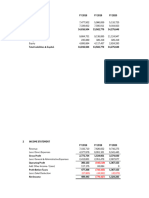

Financial Plan - Cakes Inside

Financial Plan - Cakes Inside

You might also like

- Class Case 3 - There's More To Us Than Meets The EyeDocument11 pagesClass Case 3 - There's More To Us Than Meets The EyeHannahPojaFeria50% (2)

- Forecasting ProblemsDocument7 pagesForecasting ProblemsJoel Pangisban0% (3)

- Estimation of Doubtful Accounts: Problem 12-1 (AICPA Adapted)Document15 pagesEstimation of Doubtful Accounts: Problem 12-1 (AICPA Adapted)Janine Lerum100% (2)

- Past Exam Answer Key (To Consol BS)Document53 pagesPast Exam Answer Key (To Consol BS)Huệ LêNo ratings yet

- Mayes 8e CH05 SolutionsDocument36 pagesMayes 8e CH05 SolutionsRamez AhmedNo ratings yet

- Riel Corporation Comparative Statements of Financial Position December 31, 2025 Increase (Decrease) 2025 2024 Amount PercentDocument6 pagesRiel Corporation Comparative Statements of Financial Position December 31, 2025 Increase (Decrease) 2025 2024 Amount PercentKitheia Ostrava Reisenchauer100% (3)

- P and L PDFDocument2 pagesP and L PDFjigar jainNo ratings yet

- Sample Financial PlanDocument19 pagesSample Financial PlanAlexandria GonzalesNo ratings yet

- Learning Activity 5 - Financial PlanDocument6 pagesLearning Activity 5 - Financial PlanGeryca CarranzaNo ratings yet

- SWOT of EIH Ltd.Document13 pagesSWOT of EIH Ltd.Sahil AhammedNo ratings yet

- HCL Technologies: PrintDocument2 pagesHCL Technologies: PrintSachin SinghNo ratings yet

- Cakes Inside: Biratnagar, NepalDocument23 pagesCakes Inside: Biratnagar, NepalDenimNo ratings yet

- Discounted Cash FlowDocument9 pagesDiscounted Cash FlowAditya JandialNo ratings yet

- Balance Sheet of Reliance IndustriesDocument12 pagesBalance Sheet of Reliance IndustriesMohit Kumar SinghNo ratings yet

- CHAPTER 4 Financials Velas Encendida Candles 3 12 19Document18 pagesCHAPTER 4 Financials Velas Encendida Candles 3 12 19JenilynNo ratings yet

- Group AssignmentDocument6 pagesGroup AssignmentIshiyaku Adamu NjiddaNo ratings yet

- Financial-Assignment - Nagarjuna Reddy (18MBARB025)Document16 pagesFinancial-Assignment - Nagarjuna Reddy (18MBARB025)Raghava JinkaNo ratings yet

- Financial PlanDocument7 pagesFinancial PlanGeryca CarranzaNo ratings yet

- Panda Eco System Berhad - Prospectus Dated 8 November 2023 (Part 3)Document172 pagesPanda Eco System Berhad - Prospectus Dated 8 November 2023 (Part 3)geniuskkNo ratings yet

- HDFC Bank Ratio AnalysisDocument14 pagesHDFC Bank Ratio Analysissunnykumar.m2325No ratings yet

- Ratio ... Financial StatementsDocument17 pagesRatio ... Financial Statementsjinsha firozNo ratings yet

- Fina 004Document4 pagesFina 004Mike RajasNo ratings yet

- Binish M ModelDocument8 pagesBinish M ModellyrastarfallauthorNo ratings yet

- UploadDocument83 pagesUploadAli BMSNo ratings yet

- Audit - QuestionsDocument6 pagesAudit - Questionsnaveen pragashNo ratings yet

- Case Study 2Document4 pagesCase Study 2Sarwanti PurwandariNo ratings yet

- Hindalco Company's Finance DepartmentDocument14 pagesHindalco Company's Finance DepartmentJaydeep SolankiNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument8 pagesFinancial Statements, Cash Flow, and TaxesRaihan Eibna RezaNo ratings yet

