Download as docx, pdf, or txt

You might also like

- Comments On Past Exam Question PracticeDocument9 pagesComments On Past Exam Question Practicetcqing1012No ratings yet

- Buckwold 21e - CH 7 Selected SolutionsDocument41 pagesBuckwold 21e - CH 7 Selected SolutionsLucy100% (1)

- Solutions Manual For Principles of Taxation For Business and Investment Planning 2024 27th Edition by Jones, Rhoades-Catanach, Callaghan, KubickDocument7 pagesSolutions Manual For Principles of Taxation For Business and Investment Planning 2024 27th Edition by Jones, Rhoades-Catanach, Callaghan, KubickDiya ReddyNo ratings yet

- Chapter 05 SolutionsDocument7 pagesChapter 05 SolutionsShahnawaz KhanNo ratings yet

- CH 4 & 5 Extra Practic Summer 2023Document9 pagesCH 4 & 5 Extra Practic Summer 2023Ruth KatakaNo ratings yet

- Manto Ke 100 Behtreen Afsane PDFDocument1,320 pagesManto Ke 100 Behtreen Afsane PDFhidayatk_1390% (52)

- ACC 430 Chapter 17Document13 pagesACC 430 Chapter 17vikkiNo ratings yet

- Dissertation Employee Tracking SystemDocument50 pagesDissertation Employee Tracking Systemtanmay agrawal50% (2)

- BT 211 Module 05 1Document12 pagesBT 211 Module 05 1Franz PampolinaNo ratings yet

- Law AssessmentDocument8 pagesLaw AssessmentHina MubarakNo ratings yet

- AICPA - CPA Reg 2017Document12 pagesAICPA - CPA Reg 2017Gene'sNo ratings yet

- Taxation Law 1 Compiled QuestionsDocument4 pagesTaxation Law 1 Compiled QuestionsTiffany HuntNo ratings yet

- Chapter 3 - Investment IncomeDocument26 pagesChapter 3 - Investment IncomeRyan YangNo ratings yet

- South Western Federal Taxation 2016 Essentials of Taxation Individuals and Business Entities 19th Edition Raabe Solutions ManualDocument44 pagesSouth Western Federal Taxation 2016 Essentials of Taxation Individuals and Business Entities 19th Edition Raabe Solutions Manualvernier.decyliclnn4100% (25)

- SolutionsDocument23 pagesSolutionsapi-3817072No ratings yet

- TaxationDocument7 pagesTaxationRahul Singh DeoNo ratings yet

- South-Western Federal Taxation 2016 Individual Income Taxes 39th Edition Hoffman Solutions Manual 1Document26 pagesSouth-Western Federal Taxation 2016 Individual Income Taxes 39th Edition Hoffman Solutions Manual 1alisha100% (53)

- South Western Federal Taxation 2016 Individual Income Taxes 39Th Edition Hoffman Solutions Manual Full Chapter PDFDocument36 pagesSouth Western Federal Taxation 2016 Individual Income Taxes 39Th Edition Hoffman Solutions Manual Full Chapter PDFfred.henderson352100% (12)

- Fabm 12 Q2 1002 AkDocument5 pagesFabm 12 Q2 1002 Akanna paulaNo ratings yet

- Pearsons Federal Taxation 2018 Individuals 31st Edition Rupert Solutions ManualDocument30 pagesPearsons Federal Taxation 2018 Individuals 31st Edition Rupert Solutions Manualsilingvolumedvh2myq100% (26)

- Pearsons Federal Taxation 2018 Comprehensive 31St Edition Rupert Solutions Manual Full Chapter PDFDocument51 pagesPearsons Federal Taxation 2018 Comprehensive 31St Edition Rupert Solutions Manual Full Chapter PDFWilliamDanielsezgj100% (10)

- BUS 168A Midterm ReviewDocument5 pagesBUS 168A Midterm ReviewcalebrmanNo ratings yet

- Heads of Income - Income From SalaryDocument10 pagesHeads of Income - Income From SalaryBhavesh KhillareNo ratings yet

