Assignment On Presentment Under Negotiable Instruments

Assignment On Presentment Under Negotiable Instruments

You might also like

- Research Project 2 On Indigo AirlinesDocument13 pagesResearch Project 2 On Indigo AirlinesNaresh Reddy100% (3)

- Counter ClaimDocument11 pagesCounter ClaimAkash RoyNo ratings yet

- Dishonour of Negotiable Instruments PDFDocument33 pagesDishonour of Negotiable Instruments PDFabhisheknnd312100% (3)

- Presentment of Negotiable InstrumentDocument16 pagesPresentment of Negotiable InstrumentRahul Paliya83% (6)

- PDF4687 Discretionary Trust Settlor IncludedDocument12 pagesPDF4687 Discretionary Trust Settlor IncludedShashank DubeyNo ratings yet

- Mukul Internship ReportDocument15 pagesMukul Internship ReportMukul BajajNo ratings yet

- GMAT Crititcal Reasoning (Practice)Document11 pagesGMAT Crititcal Reasoning (Practice)Hương HuỳnhNo ratings yet

- Chap 007Document19 pagesChap 007charlie simoNo ratings yet

- Negotiable Instruments Act 1881Document9 pagesNegotiable Instruments Act 1881Istakhar AlamNo ratings yet

- The Negotiable Instruments Act 1881Document119 pagesThe Negotiable Instruments Act 1881Sunayana GuptaNo ratings yet

- Contract Law Specific Relief ActDocument9 pagesContract Law Specific Relief ActLeina Suren100% (1)

- 95093negotiable Instrument ActDocument60 pages95093negotiable Instrument ActIshan BramhbhattNo ratings yet

- Perpetual Injunction When Granted and When Refused: MR.M Suneel Kumar Senior Civil Judge SompetaDocument29 pagesPerpetual Injunction When Granted and When Refused: MR.M Suneel Kumar Senior Civil Judge Sompetakrishna reddyNo ratings yet

- Negotiable Instruments - Dishonour and Discharge - Group VDocument56 pagesNegotiable Instruments - Dishonour and Discharge - Group VSaurabh PatelNo ratings yet

- Holder & Holder in Due CourseDocument1 pageHolder & Holder in Due Courserohansinha77No ratings yet

- Legal Maxims Second Year PDFDocument7 pagesLegal Maxims Second Year PDFBhavya KohliNo ratings yet

- Registration Act 1908Document65 pagesRegistration Act 1908Gopi KumaramNo ratings yet

- Actions and Remedies For Dealing With InfringementDocument11 pagesActions and Remedies For Dealing With InfringementgivamathanNo ratings yet

- Offer or Tender of PerformanceDocument7 pagesOffer or Tender of PerformanceWeiNo ratings yet

- Negotiable Instrument ActDocument18 pagesNegotiable Instrument ActmahendrabpatelNo ratings yet

- Capacity To ContractDocument33 pagesCapacity To ContractAbhay MalikNo ratings yet

- Counter Claims in Civil SuitsDocument7 pagesCounter Claims in Civil SuitsAmita SinwarNo ratings yet

- Indian Stamp Act, 1899Document27 pagesIndian Stamp Act, 1899Cliffton KinnyNo ratings yet

- Quo Warranto FinalDocument23 pagesQuo Warranto FinalSameeksha XalxoNo ratings yet

- Holder in Due CourseDocument4 pagesHolder in Due CourseMuskan TandonNo ratings yet

- Introduction To Transfer of Property ActDocument16 pagesIntroduction To Transfer of Property ActakhilNo ratings yet

- What Is Specific PerformanceDocument6 pagesWhat Is Specific PerformanceZeeshan Ahmed QaziNo ratings yet

- Demand Promissory Note PDFDocument1 pageDemand Promissory Note PDFDexter Chua100% (1)

- 128 SuretyDocument11 pages128 SuretyNitya Nand Pandey100% (1)

- Law On Stamp Duty and Registration - Sri B Shiva Sankar RaoDocument47 pagesLaw On Stamp Duty and Registration - Sri B Shiva Sankar RaoPerumbhudurumaruNo ratings yet

