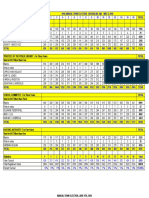

Advisory Committee Chair Mike Sandman's Explanation On The $26.6M in Unassigned Funds

Advisory Committee Chair Mike Sandman's Explanation On The $26.6M in Unassigned Funds

You might also like

- Maryland American Water BillDocument1 pageMaryland American Water BillOmar BouayadNo ratings yet

- Paystub 3Document1 pagePaystub 3J RequenaNo ratings yet

- OBN - AFBA - Issue 36 (August 2021)Document1 pageOBN - AFBA - Issue 36 (August 2021)Nate TobikNo ratings yet

- Amy Hall Civil Complaint Against The Brookline Police DepartmentDocument13 pagesAmy Hall Civil Complaint Against The Brookline Police DepartmentAbby PatkinNo ratings yet

- NY CashflowcrunchDocument8 pagesNY CashflowcrunchZerohedgeNo ratings yet

- CFO Opening StatementDocument3 pagesCFO Opening StatementThe Daily LineNo ratings yet

- The Demise of Silicon Valley Bank - by Marc RubinsteinDocument10 pagesThe Demise of Silicon Valley Bank - by Marc Rubinsteinkaala_yuvrajNo ratings yet

- RCSD Budget Update 04-07-20Document11 pagesRCSD Budget Update 04-07-20WXXI NewsNo ratings yet

- 2013 State of The City ReportDocument6 pages2013 State of The City ReportScott FranzNo ratings yet

- New York's Deficit Shuffle: April 2010Document23 pagesNew York's Deficit Shuffle: April 2010Casey SeilerNo ratings yet

- Discussion Paper - Municipal BondsDocument3 pagesDiscussion Paper - Municipal BondsmalyalarahulNo ratings yet

- 5-NURFC Highlights For 5 June 2007 MeetingDocument1 page5-NURFC Highlights For 5 June 2007 MeetingCOASTNo ratings yet

- Commission of Inquiry Report 4 - 4Document8 pagesCommission of Inquiry Report 4 - 4michael_olson6605No ratings yet

- City of San Diego General Fund Reserve Benchmark and Review: Office of The Independent Budget Analyst ReportDocument9 pagesCity of San Diego General Fund Reserve Benchmark and Review: Office of The Independent Budget Analyst Reportapi-26844346No ratings yet

- Acct 260 Cafr 6-17Document4 pagesAcct 260 Cafr 6-17StephanieNo ratings yet

- New York State Dedicated Highway and Bridge Trust Fund CrossroadsDocument18 pagesNew York State Dedicated Highway and Bridge Trust Fund CrossroadsNews10NBCNo ratings yet

- Sellside 121921Document49 pagesSellside 121921jolly soNo ratings yet

- Seattle Considers Expanding 'JumpStart' Tax On Big Businesses To Plug Budget DeficitDocument15 pagesSeattle Considers Expanding 'JumpStart' Tax On Big Businesses To Plug Budget DeficitGeekWireNo ratings yet

- 2009-08-12 Saxo Bank Research Note - FDIC DIFDocument3 pages2009-08-12 Saxo Bank Research Note - FDIC DIFSwamiNo ratings yet

- (Almeida, Asia-Pacific 2021) Liquidity Management During The Covid 19 PandemicDocument18 pages(Almeida, Asia-Pacific 2021) Liquidity Management During The Covid 19 PandemicFelipe & Alexandre M CostaNo ratings yet

- Budget Deficit and Public DebtDocument3 pagesBudget Deficit and Public DebtFaisal AwanNo ratings yet

- Binder - LL - SecDocument23 pagesBinder - LL - SecMy-Acts Of-SeditionNo ratings yet

- CBC NYC 2025 Fiscal OutlookDocument2 pagesCBC NYC 2025 Fiscal OutlookBrian HoreyNo ratings yet

- Key Excerpts: "Document4 pagesKey Excerpts: "Susie CambriaNo ratings yet

- Press Release Council of The District of ColumbiaDocument4 pagesPress Release Council of The District of ColumbiaSusie Cambria100% (2)

- Brockton Schools AuditDocument4 pagesBrockton Schools AuditBoston 25 DeskNo ratings yet