- See Melville p90: Exercise To Be Completed in Advance of The Seminar Based On Unit 3Document8 pagesSee Melville p90: Exercise To Be Completed in Advance of The Seminar Based On Unit 3Bhuvan BhatiaNo ratings yet

- Income TaxationDocument7 pagesIncome TaxationDummy GoogleNo ratings yet

- Solution 1: Calculation of Total Assessable Income, Taxable Income, Tax LiabilityDocument14 pagesSolution 1: Calculation of Total Assessable Income, Taxable Income, Tax LiabilityDevender SharmaNo ratings yet

- US Internal Revenue Service: F1040es - 2000Document7 pagesUS Internal Revenue Service: F1040es - 2000IRSNo ratings yet

- Co-Ownership, Estate and TrustDocument6 pagesCo-Ownership, Estate and TrustRyan Christian Balanquit100% (2)

- F1040es 2020Document12 pagesF1040es 2020Job SchwartzNo ratings yet

- F1040es 2018Document18 pagesF1040es 2018diversified1No ratings yet

- W13 Module 11 - Income Tax of Estates and TrustsDocument5 pagesW13 Module 11 - Income Tax of Estates and Trustscamille ducutNo ratings yet

- TaxPlanning06 07Document17 pagesTaxPlanning06 07Lathif PashaNo ratings yet

- Pearsons Federal Taxation 2018 Comprehensive 31st Edition Rupert Solutions ManualDocument30 pagesPearsons Federal Taxation 2018 Comprehensive 31st Edition Rupert Solutions Manualalyssahoffmantbqfyjwszi100% (30)

- Classification of Deductible Expenses Section 212 Expenses:: Have AGI LimitationsDocument6 pagesClassification of Deductible Expenses Section 212 Expenses:: Have AGI Limitations张心怡No ratings yet

- South Western Federal Taxation 2017 Comprehensive 40Th Edition Hoffman Solutions Manual Full Chapter PDFDocument36 pagesSouth Western Federal Taxation 2017 Comprehensive 40Th Edition Hoffman Solutions Manual Full Chapter PDFfred.henderson352100% (11)

- TIF Problems 07-10 (2014)Document141 pagesTIF Problems 07-10 (2014)Mariella NiyoyunguruzaNo ratings yet

- TaxationDocument12 pagesTaxationjanahh.omNo ratings yet

- South-Western Federal Taxation 2016 Comprehensive 39th Edition Solution Manual 1Document36 pagesSouth-Western Federal Taxation 2016 Comprehensive 39th Edition Solution Manual 1briancrosbyqfakzcndys100% (28)

- Dividend Received From A Domestic CompanyDocument9 pagesDividend Received From A Domestic Companyshiraz shabbirNo ratings yet

- Final Document On Tax LawDocument13 pagesFinal Document On Tax LawkimtexNo ratings yet

- Taxation LawDocument17 pagesTaxation LawSujay KhotNo ratings yet

- Crosswalk CPA Review: Tax UpdateDocument4 pagesCrosswalk CPA Review: Tax UpdateAdhira VenkatNo ratings yet

- 0456Document4 pages0456Usman Shaukat Khan100% (1)

- Ch4-Recordedlecture-Fall2023 17 5166787619170306Document38 pagesCh4-Recordedlecture-Fall2023 17 5166787619170306ronny nyagakaNo ratings yet

- PIT09 Tax ReducersDocument8 pagesPIT09 Tax ReducersAlellie Khay D JordanNo ratings yet

- Computation of Taxable Income and Tax LiabilityDocument9 pagesComputation of Taxable Income and Tax LiabilityaNo ratings yet

- Income Tax Basics - July 2023Document6 pagesIncome Tax Basics - July 2023maharajabby81No ratings yet

- KEY WORDS - Income TaxationDocument23 pagesKEY WORDS - Income TaxationQueenVictoriaAshleyPrietoNo ratings yet

