Financial Ratio Analysis of Aamra

Financial Ratio Analysis of Aamra

You might also like

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetFrom EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetRating: 4.5 out of 5 stars4.5/5 (14)

- Financial Ratio Analysis AssignmentDocument10 pagesFinancial Ratio Analysis Assignmentzain5435467% (3)

- Ratio AnalysisDocument11 pagesRatio AnalysisMadavee JinadasaNo ratings yet

- AuditingDocument30 pagesAuditingMary Rose Mendoza91% (11)

- P&G Company Financial AnalysisDocument42 pagesP&G Company Financial Analysisramki07303375% (4)

- Assignment On Financial Statement Ratio AnalysisDocument27 pagesAssignment On Financial Statement Ratio AnalysisShourav87% (23)

- Ratio Ultratech Cement FinalDocument89 pagesRatio Ultratech Cement FinalDeepti Sharma100% (3)

- FABM 2 Statement of Financial PositionDocument20 pagesFABM 2 Statement of Financial PositionVictoria Manalaysay100% (1)

- Case Studies in Finance and AccountingDocument143 pagesCase Studies in Finance and AccountingRama Krishna Yelamanchili63% (8)

- Financial Ratio AnalysisDocument29 pagesFinancial Ratio AnalysisAbubakar Danmashi82% (17)

- Analysis AssignmentDocument3 pagesAnalysis AssignmentmadyanoshieNo ratings yet

- Financial Ratio AnalysisDocument25 pagesFinancial Ratio AnalysisSimran SinghNo ratings yet

- Analysis of Financial Statement Sample Assignment SolutionDocument23 pagesAnalysis of Financial Statement Sample Assignment SolutionNaveed Saifi100% (5)

- Investment Appraisals Research Proposal 11% FinalDocument19 pagesInvestment Appraisals Research Proposal 11% FinalgishaqueNo ratings yet

- Conclusion: Statements Are The Financial Statements of A Group Presented As Those of A Single Economic EntityDocument2 pagesConclusion: Statements Are The Financial Statements of A Group Presented As Those of A Single Economic EntityJayesh Gawade100% (1)

- Financial Statement Analysis ProjectDocument15 pagesFinancial Statement Analysis ProjectAnonymous wcE2ABquENo ratings yet

- Microsoft - Apple Financial AnalysisDocument27 pagesMicrosoft - Apple Financial Analysisapi-302274400100% (1)

- Corporate Finance AssignmentDocument3 pagesCorporate Finance AssignmenttahaalkibsiNo ratings yet

- 10 Principles of Basic Financial ManagementDocument7 pages10 Principles of Basic Financial ManagementJeyavikinesh Selvakkugan100% (3)

- Mba ThesisDocument170 pagesMba ThesisMushtaq Ahmed Lodhi100% (7)

- RFQ - Development of Modern Silos at 6 Locations in 5 States of India On DBFOT Basis Under PPP ModeDocument150 pagesRFQ - Development of Modern Silos at 6 Locations in 5 States of India On DBFOT Basis Under PPP Modeakhileshver singh100% (1)

- Financial Ratio AnalysisDocument11 pagesFinancial Ratio Analysispradeep100% (5)

- Financial Ratio Analysis Final-No in TextDocument32 pagesFinancial Ratio Analysis Final-No in TextMini8912No ratings yet

- Financial Ratio AnalysisDocument67 pagesFinancial Ratio Analysisrxrohit_23100% (2)

- Financial Ratio AnalysisDocument53 pagesFinancial Ratio AnalysisLaurentia Nurak100% (5)

- Project On Ratio AnalysisDocument57 pagesProject On Ratio Analysisc517880% (5)

- Financial Ratios 2Document7 pagesFinancial Ratios 2Mohammed UsmanNo ratings yet

- Financial Ratio AnalysisDocument8 pagesFinancial Ratio AnalysisNeil Nadua0% (1)

- Analisis RatioDocument5 pagesAnalisis RatioKata AssalamualaikumNo ratings yet

- Ratio AnalysisDocument96 pagesRatio AnalysisPUTERI NUR SYAHIRA SYAZWANI100% (3)

- Financial Analysis ReportDocument51 pagesFinancial Analysis Reportpinkeshparvani50% (2)

- Ratio AnalysisDocument114 pagesRatio AnalysisMehul Jain92% (12)

