Download as pdf or txt

You might also like

- Making A Tough Personnel Decision at Nova Waterfront HotelDocument11 pagesMaking A Tough Personnel Decision at Nova Waterfront HotelSiddharthNo ratings yet

- A Project Report Pepsi VS Coca ColaDocument67 pagesA Project Report Pepsi VS Coca Colasharma_bigamit_sharma92% (90)

- Inc42's Annual Indian Startup Funding Report 2021Document91 pagesInc42's Annual Indian Startup Funding Report 2021Ritik MehtaNo ratings yet

- Borghese & Torlonia Banking Mafia - Black NobilityDocument29 pagesBorghese & Torlonia Banking Mafia - Black NobilitychavalukoNo ratings yet

- Chapter 1 - Introduction To Cost AccountingDocument34 pagesChapter 1 - Introduction To Cost AccountingGlaiza Lipana PingolNo ratings yet

- StepSmart Fitness ExlDocument9 pagesStepSmart Fitness ExlNishiGogia50% (2)

- Financials WorksheetDocument3 pagesFinancials WorksheetSiddharthNo ratings yet

- Question 5-What Should L. L. Bean Do To Improve Its Forecasting Process?Document1 pageQuestion 5-What Should L. L. Bean Do To Improve Its Forecasting Process?SiddharthNo ratings yet

- Management Accounting: BY - Aprajita Malhan (32) Bharti Singh (44) (Mba - A)Document25 pagesManagement Accounting: BY - Aprajita Malhan (32) Bharti Singh (44) (Mba - A)Jennifer HerreraNo ratings yet

- Chapter 1 - Intro - CLC - handout.pptxDocument26 pagesChapter 1 - Intro - CLC - handout.pptxHoàng Bảo TrâmNo ratings yet

- 1-Ch 1Document13 pages1-Ch 1pks009No ratings yet

- Ch01 Introduction To Cost AccountingDocument21 pagesCh01 Introduction To Cost AccountingElaisa Nina Marie TrinidadNo ratings yet

- Ma Chapter 01Document14 pagesMa Chapter 01sharxx47No ratings yet

- RSHBBA207171022215134Document25 pagesRSHBBA207171022215134Suraj MishraNo ratings yet

- Cost Accounting Foundations and EvolutionsDocument49 pagesCost Accounting Foundations and EvolutionsTina LlorcaNo ratings yet

- Chapter 1 - Intro - CLC - HandoutDocument26 pagesChapter 1 - Intro - CLC - HandoutMai ChiNo ratings yet

- Materi AKMENDocument102 pagesMateri AKMENSagita Rajagukguk100% (1)

- PDF Crop PDFDocument94 pagesPDF Crop PDFEdison CabatbatNo ratings yet

- Management Accounting Chapter 1Document30 pagesManagement Accounting Chapter 1dawsonNo ratings yet

- Management Accounting: Information That Creates ValueDocument101 pagesManagement Accounting: Information That Creates ValueChuah Chong Ann100% (1)

- Management Control SystemDocument34 pagesManagement Control Systemravish419100% (6)

- MAC BepDocument54 pagesMAC BepambrosiaeffectNo ratings yet

- Introduction To Management AccountingDocument6 pagesIntroduction To Management AccountingHera AsuncionNo ratings yet

- Chapter 1Document23 pagesChapter 1Nandini SinhaNo ratings yet

- FINANCIAL MANAGEMENT For Agribusiness CPU 2nd Sem 2018-2019Document221 pagesFINANCIAL MANAGEMENT For Agribusiness CPU 2nd Sem 2018-2019Joyce Wendam100% (2)

- Macc Maksi - How Management Accounting Information Support Decision MakingDocument31 pagesMacc Maksi - How Management Accounting Information Support Decision MakinglovianicyndiNo ratings yet

- Chapter 1 Cost Accounting FundamentalsDocument15 pagesChapter 1 Cost Accounting FundamentalsMarriel Fate Cullano0% (1)

- Straco ReviewerDocument5 pagesStraco ReviewerKemberly JavaNo ratings yet

- ACCY918 - Week1 - Introduciton and Cost Concepts - Lecture NoteDocument83 pagesACCY918 - Week1 - Introduciton and Cost Concepts - Lecture NoteNIRAJ SharmaNo ratings yet

- Assessing Financial StatementsDocument34 pagesAssessing Financial StatementsGotenk JujuNo ratings yet