- Homework ES 2 Solution ACCT 553Document5 pagesHomework ES 2 Solution ACCT 553Mohammad IslamNo ratings yet

- Screenshot 2024-04-25 at 10.18.59 PMDocument60 pagesScreenshot 2024-04-25 at 10.18.59 PMLamita DerghamNo ratings yet

- Income Tax On Estates and Trusts: A. Taxability of EstatesDocument4 pagesIncome Tax On Estates and Trusts: A. Taxability of EstatesKevin OnaroNo ratings yet

- Tax On Estates and Trusts: A. Taxability of EstatesDocument4 pagesTax On Estates and Trusts: A. Taxability of EstatesGeorgianne Isla AllejeNo ratings yet

- Tax Mock Bar ExamDocument6 pagesTax Mock Bar ExamMarco RvsNo ratings yet

- South Western Federal Taxation 2020 Comprehensive 43rd Edition Maloney Solutions ManualDocument38 pagesSouth Western Federal Taxation 2020 Comprehensive 43rd Edition Maloney Solutions Manualmateosowhite100% (20)

- Aq 10Document58 pagesAq 10Minie KimNo ratings yet

- Acct 470 Pre Quiz Chapter 4,5,9-12Document28 pagesAcct 470 Pre Quiz Chapter 4,5,9-12karissa.jqasm.0No ratings yet

- Filling For Claim For RefundDocument8 pagesFilling For Claim For RefundsheldonNo ratings yet

- ACC 430 Chapter 10Document20 pagesACC 430 Chapter 10vikkiNo ratings yet

- 1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Document5 pages1.7.7.1. Entertainment Allowance (U/s 16 (Ii) ) : 1.7.7. Deduction Out of Gross Salary (Section 16)Vinod PillaiNo ratings yet

- EA MCQs and VIDEOSDocument9 pagesEA MCQs and VIDEOSKalpak RaneNo ratings yet

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- Impact of Demonetisation On DelhiDocument51 pagesImpact of Demonetisation On Delhitanmay agrawalNo ratings yet

- Impact of Globalization On The Taxi Industry in IndiaDocument64 pagesImpact of Globalization On The Taxi Industry in Indiatanmay agrawalNo ratings yet

- Export of Namkeen PDFDocument10 pagesExport of Namkeen PDFtanmay agrawalNo ratings yet

- Maggi Research Proposal Standard)Document10 pagesMaggi Research Proposal Standard)tanmay agrawalNo ratings yet

- The Criminal LawDocument8 pagesThe Criminal Lawtanmay agrawalNo ratings yet

- The Criminal LawDocument8 pagesThe Criminal Lawtanmay agrawalNo ratings yet

- The Australian Constitutional LawDocument6 pagesThe Australian Constitutional Lawtanmay agrawalNo ratings yet

- Learning Module-Systematic Literature Review (Academic Writing)Document37 pagesLearning Module-Systematic Literature Review (Academic Writing)tanmay agrawalNo ratings yet

- Taxation Assignment Help OnlineDocument4 pagesTaxation Assignment Help Onlinetanmay agrawalNo ratings yet

- Impact of Demonetisation On DelhiDocument51 pagesImpact of Demonetisation On Delhitanmay agrawalNo ratings yet

- Legal Case StudyDocument12 pagesLegal Case Studytanmay agrawalNo ratings yet

- Investment Project PDFDocument15 pagesInvestment Project PDFtanmay agrawalNo ratings yet

- Iibf Jaiib ApplicationDocument4 pagesIibf Jaiib Applicationreachtorajan700No ratings yet

- Brief: SDG Priorities For BangladeshDocument3 pagesBrief: SDG Priorities For BangladeshMrz AshikNo ratings yet

- Business Law: Certificate in Accounting and Finance Stage ExaminationDocument3 pagesBusiness Law: Certificate in Accounting and Finance Stage ExaminationKashan KhanNo ratings yet

- National Geographic Afghanistan Hidden TreasuresDocument4 pagesNational Geographic Afghanistan Hidden TreasuresJohnNY_TexNo ratings yet

