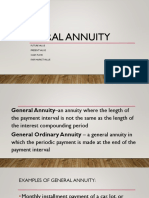

Simple Annuities

Simple Annuities

You might also like

- Thompson Asset ManagementDocument17 pagesThompson Asset ManagementJessicaNo ratings yet

- Activity Worksheet Grade 11 Week 3Document3 pagesActivity Worksheet Grade 11 Week 3Glaiza SaltingNo ratings yet

- Lesson 31 Supplementary ExercisesDocument1 pageLesson 31 Supplementary ExercisesPam G.100% (1)

- Television Main Section and PartsDocument5 pagesTelevision Main Section and Partselma anacleto88% (8)

- One Pager - BXA Sales - Ver 1.2-1Document2 pagesOne Pager - BXA Sales - Ver 1.2-1Ques LeeNo ratings yet

- Requirement Membership ApplicationDocument7 pagesRequirement Membership ApplicationkezNo ratings yet

- WEEK 8.3 Intercepts, Zeroes, and Asymptotes of Logarithmic FunctionsDocument11 pagesWEEK 8.3 Intercepts, Zeroes, and Asymptotes of Logarithmic FunctionsOreo ProductionsNo ratings yet

- LM Precal Grade11 Sem1Document356 pagesLM Precal Grade11 Sem1Nefarious Mitsiukie100% (1)

- Basic Calculus: Quarter 3 - Module 5 Rules of DifferentiationDocument28 pagesBasic Calculus: Quarter 3 - Module 5 Rules of DifferentiationHarold BunaosNo ratings yet

- General Annuity: Future Value Present Value Cash Flow Fair Market ValueDocument7 pagesGeneral Annuity: Future Value Present Value Cash Flow Fair Market ValueReyes C. Ervin0% (1)

- SeatworkDocument2 pagesSeatworkPEÑAS, CHARY ANN C.No ratings yet

- Lesson 12 Exponential FunctionDocument34 pagesLesson 12 Exponential FunctionFretchie Anne C. LauroNo ratings yet

- Gen Math Week 6Document9 pagesGen Math Week 6sellos Ko0% (1)

- General Mathematics: Quarter 1 Week 4 Module 9Document12 pagesGeneral Mathematics: Quarter 1 Week 4 Module 9Barez Fernandez ZacNo ratings yet

- General Mathematics: Simple and Compound InterestDocument19 pagesGeneral Mathematics: Simple and Compound InterestLynette LicsiNo ratings yet

- Statprob11 q3 Mod3 Week5 8 Sampling and Sampling Distribution Version2Document45 pagesStatprob11 q3 Mod3 Week5 8 Sampling and Sampling Distribution Version2judylyn elizagaNo ratings yet

- Determine Whether The Given Is A Logarithmic FunctionDocument3 pagesDetermine Whether The Given Is A Logarithmic FunctionShehonny Villanueva-Bayaban100% (1)

- General Mathematics: Quarter 1 - ModuleDocument15 pagesGeneral Mathematics: Quarter 1 - ModuleJinky Bon100% (1)

- General Mathematics: Quarter 1 - Module 1: FunctionsDocument20 pagesGeneral Mathematics: Quarter 1 - Module 1: FunctionsRubenNo ratings yet

- Exponential Models: General MathematicsDocument33 pagesExponential Models: General MathematicsJulie Ann Barba TayasNo ratings yet

- Stat Module Q3 Week1Document11 pagesStat Module Q3 Week1Eloisa Jane BituinNo ratings yet

- General Mathematics - Grade 11 Fair Market Value and Deferred AnnuityDocument13 pagesGeneral Mathematics - Grade 11 Fair Market Value and Deferred AnnuityMaxine ReyesNo ratings yet

- GenMath11 - Q2 - Mod2 - Interest Maturity Present and Future Values in Simple and Compound Interest - Version2 From CE1 Ce2 1Document31 pagesGenMath11 - Q2 - Mod2 - Interest Maturity Present and Future Values in Simple and Compound Interest - Version2 From CE1 Ce2 1Emmarie MercadoNo ratings yet

- Lesson 1 - The Limit of A Function - Theorems and ExamplesDocument65 pagesLesson 1 - The Limit of A Function - Theorems and ExamplesLyca EstolaNo ratings yet

- PRE-CALCULUS-W5-SLEM PC11AGfuucc Quarter1 Week5Document6 pagesPRE-CALCULUS-W5-SLEM PC11AGfuucc Quarter1 Week5Lemuel FajutagNo ratings yet

