AnalysisDocument65 pagesChapter 3 - Cost Volume and Cost Volume Profit AnalysisGabai AsaiNo ratings yet

- MasterbudgetDocument154 pagesMasterbudgetrochielanciolaNo ratings yet

- Overhead CostingDocument15 pagesOverhead CostingMrinmoy SahaNo ratings yet

- Managerial Accounting Chapter 5 With SolutionsDocument43 pagesManagerial Accounting Chapter 5 With SolutionsRay LiuNo ratings yet

- ACCT 2102: Principles of Management AccountingDocument55 pagesACCT 2102: Principles of Management AccountingSihua ChengNo ratings yet

- Acct 202 Ch5Document39 pagesAcct 202 Ch5Hải Anh LươngNo ratings yet

- Prepared by DR - Hassan Sweillam University of 6 of October, EgyptDocument25 pagesPrepared by DR - Hassan Sweillam University of 6 of October, EgyptjgjghNo ratings yet

- MGMT Science Notes 03 CVP AnalysisDocument8 pagesMGMT Science Notes 03 CVP AnalysismichelleNo ratings yet

- Mas 42b Cost Behavior With Regression AnalysisDocument7 pagesMas 42b Cost Behavior With Regression AnalysisMary Joyce SiyNo ratings yet

- CMA CH 2 - CVP Analysis March 2019-2Document100 pagesCMA CH 2 - CVP Analysis March 2019-2Henok FikaduNo ratings yet

- MAS 02 Cost Behavior With Regression AnalysisDocument6 pagesMAS 02 Cost Behavior With Regression AnalysisJericho G. BariringNo ratings yet

- SCM Lesson 2 PDFDocument4 pagesSCM Lesson 2 PDFMainit, Shiela Mae, S.No ratings yet

- Session 10+11 - Cost Volume Profit RelationshipDocument44 pagesSession 10+11 - Cost Volume Profit Relationshiphieucaiminh155No ratings yet

- 2 - Cost Concepts and BehaviorsDocument4 pages2 - Cost Concepts and BehaviorsKaryl FailmaNo ratings yet

- Slide Chapter 2Document65 pagesSlide Chapter 2daoviethung29No ratings yet

- im_ch03Document7 pagesim_ch03Lena RingoNo ratings yet

- CH 22Document79 pagesCH 22Hasan AzmiNo ratings yet

- Chapter 1 - MAS IntroductionDocument9 pagesChapter 1 - MAS Introductionchelsea kayle licomes fuentesNo ratings yet

- Cost Accounting Ch03 1Document86 pagesCost Accounting Ch03 1Cali100% (1)

- Ammar ch2Document14 pagesAmmar ch2Dania Al-ȜbadiNo ratings yet

- 03 Cost BehaviourDocument24 pages03 Cost BehaviourArindam DasNo ratings yet

- MAS-01 Cost Behavior AnalysisDocument6 pagesMAS-01 Cost Behavior AnalysisPaupauNo ratings yet

- Managerial Accounting - Chapter 05Document11 pagesManagerial Accounting - Chapter 05jingsuke88% (8)

- Session 3 Cost Behavior ACCT2121Document28 pagesSession 3 Cost Behavior ACCT2121chloe lamxdNo ratings yet

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument83 pagesPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegeH.R. RobinNo ratings yet

- High Low and Least Square PDFDocument4 pagesHigh Low and Least Square PDFmarioNo ratings yet

- Presentation Chapter 6 - CompletedDocument49 pagesPresentation Chapter 6 - CompletedStephanie Ayu PraditaNo ratings yet

- MAS-02 Cost Terms, Concepts and BehaviorDocument4 pagesMAS-02 Cost Terms, Concepts and BehaviorMichael BaguyoNo ratings yet

- Chapter 10 CostDocument17 pagesChapter 10 Costالمنتج عمرNo ratings yet

- Accounting For Factory OverheadDocument44 pagesAccounting For Factory OverheadAhmed hassanNo ratings yet

- Analyzing Cost-Volume-Profit IssuesDocument55 pagesAnalyzing Cost-Volume-Profit IssuesVaisal AmirNo ratings yet