- Arbitration Assn Application SATCOMM911Document8 pagesArbitration Assn Application SATCOMM911CK in DC0% (1)

- 2.1 Offer: INDIAN CONTRACT ACT 1872: OFFER Business RegulationsDocument3 pages2.1 Offer: INDIAN CONTRACT ACT 1872: OFFER Business Regulationskarthik karthikNo ratings yet

- Civil Procedure Code - Written Statement, Set-Off & Counter ClaimDocument4 pagesCivil Procedure Code - Written Statement, Set-Off & Counter ClaimMuhammadImranIrshadNo ratings yet

- Equity PrototypeDocument17 pagesEquity PrototypeMugambo MirzyaNo ratings yet

- Promisory Note: Unit - 2 BY Prof. Thaseen Sultana GFGC Frazer Town, BangaloreDocument12 pagesPromisory Note: Unit - 2 BY Prof. Thaseen Sultana GFGC Frazer Town, BangaloreThaseen SultanaNo ratings yet

- Notes ConsiderationDocument5 pagesNotes Consideration3D StormNo ratings yet

- Limitation ActDocument28 pagesLimitation ActHuzefa Mannan DohadwalaNo ratings yet

- Banking Law and PracticeDocument59 pagesBanking Law and PracticeThanga Durai100% (2)

- Rules of EquityDocument15 pagesRules of EquityKirti SoniNo ratings yet

- Module 2 (B) Promissory Note: Negotiable Instruments Act (Module 2B) The LAW LearnersDocument5 pagesModule 2 (B) Promissory Note: Negotiable Instruments Act (Module 2B) The LAW LearnersAbhishek100% (1)

- "Debenture Trustee" - Position, Powers and Duties - It Is The LawDocument13 pages"Debenture Trustee" - Position, Powers and Duties - It Is The LawRohitSharmaNo ratings yet

- The Rights of The Banker IncludeDocument5 pagesThe Rights of The Banker Includem_dattaias67% (3)

- Rules Under The Indian Stamp Act, 1899 PreliminaryDocument58 pagesRules Under The Indian Stamp Act, 1899 PreliminaryMohan BabuNo ratings yet

- Discharge of ContractDocument16 pagesDischarge of ContractBarun GuptaNo ratings yet

- Law of Banking ProjectDocument20 pagesLaw of Banking ProjectUday ReddyNo ratings yet

- Chapter 11 - 15 PDFDocument83 pagesChapter 11 - 15 PDFNusrat ShatyNo ratings yet

- ConveyanceDocument3 pagesConveyanceAnushree MahindraNo ratings yet

- Specific Contract Full Notes - 231011 - 192140Document150 pagesSpecific Contract Full Notes - 231011 - 192140Sereena C SNo ratings yet

- The Sales of Goods Act (1930)Document44 pagesThe Sales of Goods Act (1930)swatishetNo ratings yet

- (B-4) Bills of Exchange ActDocument67 pages(B-4) Bills of Exchange ActJoy100% (1)

- Negotiable Instrument Act, 1881Document25 pagesNegotiable Instrument Act, 1881Garima100% (1)

- Bona Fide Purchaser CaselawDocument5 pagesBona Fide Purchaser CaselawShehzad Haider100% (1)

- Instantaneous ContractsDocument19 pagesInstantaneous ContractsParikshit100% (1)

- CreditCardCreditAgreement 1323-28042013Document7 pagesCreditCardCreditAgreement 1323-28042013Fabian DeeNo ratings yet

- Unit - 1: Contract LawDocument56 pagesUnit - 1: Contract LawPremendra SahuNo ratings yet

- Promissory Note PDFDocument3 pagesPromissory Note PDFDeonandan kumarNo ratings yet

- Dishonour of Negotiable InstrumentDocument10 pagesDishonour of Negotiable Instrumentvishal bagariaNo ratings yet

- Banker Customer RelationshipDocument7 pagesBanker Customer RelationshipPadmasree HarishNo ratings yet

- Joinder of ChargesDocument2 pagesJoinder of ChargesEvening Folks TeamNo ratings yet

- Mercantile LawDocument37 pagesMercantile LawskrzakNo ratings yet

- Notice of DefaultDocument3 pagesNotice of DefaultMilos RandjelovicNo ratings yet