- 0910 BudgetDocument346 pages0910 BudgetValerie F. LeonardNo ratings yet

- Acc423 in 2015 Better City Received 5000000 of BondDocument8 pagesAcc423 in 2015 Better City Received 5000000 of BondDoreenNo ratings yet

- SL Debt Trap (30april2017)Document4 pagesSL Debt Trap (30april2017)Jagath SenaNo ratings yet

- ACFR REPORTDocument13 pagesACFR REPORTQuyên QuyênNo ratings yet

- Council Questions - Fiscal Year 2013 Budget Discussion March 2012Document6 pagesCouncil Questions - Fiscal Year 2013 Budget Discussion March 2012Richard G. FimbresNo ratings yet

- Citizens Union - Spending in The Shadows - Nonspecific Funding in The FY 19 NYS Executive BudgetDocument25 pagesCitizens Union - Spending in The Shadows - Nonspecific Funding in The FY 19 NYS Executive BudgetCitizens UnionNo ratings yet

- TimeIsMoney-Jansen Katz McKinsey2002Document10 pagesTimeIsMoney-Jansen Katz McKinsey2002Shubham ChoudharyNo ratings yet

- NYSenate Republican WhiteBook FY2020 FINALDocument276 pagesNYSenate Republican WhiteBook FY2020 FINALNew York SenateNo ratings yet

- Binder Allen MisfeasanceDocument8 pagesBinder Allen MisfeasanceMy-Acts Of-SeditionNo ratings yet

- Review of The Financial Plan of The City of New York: Report 10-2016Document36 pagesReview of The Financial Plan of The City of New York: Report 10-2016Nick ReismanNo ratings yet

- Written Assignment Unit 6 Promissory Notes Bus 1102Document5 pagesWritten Assignment Unit 6 Promissory Notes Bus 1102lisalumm2No ratings yet

- Canada's Vast Pension Fund Is Gaining Even More Financial Clout - Moose in The MarketDocument2 pagesCanada's Vast Pension Fund Is Gaining Even More Financial Clout - Moose in The MarketFaustinNo ratings yet

- 2016 17 Enacted Budget FinplanDocument47 pages2016 17 Enacted Budget FinplanMatthew HamiltonNo ratings yet

- Def 4Document7 pagesDef 4Guezil Joy DelfinNo ratings yet

- Nov 2022 - Volume - 11 FinalDocument12 pagesNov 2022 - Volume - 11 Finalkaushal talukderNo ratings yet

- 14-Freedom Center Analysis Update Febuary 2007Document3 pages14-Freedom Center Analysis Update Febuary 2007COASTNo ratings yet

- Standing Strong With The BOGDocument6 pagesStanding Strong With The BOGFred DzakpataNo ratings yet

- FRMO Corp. 2019 Shareholder Letter: Part I: New VenturesDocument8 pagesFRMO Corp. 2019 Shareholder Letter: Part I: New VenturesPland SpringNo ratings yet

- Accounting For Grants: Liability Method.: How-To Guide GR1Document3 pagesAccounting For Grants: Liability Method.: How-To Guide GR1cris lu salemNo ratings yet

- Livingston County 2024 Proposed BudgetDocument395 pagesLivingston County 2024 Proposed BudgetThe Livingston County NewsNo ratings yet

- Assignment On LGA.Document9 pagesAssignment On LGA.kenneth kayetaNo ratings yet

- 4.29 Finance Speech FinalDocument18 pages4.29 Finance Speech FinalCrains Chicago BusinessNo ratings yet

- Feb 16 Emergency President Report CUP76Document11 pagesFeb 16 Emergency President Report CUP76jsource2007No ratings yet

- 2016 17 Enacted Budget Report PDFDocument74 pages2016 17 Enacted Budget Report PDFNick ReismanNo ratings yet

- CZBS - Playing A Different GameDocument5 pagesCZBS - Playing A Different GameWillNo ratings yet

- Grants Interest Rate Observer Summer E IssueDocument24 pagesGrants Interest Rate Observer Summer E IssueCanadianValueNo ratings yet

- Fixed Income Markets Assignment: TanushiDocument5 pagesFixed Income Markets Assignment: TanushiTanushiNo ratings yet

- Best Goverment FundDocument12 pagesBest Goverment FundMinaw BelayNo ratings yet

- Other Comprehensive Basis of Accounting (OCBOA) Cash Basis Notes To The Financial StatementsDocument39 pagesOther Comprehensive Basis of Accounting (OCBOA) Cash Basis Notes To The Financial StatementsDexter P. VargasNo ratings yet