- Updates in Managerial AccountingDocument15 pagesUpdates in Managerial Accountingstudentone50% (2)

- IAPI Webinar Stathis GouldDocument17 pagesIAPI Webinar Stathis GoulddjagoenkNo ratings yet

- Finance For Non Financial ManagersDocument5 pagesFinance For Non Financial ManagersBrighton Masuku0% (2)

- Auditcommitteeleadingpractices bb2278 February2012Document15 pagesAuditcommitteeleadingpractices bb2278 February2012Darius RamNo ratings yet

- Accounts Project Assingment 1 (Raj Vardhan Agarwal 1782084)Document8 pagesAccounts Project Assingment 1 (Raj Vardhan Agarwal 1782084)raj vardhan agarwalNo ratings yet

- Chapter 1 Managerial AccountingDocument9 pagesChapter 1 Managerial AccountingApril Pearl VenezuelaNo ratings yet

- Week 1-The Management ProcessDocument16 pagesWeek 1-The Management ProcessRichard Oliver CortezNo ratings yet

- Presentation 001 Management Services Concepts Practices and StandardsDocument33 pagesPresentation 001 Management Services Concepts Practices and StandardsNoe AgubangNo ratings yet

- Module 1 - Basic Concepts in Cost AccountingDocument11 pagesModule 1 - Basic Concepts in Cost AccountingSarah Jane Dulnuan NipahoyNo ratings yet

- Chapter 1 - Managerial Accounting and The Business EnvironmentDocument48 pagesChapter 1 - Managerial Accounting and The Business Environmentahmedemad20452045No ratings yet

- Chapter 01 Overview of Cost Management and StrategyDocument8 pagesChapter 01 Overview of Cost Management and StrategyAccounting MaterialsNo ratings yet

- Lesson 1 - Strategic Cost Management and Management AccountingDocument4 pagesLesson 1 - Strategic Cost Management and Management AccountingBernaNo ratings yet

- Introduction To Managerial AccountingDocument37 pagesIntroduction To Managerial AccountingJINKY BULAHANNo ratings yet

- Introduction To Managerial AccountingDocument37 pagesIntroduction To Managerial AccountingJINKY BULAHANNo ratings yet

- MGT 207Document17 pagesMGT 207Alkhair SangcopanNo ratings yet

- Chp.1. The Manager and Management AccountingDocument16 pagesChp.1. The Manager and Management AccountingLisa FebrianiNo ratings yet

- The Manager and Management Accounting: © 2012 Pearson Education. All Rights ReservedDocument16 pagesThe Manager and Management Accounting: © 2012 Pearson Education. All Rights ReservedMary Haniel Joy ParbaNo ratings yet

- The Accountant's Role in The OrganizationDocument13 pagesThe Accountant's Role in The OrganizationLaraib TajNo ratings yet

- Chapter 3Document78 pagesChapter 3Ashebir AsfawNo ratings yet

- Chapter 1 - How Management Accounting Information Supports Decision MakingDocument13 pagesChapter 1 - How Management Accounting Information Supports Decision MakingReynie Ann Sanchez TolentinoNo ratings yet

- Sess 1Document4 pagesSess 1khanhnguyenfgoNo ratings yet

- 7 E's in Management AccountingDocument18 pages7 E's in Management AccountingLabib Shah100% (2)

- Setting An Audit StrategyDocument14 pagesSetting An Audit Strategyhassanjamil123No ratings yet

- MBA 533 Lecture 1 Introduction To Accounting For ManagersDocument23 pagesMBA 533 Lecture 1 Introduction To Accounting For ManagersTrymore KondeNo ratings yet

- Lect 1 Accounting in BusinessDocument54 pagesLect 1 Accounting in Businessjoeltan111No ratings yet

- Chapter 1 NotesDocument38 pagesChapter 1 NotesHaroon ZaheerNo ratings yet

- Cost AccountingDocument4 pagesCost AccountingAretha Joi Domingo PrezaNo ratings yet

- Unit - 1 CH 1-Managerial Accounting-An OverviewDocument24 pagesUnit - 1 CH 1-Managerial Accounting-An OverviewAkshay KumarNo ratings yet

- CH 1 CostDocument26 pagesCH 1 Costehab kamalNo ratings yet

- Cost & Management AccountingDocument197 pagesCost & Management Accountingmmjmmj100% (1)