- Financial Analysis Automobile IndustryDocument38 pagesFinancial Analysis Automobile Industryali iqbalNo ratings yet

- Interpretation of Financial StatementsDocument11 pagesInterpretation of Financial StatementsMaverick CardsNo ratings yet

- MBA Project On Financial RatiosDocument67 pagesMBA Project On Financial Ratioskamdica86% (21)

- Limitation of Ratio AnalysisDocument5 pagesLimitation of Ratio AnalysisMir Wajahat AliNo ratings yet

- Equity Research Report Writing ProcessDocument6 pagesEquity Research Report Writing ProcessQuofi SeliNo ratings yet

- Report On Financial Statement of InfosysDocument22 pagesReport On Financial Statement of InfosysSoham Khanna100% (2)

- ACC102 Financial Statement AnalysisDocument18 pagesACC102 Financial Statement Analysiscraigkrupski12No ratings yet

- Financial Ratios and Their InterpretationDocument10 pagesFinancial Ratios and Their InterpretationPriyanka_Bhans_7838100% (4)

- Financial Statement AnalysisDocument88 pagesFinancial Statement Analysisrohila200195% (38)

- Financial AnalysisDocument107 pagesFinancial AnalysisRamachandran Mahendran100% (4)

- Cash Flow Analysis and StatementDocument127 pagesCash Flow Analysis and Statementsnhk679546100% (6)

- Fundamental Analysis of IT SectorDocument12 pagesFundamental Analysis of IT SectorManasi Kalgutkar100% (2)

- Financial Performance Analysis Mba Project Report DownloadDocument3 pagesFinancial Performance Analysis Mba Project Report DownloadAhamed Ibrahim100% (3)

- Comparative Analysis of Financial Statements 1Document44 pagesComparative Analysis of Financial Statements 1The onion factory100% (1)

- Fundamental Analysis-BHEL - Equity Research ReportDocument5 pagesFundamental Analysis-BHEL - Equity Research ReportChrisNo ratings yet

- Final Report Ratio Analysis Kohinoor Textile Mill PVT: Presented byDocument20 pagesFinal Report Ratio Analysis Kohinoor Textile Mill PVT: Presented byAmoOnBaLushiNo ratings yet

- An Analysis of Financial PerformanceDocument76 pagesAn Analysis of Financial PerformanceShah Kamal100% (8)

- Five Year Financial Statement Analysis of Shell and PSODocument87 pagesFive Year Financial Statement Analysis of Shell and PSOOmer Piracha83% (6)

- Question No: 1 (Marks: 1) - Please Choose OneDocument15 pagesQuestion No: 1 (Marks: 1) - Please Choose OneHassanalizaidi100% (1)

- Ratio Analysis Formula Excel TemplateDocument5 pagesRatio Analysis Formula Excel TemplateTarun MittalNo ratings yet

- Financial Analysis of Selected Textile CompaniesDocument76 pagesFinancial Analysis of Selected Textile CompaniesShahid Mehmood80% (10)

- ARTICLE REVIEW GuidelineDocument2 pagesARTICLE REVIEW Guidelineseble hailemariamNo ratings yet

- Financial Statement and Ratio AnalysisDocument182 pagesFinancial Statement and Ratio AnalysisAsad AliNo ratings yet

- Gitman 12e 525314 IM ch11r 2Document25 pagesGitman 12e 525314 IM ch11r 2jasminroxas87% (15)

- Financial Analysis, Planning and Forecasting Theory and ApplicationDocument102 pagesFinancial Analysis, Planning and Forecasting Theory and ApplicationJose MartinezNo ratings yet

- Stock Valuation Case Report SampleDocument14 pagesStock Valuation Case Report SampleSravanthi Dusi100% (2)

- Decoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisFrom EverandDecoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisNo ratings yet

- Marketing Strategies On Mercantile BankDocument53 pagesMarketing Strategies On Mercantile BankMD. Zakir Hossain AntorNo ratings yet

- Reshma - SIP FINALDocument70 pagesReshma - SIP FINALReshma RaulNo ratings yet

- Capstone Projectpratim Roy Pgdm18381Document30 pagesCapstone Projectpratim Roy Pgdm18381mayankNo ratings yet

- Investment Avenues Available in BangladeshDocument16 pagesInvestment Avenues Available in BangladeshangelNo ratings yet