- Precalculus: Circle With Center at (0, 0)Document18 pagesPrecalculus: Circle With Center at (0, 0)Rain PasiaNo ratings yet

- LAS 9 GenMath 11Document9 pagesLAS 9 GenMath 11Chantal AltheaNo ratings yet

- General Quarter 2 - Week 1: ZZZZZZDocument14 pagesGeneral Quarter 2 - Week 1: ZZZZZZJakim Lopez0% (1)

- Lesson: Graphing Logarithmic Functions Learning Outcome(s) : at The End of The Lesson, The Learner Is Able To Represent ADocument19 pagesLesson: Graphing Logarithmic Functions Learning Outcome(s) : at The End of The Lesson, The Learner Is Able To Represent AKristina PabloNo ratings yet

- GM 016 344575 PDFDocument15 pagesGM 016 344575 PDFeunha allaybanNo ratings yet

- Stat LAS 15Document7 pagesStat LAS 15aljun badeNo ratings yet

- PDF General Math LM For Shs CompressDocument313 pagesPDF General Math LM For Shs CompressAltheaGuanzon100% (1)

- LAS Gen - Math Q1 W2BeduyaPNHSDocument15 pagesLAS Gen - Math Q1 W2BeduyaPNHSJerry GabacNo ratings yet

- CC3 SGM1Document21 pagesCC3 SGM1Jayla Mae YapNo ratings yet

- Signed Off General Mathematics11 q1 m2 Rational Functions v3Document47 pagesSigned Off General Mathematics11 q1 m2 Rational Functions v3HONEY LYN PARASNo ratings yet

- Statistics and Probability: Quarter 3 - Module 2: Mean and Variance of Discrete Random VariableDocument19 pagesStatistics and Probability: Quarter 3 - Module 2: Mean and Variance of Discrete Random VariableYdzel Jay Dela TorreNo ratings yet

- 2ND Quarter Modules Gen MathDocument159 pages2ND Quarter Modules Gen MathJester Guballa de LeonNo ratings yet

- Statprob - q3 - Mod9 - Solving Real Life Preoblems Involving Mean and Variance - v2Document27 pagesStatprob - q3 - Mod9 - Solving Real Life Preoblems Involving Mean and Variance - v2Moreal QazNo ratings yet

- Rev01 - Q2.ESS MELC 12Document32 pagesRev01 - Q2.ESS MELC 12jiamail gampongNo ratings yet

- Lender: Origin or Loan DateDocument4 pagesLender: Origin or Loan DateIrish Mae JovitaNo ratings yet

- General Mathematics: Quarter 1 - Module 8: The Domain and Range of A Rational FunctionsDocument19 pagesGeneral Mathematics: Quarter 1 - Module 8: The Domain and Range of A Rational FunctionsPrecious Ann VelasquezNo ratings yet

- Enior IGH Chool: Module No. Title: Sampling Distribution of Sample Means Overview/ Introductio N Learning ObjectivesDocument27 pagesEnior IGH Chool: Module No. Title: Sampling Distribution of Sample Means Overview/ Introductio N Learning ObjectivesVan Errl Nicolai SantosNo ratings yet

- GenMath Q1 Module2 Rational FunctionDocument25 pagesGenMath Q1 Module2 Rational FunctionGine Bert Fariñas PalabricaNo ratings yet

- Activity Sheets: Quarter 2 - MELC 3Document8 pagesActivity Sheets: Quarter 2 - MELC 3Lalaine Jhen Dela CruzNo ratings yet

- Genmath11 q2 Mod1and 2 Week1Document42 pagesGenmath11 q2 Mod1and 2 Week1Aaron LacasandileNo ratings yet

- Stat and Prob Q4 Week 3 Module 11 Alexander Randy EstradaDocument21 pagesStat and Prob Q4 Week 3 Module 11 Alexander Randy Estradagabezarate071No ratings yet

- GenmathDocument9 pagesGenmathJuliet RoseNo ratings yet

- Gen Math11 Q1 Mod3 Operations On Functions 08082020Document1 pageGen Math11 Q1 Mod3 Operations On Functions 08082020Lyrech Samalio100% (3)

- Basic Calculus: Problems Involving ContinuityDocument13 pagesBasic Calculus: Problems Involving ContinuityLorea Dechavez100% (1)

- Gen Math Q1 Mod 1Document21 pagesGen Math Q1 Mod 1Joselito UbaldoNo ratings yet

- Signed Off Statistics and Probability11 q2 m3 Random Sampling and Sampling Distribution v3Document64 pagesSigned Off Statistics and Probability11 q2 m3 Random Sampling and Sampling Distribution v3Rona Marie BulaongNo ratings yet