- Smoking During Pregnancy FinalDocument14 pagesSmoking During Pregnancy Finalapi-232728488No ratings yet

- A Development Bank Is A Polygonal Development Finance Institution Devoted To Improving The Social and Monetary Development of Its Associate NationsDocument2 pagesA Development Bank Is A Polygonal Development Finance Institution Devoted To Improving The Social and Monetary Development of Its Associate NationsAjay SolankiNo ratings yet

- Catalogo de BendixDocument31 pagesCatalogo de BendixLENER ANTONIO ALACHE MENDOZANo ratings yet

- Lawrence Connell v. Linda Ammons - Court Opinion Denying Motion To Change VenueDocument3 pagesLawrence Connell v. Linda Ammons - Court Opinion Denying Motion To Change VenueLegal InsurrectionNo ratings yet

- Argument Lesson Socratic SeminarDocument5 pagesArgument Lesson Socratic Seminarapi-346495805No ratings yet

- Art. Methodological Issues in Cross Cultural Marketing Research. A State of The Art Review PDFDocument45 pagesArt. Methodological Issues in Cross Cultural Marketing Research. A State of The Art Review PDFM.C MejiaNo ratings yet

- OSX Entrepreneurship Ch07Document29 pagesOSX Entrepreneurship Ch07Camila Alexandra SHIALER FIGUEROANo ratings yet

- ContractDocument3 pagesContractrodelyn ubalubaoNo ratings yet

- Haitham Samir C.V - FinalDocument5 pagesHaitham Samir C.V - FinalElizabeth SmithNo ratings yet

- Class Notes On Agrobiodiversity Conservation and Climate Change 022Document156 pagesClass Notes On Agrobiodiversity Conservation and Climate Change 022Kabir Singh100% (1)

- Test The VisionaryDocument2 pagesTest The VisionaryrlcruzNo ratings yet

- GRADE 5 AGUINALDO Numeracy Profile of LearnersDocument7 pagesGRADE 5 AGUINALDO Numeracy Profile of Learnersroel labayNo ratings yet

- W. Edwards DemingDocument2 pagesW. Edwards DemingJake Pantaleon Boston100% (2)

- 1 Aloandro Ben Bakr - BeatrizDocument1 page1 Aloandro Ben Bakr - BeatrizDavid DayNo ratings yet

- R.A. 7659 PDFDocument13 pagesR.A. 7659 PDFMarion Yves MosonesNo ratings yet

- Chapter 1 - Organizational Behavior TodayDocument25 pagesChapter 1 - Organizational Behavior TodayK-an SolNo ratings yet

- Case Study GoogleplexDocument6 pagesCase Study GoogleplexRoger Madorell100% (1)

- Logical Criticism of Buddhist DoctrinesDocument340 pagesLogical Criticism of Buddhist DoctrinesAvi Sion100% (1)

- Globalization L7Document42 pagesGlobalization L7Cherrie Chu SiuwanNo ratings yet

- Chapter 17 (Hukm Shar'i)Document16 pagesChapter 17 (Hukm Shar'i)MutyaAlmodienteCocjin100% (1)

- William Shakespeare's SonnetsDocument5 pagesWilliam Shakespeare's Sonnetsgabryela22No ratings yet

- CHP 10Document9 pagesCHP 10KhjNo ratings yet

- Case Analysis: Enrollment: Contract Law & FerpaDocument3 pagesCase Analysis: Enrollment: Contract Law & FerpaJenny B.No ratings yet

- Ignacy Jan Paderewski A Discography of His European RecordingsDocument9 pagesIgnacy Jan Paderewski A Discography of His European RecordingsCody NguyenNo ratings yet

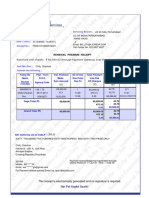

- Received With Thanks ' 60,569.62 Through Payment Gateway Over The Internet FromDocument1 pageReceived With Thanks ' 60,569.62 Through Payment Gateway Over The Internet FromCSK100% (1)