- Chapter 18 Cost-Volume-ProfitDocument78 pagesChapter 18 Cost-Volume-ProfitmualajmiNo ratings yet

- Lecture 7 Theory of CostDocument32 pagesLecture 7 Theory of CostMd. Didarul AlamNo ratings yet

- Act 202 Chapter 6Document40 pagesAct 202 Chapter 6Shaon KhanNo ratings yet

- ACT202 - Chapter 6Document38 pagesACT202 - Chapter 6arafkhan1623No ratings yet

- Chapter Outline: Learning ObjectivesDocument76 pagesChapter Outline: Learning Objectiveskarla beatriceNo ratings yet

- Reviewer Mas 4Document82 pagesReviewer Mas 4Angelina SecretarioNo ratings yet

- CH 22Document93 pagesCH 22Hanifah OktarizaNo ratings yet

- Distinguish Between Variable and Fixed CostsDocument7 pagesDistinguish Between Variable and Fixed CostsBianca PuglissiNo ratings yet

- MAS-02: Cost Behavior Regression Analysis: - T R S ADocument124 pagesMAS-02: Cost Behavior Regression Analysis: - T R S ADestiny LazarteNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- AMD Topic 5Document30 pagesAMD Topic 5Anjeena ShresthaNo ratings yet

- AMD2019s2 Topic 6Document28 pagesAMD2019s2 Topic 6Anjeena ShresthaNo ratings yet

- Aggregate Demand: Macroeconomic Variables: Demanded! - AD Shifts To The RightDocument7 pagesAggregate Demand: Macroeconomic Variables: Demanded! - AD Shifts To The RightAnjeena ShresthaNo ratings yet

- Name: Shristi Subedi Student Id: 3271397Document4 pagesName: Shristi Subedi Student Id: 3271397Anjeena ShresthaNo ratings yet

- Sampling Method (RM&RP)Document15 pagesSampling Method (RM&RP)Anjeena ShresthaNo ratings yet

- 501 Assessment Advance DiplomaDocument7 pages501 Assessment Advance DiplomaAnjeena ShresthaNo ratings yet

- Student Overall Assessment Record SheetDocument2 pagesStudent Overall Assessment Record SheetAnjeena ShresthaNo ratings yet

- Assignment 3 - Cover Sheet Managing, Leading, Organising &stewardship - 21937Document3 pagesAssignment 3 - Cover Sheet Managing, Leading, Organising &stewardship - 21937Anjeena ShresthaNo ratings yet

- 501 Assessment Advance DiplomaDocument7 pages501 Assessment Advance DiplomaAnjeena ShresthaNo ratings yet

- PR CHP 5 - Ex 5-1 - Kelompok 1Document2 pagesPR CHP 5 - Ex 5-1 - Kelompok 1Lucky esteritaNo ratings yet

- Activity Based CostingDocument6 pagesActivity Based CostingmisgiegirmaNo ratings yet

- Cost Accounting A Managerial Emphasis Canadian 8th Edition Horngren Solutions Manual instant download all chapterDocument75 pagesCost Accounting A Managerial Emphasis Canadian 8th Edition Horngren Solutions Manual instant download all chaptertunkuebbing7100% (2)

- Program/Course Bcom (A&F) Class Tybcom (A&F) Semester VI Subject Financial Accounting-Vii Subject Code 85601 Exam Date 05.10.2020Document28 pagesProgram/Course Bcom (A&F) Class Tybcom (A&F) Semester VI Subject Financial Accounting-Vii Subject Code 85601 Exam Date 05.10.2020hareshNo ratings yet

- References: WorksheetDocument4 pagesReferences: Worksheetsuruth242No ratings yet

- Job Order Costing: Cost Accounting Project 1Document19 pagesJob Order Costing: Cost Accounting Project 1imranumerNo ratings yet

- Contoh Soal Problem 8-32Document2 pagesContoh Soal Problem 8-32bella0% (1)

- Aeco2 MidtermDocument5 pagesAeco2 MidtermvsplanciaNo ratings yet

- Chapter Five Lecture NoteDocument15 pagesChapter Five Lecture NoteAbrha636No ratings yet