- Statistics and ProbabilityDocument71 pagesStatistics and ProbabilityMarian SolivaNo ratings yet

- #NOTE: The Cash Value or Cash Price Is Equal To #NOTE: The Cash Value or Cash Price Is Equal ToDocument1 page#NOTE: The Cash Value or Cash Price Is Equal To #NOTE: The Cash Value or Cash Price Is Equal ToMikko PerezNo ratings yet

- Stat Prob Week 5 6Document15 pagesStat Prob Week 5 6jayson santos0% (1)

- Topic 13 Percentiles and T-Distribution PDFDocument5 pagesTopic 13 Percentiles and T-Distribution PDFPrincess VernieceNo ratings yet

- Supplementary ExercisesDocument14 pagesSupplementary ExercisesCastillo Sibayan Kev0% (1)

- GEN-CHEM-1 G11 Module3 Q1W3 MODDocument15 pagesGEN-CHEM-1 G11 Module3 Q1W3 MODDaniel Corcino100% (1)

- Statisticsprobability11 q4 Week2 v4Document10 pagesStatisticsprobability11 q4 Week2 v4Sheryn CredoNo ratings yet

- STATISTICS Q3 WEEK-9 Revision-3Document17 pagesSTATISTICS Q3 WEEK-9 Revision-3ace fuentesNo ratings yet

- Reading and Writing Q2 M11Document19 pagesReading and Writing Q2 M11Justine Mark GuzmanNo ratings yet

- Virtual Meet GMDocument34 pagesVirtual Meet GMLea Mae Vivo GeleraNo ratings yet

- WW6 7 Self Learning ModuleDocument27 pagesWW6 7 Self Learning ModuleIrish MendozaNo ratings yet

- Piecewise and Inverse Functions and Composition of FunctionsDocument35 pagesPiecewise and Inverse Functions and Composition of FunctionsDCHKLian 17100% (1)

- Simple and General AnnuitiesDocument12 pagesSimple and General AnnuitiesEarl Clyde BañezNo ratings yet

- Automotive 11 Summative Test 11 Second SemDocument1 pageAutomotive 11 Summative Test 11 Second Semelma anacleto100% (1)

- Front Office Services Second Quarter Summative TestDocument4 pagesFront Office Services Second Quarter Summative Testelma anacleto100% (2)

- APPLIED ECONOMIC Summative TestDocument4 pagesAPPLIED ECONOMIC Summative Testelma anacleto80% (5)

- Subject: General ChemistryDocument2 pagesSubject: General Chemistryelma anacletoNo ratings yet

- Module 5 (Week 7 and 8)Document11 pagesModule 5 (Week 7 and 8)elma anacletoNo ratings yet

- Contemporary Module 1Document18 pagesContemporary Module 1elma anacleto100% (1)

- Part III: Read The Following Question and Write The Correct Answer in Separate Sheet of PaperDocument1 pagePart III: Read The Following Question and Write The Correct Answer in Separate Sheet of Paperelma anacletoNo ratings yet

- SUBJECT SYLLABUS - Filipino Sa Piling LaranganDocument3 pagesSUBJECT SYLLABUS - Filipino Sa Piling Laranganelma anacletoNo ratings yet

- Housekeeping 11 Second Quarter Summative TestDocument2 pagesHousekeeping 11 Second Quarter Summative Testelma anacleto100% (2)

- Objectives: Holt Algebra 2Document14 pagesObjectives: Holt Algebra 2elma anacletoNo ratings yet

- RequestDocument1 pageRequestelma anacletoNo ratings yet

- ReferencesDocument9 pagesReferenceselma anacletoNo ratings yet

- Task Sheet 1.1-4: Title: Assemble Computer HardwareDocument1 pageTask Sheet 1.1-4: Title: Assemble Computer Hardwareelma anacletoNo ratings yet

- DRRM Module 1Document10 pagesDRRM Module 1elma anacletoNo ratings yet

- Literature Broadly Is Any Collection Of: o o o o o o o o o o o o o o oDocument6 pagesLiterature Broadly Is Any Collection Of: o o o o o o o o o o o o o o oelma anacletoNo ratings yet

- This Article Is About The Field of StudyDocument5 pagesThis Article Is About The Field of Studyelma anacletoNo ratings yet

- Relationships: - in Bibliographic Records and in Authority RecordsDocument46 pagesRelationships: - in Bibliographic Records and in Authority Recordselma anacletoNo ratings yet