- Financial Report For The Year 2020-21-DDocument74 pagesFinancial Report For The Year 2020-21-DAmanuel TewoldeNo ratings yet

- Projected Statement of Financial PerformanceDocument7 pagesProjected Statement of Financial PerformanceAngelli LamiqueNo ratings yet

- Financial Model 3 Statement Model - Final - MotilalDocument13 pagesFinancial Model 3 Statement Model - Final - MotilalSouvik BardhanNo ratings yet

- Lecture - 5 - CFI-3-statement-model-completeDocument37 pagesLecture - 5 - CFI-3-statement-model-completeshreyasNo ratings yet

- Saif Powetc Ltd. - Aameer 23068 (C)Document13 pagesSaif Powetc Ltd. - Aameer 23068 (C)Aameer ShahansahNo ratings yet

- Financia ASPECT - AlarmDocument26 pagesFinancia ASPECT - AlarmEumar FabruadaNo ratings yet

- Illustrative Full Set of IFRS For SME Financial StatementsDocument16 pagesIllustrative Full Set of IFRS For SME Financial StatementsGirma NegashNo ratings yet

- ANSWERS For Horizontal Analysis Application-CBA CorporationDocument4 pagesANSWERS For Horizontal Analysis Application-CBA CorporationYhadNo ratings yet

- Financial PlanDocument20 pagesFinancial Planzhijaescosio25No ratings yet

- Unity Food QR Sep 2021 (Nov 02)Document31 pagesUnity Food QR Sep 2021 (Nov 02)Sohail MehmoodNo ratings yet

- 1st-Case-Study - Financial-Statement-Analysis - Group 5Document18 pages1st-Case-Study - Financial-Statement-Analysis - Group 5gellie villarinNo ratings yet

- Apple FinancialDocument8 pagesApple FinancialmeoboyNo ratings yet

- Business PlanDocument11 pagesBusiness Plananil thapaNo ratings yet

- Solution Q1Document10 pagesSolution Q1سنبل ملکNo ratings yet

- Financial StatementsDocument14 pagesFinancial Statementsthenal kulandaianNo ratings yet

- Corporate Reporting Ma-2023 QuestionDocument6 pagesCorporate Reporting Ma-2023 QuestionMDSadeq-ulIslamNo ratings yet

- Nippon Life India Asset Management Profit & Loss Account, Nippon Life India Asset Management Financial Statement & AccountsDocument1 pageNippon Life India Asset Management Profit & Loss Account, Nippon Life India Asset Management Financial Statement & AccountsToxic MaviNo ratings yet

- RBA+FINANCE AssignmentDocument5 pagesRBA+FINANCE AssignmentAbhishek mudaliarNo ratings yet

- Hindustanprofit LossDocument2 pagesHindustanprofit LossPradeep WaghNo ratings yet

- Financial PlanningDocument22 pagesFinancial Planningangshu002085% (13)

- EVA ExampleDocument27 pagesEVA Examplewelcome2jungleNo ratings yet

- Assignment: Topic: Financial Statement Analysis of National Bank of PakistanDocument28 pagesAssignment: Topic: Financial Statement Analysis of National Bank of PakistanSadaf AliNo ratings yet

- Rak Ceramics: Income StatementDocument27 pagesRak Ceramics: Income StatementRafsan JahangirNo ratings yet

- Dalmia Bharat Sugar and Industries Ltd.Document19 pagesDalmia Bharat Sugar and Industries Ltd.Shweta GargNo ratings yet

- ABS CBN CorporationDocument16 pagesABS CBN CorporationAlyssa BeatriceNo ratings yet

- Income Statement of Apple IncDocument6 pagesIncome Statement of Apple IncBharat PanthiNo ratings yet

- Lakh Datta Flour MillsDocument14 pagesLakh Datta Flour MillsjimmuNo ratings yet