- Percentage Increase and DecreaseDocument3 pagesPercentage Increase and DecreaseLai Kee KongNo ratings yet

- Chapter No.04 - Process Costing and Hybrid Product-Costing SystemsDocument39 pagesChapter No.04 - Process Costing and Hybrid Product-Costing SystemsWali NoorzadNo ratings yet

- Individual Assignment 2 Managerial AccountingDocument3 pagesIndividual Assignment 2 Managerial AccountingCodyxanssNo ratings yet

- Marginal Vs Absorption CostingDocument13 pagesMarginal Vs Absorption CostingRugeyye RashidNo ratings yet

- Job and Batch CostingDocument2 pagesJob and Batch CostingAbu bakar JunidNo ratings yet

- Prof. Sam.: RegardsDocument7 pagesProf. Sam.: RegardsKoshy ThankachenNo ratings yet

- 405 Cost Accounting SY BCOMDocument8 pages405 Cost Accounting SY BCOMTejas DasnurkarNo ratings yet

- FMID Mid Mock Spring 22Document2 pagesFMID Mid Mock Spring 22Umer FarooqNo ratings yet

- CHAPTER 6 ExercisesDocument15 pagesCHAPTER 6 ExercisesMoshir Aly100% (1)

- Prelim ExamFDocument4 pagesPrelim ExamFMa Jodelyn RosinNo ratings yet

- Absorption and Marginal Costing Worked ExamplesDocument5 pagesAbsorption and Marginal Costing Worked ExamplesSUHRIT BISWASNo ratings yet

- J54 S4HANA2022 BPD en Overhead Cost AccountingDocument51 pagesJ54 S4HANA2022 BPD en Overhead Cost AccountingMickael QUESNOTNo ratings yet

- Costassign JoDocument4 pagesCostassign Jokishi8mempinNo ratings yet

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument38 pagesAuditing and Assurance Services: Seventeenth Edition, Global Edition賴宥禎No ratings yet

- Café Coffee Day: Project Report ONDocument32 pagesCafé Coffee Day: Project Report ONaditig22No ratings yet

- Quiz Finals CostDocument3 pagesQuiz Finals CostALLYSON BURAGANo ratings yet

- Acc502 AssignmrntDocument3 pagesAcc502 Assignmrntsuleman yousafzaiNo ratings yet

- ACC228 - WEEK 3&4 - ULObDocument16 pagesACC228 - WEEK 3&4 - ULObDaniel RosalesNo ratings yet

Download as pdf or txt

You might also like

- Job Order Costing: Learning ObjectivesDocument50 pagesJob Order Costing: Learning ObjectivesTNo ratings yet

- Acc311 Excel Week3 Project 1Document3 pagesAcc311 Excel Week3 Project 1Lilian LNo ratings yet

- Sample Solution Manual For Management Accounting 2nd Edition by Leslie G. EldenburgDocument40 pagesSample Solution Manual For Management Accounting 2nd Edition by Leslie G. EldenburgAshwin Thiyagarajan100% (1)

- Chapter 6 Solutions Comm 305Document31 pagesChapter 6 Solutions Comm 305mike0% (5)

- 3.1 Definition and Application of Cost Behaviour ConceptDocument6 pages3.1 Definition and Application of Cost Behaviour ConceptPrince PierreNo ratings yet

- Cost Concepts and Classifications: Fixed Vs Direct Vs Variable Indirect Functional Vs BehavioralDocument20 pagesCost Concepts and Classifications: Fixed Vs Direct Vs Variable Indirect Functional Vs BehavioralNur Hidayah Yusof LatifNo ratings yet

- Cost Concept and SegregationDocument1 pageCost Concept and SegregationsatyaNo ratings yet

- ACC202 SU6 Jan2020Document31 pagesACC202 SU6 Jan2020hashtagjxNo ratings yet

- Cost Classification Based On Cost BehaviorDocument38 pagesCost Classification Based On Cost Behaviorshriya2413No ratings yet

- Mixed CostDocument4 pagesMixed CostPeter WagdyNo ratings yet

- Cost BehaviorDocument29 pagesCost BehaviorLucy UnNo ratings yet

- Introduction To Cost ManagementDocument31 pagesIntroduction To Cost ManagementVINCENT GAYRAMONNo ratings yet