- Eustress or Distress An Empirical Study of PerceivDocument10 pagesEustress or Distress An Empirical Study of Perceivelma anacletoNo ratings yet

- Task Sheet Title: Installing An Application Performance ObjectiveDocument2 pagesTask Sheet Title: Installing An Application Performance Objectiveelma anacletoNo ratings yet

- What Is ICTDocument1 pageWhat Is ICTelma anacletoNo ratings yet

- Rolly Japitana Salinas JRDocument3 pagesRolly Japitana Salinas JRelma anacletoNo ratings yet

- Banking Operation &management: Presidency CollegeDocument46 pagesBanking Operation &management: Presidency CollegeKaran RajNo ratings yet

- FAQ Business Direct 1Document15 pagesFAQ Business Direct 1maryrobert8322No ratings yet

- Doomsday CycleDocument5 pagesDoomsday CyclenovriadyNo ratings yet

- SS 2 Store MGT Third Term E-Learning NoteDocument38 pagesSS 2 Store MGT Third Term E-Learning Notepalmer okiemuteNo ratings yet

- Ibps Po MainsDocument169 pagesIbps Po MainsSaurabh AnandNo ratings yet

- Test Bank For Corporate Finance 13th Stephen Ross Randolph Westerfield Jeffrey JaffeDocument54 pagesTest Bank For Corporate Finance 13th Stephen Ross Randolph Westerfield Jeffrey Jaffemarcuskenyatta275No ratings yet

- Impact of Demonetization On Microfinance SectorDocument4 pagesImpact of Demonetization On Microfinance SectorGibin KollamparambilNo ratings yet

- Peer-Review Assessment Course 1aDocument5 pagesPeer-Review Assessment Course 1aSamael LightbringerNo ratings yet

- Chapter 3. Solution Exercises Income StatementDocument13 pagesChapter 3. Solution Exercises Income StatementHECTOR ORTEGANo ratings yet

- Royal Bank of Scotland: Corporate Rap SheetDocument9 pagesRoyal Bank of Scotland: Corporate Rap SheetMohsen KhanNo ratings yet

- Priyadarshini Spinning Mills Ltd-Winding Up NoticeDocument3 pagesPriyadarshini Spinning Mills Ltd-Winding Up NoticeAbhijit TripathiNo ratings yet

- Simple Interest Worksheet 1Document2 pagesSimple Interest Worksheet 1vajoorbiNo ratings yet

- Current LiabilitiesDocument94 pagesCurrent LiabilitiesDawit TilahunNo ratings yet

- HDFC SL CrestDocument1 pageHDFC SL Crestk_kishan288No ratings yet

- The Income StatementDocument10 pagesThe Income Statementayoub mechouatNo ratings yet

- Universal LoanDocument4 pagesUniversal LoanOlivia AvaNo ratings yet

- Fifteen Transactions or Events Affecting Computer Specialists Inc Are AsDocument1 pageFifteen Transactions or Events Affecting Computer Specialists Inc Are Astrilocksp SinghNo ratings yet

- PRR Edu11-2019Document14,118 pagesPRR Edu11-2019attaNo ratings yet

- Dr. M.G.R Educational and Research Instution, ChennaiDocument54 pagesDr. M.G.R Educational and Research Instution, ChennaiVijay MNo ratings yet

- Deutsche UFG Capital Management - ENGDocument28 pagesDeutsche UFG Capital Management - ENGAnton DenisovNo ratings yet

- Study On Capital MarketsDocument78 pagesStudy On Capital Marketsmanuuu patel0% (1)

- CFM AssignmentDocument26 pagesCFM AssignmentNaman VarshneyNo ratings yet

- Group 5 PresentationDocument10 pagesGroup 5 PresentationGervinBulataoNo ratings yet

- Darpan Kumar 100014663 Proposal No: Save & Assure Investment Secure Fund (SA) Fund: Plan: Alac-Banca-Mcb-St-Suk BranchDocument4 pagesDarpan Kumar 100014663 Proposal No: Save & Assure Investment Secure Fund (SA) Fund: Plan: Alac-Banca-Mcb-St-Suk BranchHaris AliNo ratings yet

- Chemical RatesDocument12 pagesChemical RatesKABIR CHOPRANo ratings yet

- Instructional Planning: Detailed Lesson Plan (DLP) FormatDocument5 pagesInstructional Planning: Detailed Lesson Plan (DLP) FormatDaisy PaoNo ratings yet

- Chapter 5: Books of Accounts & Double-Entry System (FAR By: Millan)Document17 pagesChapter 5: Books of Accounts & Double-Entry System (FAR By: Millan)Portia AbestanoNo ratings yet