- 2011017042.ahivusan Talukder (Tipu) PDFDocument22 pages2011017042.ahivusan Talukder (Tipu) PDFangelNo ratings yet

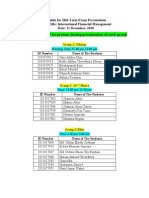

- All Students Must Be Present During Presentation of Each GroupDocument1 pageAll Students Must Be Present During Presentation of Each GroupangelNo ratings yet

- Developing A Multinational Sporting Goods CorporationDocument3 pagesDeveloping A Multinational Sporting Goods CorporationangelNo ratings yet

- 2011017038.shahriar Ahmed ChowdhuryDocument19 pages2011017038.shahriar Ahmed ChowdhuryangelNo ratings yet

- 2011017045.rakhi Bishyas PDFDocument29 pages2011017045.rakhi Bishyas PDFangelNo ratings yet

- Assignment On "Covid 19 and It's Impacts On Employment-International Perspective"Document16 pagesAssignment On "Covid 19 and It's Impacts On Employment-International Perspective"angelNo ratings yet

- Exposure To International Flow of FundsDocument7 pagesExposure To International Flow of FundsangelNo ratings yet

- 2011017040.biman ChowdhuryDocument23 pages2011017040.biman ChowdhuryangelNo ratings yet

- 2011017012.jakia Akther MituDocument32 pages2011017012.jakia Akther MituangelNo ratings yet

- 2011017044.lima Akther Dilruba PDFDocument19 pages2011017044.lima Akther Dilruba PDFangelNo ratings yet

- 2011017004.gulam Haidar SiddiqueDocument24 pages2011017004.gulam Haidar SiddiqueangelNo ratings yet

- 2011017013.bably Akther Chowdhury MouryDocument18 pages2011017013.bably Akther Chowdhury MouryangelNo ratings yet

- An Assignment On: Covid 19 and Its Impacts On Employment-International PerspectiveDocument19 pagesAn Assignment On: Covid 19 and Its Impacts On Employment-International Perspectiveangel100% (1)

- An Assignment On "Covid 19 and Its Impact On Employment: Bangladesh Perspective"Document26 pagesAn Assignment On "Covid 19 and Its Impact On Employment: Bangladesh Perspective"angelNo ratings yet

- Dear RespondentDocument5 pagesDear RespondentangelNo ratings yet

- 2011017001.avishek Talukder DiproDocument18 pages2011017001.avishek Talukder DiproangelNo ratings yet

- Chapter 4: AppendixDocument5 pagesChapter 4: AppendixangelNo ratings yet

- Leading University: On Problem and Prospectus of Tailoring Shop in Sylhet''Document4 pagesLeading University: On Problem and Prospectus of Tailoring Shop in Sylhet''angelNo ratings yet

- Chapter 1: IntroductionDocument20 pagesChapter 1: IntroductionangelNo ratings yet

- Group 3 Vikings - MBA 4th-BDocument24 pagesGroup 3 Vikings - MBA 4th-BangelNo ratings yet

- Group 3 VikingsDocument30 pagesGroup 3 VikingsangelNo ratings yet

- Student List With Topic CodeDocument2 pagesStudent List With Topic CodeangelNo ratings yet

- Assignment On Strengths and WeaknessDocument3 pagesAssignment On Strengths and WeaknessangelNo ratings yet

- Exam Schedule Spring - 20Document2 pagesExam Schedule Spring - 20angelNo ratings yet

- Simple Progressive Simple Progressive: Active Voice Passive VoiceDocument2 pagesSimple Progressive Simple Progressive: Active Voice Passive VoiceangelNo ratings yet

- Identify The Distinctive Characteristics/Behaviors of Quality Leaders/LeadershipDocument2 pagesIdentify The Distinctive Characteristics/Behaviors of Quality Leaders/LeadershipangelNo ratings yet

- Leading University, Sylhet: Student ID Student Name Mid-TermDocument2 pagesLeading University, Sylhet: Student ID Student Name Mid-TermangelNo ratings yet

- Assignment On Describe Your Five Strengths and Five Weakness With Reasons Justifying ThemDocument3 pagesAssignment On Describe Your Five Strengths and Five Weakness With Reasons Justifying ThemangelNo ratings yet