- FY 2024 Recommended Operating BudgetDocument275 pagesFY 2024 Recommended Operating BudgetSarah Joy BaybayonNo ratings yet

- Otc FSRL 2020Document66 pagesOtc FSRL 2020Vinayak BagayaNo ratings yet

- Livingston County Adopted Budget (2023)Document401 pagesLivingston County Adopted Budget (2023)Watertown Daily TimesNo ratings yet

- Risks Faced by Financial Institutions: Sudheer Chava Fall 2016Document31 pagesRisks Faced by Financial Institutions: Sudheer Chava Fall 2016sidNo ratings yet

- Asian Development Bank Trust Funds Report 2020: Includes Global and Special FundsFrom EverandAsian Development Bank Trust Funds Report 2020: Includes Global and Special FundsNo ratings yet

- Browder ComplaintDocument9 pagesBrowder ComplaintAbby PatkinNo ratings yet

- Natick 2022 Town Election Unofficial ResultsDocument4 pagesNatick 2022 Town Election Unofficial ResultsAbby PatkinNo ratings yet

- Judge Wilkins' Decision Denying Town Appeal of Civil Service DecisionDocument15 pagesJudge Wilkins' Decision Denying Town Appeal of Civil Service DecisionAbby PatkinNo ratings yet

- Alston DecisionDocument9 pagesAlston DecisionReporterJennaNo ratings yet

- Unofficial Results 05-04-2021Document11 pagesUnofficial Results 05-04-2021Jenna FisherNo ratings yet

- Un-Official Results 06.09.20Document9 pagesUn-Official Results 06.09.20ReporterJennaNo ratings yet

- Brookline's Super Tuesday Unofficial ResultsDocument7 pagesBrookline's Super Tuesday Unofficial ResultsAbby PatkinNo ratings yet

- Special Town Counsel's Response On NPS Baldwin EmailDocument4 pagesSpecial Town Counsel's Response On NPS Baldwin EmailAbby PatkinNo ratings yet

- Unofficial Results of Brookline's 2019 ElectionDocument9 pagesUnofficial Results of Brookline's 2019 ElectionAbby PatkinNo ratings yet

- Solution Manual For Advanced Accounting 7th Edition Debra C Jeter Paul K ChaneyDocument29 pagesSolution Manual For Advanced Accounting 7th Edition Debra C Jeter Paul K Chaneybraidscanty8unib100% (45)

- Role of Icab and IcmabDocument12 pagesRole of Icab and IcmabEast West Technical InstituteNo ratings yet

- Principle of Legislation and Interpretation of StatutesDocument15 pagesPrinciple of Legislation and Interpretation of StatutesMayank TripathiNo ratings yet

- Ajay Sharma Anticipatory Bail Sonika 2017Document31 pagesAjay Sharma Anticipatory Bail Sonika 2017Anirudh Kaushal50% (2)

- Ds 160 BHDocument7 pagesDs 160 BHanilpunnamNo ratings yet

- Wills and Succession 2Document22 pagesWills and Succession 2lex omniaeNo ratings yet

- SEBI Grade A Phase I and Phase II Course: Facebook: TelegramDocument15 pagesSEBI Grade A Phase I and Phase II Course: Facebook: TelegramartizutshiNo ratings yet

- Europower EPX2800/EPX4000: Quick Start GuideDocument15 pagesEuropower EPX2800/EPX4000: Quick Start GuideSalvador VelasquezNo ratings yet

- August 2018 Pharmacist Licensure Examination: Seq. NODocument4 pagesAugust 2018 Pharmacist Licensure Examination: Seq. NOPRC BoardNo ratings yet

- E.I. DuPont de Nemours and Company v. Heraeus Materials Technology Et. Al.Document7 pagesE.I. DuPont de Nemours and Company v. Heraeus Materials Technology Et. Al.PriorSmartNo ratings yet

- Summary - Civil DisobedienceDocument3 pagesSummary - Civil DisobedienceQueenNo ratings yet

- Bylaws REG V.nov 2021Document15 pagesBylaws REG V.nov 2021Lean Manuel Paragas100% (1)

- Lexisnexis Capsule Summary: © 2004 Lexisnexis, A Division of Reed Elsevier Inc. All Rights ReservedDocument73 pagesLexisnexis Capsule Summary: © 2004 Lexisnexis, A Division of Reed Elsevier Inc. All Rights ReservedOlivia SchmidNo ratings yet