Download as pdf or txt

You might also like

- Thompson Asset ManagementDocument17 pagesThompson Asset ManagementJessicaNo ratings yet

- Activity Worksheet Grade 11 Week 3Document3 pagesActivity Worksheet Grade 11 Week 3Glaiza SaltingNo ratings yet

- Lesson 31 Supplementary ExercisesDocument1 pageLesson 31 Supplementary ExercisesPam G.100% (1)

- Television Main Section and PartsDocument5 pagesTelevision Main Section and Partselma anacleto88% (8)

- One Pager - BXA Sales - Ver 1.2-1Document2 pagesOne Pager - BXA Sales - Ver 1.2-1Ques LeeNo ratings yet

- Requirement Membership ApplicationDocument7 pagesRequirement Membership ApplicationkezNo ratings yet

- WEEK 8.3 Intercepts, Zeroes, and Asymptotes of Logarithmic FunctionsDocument11 pagesWEEK 8.3 Intercepts, Zeroes, and Asymptotes of Logarithmic FunctionsOreo ProductionsNo ratings yet

- LM Precal Grade11 Sem1Document356 pagesLM Precal Grade11 Sem1Nefarious Mitsiukie100% (1)

- Basic Calculus: Quarter 3 - Module 5 Rules of DifferentiationDocument28 pagesBasic Calculus: Quarter 3 - Module 5 Rules of DifferentiationHarold BunaosNo ratings yet

- General Annuity: Future Value Present Value Cash Flow Fair Market ValueDocument7 pagesGeneral Annuity: Future Value Present Value Cash Flow Fair Market ValueReyes C. Ervin0% (1)

- SeatworkDocument2 pagesSeatworkPEÑAS, CHARY ANN C.No ratings yet

- Lesson 12 Exponential FunctionDocument34 pagesLesson 12 Exponential FunctionFretchie Anne C. LauroNo ratings yet

- Gen Math Week 6Document9 pagesGen Math Week 6sellos Ko0% (1)

- General Mathematics: Quarter 1 Week 4 Module 9Document12 pagesGeneral Mathematics: Quarter 1 Week 4 Module 9Barez Fernandez ZacNo ratings yet

- General Mathematics: Simple and Compound InterestDocument19 pagesGeneral Mathematics: Simple and Compound InterestLynette LicsiNo ratings yet

- Statprob11 q3 Mod3 Week5 8 Sampling and Sampling Distribution Version2Document45 pagesStatprob11 q3 Mod3 Week5 8 Sampling and Sampling Distribution Version2judylyn elizagaNo ratings yet

- Determine Whether The Given Is A Logarithmic FunctionDocument3 pagesDetermine Whether The Given Is A Logarithmic FunctionShehonny Villanueva-Bayaban100% (1)

- General Mathematics: Quarter 1 - ModuleDocument15 pagesGeneral Mathematics: Quarter 1 - ModuleJinky Bon100% (1)

- General Mathematics: Quarter 1 - Module 1: FunctionsDocument20 pagesGeneral Mathematics: Quarter 1 - Module 1: FunctionsRubenNo ratings yet

- Exponential Models: General MathematicsDocument33 pagesExponential Models: General MathematicsJulie Ann Barba TayasNo ratings yet

- Stat Module Q3 Week1Document11 pagesStat Module Q3 Week1Eloisa Jane BituinNo ratings yet

- General Mathematics - Grade 11 Fair Market Value and Deferred AnnuityDocument13 pagesGeneral Mathematics - Grade 11 Fair Market Value and Deferred AnnuityMaxine ReyesNo ratings yet

- GenMath11 - Q2 - Mod2 - Interest Maturity Present and Future Values in Simple and Compound Interest - Version2 From CE1 Ce2 1Document31 pagesGenMath11 - Q2 - Mod2 - Interest Maturity Present and Future Values in Simple and Compound Interest - Version2 From CE1 Ce2 1Emmarie MercadoNo ratings yet

- Lesson 1 - The Limit of A Function - Theorems and ExamplesDocument65 pagesLesson 1 - The Limit of A Function - Theorems and ExamplesLyca EstolaNo ratings yet

- PRE-CALCULUS-W5-SLEM PC11AGfuucc Quarter1 Week5Document6 pagesPRE-CALCULUS-W5-SLEM PC11AGfuucc Quarter1 Week5Lemuel FajutagNo ratings yet

- Precalculus: Circle With Center at (0, 0)Document18 pagesPrecalculus: Circle With Center at (0, 0)Rain PasiaNo ratings yet