- A Treatise on Fraudulent Conveyances and Creditors' Bills: With a Discussion of Void and Voidable ActsFrom EverandA Treatise on Fraudulent Conveyances and Creditors' Bills: With a Discussion of Void and Voidable ActsRating: 1 out of 5 stars1/5 (1)

- The Declaration of Independence: A Play for Many ReadersFrom EverandThe Declaration of Independence: A Play for Many ReadersNo ratings yet

- Negotiable Instruments 12 08052023 085138pmDocument27 pagesNegotiable Instruments 12 08052023 085138pmMeraj Ali100% (2)

- Manu/sc/0181/1958 Manu/sc/0821/1996 Manu/sc/0327/1964 Manu/sc/0003/1958 Manu/sc/0085/1956Document68 pagesManu/sc/0181/1958 Manu/sc/0821/1996 Manu/sc/0327/1964 Manu/sc/0003/1958 Manu/sc/0085/1956Mukul BajajNo ratings yet

- Sec 25 HmaDocument3 pagesSec 25 HmaMukul BajajNo ratings yet

- NF - WWI - Treaty of VersaillesDocument39 pagesNF - WWI - Treaty of VersaillesMukul BajajNo ratings yet

- PDM Sompeta-Dt07122019Document8 pagesPDM Sompeta-Dt07122019Mukul BajajNo ratings yet

- MsBarbensRevisedEditedNoPoliticalCartoonsTreaty of VersaillesDocument134 pagesMsBarbensRevisedEditedNoPoliticalCartoonsTreaty of VersaillesMukul BajajNo ratings yet

- 6 The Treaty of VersaillesDocument18 pages6 The Treaty of VersaillesMukul BajajNo ratings yet

- Treaty of Versailles NotesDocument28 pagesTreaty of Versailles NotesMukul BajajNo ratings yet

- A Project Report On - "Online Dispue Resolution in India" Manipal University JaipurDocument12 pagesA Project Report On - "Online Dispue Resolution in India" Manipal University JaipurMukul Bajaj100% (1)

- Treaty of VersaillesDocument20 pagesTreaty of VersaillesMukul BajajNo ratings yet

- A Project Report On - "Locard'S Principle of Exchange" Manipal University JaipurDocument12 pagesA Project Report On - "Locard'S Principle of Exchange" Manipal University JaipurMukul BajajNo ratings yet

- Annexure II PDFDocument1 pageAnnexure II PDFMukul BajajNo ratings yet

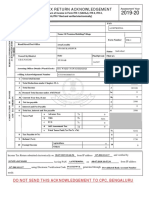

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruMukul BajajNo ratings yet

- (Pursuing 4 Year of The B.A./LL.B. (Hons.) Course) : Mail D Hone ODocument3 pages(Pursuing 4 Year of The B.A./LL.B. (Hons.) Course) : Mail D Hone OMukul BajajNo ratings yet

- Gautam Forensic ScienceDocument14 pagesGautam Forensic ScienceMukul BajajNo ratings yet

- Happy Forging Training Report by Dipankar AroraDocument4 pagesHappy Forging Training Report by Dipankar AroraMukul BajajNo ratings yet

- Application Transcripts MUKULDocument2 pagesApplication Transcripts MUKULMukul BajajNo ratings yet

- Mukul CPC ProjectDocument15 pagesMukul CPC ProjectMukul BajajNo ratings yet

- Cases of PresentmentDocument1 pageCases of PresentmentMukul BajajNo ratings yet

- Armed Forces Special Power ActDocument14 pagesArmed Forces Special Power ActMukul BajajNo ratings yet

- Online Payment Receipt For Returning Students (2019-20) : Ref. No. (University Roll No) 2018MCA2020Document3 pagesOnline Payment Receipt For Returning Students (2019-20) : Ref. No. (University Roll No) 2018MCA2020Mukul BajajNo ratings yet

- Caa ExplainedDocument8 pagesCaa ExplainedMukul BajajNo ratings yet

- Application Transcripts ARPITDocument2 pagesApplication Transcripts ARPITMukul BajajNo ratings yet