- Contract of SaleDocument18 pagesContract of SaleAmie Jane MirandaNo ratings yet

- Validity of Global Moonsighting: 1. Cause of Rama Ān FastDocument3 pagesValidity of Global Moonsighting: 1. Cause of Rama Ān FastYahya AliNo ratings yet

- Steamship Mutual vs. Sulpicio Lines, G.R. No. 196072, 2017Document33 pagesSteamship Mutual vs. Sulpicio Lines, G.R. No. 196072, 2017Nikko AlelojoNo ratings yet

- El Filibusterismo: Morales Vin Allen A. BSE-2CDocument12 pagesEl Filibusterismo: Morales Vin Allen A. BSE-2CRenz MoralesNo ratings yet

- MECA Newsletter Spring 2023Document8 pagesMECA Newsletter Spring 2023Middle East Children's AllianceNo ratings yet

- Financial Reporting: © The Institute of Chartered Accountants of IndiaDocument5 pagesFinancial Reporting: © The Institute of Chartered Accountants of IndiaRITZ BROWNNo ratings yet

- The Analysis of Taiwan's Labor Standards ActDocument2 pagesThe Analysis of Taiwan's Labor Standards ActJeslynNo ratings yet

- Midterm SalesDocument3 pagesMidterm SalesArzaga Dessa BCNo ratings yet

- Anil RSMSSB ApplicationDocument3 pagesAnil RSMSSB ApplicationACE CTPPNo ratings yet

- Garcia Vs VazquezDocument1 pageGarcia Vs VazquezAbrahamNo ratings yet

- Proposed Rape Kit Law - SB0014Document2 pagesProposed Rape Kit Law - SB0014FOX 17 News Digital StaffNo ratings yet

- Criminal Procedure Case Digest (Morgan) 2.0Document20 pagesCriminal Procedure Case Digest (Morgan) 2.0pasmoNo ratings yet

- CPCCBC5002A - Unit Assessment PackDocument70 pagesCPCCBC5002A - Unit Assessment PackDivya JoshiNo ratings yet

- Affordable CebuDocument19 pagesAffordable CebuNicko TanteNo ratings yet

- Art. 1156 1178Document18 pagesArt. 1156 1178Vortex100% (1)

Download as docx, pdf, or txt

You might also like

- Maryland American Water BillDocument1 pageMaryland American Water BillOmar BouayadNo ratings yet

- Paystub 3Document1 pagePaystub 3J RequenaNo ratings yet

- OBN - AFBA - Issue 36 (August 2021)Document1 pageOBN - AFBA - Issue 36 (August 2021)Nate TobikNo ratings yet

- Amy Hall Civil Complaint Against The Brookline Police DepartmentDocument13 pagesAmy Hall Civil Complaint Against The Brookline Police DepartmentAbby PatkinNo ratings yet

- NY CashflowcrunchDocument8 pagesNY CashflowcrunchZerohedgeNo ratings yet

- CFO Opening StatementDocument3 pagesCFO Opening StatementThe Daily LineNo ratings yet

- The Demise of Silicon Valley Bank - by Marc RubinsteinDocument10 pagesThe Demise of Silicon Valley Bank - by Marc Rubinsteinkaala_yuvrajNo ratings yet

- RCSD Budget Update 04-07-20Document11 pagesRCSD Budget Update 04-07-20WXXI NewsNo ratings yet

- 2013 State of The City ReportDocument6 pages2013 State of The City ReportScott FranzNo ratings yet

- New York's Deficit Shuffle: April 2010Document23 pagesNew York's Deficit Shuffle: April 2010Casey SeilerNo ratings yet

- Discussion Paper - Municipal BondsDocument3 pagesDiscussion Paper - Municipal BondsmalyalarahulNo ratings yet

- 5-NURFC Highlights For 5 June 2007 MeetingDocument1 page5-NURFC Highlights For 5 June 2007 MeetingCOASTNo ratings yet

- Commission of Inquiry Report 4 - 4Document8 pagesCommission of Inquiry Report 4 - 4michael_olson6605No ratings yet

- City of San Diego General Fund Reserve Benchmark and Review: Office of The Independent Budget Analyst ReportDocument9 pagesCity of San Diego General Fund Reserve Benchmark and Review: Office of The Independent Budget Analyst Reportapi-26844346No ratings yet