- LAS 9 GenMath 11Document9 pagesLAS 9 GenMath 11Chantal AltheaNo ratings yet

- General Quarter 2 - Week 1: ZZZZZZDocument14 pagesGeneral Quarter 2 - Week 1: ZZZZZZJakim Lopez0% (1)

- Lesson: Graphing Logarithmic Functions Learning Outcome(s) : at The End of The Lesson, The Learner Is Able To Represent ADocument19 pagesLesson: Graphing Logarithmic Functions Learning Outcome(s) : at The End of The Lesson, The Learner Is Able To Represent AKristina PabloNo ratings yet

- GM 016 344575 PDFDocument15 pagesGM 016 344575 PDFeunha allaybanNo ratings yet

- Stat LAS 15Document7 pagesStat LAS 15aljun badeNo ratings yet

- PDF General Math LM For Shs CompressDocument313 pagesPDF General Math LM For Shs CompressAltheaGuanzon100% (1)

- LAS Gen - Math Q1 W2BeduyaPNHSDocument15 pagesLAS Gen - Math Q1 W2BeduyaPNHSJerry GabacNo ratings yet

- CC3 SGM1Document21 pagesCC3 SGM1Jayla Mae YapNo ratings yet

- Signed Off General Mathematics11 q1 m2 Rational Functions v3Document47 pagesSigned Off General Mathematics11 q1 m2 Rational Functions v3HONEY LYN PARASNo ratings yet

- Statistics and Probability: Quarter 3 - Module 2: Mean and Variance of Discrete Random VariableDocument19 pagesStatistics and Probability: Quarter 3 - Module 2: Mean and Variance of Discrete Random VariableYdzel Jay Dela TorreNo ratings yet

- 2ND Quarter Modules Gen MathDocument159 pages2ND Quarter Modules Gen MathJester Guballa de LeonNo ratings yet

- Statprob - q3 - Mod9 - Solving Real Life Preoblems Involving Mean and Variance - v2Document27 pagesStatprob - q3 - Mod9 - Solving Real Life Preoblems Involving Mean and Variance - v2Moreal QazNo ratings yet

- Rev01 - Q2.ESS MELC 12Document32 pagesRev01 - Q2.ESS MELC 12jiamail gampongNo ratings yet

- Lender: Origin or Loan DateDocument4 pagesLender: Origin or Loan DateIrish Mae JovitaNo ratings yet

- General Mathematics: Quarter 1 - Module 8: The Domain and Range of A Rational FunctionsDocument19 pagesGeneral Mathematics: Quarter 1 - Module 8: The Domain and Range of A Rational FunctionsPrecious Ann VelasquezNo ratings yet

- Enior IGH Chool: Module No. Title: Sampling Distribution of Sample Means Overview/ Introductio N Learning ObjectivesDocument27 pagesEnior IGH Chool: Module No. Title: Sampling Distribution of Sample Means Overview/ Introductio N Learning ObjectivesVan Errl Nicolai SantosNo ratings yet

- GenMath Q1 Module2 Rational FunctionDocument25 pagesGenMath Q1 Module2 Rational FunctionGine Bert Fariñas PalabricaNo ratings yet

- Activity Sheets: Quarter 2 - MELC 3Document8 pagesActivity Sheets: Quarter 2 - MELC 3Lalaine Jhen Dela CruzNo ratings yet

- Genmath11 q2 Mod1and 2 Week1Document42 pagesGenmath11 q2 Mod1and 2 Week1Aaron LacasandileNo ratings yet

- Stat and Prob Q4 Week 3 Module 11 Alexander Randy EstradaDocument21 pagesStat and Prob Q4 Week 3 Module 11 Alexander Randy Estradagabezarate071No ratings yet

- GenmathDocument9 pagesGenmathJuliet RoseNo ratings yet

- Gen Math11 Q1 Mod3 Operations On Functions 08082020Document1 pageGen Math11 Q1 Mod3 Operations On Functions 08082020Lyrech Samalio100% (3)

- Basic Calculus: Problems Involving ContinuityDocument13 pagesBasic Calculus: Problems Involving ContinuityLorea Dechavez100% (1)

- Gen Math Q1 Mod 1Document21 pagesGen Math Q1 Mod 1Joselito UbaldoNo ratings yet

- Signed Off Statistics and Probability11 q2 m3 Random Sampling and Sampling Distribution v3Document64 pagesSigned Off Statistics and Probability11 q2 m3 Random Sampling and Sampling Distribution v3Rona Marie BulaongNo ratings yet