- Bureau Veritas BrochureDocument7 pagesBureau Veritas BrochureAnonyNo ratings yet

- Office of The Controller of Examinations Anna University, Chennai - 600 025 Application For Issue of Duplicate CertificateDocument3 pagesOffice of The Controller of Examinations Anna University, Chennai - 600 025 Application For Issue of Duplicate CertificatevinithaNo ratings yet

- Beams11 ppt05Document39 pagesBeams11 ppt05Christian TambunanNo ratings yet

- Lotrene LLDPE Datasheet PDFDocument6 pagesLotrene LLDPE Datasheet PDFThụy Thảo LinhNo ratings yet

- Terms and Conditions: Service Plan SummaryDocument1 pageTerms and Conditions: Service Plan Summarypallavbadhiyal13100% (1)

- 4th Generation MaintenanceDocument11 pages4th Generation MaintenancesharmasourabhNo ratings yet

- Proposal For QMS Consultancy Services - EKO AtlanticDocument7 pagesProposal For QMS Consultancy Services - EKO AtlanticGeorges Abi JaoudeNo ratings yet

- Triumph Handbook July 2013Document43 pagesTriumph Handbook July 2013JovanNo ratings yet

- SOCAP 10th Anniversary BookletDocument84 pagesSOCAP 10th Anniversary BookletSocial Capital Markets100% (1)

- Innerwear Industry Pitch PresentationDocument19 pagesInnerwear Industry Pitch PresentationRupeshKumarNo ratings yet

- The Differences Between Management and LeadershipDocument10 pagesThe Differences Between Management and LeadershipShairel GesimNo ratings yet

- Event Program - 2010 Ypulse Youth Marketing MashupDocument31 pagesEvent Program - 2010 Ypulse Youth Marketing MashupDerek E. BairdNo ratings yet

- BRM Module 2 CGDocument7 pagesBRM Module 2 CGsudharshan235No ratings yet

- أهمية تحليل الهيكل المالي في تقييم الأداء المالي لمؤسسة باتيميتال بولاية عين دفلى لفترة 2015 2017Document20 pagesأهمية تحليل الهيكل المالي في تقييم الأداء المالي لمؤسسة باتيميتال بولاية عين دفلى لفترة 2015 2017d5tjb9gvpmNo ratings yet

- 5.2 Manajemen OrganisasiDocument12 pages5.2 Manajemen OrganisasiMochammad HafizhNo ratings yet

- CAF Gasket Removal ManualDocument3 pagesCAF Gasket Removal Manualgirish_motiyaniNo ratings yet

- Problem (Orange Peel & Dented)Document2 pagesProblem (Orange Peel & Dented)Marketing TanajawaNo ratings yet

- ASCandidate Application FormDocument1 pageASCandidate Application FormShubHam DiMriNo ratings yet

- Steel BCGDocument40 pagesSteel BCGBinod Kumar PadhiNo ratings yet

- Importing, Exporting, and Sourcing: Global MarketingDocument28 pagesImporting, Exporting, and Sourcing: Global MarketingÖmer DoganNo ratings yet

- Internship Report (3)Document3 pagesInternship Report (3)Saqib LiaqatNo ratings yet

- Tugas Bahasa Inggris Hukum: Nama: Herdini Juliyani NPM: 1900874201314 Dosen Pengampu: Yanti Ismiyati,,S.Pd.,M.PdDocument4 pagesTugas Bahasa Inggris Hukum: Nama: Herdini Juliyani NPM: 1900874201314 Dosen Pengampu: Yanti Ismiyati,,S.Pd.,M.PdCakra ChandrascaNo ratings yet

- Chapter 1 - History of CooperativesDocument9 pagesChapter 1 - History of CooperativesAlzcareen Erie LiwayanNo ratings yet

- Tommy Hilfiger VM FinalDocument26 pagesTommy Hilfiger VM Finalkartika ranaNo ratings yet

- Appendix 37 - Instructions - CBRegDocument1 pageAppendix 37 - Instructions - CBRegabbey89No ratings yet