- Acct 260 Cafr 6-17Document4 pagesAcct 260 Cafr 6-17StephanieNo ratings yet

- New York State Dedicated Highway and Bridge Trust Fund CrossroadsDocument18 pagesNew York State Dedicated Highway and Bridge Trust Fund CrossroadsNews10NBCNo ratings yet

- Sellside 121921Document49 pagesSellside 121921jolly soNo ratings yet

- Seattle Considers Expanding 'JumpStart' Tax On Big Businesses To Plug Budget DeficitDocument15 pagesSeattle Considers Expanding 'JumpStart' Tax On Big Businesses To Plug Budget DeficitGeekWireNo ratings yet

- 2009-08-12 Saxo Bank Research Note - FDIC DIFDocument3 pages2009-08-12 Saxo Bank Research Note - FDIC DIFSwamiNo ratings yet

- (Almeida, Asia-Pacific 2021) Liquidity Management During The Covid 19 PandemicDocument18 pages(Almeida, Asia-Pacific 2021) Liquidity Management During The Covid 19 PandemicFelipe & Alexandre M CostaNo ratings yet

- Budget Deficit and Public DebtDocument3 pagesBudget Deficit and Public DebtFaisal AwanNo ratings yet

- Binder - LL - SecDocument23 pagesBinder - LL - SecMy-Acts Of-SeditionNo ratings yet

- CBC NYC 2025 Fiscal OutlookDocument2 pagesCBC NYC 2025 Fiscal OutlookBrian HoreyNo ratings yet

- Key Excerpts: "Document4 pagesKey Excerpts: "Susie CambriaNo ratings yet

- Press Release Council of The District of ColumbiaDocument4 pagesPress Release Council of The District of ColumbiaSusie Cambria100% (2)

- Brockton Schools AuditDocument4 pagesBrockton Schools AuditBoston 25 DeskNo ratings yet

- 0910 BudgetDocument346 pages0910 BudgetValerie F. LeonardNo ratings yet

- Acc423 in 2015 Better City Received 5000000 of BondDocument8 pagesAcc423 in 2015 Better City Received 5000000 of BondDoreenNo ratings yet

- SL Debt Trap (30april2017)Document4 pagesSL Debt Trap (30april2017)Jagath SenaNo ratings yet

- ACFR REPORTDocument13 pagesACFR REPORTQuyên QuyênNo ratings yet

- Council Questions - Fiscal Year 2013 Budget Discussion March 2012Document6 pagesCouncil Questions - Fiscal Year 2013 Budget Discussion March 2012Richard G. FimbresNo ratings yet

- Citizens Union - Spending in The Shadows - Nonspecific Funding in The FY 19 NYS Executive BudgetDocument25 pagesCitizens Union - Spending in The Shadows - Nonspecific Funding in The FY 19 NYS Executive BudgetCitizens UnionNo ratings yet

- TimeIsMoney-Jansen Katz McKinsey2002Document10 pagesTimeIsMoney-Jansen Katz McKinsey2002Shubham ChoudharyNo ratings yet

- NYSenate Republican WhiteBook FY2020 FINALDocument276 pagesNYSenate Republican WhiteBook FY2020 FINALNew York SenateNo ratings yet

- Binder Allen MisfeasanceDocument8 pagesBinder Allen MisfeasanceMy-Acts Of-SeditionNo ratings yet

- Review of The Financial Plan of The City of New York: Report 10-2016Document36 pagesReview of The Financial Plan of The City of New York: Report 10-2016Nick ReismanNo ratings yet

- Written Assignment Unit 6 Promissory Notes Bus 1102Document5 pagesWritten Assignment Unit 6 Promissory Notes Bus 1102lisalumm2No ratings yet

- Canada's Vast Pension Fund Is Gaining Even More Financial Clout - Moose in The MarketDocument2 pagesCanada's Vast Pension Fund Is Gaining Even More Financial Clout - Moose in The MarketFaustinNo ratings yet

- 2016 17 Enacted Budget FinplanDocument47 pages2016 17 Enacted Budget FinplanMatthew HamiltonNo ratings yet

- Def 4Document7 pagesDef 4Guezil Joy DelfinNo ratings yet

- Nov 2022 - Volume - 11 FinalDocument12 pagesNov 2022 - Volume - 11 Finalkaushal talukderNo ratings yet