- Group List of MBA 4 - B: Group 1: Wolf Pack ID Number Name of The StudentsDocument2 pagesGroup List of MBA 4 - B: Group 1: Wolf Pack ID Number Name of The StudentsangelNo ratings yet

- Assignment Chapter 3 Problem 1 SolutionDocument13 pagesAssignment Chapter 3 Problem 1 SolutionMUHAMMAD AMMAD ARSHADNo ratings yet

- Toaz - Info Quiz 6 With Solutiondocx PRDocument15 pagesToaz - Info Quiz 6 With Solutiondocx PRReland CastroNo ratings yet

- ACCO 3133 - Midterm Exam - August 18, 2013Document12 pagesACCO 3133 - Midterm Exam - August 18, 2013April Roes Catimbang OrlinNo ratings yet

- Bireme Capital - Investing Through The PandemicDocument106 pagesBireme Capital - Investing Through The PandemicbrineshrimpNo ratings yet

- AICPADocument2 pagesAICPAAngeline RamirezNo ratings yet

- Preparation of Financial Statements-Limited CompaniesDocument9 pagesPreparation of Financial Statements-Limited CompaniesHeavens MupedzisaNo ratings yet

- Toaz - Info WFWFW PRDocument37 pagesToaz - Info WFWFW PRLiaNo ratings yet

- Starbucks Case StudyDocument80 pagesStarbucks Case StudySaniaSuhailNo ratings yet

- Chapter 2 Accounting ElementsDocument40 pagesChapter 2 Accounting ElementsVivek GargNo ratings yet

- Accounting Cycle Exercises 1 (Walther and Skousen) PDFDocument58 pagesAccounting Cycle Exercises 1 (Walther and Skousen) PDFcuongacc100% (1)

- Account Information Form: For Corporations and Partnerships in GeneralDocument6 pagesAccount Information Form: For Corporations and Partnerships in GeneralErichSantosValdeviesoNo ratings yet

- FLR180614FL ADocument31 pagesFLR180614FL ASrinivas KonathamNo ratings yet

- A Project Report On "The Study of Topic Name"Document86 pagesA Project Report On "The Study of Topic Name"anjuNo ratings yet

- Accounting ElementsDocument21 pagesAccounting Elementsdemonking1273433No ratings yet

- Review of Accounting Cycle Review of Accounting CycleDocument4 pagesReview of Accounting Cycle Review of Accounting CycleJerome BaluseroNo ratings yet

- Ch3 IASC Conceptual Framework 2Document30 pagesCh3 IASC Conceptual Framework 2Ramchundar Karuna100% (1)

- Commonly Found Errors in Reporting Practices - ICAIDocument166 pagesCommonly Found Errors in Reporting Practices - ICAIKANNAPPAN NAGARAJANNo ratings yet

- LankaBangla Finance Limited: A Study On Leasing (NBFI) SectorDocument23 pagesLankaBangla Finance Limited: A Study On Leasing (NBFI) SectorRajesh PaulNo ratings yet

- Accounting Concept and Practice: Accounting A Malaysian Perspective 5eDocument63 pagesAccounting Concept and Practice: Accounting A Malaysian Perspective 5eCarmenn LouNo ratings yet

- Chapter 22 - Retained EarningsDocument35 pagesChapter 22 - Retained Earningswala akong pake sayoNo ratings yet

- Base On Penman Course OveeviewDocument10 pagesBase On Penman Course OveeviewPrabowoNo ratings yet

- Exercise 1: Solution: Dewitt's Budgeted Operating Income StatementDocument6 pagesExercise 1: Solution: Dewitt's Budgeted Operating Income StatementShawn MendezNo ratings yet

- Capital Markets Secondary MarketsDocument32 pagesCapital Markets Secondary Marketsmedha_mehtaNo ratings yet

- FM - PharmexDocument63 pagesFM - PharmexadyashasmileNo ratings yet

- Fin464 Final ReportDocument10 pagesFin464 Final ReportTakia KhanNo ratings yet

- Dupont Model and Product Profitability Analysis Based On Activity-Based Costing and Economic Value AddedDocument12 pagesDupont Model and Product Profitability Analysis Based On Activity-Based Costing and Economic Value AddedGaurav SonkeshariyaNo ratings yet

- 161 14 PFRS 9 Financial Instrument Investment in Financial AssetDocument5 pages161 14 PFRS 9 Financial Instrument Investment in Financial AssetRegina Gregoria SalasNo ratings yet