- Redemption FormDocument1 pageRedemption FormHema LatthaNo ratings yet

- Chem PoemDocument2 pagesChem PoemEthan MamarNo ratings yet

Download as docx, pdf, or txt

You might also like

- Research Project 2 On Indigo AirlinesDocument13 pagesResearch Project 2 On Indigo AirlinesNaresh Reddy100% (3)

- Counter ClaimDocument11 pagesCounter ClaimAkash RoyNo ratings yet

- Dishonour of Negotiable Instruments PDFDocument33 pagesDishonour of Negotiable Instruments PDFabhisheknnd312100% (3)

- Presentment of Negotiable InstrumentDocument16 pagesPresentment of Negotiable InstrumentRahul Paliya83% (6)

- PDF4687 Discretionary Trust Settlor IncludedDocument12 pagesPDF4687 Discretionary Trust Settlor IncludedShashank DubeyNo ratings yet

- Mukul Internship ReportDocument15 pagesMukul Internship ReportMukul BajajNo ratings yet

- GMAT Crititcal Reasoning (Practice)Document11 pagesGMAT Crititcal Reasoning (Practice)Hương HuỳnhNo ratings yet

- Chap 007Document19 pagesChap 007charlie simoNo ratings yet

- Negotiable Instruments Act 1881Document9 pagesNegotiable Instruments Act 1881Istakhar AlamNo ratings yet

- The Negotiable Instruments Act 1881Document119 pagesThe Negotiable Instruments Act 1881Sunayana GuptaNo ratings yet

- Contract Law Specific Relief ActDocument9 pagesContract Law Specific Relief ActLeina Suren100% (1)

- 95093negotiable Instrument ActDocument60 pages95093negotiable Instrument ActIshan BramhbhattNo ratings yet

- Perpetual Injunction When Granted and When Refused: MR.M Suneel Kumar Senior Civil Judge SompetaDocument29 pagesPerpetual Injunction When Granted and When Refused: MR.M Suneel Kumar Senior Civil Judge Sompetakrishna reddyNo ratings yet

- Negotiable Instruments - Dishonour and Discharge - Group VDocument56 pagesNegotiable Instruments - Dishonour and Discharge - Group VSaurabh PatelNo ratings yet

- Holder & Holder in Due CourseDocument1 pageHolder & Holder in Due Courserohansinha77No ratings yet

- Legal Maxims Second Year PDFDocument7 pagesLegal Maxims Second Year PDFBhavya KohliNo ratings yet

- Registration Act 1908Document65 pagesRegistration Act 1908Gopi KumaramNo ratings yet

- Actions and Remedies For Dealing With InfringementDocument11 pagesActions and Remedies For Dealing With InfringementgivamathanNo ratings yet

- Offer or Tender of PerformanceDocument7 pagesOffer or Tender of PerformanceWeiNo ratings yet

- Negotiable Instrument ActDocument18 pagesNegotiable Instrument ActmahendrabpatelNo ratings yet

- Capacity To ContractDocument33 pagesCapacity To ContractAbhay MalikNo ratings yet

- Counter Claims in Civil SuitsDocument7 pagesCounter Claims in Civil SuitsAmita SinwarNo ratings yet

- Indian Stamp Act, 1899Document27 pagesIndian Stamp Act, 1899Cliffton KinnyNo ratings yet

- Quo Warranto FinalDocument23 pagesQuo Warranto FinalSameeksha XalxoNo ratings yet

- Holder in Due CourseDocument4 pagesHolder in Due CourseMuskan TandonNo ratings yet

- Introduction To Transfer of Property ActDocument16 pagesIntroduction To Transfer of Property ActakhilNo ratings yet

- What Is Specific PerformanceDocument6 pagesWhat Is Specific PerformanceZeeshan Ahmed QaziNo ratings yet

- Demand Promissory Note PDFDocument1 pageDemand Promissory Note PDFDexter Chua100% (1)

- 128 SuretyDocument11 pages128 SuretyNitya Nand Pandey100% (1)

- Law On Stamp Duty and Registration - Sri B Shiva Sankar RaoDocument47 pagesLaw On Stamp Duty and Registration - Sri B Shiva Sankar RaoPerumbhudurumaruNo ratings yet

- Arbitration Assn Application SATCOMM911Document8 pagesArbitration Assn Application SATCOMM911CK in DC0% (1)