- COST ESTIMATION A Class Lecture by Rashid Hussain 1657763473Document55 pagesCOST ESTIMATION A Class Lecture by Rashid Hussain 1657763473HiteshSandhalNo ratings yet

- Chap 022Document42 pagesChap 022Mohamed AlyNo ratings yet

- CMA Part 2 Financial Decision Making: Study Unit 8 - CVP Analysis and Marginal AnalysisDocument85 pagesCMA Part 2 Financial Decision Making: Study Unit 8 - CVP Analysis and Marginal AnalysisNEERAJ GUPTANo ratings yet

- Managerial Accounting: Dr. Zubair AhmadDocument24 pagesManagerial Accounting: Dr. Zubair AhmadCaylessNo ratings yet

- (Semi-Variable) Total Variable) Cost As Production Unit Fixed Costs) As Production IncreaseDocument4 pages(Semi-Variable) Total Variable) Cost As Production Unit Fixed Costs) As Production IncreaseClint AbenojaNo ratings yet

- 02 Cost Behavior With Regression AnalysisDocument6 pages02 Cost Behavior With Regression Analysisrandomlungs121223No ratings yet

- MAC Summary of FormulasDocument25 pagesMAC Summary of FormulasRuNo ratings yet

- Cost AccountingDocument3 pagesCost AccountingABDUL RAHIM G. ACOONNo ratings yet

- Chapter 18 Slides MSREDocument43 pagesChapter 18 Slides MSREMichael CorreaNo ratings yet

- Chapter 3 - Cost Volume and Cost Volume Profit AnalysisDocument65 pagesChapter 3 - Cost Volume and Cost Volume Profit AnalysisGabai AsaiNo ratings yet

- MasterbudgetDocument154 pagesMasterbudgetrochielanciolaNo ratings yet

- Overhead CostingDocument15 pagesOverhead CostingMrinmoy SahaNo ratings yet

- Managerial Accounting Chapter 5 With SolutionsDocument43 pagesManagerial Accounting Chapter 5 With SolutionsRay LiuNo ratings yet

- ACCT 2102: Principles of Management AccountingDocument55 pagesACCT 2102: Principles of Management AccountingSihua ChengNo ratings yet

- Acct 202 Ch5Document39 pagesAcct 202 Ch5Hải Anh LươngNo ratings yet

- Prepared by DR - Hassan Sweillam University of 6 of October, EgyptDocument25 pagesPrepared by DR - Hassan Sweillam University of 6 of October, EgyptjgjghNo ratings yet

- MGMT Science Notes 03 CVP AnalysisDocument8 pagesMGMT Science Notes 03 CVP AnalysismichelleNo ratings yet

- Mas 42b Cost Behavior With Regression AnalysisDocument7 pagesMas 42b Cost Behavior With Regression AnalysisMary Joyce SiyNo ratings yet

- CMA CH 2 - CVP Analysis March 2019-2Document100 pagesCMA CH 2 - CVP Analysis March 2019-2Henok FikaduNo ratings yet

- MAS 02 Cost Behavior With Regression AnalysisDocument6 pagesMAS 02 Cost Behavior With Regression AnalysisJericho G. BariringNo ratings yet

- SCM Lesson 2 PDFDocument4 pagesSCM Lesson 2 PDFMainit, Shiela Mae, S.No ratings yet

- Session 10+11 - Cost Volume Profit RelationshipDocument44 pagesSession 10+11 - Cost Volume Profit Relationshiphieucaiminh155No ratings yet

- 2 - Cost Concepts and BehaviorsDocument4 pages2 - Cost Concepts and BehaviorsKaryl FailmaNo ratings yet

- Slide Chapter 2Document65 pagesSlide Chapter 2daoviethung29No ratings yet

- im_ch03Document7 pagesim_ch03Lena RingoNo ratings yet

- CH 22Document79 pagesCH 22Hasan AzmiNo ratings yet

- Chapter 1 - MAS IntroductionDocument9 pagesChapter 1 - MAS Introductionchelsea kayle licomes fuentesNo ratings yet