Download as docx, pdf, or txt

You might also like

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetFrom EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetRating: 4.5 out of 5 stars4.5/5 (14)

- Financial Ratio Analysis AssignmentDocument10 pagesFinancial Ratio Analysis Assignmentzain5435467% (3)

- Ratio AnalysisDocument11 pagesRatio AnalysisMadavee JinadasaNo ratings yet

- AuditingDocument30 pagesAuditingMary Rose Mendoza91% (11)

- P&G Company Financial AnalysisDocument42 pagesP&G Company Financial Analysisramki07303375% (4)

- Assignment On Financial Statement Ratio AnalysisDocument27 pagesAssignment On Financial Statement Ratio AnalysisShourav87% (23)

- Ratio Ultratech Cement FinalDocument89 pagesRatio Ultratech Cement FinalDeepti Sharma100% (3)

- FABM 2 Statement of Financial PositionDocument20 pagesFABM 2 Statement of Financial PositionVictoria Manalaysay100% (1)

- Case Studies in Finance and AccountingDocument143 pagesCase Studies in Finance and AccountingRama Krishna Yelamanchili63% (8)

- Financial Ratio AnalysisDocument29 pagesFinancial Ratio AnalysisAbubakar Danmashi82% (17)

- Analysis AssignmentDocument3 pagesAnalysis AssignmentmadyanoshieNo ratings yet

- Financial Ratio AnalysisDocument25 pagesFinancial Ratio AnalysisSimran SinghNo ratings yet

- Analysis of Financial Statement Sample Assignment SolutionDocument23 pagesAnalysis of Financial Statement Sample Assignment SolutionNaveed Saifi100% (5)

- Investment Appraisals Research Proposal 11% FinalDocument19 pagesInvestment Appraisals Research Proposal 11% FinalgishaqueNo ratings yet

- Conclusion: Statements Are The Financial Statements of A Group Presented As Those of A Single Economic EntityDocument2 pagesConclusion: Statements Are The Financial Statements of A Group Presented As Those of A Single Economic EntityJayesh Gawade100% (1)

- Financial Statement Analysis ProjectDocument15 pagesFinancial Statement Analysis ProjectAnonymous wcE2ABquENo ratings yet

- Microsoft - Apple Financial AnalysisDocument27 pagesMicrosoft - Apple Financial Analysisapi-302274400100% (1)

- Corporate Finance AssignmentDocument3 pagesCorporate Finance AssignmenttahaalkibsiNo ratings yet

- 10 Principles of Basic Financial ManagementDocument7 pages10 Principles of Basic Financial ManagementJeyavikinesh Selvakkugan100% (3)

- Mba ThesisDocument170 pagesMba ThesisMushtaq Ahmed Lodhi100% (7)

- RFQ - Development of Modern Silos at 6 Locations in 5 States of India On DBFOT Basis Under PPP ModeDocument150 pagesRFQ - Development of Modern Silos at 6 Locations in 5 States of India On DBFOT Basis Under PPP Modeakhileshver singh100% (1)

- Financial Ratio AnalysisDocument11 pagesFinancial Ratio Analysispradeep100% (5)

- Financial Ratio Analysis Final-No in TextDocument32 pagesFinancial Ratio Analysis Final-No in TextMini8912No ratings yet

- Financial Ratio AnalysisDocument67 pagesFinancial Ratio Analysisrxrohit_23100% (2)

- Financial Ratio AnalysisDocument53 pagesFinancial Ratio AnalysisLaurentia Nurak100% (5)

- Project On Ratio AnalysisDocument57 pagesProject On Ratio Analysisc517880% (5)

- Financial Ratios 2Document7 pagesFinancial Ratios 2Mohammed UsmanNo ratings yet

- Financial Ratio AnalysisDocument8 pagesFinancial Ratio AnalysisNeil Nadua0% (1)

- Analisis RatioDocument5 pagesAnalisis RatioKata AssalamualaikumNo ratings yet

- Ratio AnalysisDocument96 pagesRatio AnalysisPUTERI NUR SYAHIRA SYAZWANI100% (3)

- Financial Analysis ReportDocument51 pagesFinancial Analysis Reportpinkeshparvani50% (2)