- 2.1 Offer: INDIAN CONTRACT ACT 1872: OFFER Business RegulationsDocument3 pages2.1 Offer: INDIAN CONTRACT ACT 1872: OFFER Business Regulationskarthik karthikNo ratings yet

- Civil Procedure Code - Written Statement, Set-Off & Counter ClaimDocument4 pagesCivil Procedure Code - Written Statement, Set-Off & Counter ClaimMuhammadImranIrshadNo ratings yet

- Equity PrototypeDocument17 pagesEquity PrototypeMugambo MirzyaNo ratings yet

- Promisory Note: Unit - 2 BY Prof. Thaseen Sultana GFGC Frazer Town, BangaloreDocument12 pagesPromisory Note: Unit - 2 BY Prof. Thaseen Sultana GFGC Frazer Town, BangaloreThaseen SultanaNo ratings yet

- Notes ConsiderationDocument5 pagesNotes Consideration3D StormNo ratings yet

- Limitation ActDocument28 pagesLimitation ActHuzefa Mannan DohadwalaNo ratings yet

- Banking Law and PracticeDocument59 pagesBanking Law and PracticeThanga Durai100% (2)

- Rules of EquityDocument15 pagesRules of EquityKirti SoniNo ratings yet

- Module 2 (B) Promissory Note: Negotiable Instruments Act (Module 2B) The LAW LearnersDocument5 pagesModule 2 (B) Promissory Note: Negotiable Instruments Act (Module 2B) The LAW LearnersAbhishek100% (1)

- "Debenture Trustee" - Position, Powers and Duties - It Is The LawDocument13 pages"Debenture Trustee" - Position, Powers and Duties - It Is The LawRohitSharmaNo ratings yet

- The Rights of The Banker IncludeDocument5 pagesThe Rights of The Banker Includem_dattaias67% (3)

- Rules Under The Indian Stamp Act, 1899 PreliminaryDocument58 pagesRules Under The Indian Stamp Act, 1899 PreliminaryMohan BabuNo ratings yet

- Discharge of ContractDocument16 pagesDischarge of ContractBarun GuptaNo ratings yet

- Law of Banking ProjectDocument20 pagesLaw of Banking ProjectUday ReddyNo ratings yet

- Chapter 11 - 15 PDFDocument83 pagesChapter 11 - 15 PDFNusrat ShatyNo ratings yet

- ConveyanceDocument3 pagesConveyanceAnushree MahindraNo ratings yet

- Specific Contract Full Notes - 231011 - 192140Document150 pagesSpecific Contract Full Notes - 231011 - 192140Sereena C SNo ratings yet

- The Sales of Goods Act (1930)Document44 pagesThe Sales of Goods Act (1930)swatishetNo ratings yet

- (B-4) Bills of Exchange ActDocument67 pages(B-4) Bills of Exchange ActJoy100% (1)

- Negotiable Instrument Act, 1881Document25 pagesNegotiable Instrument Act, 1881Garima100% (1)

- Bona Fide Purchaser CaselawDocument5 pagesBona Fide Purchaser CaselawShehzad Haider100% (1)

- Instantaneous ContractsDocument19 pagesInstantaneous ContractsParikshit100% (1)

- CreditCardCreditAgreement 1323-28042013Document7 pagesCreditCardCreditAgreement 1323-28042013Fabian DeeNo ratings yet

- Unit - 1: Contract LawDocument56 pagesUnit - 1: Contract LawPremendra SahuNo ratings yet

- Promissory Note PDFDocument3 pagesPromissory Note PDFDeonandan kumarNo ratings yet

- Dishonour of Negotiable InstrumentDocument10 pagesDishonour of Negotiable Instrumentvishal bagariaNo ratings yet

- Banker Customer RelationshipDocument7 pagesBanker Customer RelationshipPadmasree HarishNo ratings yet

- Joinder of ChargesDocument2 pagesJoinder of ChargesEvening Folks TeamNo ratings yet

- Mercantile LawDocument37 pagesMercantile LawskrzakNo ratings yet

- Notice of DefaultDocument3 pagesNotice of DefaultMilos RandjelovicNo ratings yet