- Management ConsultancyDocument150 pagesManagement ConsultancyEagle OrtegaNo ratings yet

- UCP - M - AccountingDocument377 pagesUCP - M - Accountingsara100% (1)

- Fma - 1Document60 pagesFma - 1Hammad QasimNo ratings yet

- 1.1 Evolution of Management Accounting - Part 1Document23 pages1.1 Evolution of Management Accounting - Part 1Dabbie JoyNo ratings yet

- The Balanced Scorecard (Review and Analysis of Kaplan and Norton's Book)From EverandThe Balanced Scorecard (Review and Analysis of Kaplan and Norton's Book)Rating: 4.5 out of 5 stars4.5/5 (3)

- Slides MilesEversonDocument9 pagesSlides MilesEversonSiddharthNo ratings yet

- Cottle-Taylor: Expanding The Oral Care in IndiaDocument9 pagesCottle-Taylor: Expanding The Oral Care in IndiaSiddharthNo ratings yet

- Task A.P. Møller - Group2 PDFDocument12 pagesTask A.P. Møller - Group2 PDFSiddharthNo ratings yet

- How To Build A Talent Pipeline Model: 1. Plan Recruitment According To Business StrategyDocument3 pagesHow To Build A Talent Pipeline Model: 1. Plan Recruitment According To Business StrategySiddharthNo ratings yet

- Talent Pipeline Refers To A Pool of Potential Candidates, Either Company's Employees Who AreDocument3 pagesTalent Pipeline Refers To A Pool of Potential Candidates, Either Company's Employees Who AreSiddharthNo ratings yet

- BRM Session 7 PDFDocument33 pagesBRM Session 7 PDFSiddharthNo ratings yet

- Session 8 & 9 - Sales and Operations Planning Faculty - Dr. CP Garg, IIM RohtakDocument31 pagesSession 8 & 9 - Sales and Operations Planning Faculty - Dr. CP Garg, IIM RohtakSiddharthNo ratings yet

- LL Bean Case WorkingDocument2 pagesLL Bean Case WorkingSiddharthNo ratings yet

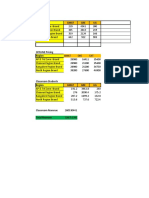

- 0.3 Demand Probability 0.1 60 3% 0 0 110 70 6% 0 0 80 13% 0 0 90 18% 0 0 100 20% 0 0 110 15% 0 0 120 16% 0 0 130 6% 0 140 3% 0Document1 page0.3 Demand Probability 0.1 60 3% 0 0 110 70 6% 0 0 80 13% 0 0 90 18% 0 0 100 20% 0 0 110 15% 0 0 120 16% 0 0 130 6% 0 140 3% 0SiddharthNo ratings yet

- SectionD Group15 Larsen&ToubroDocument8 pagesSectionD Group15 Larsen&ToubroSiddharthNo ratings yet

- Single Truck 400 Common Ordering Cost 350 Product Specific Cost 50 Product Cost/pound 1 Holding Cost 0.25Document10 pagesSingle Truck 400 Common Ordering Cost 350 Product Specific Cost 50 Product Cost/pound 1 Holding Cost 0.25SiddharthNo ratings yet

- MoonchemDocument4 pagesMoonchemSiddharthNo ratings yet

- 2Document4 pages2SiddharthNo ratings yet

- Region Gmat GRE UGDocument9 pagesRegion Gmat GRE UGSiddharthNo ratings yet

- 2Document4 pages2SiddharthNo ratings yet

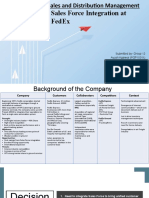

- Sales Force Integration at Fedex: Sales and Distribution ManagementDocument7 pagesSales Force Integration at Fedex: Sales and Distribution ManagementSiddharthNo ratings yet

- ComparisonDocument10 pagesComparisonSiddharthNo ratings yet

- IELTSDocument4 pagesIELTSSiddharthNo ratings yet

- Ma Excel CLVDocument2 pagesMa Excel CLVSiddharthNo ratings yet

- Ielts Prep: Edx - Plan1 Edx - Plan2Document14 pagesIelts Prep: Edx - Plan1 Edx - Plan2SiddharthNo ratings yet

- Essay Outline TemplateDocument7 pagesEssay Outline Templatefadelin50No ratings yet