- 14-Freedom Center Analysis Update Febuary 2007Document3 pages14-Freedom Center Analysis Update Febuary 2007COASTNo ratings yet

- Standing Strong With The BOGDocument6 pagesStanding Strong With The BOGFred DzakpataNo ratings yet

- FRMO Corp. 2019 Shareholder Letter: Part I: New VenturesDocument8 pagesFRMO Corp. 2019 Shareholder Letter: Part I: New VenturesPland SpringNo ratings yet

- Accounting For Grants: Liability Method.: How-To Guide GR1Document3 pagesAccounting For Grants: Liability Method.: How-To Guide GR1cris lu salemNo ratings yet

- Livingston County 2024 Proposed BudgetDocument395 pagesLivingston County 2024 Proposed BudgetThe Livingston County NewsNo ratings yet

- Assignment On LGA.Document9 pagesAssignment On LGA.kenneth kayetaNo ratings yet

- 4.29 Finance Speech FinalDocument18 pages4.29 Finance Speech FinalCrains Chicago BusinessNo ratings yet

- Feb 16 Emergency President Report CUP76Document11 pagesFeb 16 Emergency President Report CUP76jsource2007No ratings yet

- 2016 17 Enacted Budget Report PDFDocument74 pages2016 17 Enacted Budget Report PDFNick ReismanNo ratings yet

- CZBS - Playing A Different GameDocument5 pagesCZBS - Playing A Different GameWillNo ratings yet

- Grants Interest Rate Observer Summer E IssueDocument24 pagesGrants Interest Rate Observer Summer E IssueCanadianValueNo ratings yet

- Fixed Income Markets Assignment: TanushiDocument5 pagesFixed Income Markets Assignment: TanushiTanushiNo ratings yet

- Best Goverment FundDocument12 pagesBest Goverment FundMinaw BelayNo ratings yet

- Other Comprehensive Basis of Accounting (OCBOA) Cash Basis Notes To The Financial StatementsDocument39 pagesOther Comprehensive Basis of Accounting (OCBOA) Cash Basis Notes To The Financial StatementsDexter P. VargasNo ratings yet

- FY 2024 Recommended Operating BudgetDocument275 pagesFY 2024 Recommended Operating BudgetSarah Joy BaybayonNo ratings yet

- Otc FSRL 2020Document66 pagesOtc FSRL 2020Vinayak BagayaNo ratings yet

- Livingston County Adopted Budget (2023)Document401 pagesLivingston County Adopted Budget (2023)Watertown Daily TimesNo ratings yet

- Risks Faced by Financial Institutions: Sudheer Chava Fall 2016Document31 pagesRisks Faced by Financial Institutions: Sudheer Chava Fall 2016sidNo ratings yet

- Asian Development Bank Trust Funds Report 2020: Includes Global and Special FundsFrom EverandAsian Development Bank Trust Funds Report 2020: Includes Global and Special FundsNo ratings yet

- Browder ComplaintDocument9 pagesBrowder ComplaintAbby PatkinNo ratings yet

- Natick 2022 Town Election Unofficial ResultsDocument4 pagesNatick 2022 Town Election Unofficial ResultsAbby PatkinNo ratings yet

- Judge Wilkins' Decision Denying Town Appeal of Civil Service DecisionDocument15 pagesJudge Wilkins' Decision Denying Town Appeal of Civil Service DecisionAbby PatkinNo ratings yet

- Alston DecisionDocument9 pagesAlston DecisionReporterJennaNo ratings yet

- Unofficial Results 05-04-2021Document11 pagesUnofficial Results 05-04-2021Jenna FisherNo ratings yet

- Un-Official Results 06.09.20Document9 pagesUn-Official Results 06.09.20ReporterJennaNo ratings yet

- Brookline's Super Tuesday Unofficial ResultsDocument7 pagesBrookline's Super Tuesday Unofficial ResultsAbby PatkinNo ratings yet

- Special Town Counsel's Response On NPS Baldwin EmailDocument4 pagesSpecial Town Counsel's Response On NPS Baldwin EmailAbby PatkinNo ratings yet

- Unofficial Results of Brookline's 2019 ElectionDocument9 pagesUnofficial Results of Brookline's 2019 ElectionAbby PatkinNo ratings yet

- Solution Manual For Advanced Accounting 7th Edition Debra C Jeter Paul K ChaneyDocument29 pagesSolution Manual For Advanced Accounting 7th Edition Debra C Jeter Paul K Chaneybraidscanty8unib100% (45)