- Description Variable 2008: Financial Leverege (Nfo/cse)Document9 pagesDescription Variable 2008: Financial Leverege (Nfo/cse)Nizam Uddin MasudNo ratings yet

- Acct 401 Tutorial Set FiveDocument13 pagesAcct 401 Tutorial Set FiveStudy GirlNo ratings yet

- Print Financials (PL)Document2 pagesPrint Financials (PL)aslam khanNo ratings yet

- Income and Project Balance SheetDocument1 pageIncome and Project Balance SheetAbu SayedNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Distribution Channels and Logistics ManagementDocument22 pagesDistribution Channels and Logistics ManagementDenimNo ratings yet

- Defination of TermsDocument14 pagesDefination of TermsDenimNo ratings yet

- Taxation Remuneration IncomeDocument10 pagesTaxation Remuneration IncomeDenimNo ratings yet

- Survey On "Employee Satisfaction of Janata Bank Nepal Limited"Document29 pagesSurvey On "Employee Satisfaction of Janata Bank Nepal Limited"DenimNo ratings yet

- Damodar Lamsal: Concept of Employment or RemunerationDocument12 pagesDamodar Lamsal: Concept of Employment or RemunerationDenimNo ratings yet

- Integrated Marketing Communication StrategyDocument11 pagesIntegrated Marketing Communication StrategyDenimNo ratings yet

- Tourism Policy, Planning and Sustainable DevelopmentDocument13 pagesTourism Policy, Planning and Sustainable DevelopmentDenimNo ratings yet

- Pricing Products: Pricing Considerations and ApproachesDocument31 pagesPricing Products: Pricing Considerations and ApproachesDenimNo ratings yet

- Tourism in NepalDocument26 pagesTourism in NepalDenimNo ratings yet

- Ecommerce Project ReportDocument15 pagesEcommerce Project ReportDenimNo ratings yet

- Future of TourismDocument11 pagesFuture of TourismDenimNo ratings yet

- Cakes Inside: Biratnagar, NepalDocument23 pagesCakes Inside: Biratnagar, NepalDenimNo ratings yet

- 1.1 Background of The StudyDocument7 pages1.1 Background of The StudyDenimNo ratings yet

- Management Accounting - NotebookDocument15 pagesManagement Accounting - NotebookDenimNo ratings yet

- Business Development Plan For V2 Travel: Submitted To: Sohan Babu KhatriDocument58 pagesBusiness Development Plan For V2 Travel: Submitted To: Sohan Babu KhatriDenimNo ratings yet

- Benefits of Internet To Business - 2Document3 pagesBenefits of Internet To Business - 2DenimNo ratings yet

- Choosing Payments MethodDocument3 pagesChoosing Payments MethodDenimNo ratings yet

- Assignment of International Finance Management: Q.N. 26) What Is Emerging Markets MSCI?Document2 pagesAssignment of International Finance Management: Q.N. 26) What Is Emerging Markets MSCI?DenimNo ratings yet

- What Is Business Intelligence?Document5 pagesWhat Is Business Intelligence?DenimNo ratings yet

- Labour Act, 1992: Chapter - 1Document5 pagesLabour Act, 1992: Chapter - 1DenimNo ratings yet

- Benefits of Internet To Business - 1Document1 pageBenefits of Internet To Business - 1DenimNo ratings yet

- Mas 1Document12 pagesMas 1HURLY BALANCARNo ratings yet

- Account Formats and Statements LayoutsDocument5 pagesAccount Formats and Statements LayoutsCynNo ratings yet

- To RSA - ERDB AOM 2019-06 (2018) Non-Submission of ReportsDocument5 pagesTo RSA - ERDB AOM 2019-06 (2018) Non-Submission of ReportsJean Monique Oabel-TolentinoNo ratings yet

- Adjusting Entries ProblemsDocument5 pagesAdjusting Entries ProblemsSharmaine manobanNo ratings yet

- Acctg 102 - Prelim Exams - 3048Document3 pagesAcctg 102 - Prelim Exams - 3048AYAME MALINAO BSA19No ratings yet