- Ratio AnalysisDocument114 pagesRatio AnalysisMehul Jain92% (12)

- Financial Analysis Automobile IndustryDocument38 pagesFinancial Analysis Automobile Industryali iqbalNo ratings yet

- Interpretation of Financial StatementsDocument11 pagesInterpretation of Financial StatementsMaverick CardsNo ratings yet

- MBA Project On Financial RatiosDocument67 pagesMBA Project On Financial Ratioskamdica86% (21)

- Limitation of Ratio AnalysisDocument5 pagesLimitation of Ratio AnalysisMir Wajahat AliNo ratings yet

- Equity Research Report Writing ProcessDocument6 pagesEquity Research Report Writing ProcessQuofi SeliNo ratings yet

- Report On Financial Statement of InfosysDocument22 pagesReport On Financial Statement of InfosysSoham Khanna100% (2)

- ACC102 Financial Statement AnalysisDocument18 pagesACC102 Financial Statement Analysiscraigkrupski12No ratings yet

- Financial Ratios and Their InterpretationDocument10 pagesFinancial Ratios and Their InterpretationPriyanka_Bhans_7838100% (4)

- Financial Statement AnalysisDocument88 pagesFinancial Statement Analysisrohila200195% (38)

- Financial AnalysisDocument107 pagesFinancial AnalysisRamachandran Mahendran100% (4)

- Cash Flow Analysis and StatementDocument127 pagesCash Flow Analysis and Statementsnhk679546100% (6)

- Fundamental Analysis of IT SectorDocument12 pagesFundamental Analysis of IT SectorManasi Kalgutkar100% (2)

- Financial Performance Analysis Mba Project Report DownloadDocument3 pagesFinancial Performance Analysis Mba Project Report DownloadAhamed Ibrahim100% (3)

- Comparative Analysis of Financial Statements 1Document44 pagesComparative Analysis of Financial Statements 1The onion factory100% (1)

- Fundamental Analysis-BHEL - Equity Research ReportDocument5 pagesFundamental Analysis-BHEL - Equity Research ReportChrisNo ratings yet

- Final Report Ratio Analysis Kohinoor Textile Mill PVT: Presented byDocument20 pagesFinal Report Ratio Analysis Kohinoor Textile Mill PVT: Presented byAmoOnBaLushiNo ratings yet

- An Analysis of Financial PerformanceDocument76 pagesAn Analysis of Financial PerformanceShah Kamal100% (8)

- Five Year Financial Statement Analysis of Shell and PSODocument87 pagesFive Year Financial Statement Analysis of Shell and PSOOmer Piracha83% (6)

- Question No: 1 (Marks: 1) - Please Choose OneDocument15 pagesQuestion No: 1 (Marks: 1) - Please Choose OneHassanalizaidi100% (1)

- Ratio Analysis Formula Excel TemplateDocument5 pagesRatio Analysis Formula Excel TemplateTarun MittalNo ratings yet

- Financial Analysis of Selected Textile CompaniesDocument76 pagesFinancial Analysis of Selected Textile CompaniesShahid Mehmood80% (10)

- ARTICLE REVIEW GuidelineDocument2 pagesARTICLE REVIEW Guidelineseble hailemariamNo ratings yet

- Financial Statement and Ratio AnalysisDocument182 pagesFinancial Statement and Ratio AnalysisAsad AliNo ratings yet

- Gitman 12e 525314 IM ch11r 2Document25 pagesGitman 12e 525314 IM ch11r 2jasminroxas87% (15)

- Financial Analysis, Planning and Forecasting Theory and ApplicationDocument102 pagesFinancial Analysis, Planning and Forecasting Theory and ApplicationJose MartinezNo ratings yet

- Stock Valuation Case Report SampleDocument14 pagesStock Valuation Case Report SampleSravanthi Dusi100% (2)

- Decoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisFrom EverandDecoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisNo ratings yet

- Marketing Strategies On Mercantile BankDocument53 pagesMarketing Strategies On Mercantile BankMD. Zakir Hossain AntorNo ratings yet

- Reshma - SIP FINALDocument70 pagesReshma - SIP FINALReshma RaulNo ratings yet

- Capstone Projectpratim Roy Pgdm18381Document30 pagesCapstone Projectpratim Roy Pgdm18381mayankNo ratings yet

- Investment Avenues Available in BangladeshDocument16 pagesInvestment Avenues Available in BangladeshangelNo ratings yet