- Statistics and ProbabilityDocument71 pagesStatistics and ProbabilityMarian SolivaNo ratings yet

- #NOTE: The Cash Value or Cash Price Is Equal To #NOTE: The Cash Value or Cash Price Is Equal ToDocument1 page#NOTE: The Cash Value or Cash Price Is Equal To #NOTE: The Cash Value or Cash Price Is Equal ToMikko PerezNo ratings yet

- Stat Prob Week 5 6Document15 pagesStat Prob Week 5 6jayson santos0% (1)

- Topic 13 Percentiles and T-Distribution PDFDocument5 pagesTopic 13 Percentiles and T-Distribution PDFPrincess VernieceNo ratings yet

- Supplementary ExercisesDocument14 pagesSupplementary ExercisesCastillo Sibayan Kev0% (1)

- GEN-CHEM-1 G11 Module3 Q1W3 MODDocument15 pagesGEN-CHEM-1 G11 Module3 Q1W3 MODDaniel Corcino100% (1)

- Statisticsprobability11 q4 Week2 v4Document10 pagesStatisticsprobability11 q4 Week2 v4Sheryn CredoNo ratings yet

- STATISTICS Q3 WEEK-9 Revision-3Document17 pagesSTATISTICS Q3 WEEK-9 Revision-3ace fuentesNo ratings yet

- Reading and Writing Q2 M11Document19 pagesReading and Writing Q2 M11Justine Mark GuzmanNo ratings yet

- Virtual Meet GMDocument34 pagesVirtual Meet GMLea Mae Vivo GeleraNo ratings yet

- WW6 7 Self Learning ModuleDocument27 pagesWW6 7 Self Learning ModuleIrish MendozaNo ratings yet

- Piecewise and Inverse Functions and Composition of FunctionsDocument35 pagesPiecewise and Inverse Functions and Composition of FunctionsDCHKLian 17100% (1)

- Simple and General AnnuitiesDocument12 pagesSimple and General AnnuitiesEarl Clyde BañezNo ratings yet

- Automotive 11 Summative Test 11 Second SemDocument1 pageAutomotive 11 Summative Test 11 Second Semelma anacleto100% (1)

- Front Office Services Second Quarter Summative TestDocument4 pagesFront Office Services Second Quarter Summative Testelma anacleto100% (2)

- APPLIED ECONOMIC Summative TestDocument4 pagesAPPLIED ECONOMIC Summative Testelma anacleto80% (5)

- Subject: General ChemistryDocument2 pagesSubject: General Chemistryelma anacletoNo ratings yet

- Module 5 (Week 7 and 8)Document11 pagesModule 5 (Week 7 and 8)elma anacletoNo ratings yet

- Contemporary Module 1Document18 pagesContemporary Module 1elma anacleto100% (1)

- Part III: Read The Following Question and Write The Correct Answer in Separate Sheet of PaperDocument1 pagePart III: Read The Following Question and Write The Correct Answer in Separate Sheet of Paperelma anacletoNo ratings yet

- SUBJECT SYLLABUS - Filipino Sa Piling LaranganDocument3 pagesSUBJECT SYLLABUS - Filipino Sa Piling Laranganelma anacletoNo ratings yet

- Housekeeping 11 Second Quarter Summative TestDocument2 pagesHousekeeping 11 Second Quarter Summative Testelma anacleto100% (2)

- Objectives: Holt Algebra 2Document14 pagesObjectives: Holt Algebra 2elma anacletoNo ratings yet

- RequestDocument1 pageRequestelma anacletoNo ratings yet

- ReferencesDocument9 pagesReferenceselma anacletoNo ratings yet

- Task Sheet 1.1-4: Title: Assemble Computer HardwareDocument1 pageTask Sheet 1.1-4: Title: Assemble Computer Hardwareelma anacletoNo ratings yet

- DRRM Module 1Document10 pagesDRRM Module 1elma anacletoNo ratings yet

- Literature Broadly Is Any Collection Of: o o o o o o o o o o o o o o oDocument6 pagesLiterature Broadly Is Any Collection Of: o o o o o o o o o o o o o o oelma anacletoNo ratings yet

- This Article Is About The Field of StudyDocument5 pagesThis Article Is About The Field of Studyelma anacletoNo ratings yet

- Relationships: - in Bibliographic Records and in Authority RecordsDocument46 pagesRelationships: - in Bibliographic Records and in Authority Recordselma anacletoNo ratings yet

- Eustress or Distress An Empirical Study of PerceivDocument10 pagesEustress or Distress An Empirical Study of Perceivelma anacletoNo ratings yet