- AT Quizzer 6 - Planning and Risk Assessment PDFDocument18 pagesAT Quizzer 6 - Planning and Risk Assessment PDFJimmyChao0% (1)

- Recognition of Construction Contract Revenue Based On PSAK 34 at PT Tunggal Jaya RayaDocument8 pagesRecognition of Construction Contract Revenue Based On PSAK 34 at PT Tunggal Jaya RayamegakadirNo ratings yet

- Activity 1 Home Office and Branch Accounting - General ProceduresDocument4 pagesActivity 1 Home Office and Branch Accounting - General ProceduresDaenielle EspinozaNo ratings yet

- Scientific Application of SCS in Manufacturing IndustriesDocument7 pagesScientific Application of SCS in Manufacturing IndustrieskrisNo ratings yet

- Cash FlowDocument81 pagesCash FlowRoy Van de SimanjuntakNo ratings yet

- Accounting For Property, Plant and Equipment - ACCA Global - 1621239130982Document13 pagesAccounting For Property, Plant and Equipment - ACCA Global - 1621239130982Farhan Osman ahmedNo ratings yet

- Principles of Auditing - Chapter - 2Document33 pagesPrinciples of Auditing - Chapter - 2Wijdan Saleem EdwanNo ratings yet

- Henry David Thoreau Civil Disobedience EssayDocument3 pagesHenry David Thoreau Civil Disobedience Essaydunqfacaf100% (2)

- 3 Accounting MechanicsDocument50 pages3 Accounting MechanicsVasu Narang100% (1)

- FAR-4105 INVENTORIES - Part 2Document3 pagesFAR-4105 INVENTORIES - Part 2music niNo ratings yet

- ACC 100 EXERCISES Topic 1 and 2 - 2024Document5 pagesACC 100 EXERCISES Topic 1 and 2 - 2024deklerkkimberey45No ratings yet

- Notes To Coursework 1314Document15 pagesNotes To Coursework 1314Quynh TranNo ratings yet

- Assignment #2 FABMDocument5 pagesAssignment #2 FABMIce Voltaire B. Guiang100% (1)

- Group 6 - Audit of The Acquisition and Payment CycleDocument20 pagesGroup 6 - Audit of The Acquisition and Payment CycleEsti SetianingsihNo ratings yet

- (New Client Acceptance) Comprehensive Case: Mt. Hood Furniture, Inc. Company Background Information: Your Employer, Reddy & Abel, LLP, CertifiedDocument5 pages(New Client Acceptance) Comprehensive Case: Mt. Hood Furniture, Inc. Company Background Information: Your Employer, Reddy & Abel, LLP, CertifiedRandy KuswantoNo ratings yet

- R12 GL StudyDocument60 pagesR12 GL StudySingh Anish K.No ratings yet

- Olaf Distributing Company Completed The Following Merchandising PDFDocument1 pageOlaf Distributing Company Completed The Following Merchandising PDFAnbu jaromiaNo ratings yet

- Going ConcernDocument3 pagesGoing Concernstejar123No ratings yet

- p1 Mo - Bak.unlockedDocument48 pagesp1 Mo - Bak.unlockedUmer PrinceNo ratings yet

- Fundamentals of Accountancy Business and Management II 2nd QDocument14 pagesFundamentals of Accountancy Business and Management II 2nd QAnonymousNo ratings yet

- Classified2018 1 28759349Document9 pagesClassified2018 1 28759349maheshNo ratings yet

- Acc Quizzes ZZZDocument22 pagesAcc Quizzes ZZZagspurealNo ratings yet

- New Syllabus PDFDocument251 pagesNew Syllabus PDFsunethraa swamyNo ratings yet

You might also like

- Class Case 3 - There's More To Us Than Meets The EyeDocument11 pagesClass Case 3 - There's More To Us Than Meets The EyeHannahPojaFeria50% (2)

- Forecasting ProblemsDocument7 pagesForecasting ProblemsJoel Pangisban0% (3)