- A Treatise on Fraudulent Conveyances and Creditors' Bills: With a Discussion of Void and Voidable ActsFrom EverandA Treatise on Fraudulent Conveyances and Creditors' Bills: With a Discussion of Void and Voidable ActsRating: 1 out of 5 stars1/5 (1)

- The Declaration of Independence: A Play for Many ReadersFrom EverandThe Declaration of Independence: A Play for Many ReadersNo ratings yet

- Negotiable Instruments 12 08052023 085138pmDocument27 pagesNegotiable Instruments 12 08052023 085138pmMeraj Ali100% (2)

- Manu/sc/0181/1958 Manu/sc/0821/1996 Manu/sc/0327/1964 Manu/sc/0003/1958 Manu/sc/0085/1956Document68 pagesManu/sc/0181/1958 Manu/sc/0821/1996 Manu/sc/0327/1964 Manu/sc/0003/1958 Manu/sc/0085/1956Mukul BajajNo ratings yet

- Sec 25 HmaDocument3 pagesSec 25 HmaMukul BajajNo ratings yet

- NF - WWI - Treaty of VersaillesDocument39 pagesNF - WWI - Treaty of VersaillesMukul BajajNo ratings yet

- PDM Sompeta-Dt07122019Document8 pagesPDM Sompeta-Dt07122019Mukul BajajNo ratings yet

- MsBarbensRevisedEditedNoPoliticalCartoonsTreaty of VersaillesDocument134 pagesMsBarbensRevisedEditedNoPoliticalCartoonsTreaty of VersaillesMukul BajajNo ratings yet

- 6 The Treaty of VersaillesDocument18 pages6 The Treaty of VersaillesMukul BajajNo ratings yet

- Treaty of Versailles NotesDocument28 pagesTreaty of Versailles NotesMukul BajajNo ratings yet

- A Project Report On - "Online Dispue Resolution in India" Manipal University JaipurDocument12 pagesA Project Report On - "Online Dispue Resolution in India" Manipal University JaipurMukul Bajaj100% (1)

- Treaty of VersaillesDocument20 pagesTreaty of VersaillesMukul BajajNo ratings yet

- A Project Report On - "Locard'S Principle of Exchange" Manipal University JaipurDocument12 pagesA Project Report On - "Locard'S Principle of Exchange" Manipal University JaipurMukul BajajNo ratings yet

- Annexure II PDFDocument1 pageAnnexure II PDFMukul BajajNo ratings yet

- Indian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruDocument1 pageIndian Income Tax Return Acknowledgement: Do Not Send This Acknowledgement To CPC, BengaluruMukul BajajNo ratings yet

- (Pursuing 4 Year of The B.A./LL.B. (Hons.) Course) : Mail D Hone ODocument3 pages(Pursuing 4 Year of The B.A./LL.B. (Hons.) Course) : Mail D Hone OMukul BajajNo ratings yet

- Gautam Forensic ScienceDocument14 pagesGautam Forensic ScienceMukul BajajNo ratings yet

- Happy Forging Training Report by Dipankar AroraDocument4 pagesHappy Forging Training Report by Dipankar AroraMukul BajajNo ratings yet

- Application Transcripts MUKULDocument2 pagesApplication Transcripts MUKULMukul BajajNo ratings yet

- Mukul CPC ProjectDocument15 pagesMukul CPC ProjectMukul BajajNo ratings yet

- Cases of PresentmentDocument1 pageCases of PresentmentMukul BajajNo ratings yet

- Armed Forces Special Power ActDocument14 pagesArmed Forces Special Power ActMukul BajajNo ratings yet

- Online Payment Receipt For Returning Students (2019-20) : Ref. No. (University Roll No) 2018MCA2020Document3 pagesOnline Payment Receipt For Returning Students (2019-20) : Ref. No. (University Roll No) 2018MCA2020Mukul BajajNo ratings yet

- Caa ExplainedDocument8 pagesCaa ExplainedMukul BajajNo ratings yet

- Application Transcripts ARPITDocument2 pagesApplication Transcripts ARPITMukul BajajNo ratings yet