- Cost Accounting Ch03 1Document86 pagesCost Accounting Ch03 1Cali100% (1)

- Ammar ch2Document14 pagesAmmar ch2Dania Al-ȜbadiNo ratings yet

- 03 Cost BehaviourDocument24 pages03 Cost BehaviourArindam DasNo ratings yet

- MAS-01 Cost Behavior AnalysisDocument6 pagesMAS-01 Cost Behavior AnalysisPaupauNo ratings yet

- Managerial Accounting - Chapter 05Document11 pagesManagerial Accounting - Chapter 05jingsuke88% (8)

- Session 3 Cost Behavior ACCT2121Document28 pagesSession 3 Cost Behavior ACCT2121chloe lamxdNo ratings yet

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument83 pagesPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegeH.R. RobinNo ratings yet

- High Low and Least Square PDFDocument4 pagesHigh Low and Least Square PDFmarioNo ratings yet

- Presentation Chapter 6 - CompletedDocument49 pagesPresentation Chapter 6 - CompletedStephanie Ayu PraditaNo ratings yet

- MAS-02 Cost Terms, Concepts and BehaviorDocument4 pagesMAS-02 Cost Terms, Concepts and BehaviorMichael BaguyoNo ratings yet

- Chapter 10 CostDocument17 pagesChapter 10 Costالمنتج عمرNo ratings yet

- Accounting For Factory OverheadDocument44 pagesAccounting For Factory OverheadAhmed hassanNo ratings yet

- Analyzing Cost-Volume-Profit IssuesDocument55 pagesAnalyzing Cost-Volume-Profit IssuesVaisal AmirNo ratings yet

- Chapter 18 Cost-Volume-ProfitDocument78 pagesChapter 18 Cost-Volume-ProfitmualajmiNo ratings yet

- Lecture 7 Theory of CostDocument32 pagesLecture 7 Theory of CostMd. Didarul AlamNo ratings yet

- Act 202 Chapter 6Document40 pagesAct 202 Chapter 6Shaon KhanNo ratings yet

- ACT202 - Chapter 6Document38 pagesACT202 - Chapter 6arafkhan1623No ratings yet

- Chapter Outline: Learning ObjectivesDocument76 pagesChapter Outline: Learning Objectiveskarla beatriceNo ratings yet

- Reviewer Mas 4Document82 pagesReviewer Mas 4Angelina SecretarioNo ratings yet

- CH 22Document93 pagesCH 22Hanifah OktarizaNo ratings yet

- Distinguish Between Variable and Fixed CostsDocument7 pagesDistinguish Between Variable and Fixed CostsBianca PuglissiNo ratings yet

- MAS-02: Cost Behavior Regression Analysis: - T R S ADocument124 pagesMAS-02: Cost Behavior Regression Analysis: - T R S ADestiny LazarteNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- AMD Topic 5Document30 pagesAMD Topic 5Anjeena ShresthaNo ratings yet

- AMD2019s2 Topic 6Document28 pagesAMD2019s2 Topic 6Anjeena ShresthaNo ratings yet

- Aggregate Demand: Macroeconomic Variables: Demanded! - AD Shifts To The RightDocument7 pagesAggregate Demand: Macroeconomic Variables: Demanded! - AD Shifts To The RightAnjeena ShresthaNo ratings yet

- Name: Shristi Subedi Student Id: 3271397Document4 pagesName: Shristi Subedi Student Id: 3271397Anjeena ShresthaNo ratings yet

- Sampling Method (RM&RP)Document15 pagesSampling Method (RM&RP)Anjeena ShresthaNo ratings yet

- 501 Assessment Advance DiplomaDocument7 pages501 Assessment Advance DiplomaAnjeena ShresthaNo ratings yet

- Student Overall Assessment Record SheetDocument2 pagesStudent Overall Assessment Record SheetAnjeena ShresthaNo ratings yet

- Assignment 3 - Cover Sheet Managing, Leading, Organising &stewardship - 21937Document3 pagesAssignment 3 - Cover Sheet Managing, Leading, Organising &stewardship - 21937Anjeena ShresthaNo ratings yet