- Estimation of Doubtful Accounts: Problem 12-1 (AICPA Adapted)Document15 pagesEstimation of Doubtful Accounts: Problem 12-1 (AICPA Adapted)Janine Lerum100% (2)

- Past Exam Answer Key (To Consol BS)Document53 pagesPast Exam Answer Key (To Consol BS)Huệ LêNo ratings yet

- Mayes 8e CH05 SolutionsDocument36 pagesMayes 8e CH05 SolutionsRamez AhmedNo ratings yet

- Riel Corporation Comparative Statements of Financial Position December 31, 2025 Increase (Decrease) 2025 2024 Amount PercentDocument6 pagesRiel Corporation Comparative Statements of Financial Position December 31, 2025 Increase (Decrease) 2025 2024 Amount PercentKitheia Ostrava Reisenchauer100% (3)

- P and L PDFDocument2 pagesP and L PDFjigar jainNo ratings yet

- Sample Financial PlanDocument19 pagesSample Financial PlanAlexandria GonzalesNo ratings yet

- Learning Activity 5 - Financial PlanDocument6 pagesLearning Activity 5 - Financial PlanGeryca CarranzaNo ratings yet

- SWOT of EIH Ltd.Document13 pagesSWOT of EIH Ltd.Sahil AhammedNo ratings yet

- HCL Technologies: PrintDocument2 pagesHCL Technologies: PrintSachin SinghNo ratings yet

- Cakes Inside: Biratnagar, NepalDocument23 pagesCakes Inside: Biratnagar, NepalDenimNo ratings yet

- Discounted Cash FlowDocument9 pagesDiscounted Cash FlowAditya JandialNo ratings yet

- Balance Sheet of Reliance IndustriesDocument12 pagesBalance Sheet of Reliance IndustriesMohit Kumar SinghNo ratings yet

- CHAPTER 4 Financials Velas Encendida Candles 3 12 19Document18 pagesCHAPTER 4 Financials Velas Encendida Candles 3 12 19JenilynNo ratings yet

- Group AssignmentDocument6 pagesGroup AssignmentIshiyaku Adamu NjiddaNo ratings yet

- Financial-Assignment - Nagarjuna Reddy (18MBARB025)Document16 pagesFinancial-Assignment - Nagarjuna Reddy (18MBARB025)Raghava JinkaNo ratings yet

- Financial PlanDocument7 pagesFinancial PlanGeryca CarranzaNo ratings yet

- Panda Eco System Berhad - Prospectus Dated 8 November 2023 (Part 3)Document172 pagesPanda Eco System Berhad - Prospectus Dated 8 November 2023 (Part 3)geniuskkNo ratings yet

- HDFC Bank Ratio AnalysisDocument14 pagesHDFC Bank Ratio Analysissunnykumar.m2325No ratings yet

- Ratio ... Financial StatementsDocument17 pagesRatio ... Financial Statementsjinsha firozNo ratings yet

- Fina 004Document4 pagesFina 004Mike RajasNo ratings yet

- Binish M ModelDocument8 pagesBinish M ModellyrastarfallauthorNo ratings yet

- UploadDocument83 pagesUploadAli BMSNo ratings yet

- Audit - QuestionsDocument6 pagesAudit - Questionsnaveen pragashNo ratings yet

- Case Study 2Document4 pagesCase Study 2Sarwanti PurwandariNo ratings yet

- Hindalco Company's Finance DepartmentDocument14 pagesHindalco Company's Finance DepartmentJaydeep SolankiNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument8 pagesFinancial Statements, Cash Flow, and TaxesRaihan Eibna RezaNo ratings yet

- Financial Report For The Year 2020-21-DDocument74 pagesFinancial Report For The Year 2020-21-DAmanuel TewoldeNo ratings yet

- Projected Statement of Financial PerformanceDocument7 pagesProjected Statement of Financial PerformanceAngelli LamiqueNo ratings yet

- Financial Model 3 Statement Model - Final - MotilalDocument13 pagesFinancial Model 3 Statement Model - Final - MotilalSouvik BardhanNo ratings yet