- 2011017042.ahivusan Talukder (Tipu) PDFDocument22 pages2011017042.ahivusan Talukder (Tipu) PDFangelNo ratings yet

- All Students Must Be Present During Presentation of Each GroupDocument1 pageAll Students Must Be Present During Presentation of Each GroupangelNo ratings yet

- Developing A Multinational Sporting Goods CorporationDocument3 pagesDeveloping A Multinational Sporting Goods CorporationangelNo ratings yet

- 2011017038.shahriar Ahmed ChowdhuryDocument19 pages2011017038.shahriar Ahmed ChowdhuryangelNo ratings yet

- 2011017045.rakhi Bishyas PDFDocument29 pages2011017045.rakhi Bishyas PDFangelNo ratings yet

- Assignment On "Covid 19 and It's Impacts On Employment-International Perspective"Document16 pagesAssignment On "Covid 19 and It's Impacts On Employment-International Perspective"angelNo ratings yet

- Exposure To International Flow of FundsDocument7 pagesExposure To International Flow of FundsangelNo ratings yet

- 2011017040.biman ChowdhuryDocument23 pages2011017040.biman ChowdhuryangelNo ratings yet

- 2011017012.jakia Akther MituDocument32 pages2011017012.jakia Akther MituangelNo ratings yet

- 2011017044.lima Akther Dilruba PDFDocument19 pages2011017044.lima Akther Dilruba PDFangelNo ratings yet

- 2011017004.gulam Haidar SiddiqueDocument24 pages2011017004.gulam Haidar SiddiqueangelNo ratings yet

- 2011017013.bably Akther Chowdhury MouryDocument18 pages2011017013.bably Akther Chowdhury MouryangelNo ratings yet

- An Assignment On: Covid 19 and Its Impacts On Employment-International PerspectiveDocument19 pagesAn Assignment On: Covid 19 and Its Impacts On Employment-International Perspectiveangel100% (1)

- An Assignment On "Covid 19 and Its Impact On Employment: Bangladesh Perspective"Document26 pagesAn Assignment On "Covid 19 and Its Impact On Employment: Bangladesh Perspective"angelNo ratings yet

- Dear RespondentDocument5 pagesDear RespondentangelNo ratings yet

- 2011017001.avishek Talukder DiproDocument18 pages2011017001.avishek Talukder DiproangelNo ratings yet

- Chapter 4: AppendixDocument5 pagesChapter 4: AppendixangelNo ratings yet

- Leading University: On Problem and Prospectus of Tailoring Shop in Sylhet''Document4 pagesLeading University: On Problem and Prospectus of Tailoring Shop in Sylhet''angelNo ratings yet

- Chapter 1: IntroductionDocument20 pagesChapter 1: IntroductionangelNo ratings yet

- Group 3 Vikings - MBA 4th-BDocument24 pagesGroup 3 Vikings - MBA 4th-BangelNo ratings yet

- Group 3 VikingsDocument30 pagesGroup 3 VikingsangelNo ratings yet

- Student List With Topic CodeDocument2 pagesStudent List With Topic CodeangelNo ratings yet

- Assignment On Strengths and WeaknessDocument3 pagesAssignment On Strengths and WeaknessangelNo ratings yet

- Exam Schedule Spring - 20Document2 pagesExam Schedule Spring - 20angelNo ratings yet

- Simple Progressive Simple Progressive: Active Voice Passive VoiceDocument2 pagesSimple Progressive Simple Progressive: Active Voice Passive VoiceangelNo ratings yet

- Identify The Distinctive Characteristics/Behaviors of Quality Leaders/LeadershipDocument2 pagesIdentify The Distinctive Characteristics/Behaviors of Quality Leaders/LeadershipangelNo ratings yet

- Leading University, Sylhet: Student ID Student Name Mid-TermDocument2 pagesLeading University, Sylhet: Student ID Student Name Mid-TermangelNo ratings yet

- Assignment On Describe Your Five Strengths and Five Weakness With Reasons Justifying ThemDocument3 pagesAssignment On Describe Your Five Strengths and Five Weakness With Reasons Justifying ThemangelNo ratings yet

- Group List of MBA 4 - B: Group 1: Wolf Pack ID Number Name of The StudentsDocument2 pagesGroup List of MBA 4 - B: Group 1: Wolf Pack ID Number Name of The StudentsangelNo ratings yet