- Role of Icab and IcmabDocument12 pagesRole of Icab and IcmabEast West Technical InstituteNo ratings yet

- Principle of Legislation and Interpretation of StatutesDocument15 pagesPrinciple of Legislation and Interpretation of StatutesMayank TripathiNo ratings yet

- Ajay Sharma Anticipatory Bail Sonika 2017Document31 pagesAjay Sharma Anticipatory Bail Sonika 2017Anirudh Kaushal50% (2)

- Ds 160 BHDocument7 pagesDs 160 BHanilpunnamNo ratings yet

- Wills and Succession 2Document22 pagesWills and Succession 2lex omniaeNo ratings yet

- SEBI Grade A Phase I and Phase II Course: Facebook: TelegramDocument15 pagesSEBI Grade A Phase I and Phase II Course: Facebook: TelegramartizutshiNo ratings yet

- Europower EPX2800/EPX4000: Quick Start GuideDocument15 pagesEuropower EPX2800/EPX4000: Quick Start GuideSalvador VelasquezNo ratings yet

- August 2018 Pharmacist Licensure Examination: Seq. NODocument4 pagesAugust 2018 Pharmacist Licensure Examination: Seq. NOPRC BoardNo ratings yet

- E.I. DuPont de Nemours and Company v. Heraeus Materials Technology Et. Al.Document7 pagesE.I. DuPont de Nemours and Company v. Heraeus Materials Technology Et. Al.PriorSmartNo ratings yet

- Summary - Civil DisobedienceDocument3 pagesSummary - Civil DisobedienceQueenNo ratings yet

- Bylaws REG V.nov 2021Document15 pagesBylaws REG V.nov 2021Lean Manuel Paragas100% (1)

- Lexisnexis Capsule Summary: © 2004 Lexisnexis, A Division of Reed Elsevier Inc. All Rights ReservedDocument73 pagesLexisnexis Capsule Summary: © 2004 Lexisnexis, A Division of Reed Elsevier Inc. All Rights ReservedOlivia SchmidNo ratings yet

- Contract of SaleDocument18 pagesContract of SaleAmie Jane MirandaNo ratings yet

- Validity of Global Moonsighting: 1. Cause of Rama Ān FastDocument3 pagesValidity of Global Moonsighting: 1. Cause of Rama Ān FastYahya AliNo ratings yet

- Steamship Mutual vs. Sulpicio Lines, G.R. No. 196072, 2017Document33 pagesSteamship Mutual vs. Sulpicio Lines, G.R. No. 196072, 2017Nikko AlelojoNo ratings yet

- El Filibusterismo: Morales Vin Allen A. BSE-2CDocument12 pagesEl Filibusterismo: Morales Vin Allen A. BSE-2CRenz MoralesNo ratings yet

- MECA Newsletter Spring 2023Document8 pagesMECA Newsletter Spring 2023Middle East Children's AllianceNo ratings yet

- Financial Reporting: © The Institute of Chartered Accountants of IndiaDocument5 pagesFinancial Reporting: © The Institute of Chartered Accountants of IndiaRITZ BROWNNo ratings yet

- The Analysis of Taiwan's Labor Standards ActDocument2 pagesThe Analysis of Taiwan's Labor Standards ActJeslynNo ratings yet

- Midterm SalesDocument3 pagesMidterm SalesArzaga Dessa BCNo ratings yet

- Anil RSMSSB ApplicationDocument3 pagesAnil RSMSSB ApplicationACE CTPPNo ratings yet

- Garcia Vs VazquezDocument1 pageGarcia Vs VazquezAbrahamNo ratings yet

- Proposed Rape Kit Law - SB0014Document2 pagesProposed Rape Kit Law - SB0014FOX 17 News Digital StaffNo ratings yet

- Criminal Procedure Case Digest (Morgan) 2.0Document20 pagesCriminal Procedure Case Digest (Morgan) 2.0pasmoNo ratings yet

- CPCCBC5002A - Unit Assessment PackDocument70 pagesCPCCBC5002A - Unit Assessment PackDivya JoshiNo ratings yet

- Affordable CebuDocument19 pagesAffordable CebuNicko TanteNo ratings yet

- Art. 1156 1178Document18 pagesArt. 1156 1178Vortex100% (1)