- Bureau Veritas BrochureDocument7 pagesBureau Veritas BrochureAnonyNo ratings yet

- Office of The Controller of Examinations Anna University, Chennai - 600 025 Application For Issue of Duplicate CertificateDocument3 pagesOffice of The Controller of Examinations Anna University, Chennai - 600 025 Application For Issue of Duplicate CertificatevinithaNo ratings yet

- Beams11 ppt05Document39 pagesBeams11 ppt05Christian TambunanNo ratings yet

- Lotrene LLDPE Datasheet PDFDocument6 pagesLotrene LLDPE Datasheet PDFThụy Thảo LinhNo ratings yet

- Terms and Conditions: Service Plan SummaryDocument1 pageTerms and Conditions: Service Plan Summarypallavbadhiyal13100% (1)

- 4th Generation MaintenanceDocument11 pages4th Generation MaintenancesharmasourabhNo ratings yet

- Proposal For QMS Consultancy Services - EKO AtlanticDocument7 pagesProposal For QMS Consultancy Services - EKO AtlanticGeorges Abi JaoudeNo ratings yet

- Triumph Handbook July 2013Document43 pagesTriumph Handbook July 2013JovanNo ratings yet

- SOCAP 10th Anniversary BookletDocument84 pagesSOCAP 10th Anniversary BookletSocial Capital Markets100% (1)

- Innerwear Industry Pitch PresentationDocument19 pagesInnerwear Industry Pitch PresentationRupeshKumarNo ratings yet

- The Differences Between Management and LeadershipDocument10 pagesThe Differences Between Management and LeadershipShairel GesimNo ratings yet

- Event Program - 2010 Ypulse Youth Marketing MashupDocument31 pagesEvent Program - 2010 Ypulse Youth Marketing MashupDerek E. BairdNo ratings yet

- BRM Module 2 CGDocument7 pagesBRM Module 2 CGsudharshan235No ratings yet

- أهمية تحليل الهيكل المالي في تقييم الأداء المالي لمؤسسة باتيميتال بولاية عين دفلى لفترة 2015 2017Document20 pagesأهمية تحليل الهيكل المالي في تقييم الأداء المالي لمؤسسة باتيميتال بولاية عين دفلى لفترة 2015 2017d5tjb9gvpmNo ratings yet

- 5.2 Manajemen OrganisasiDocument12 pages5.2 Manajemen OrganisasiMochammad HafizhNo ratings yet

- CAF Gasket Removal ManualDocument3 pagesCAF Gasket Removal Manualgirish_motiyaniNo ratings yet

- Problem (Orange Peel & Dented)Document2 pagesProblem (Orange Peel & Dented)Marketing TanajawaNo ratings yet

- ASCandidate Application FormDocument1 pageASCandidate Application FormShubHam DiMriNo ratings yet

- Steel BCGDocument40 pagesSteel BCGBinod Kumar PadhiNo ratings yet

- Importing, Exporting, and Sourcing: Global MarketingDocument28 pagesImporting, Exporting, and Sourcing: Global MarketingÖmer DoganNo ratings yet

- Internship Report (3)Document3 pagesInternship Report (3)Saqib LiaqatNo ratings yet

- Tugas Bahasa Inggris Hukum: Nama: Herdini Juliyani NPM: 1900874201314 Dosen Pengampu: Yanti Ismiyati,,S.Pd.,M.PdDocument4 pagesTugas Bahasa Inggris Hukum: Nama: Herdini Juliyani NPM: 1900874201314 Dosen Pengampu: Yanti Ismiyati,,S.Pd.,M.PdCakra ChandrascaNo ratings yet

- Chapter 1 - History of CooperativesDocument9 pagesChapter 1 - History of CooperativesAlzcareen Erie LiwayanNo ratings yet

- Tommy Hilfiger VM FinalDocument26 pagesTommy Hilfiger VM Finalkartika ranaNo ratings yet

- Appendix 37 - Instructions - CBRegDocument1 pageAppendix 37 - Instructions - CBRegabbey89No ratings yet

- Redemption FormDocument1 pageRedemption FormHema LatthaNo ratings yet

- Chem PoemDocument2 pagesChem PoemEthan MamarNo ratings yet