- Assignment Chapter 3 Problem 1 SolutionDocument13 pagesAssignment Chapter 3 Problem 1 SolutionMUHAMMAD AMMAD ARSHADNo ratings yet

- Toaz - Info Quiz 6 With Solutiondocx PRDocument15 pagesToaz - Info Quiz 6 With Solutiondocx PRReland CastroNo ratings yet

- ACCO 3133 - Midterm Exam - August 18, 2013Document12 pagesACCO 3133 - Midterm Exam - August 18, 2013April Roes Catimbang OrlinNo ratings yet

- Bireme Capital - Investing Through The PandemicDocument106 pagesBireme Capital - Investing Through The PandemicbrineshrimpNo ratings yet

- AICPADocument2 pagesAICPAAngeline RamirezNo ratings yet

- Preparation of Financial Statements-Limited CompaniesDocument9 pagesPreparation of Financial Statements-Limited CompaniesHeavens MupedzisaNo ratings yet

- Toaz - Info WFWFW PRDocument37 pagesToaz - Info WFWFW PRLiaNo ratings yet

- Starbucks Case StudyDocument80 pagesStarbucks Case StudySaniaSuhailNo ratings yet

- Chapter 2 Accounting ElementsDocument40 pagesChapter 2 Accounting ElementsVivek GargNo ratings yet

- Accounting Cycle Exercises 1 (Walther and Skousen) PDFDocument58 pagesAccounting Cycle Exercises 1 (Walther and Skousen) PDFcuongacc100% (1)

- Account Information Form: For Corporations and Partnerships in GeneralDocument6 pagesAccount Information Form: For Corporations and Partnerships in GeneralErichSantosValdeviesoNo ratings yet

- FLR180614FL ADocument31 pagesFLR180614FL ASrinivas KonathamNo ratings yet

- A Project Report On "The Study of Topic Name"Document86 pagesA Project Report On "The Study of Topic Name"anjuNo ratings yet

- Accounting ElementsDocument21 pagesAccounting Elementsdemonking1273433No ratings yet

- Review of Accounting Cycle Review of Accounting CycleDocument4 pagesReview of Accounting Cycle Review of Accounting CycleJerome BaluseroNo ratings yet

- Ch3 IASC Conceptual Framework 2Document30 pagesCh3 IASC Conceptual Framework 2Ramchundar Karuna100% (1)

- Commonly Found Errors in Reporting Practices - ICAIDocument166 pagesCommonly Found Errors in Reporting Practices - ICAIKANNAPPAN NAGARAJANNo ratings yet

- LankaBangla Finance Limited: A Study On Leasing (NBFI) SectorDocument23 pagesLankaBangla Finance Limited: A Study On Leasing (NBFI) SectorRajesh PaulNo ratings yet

- Accounting Concept and Practice: Accounting A Malaysian Perspective 5eDocument63 pagesAccounting Concept and Practice: Accounting A Malaysian Perspective 5eCarmenn LouNo ratings yet

- Chapter 22 - Retained EarningsDocument35 pagesChapter 22 - Retained Earningswala akong pake sayoNo ratings yet

- Base On Penman Course OveeviewDocument10 pagesBase On Penman Course OveeviewPrabowoNo ratings yet

- Exercise 1: Solution: Dewitt's Budgeted Operating Income StatementDocument6 pagesExercise 1: Solution: Dewitt's Budgeted Operating Income StatementShawn MendezNo ratings yet

- Capital Markets Secondary MarketsDocument32 pagesCapital Markets Secondary Marketsmedha_mehtaNo ratings yet

- FM - PharmexDocument63 pagesFM - PharmexadyashasmileNo ratings yet

- Fin464 Final ReportDocument10 pagesFin464 Final ReportTakia KhanNo ratings yet

- Dupont Model and Product Profitability Analysis Based On Activity-Based Costing and Economic Value AddedDocument12 pagesDupont Model and Product Profitability Analysis Based On Activity-Based Costing and Economic Value AddedGaurav SonkeshariyaNo ratings yet

- 161 14 PFRS 9 Financial Instrument Investment in Financial AssetDocument5 pages161 14 PFRS 9 Financial Instrument Investment in Financial AssetRegina Gregoria SalasNo ratings yet