- Doing Business in Egypt PDFDocument47 pagesDoing Business in Egypt PDFMohammed Abdul HadyNo ratings yet

- Kualitas Pelayanan Pramusaji Terhadap Kepuasan Tamu Di Restoran Cashmere Aston Solo HotelDocument7 pagesKualitas Pelayanan Pramusaji Terhadap Kepuasan Tamu Di Restoran Cashmere Aston Solo HotelRahulNo ratings yet

- Assessing The Digital Transformation Maturity of Motherboard Industry: A Fuzzy AHP ApproachDocument15 pagesAssessing The Digital Transformation Maturity of Motherboard Industry: A Fuzzy AHP ApproachBOHR International Journal of Finance and Market Research (BIJFMR)No ratings yet

- BSHRM Thesis SampleDocument8 pagesBSHRM Thesis Samplegbww46x7100% (2)

- Group-2-Group Assignment-2-ColpalDocument13 pagesGroup-2-Group Assignment-2-ColpalPushan MaitiNo ratings yet

- 14854/MARUDHAR EXP Sleeper Class (SL)Document2 pages14854/MARUDHAR EXP Sleeper Class (SL)Mohan ramNo ratings yet

- Practical Research 2 2Document28 pagesPractical Research 2 2Alian BarrogaNo ratings yet

- DLTA Laporan Keuangan 18 19Document91 pagesDLTA Laporan Keuangan 18 19Fazrin SetiawanNo ratings yet

- AC2104 - Seminar 5Document3 pagesAC2104 - Seminar 5Rachel LiuNo ratings yet

- 2022notice - MDF Email Submission 1Document1 page2022notice - MDF Email Submission 1ElaNo ratings yet

- What Does Economics Have To Do With Running A BusinessDocument13 pagesWhat Does Economics Have To Do With Running A Businesswalsonsanaani3rdNo ratings yet

- Customised Profit & Loss (Rs - in Crores) Mar 18 17-Mar 16-Mar 15-Mar 14-Mar 5,592.29 5,290.65 5,750.00 5,431.28 4,870.08Document20 pagesCustomised Profit & Loss (Rs - in Crores) Mar 18 17-Mar 16-Mar 15-Mar 14-Mar 5,592.29 5,290.65 5,750.00 5,431.28 4,870.08Akshay Yadav Student, Jaipuria LucknowNo ratings yet

- Labor Law - Prof. PanganibanDocument10 pagesLabor Law - Prof. Panganibandayve dacanay100% (1)

- Chapter 3 - Strategy in Marketing ChannelsDocument41 pagesChapter 3 - Strategy in Marketing ChannelsDr-Mohammad Yousef Alhashaiesha100% (1)

- Corporate KycDocument24 pagesCorporate KycJamaluddin SaidNo ratings yet

- Operations Strategymod1Document209 pagesOperations Strategymod1Siddharth MohapatraNo ratings yet

- Equity Table2 998e2e768fDocument53 pagesEquity Table2 998e2e768fHouse GardenNo ratings yet

- Specialized Government BanksDocument5 pagesSpecialized Government BanksCarazelli AysonNo ratings yet

- Dbm-Roii-Letter of Resignation of MS Maria Roanne A BaccayDocument10 pagesDbm-Roii-Letter of Resignation of MS Maria Roanne A BaccayJale Ann A. EspañolNo ratings yet

- SADOR'S COMPANY TerbaikDocument37 pagesSADOR'S COMPANY TerbaikHariz BukhariNo ratings yet

- Trung Nguyen CompanyDocument1 pageTrung Nguyen CompanyLinh Phạm BảoNo ratings yet

- Theories of FirmDocument30 pagesTheories of FirmAnup kattelNo ratings yet

- AzSPU SSOW Procedure For Task Risk AssessmentDocument34 pagesAzSPU SSOW Procedure For Task Risk AssessmentAmir M. ShaikhNo ratings yet

- ROD of Keya CosmeticsDocument71 pagesROD of Keya Cosmeticsrash_sblNo ratings yet

- Australasian Intercultural Cities Workshop Report 23 1 2019 FINAL PDFDocument11 pagesAustralasian Intercultural Cities Workshop Report 23 1 2019 FINAL PDFAAMIRNo ratings yet

- Ci Framework Oct21dfDocument63 pagesCi Framework Oct21dfapi-595803157No ratings yet