- 501 Assessment Advance DiplomaDocument7 pages501 Assessment Advance DiplomaAnjeena ShresthaNo ratings yet

- PR CHP 5 - Ex 5-1 - Kelompok 1Document2 pagesPR CHP 5 - Ex 5-1 - Kelompok 1Lucky esteritaNo ratings yet

- Activity Based CostingDocument6 pagesActivity Based CostingmisgiegirmaNo ratings yet

- Cost Accounting A Managerial Emphasis Canadian 8th Edition Horngren Solutions Manual instant download all chapterDocument75 pagesCost Accounting A Managerial Emphasis Canadian 8th Edition Horngren Solutions Manual instant download all chaptertunkuebbing7100% (2)

- Program/Course Bcom (A&F) Class Tybcom (A&F) Semester VI Subject Financial Accounting-Vii Subject Code 85601 Exam Date 05.10.2020Document28 pagesProgram/Course Bcom (A&F) Class Tybcom (A&F) Semester VI Subject Financial Accounting-Vii Subject Code 85601 Exam Date 05.10.2020hareshNo ratings yet

- References: WorksheetDocument4 pagesReferences: Worksheetsuruth242No ratings yet

- Job Order Costing: Cost Accounting Project 1Document19 pagesJob Order Costing: Cost Accounting Project 1imranumerNo ratings yet

- Contoh Soal Problem 8-32Document2 pagesContoh Soal Problem 8-32bella0% (1)

- Aeco2 MidtermDocument5 pagesAeco2 MidtermvsplanciaNo ratings yet

- Chapter Five Lecture NoteDocument15 pagesChapter Five Lecture NoteAbrha636No ratings yet

- Percentage Increase and DecreaseDocument3 pagesPercentage Increase and DecreaseLai Kee KongNo ratings yet

- Chapter No.04 - Process Costing and Hybrid Product-Costing SystemsDocument39 pagesChapter No.04 - Process Costing and Hybrid Product-Costing SystemsWali NoorzadNo ratings yet

- Individual Assignment 2 Managerial AccountingDocument3 pagesIndividual Assignment 2 Managerial AccountingCodyxanssNo ratings yet

- Marginal Vs Absorption CostingDocument13 pagesMarginal Vs Absorption CostingRugeyye RashidNo ratings yet

- Job and Batch CostingDocument2 pagesJob and Batch CostingAbu bakar JunidNo ratings yet

- Prof. Sam.: RegardsDocument7 pagesProf. Sam.: RegardsKoshy ThankachenNo ratings yet

- 405 Cost Accounting SY BCOMDocument8 pages405 Cost Accounting SY BCOMTejas DasnurkarNo ratings yet

- FMID Mid Mock Spring 22Document2 pagesFMID Mid Mock Spring 22Umer FarooqNo ratings yet

- CHAPTER 6 ExercisesDocument15 pagesCHAPTER 6 ExercisesMoshir Aly100% (1)

- Prelim ExamFDocument4 pagesPrelim ExamFMa Jodelyn RosinNo ratings yet

- Absorption and Marginal Costing Worked ExamplesDocument5 pagesAbsorption and Marginal Costing Worked ExamplesSUHRIT BISWASNo ratings yet

- J54 S4HANA2022 BPD en Overhead Cost AccountingDocument51 pagesJ54 S4HANA2022 BPD en Overhead Cost AccountingMickael QUESNOTNo ratings yet

- Costassign JoDocument4 pagesCostassign Jokishi8mempinNo ratings yet

- Auditing and Assurance Services: Seventeenth Edition, Global EditionDocument38 pagesAuditing and Assurance Services: Seventeenth Edition, Global Edition賴宥禎No ratings yet

- Café Coffee Day: Project Report ONDocument32 pagesCafé Coffee Day: Project Report ONaditig22No ratings yet

- Quiz Finals CostDocument3 pagesQuiz Finals CostALLYSON BURAGANo ratings yet

- Acc502 AssignmrntDocument3 pagesAcc502 Assignmrntsuleman yousafzaiNo ratings yet

- ACC228 - WEEK 3&4 - ULObDocument16 pagesACC228 - WEEK 3&4 - ULObDaniel RosalesNo ratings yet