- Task Sheet Title: Installing An Application Performance ObjectiveDocument2 pagesTask Sheet Title: Installing An Application Performance Objectiveelma anacletoNo ratings yet

- What Is ICTDocument1 pageWhat Is ICTelma anacletoNo ratings yet

- Rolly Japitana Salinas JRDocument3 pagesRolly Japitana Salinas JRelma anacletoNo ratings yet

- Banking Operation &management: Presidency CollegeDocument46 pagesBanking Operation &management: Presidency CollegeKaran RajNo ratings yet

- FAQ Business Direct 1Document15 pagesFAQ Business Direct 1maryrobert8322No ratings yet

- Doomsday CycleDocument5 pagesDoomsday CyclenovriadyNo ratings yet

- SS 2 Store MGT Third Term E-Learning NoteDocument38 pagesSS 2 Store MGT Third Term E-Learning Notepalmer okiemuteNo ratings yet

- Ibps Po MainsDocument169 pagesIbps Po MainsSaurabh AnandNo ratings yet

- Test Bank For Corporate Finance 13th Stephen Ross Randolph Westerfield Jeffrey JaffeDocument54 pagesTest Bank For Corporate Finance 13th Stephen Ross Randolph Westerfield Jeffrey Jaffemarcuskenyatta275No ratings yet

- Impact of Demonetization On Microfinance SectorDocument4 pagesImpact of Demonetization On Microfinance SectorGibin KollamparambilNo ratings yet

- Peer-Review Assessment Course 1aDocument5 pagesPeer-Review Assessment Course 1aSamael LightbringerNo ratings yet

- Chapter 3. Solution Exercises Income StatementDocument13 pagesChapter 3. Solution Exercises Income StatementHECTOR ORTEGANo ratings yet

- Royal Bank of Scotland: Corporate Rap SheetDocument9 pagesRoyal Bank of Scotland: Corporate Rap SheetMohsen KhanNo ratings yet

- Priyadarshini Spinning Mills Ltd-Winding Up NoticeDocument3 pagesPriyadarshini Spinning Mills Ltd-Winding Up NoticeAbhijit TripathiNo ratings yet

- Simple Interest Worksheet 1Document2 pagesSimple Interest Worksheet 1vajoorbiNo ratings yet

- Current LiabilitiesDocument94 pagesCurrent LiabilitiesDawit TilahunNo ratings yet

- HDFC SL CrestDocument1 pageHDFC SL Crestk_kishan288No ratings yet

- The Income StatementDocument10 pagesThe Income Statementayoub mechouatNo ratings yet

- Universal LoanDocument4 pagesUniversal LoanOlivia AvaNo ratings yet

- Fifteen Transactions or Events Affecting Computer Specialists Inc Are AsDocument1 pageFifteen Transactions or Events Affecting Computer Specialists Inc Are Astrilocksp SinghNo ratings yet

- PRR Edu11-2019Document14,118 pagesPRR Edu11-2019attaNo ratings yet

- Dr. M.G.R Educational and Research Instution, ChennaiDocument54 pagesDr. M.G.R Educational and Research Instution, ChennaiVijay MNo ratings yet

- Deutsche UFG Capital Management - ENGDocument28 pagesDeutsche UFG Capital Management - ENGAnton DenisovNo ratings yet

- Study On Capital MarketsDocument78 pagesStudy On Capital Marketsmanuuu patel0% (1)

- CFM AssignmentDocument26 pagesCFM AssignmentNaman VarshneyNo ratings yet

- Group 5 PresentationDocument10 pagesGroup 5 PresentationGervinBulataoNo ratings yet

- Darpan Kumar 100014663 Proposal No: Save & Assure Investment Secure Fund (SA) Fund: Plan: Alac-Banca-Mcb-St-Suk BranchDocument4 pagesDarpan Kumar 100014663 Proposal No: Save & Assure Investment Secure Fund (SA) Fund: Plan: Alac-Banca-Mcb-St-Suk BranchHaris AliNo ratings yet

- Chemical RatesDocument12 pagesChemical RatesKABIR CHOPRANo ratings yet

- Instructional Planning: Detailed Lesson Plan (DLP) FormatDocument5 pagesInstructional Planning: Detailed Lesson Plan (DLP) FormatDaisy PaoNo ratings yet

- Chapter 5: Books of Accounts & Double-Entry System (FAR By: Millan)Document17 pagesChapter 5: Books of Accounts & Double-Entry System (FAR By: Millan)Portia AbestanoNo ratings yet