- Lecture - 5 - CFI-3-statement-model-completeDocument37 pagesLecture - 5 - CFI-3-statement-model-completeshreyasNo ratings yet

- Saif Powetc Ltd. - Aameer 23068 (C)Document13 pagesSaif Powetc Ltd. - Aameer 23068 (C)Aameer ShahansahNo ratings yet

- Financia ASPECT - AlarmDocument26 pagesFinancia ASPECT - AlarmEumar FabruadaNo ratings yet

- Illustrative Full Set of IFRS For SME Financial StatementsDocument16 pagesIllustrative Full Set of IFRS For SME Financial StatementsGirma NegashNo ratings yet

- ANSWERS For Horizontal Analysis Application-CBA CorporationDocument4 pagesANSWERS For Horizontal Analysis Application-CBA CorporationYhadNo ratings yet

- Financial PlanDocument20 pagesFinancial Planzhijaescosio25No ratings yet

- Unity Food QR Sep 2021 (Nov 02)Document31 pagesUnity Food QR Sep 2021 (Nov 02)Sohail MehmoodNo ratings yet

- 1st-Case-Study - Financial-Statement-Analysis - Group 5Document18 pages1st-Case-Study - Financial-Statement-Analysis - Group 5gellie villarinNo ratings yet

- Apple FinancialDocument8 pagesApple FinancialmeoboyNo ratings yet

- Business PlanDocument11 pagesBusiness Plananil thapaNo ratings yet

- Solution Q1Document10 pagesSolution Q1سنبل ملکNo ratings yet

- Financial StatementsDocument14 pagesFinancial Statementsthenal kulandaianNo ratings yet

- Corporate Reporting Ma-2023 QuestionDocument6 pagesCorporate Reporting Ma-2023 QuestionMDSadeq-ulIslamNo ratings yet

- Nippon Life India Asset Management Profit & Loss Account, Nippon Life India Asset Management Financial Statement & AccountsDocument1 pageNippon Life India Asset Management Profit & Loss Account, Nippon Life India Asset Management Financial Statement & AccountsToxic MaviNo ratings yet

- RBA+FINANCE AssignmentDocument5 pagesRBA+FINANCE AssignmentAbhishek mudaliarNo ratings yet

- Hindustanprofit LossDocument2 pagesHindustanprofit LossPradeep WaghNo ratings yet

- Financial PlanningDocument22 pagesFinancial Planningangshu002085% (13)

- EVA ExampleDocument27 pagesEVA Examplewelcome2jungleNo ratings yet

- Assignment: Topic: Financial Statement Analysis of National Bank of PakistanDocument28 pagesAssignment: Topic: Financial Statement Analysis of National Bank of PakistanSadaf AliNo ratings yet

- Rak Ceramics: Income StatementDocument27 pagesRak Ceramics: Income StatementRafsan JahangirNo ratings yet

- Dalmia Bharat Sugar and Industries Ltd.Document19 pagesDalmia Bharat Sugar and Industries Ltd.Shweta GargNo ratings yet

- ABS CBN CorporationDocument16 pagesABS CBN CorporationAlyssa BeatriceNo ratings yet

- Income Statement of Apple IncDocument6 pagesIncome Statement of Apple IncBharat PanthiNo ratings yet

- Lakh Datta Flour MillsDocument14 pagesLakh Datta Flour MillsjimmuNo ratings yet

- Description Variable 2008: Financial Leverege (Nfo/cse)Document9 pagesDescription Variable 2008: Financial Leverege (Nfo/cse)Nizam Uddin MasudNo ratings yet

- Acct 401 Tutorial Set FiveDocument13 pagesAcct 401 Tutorial Set FiveStudy GirlNo ratings yet

- Print Financials (PL)Document2 pagesPrint Financials (PL)aslam khanNo ratings yet

- Income and Project Balance SheetDocument1 pageIncome and Project Balance SheetAbu SayedNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Distribution Channels and Logistics ManagementDocument22 pagesDistribution Channels and Logistics ManagementDenimNo ratings yet

- Defination of TermsDocument14 pagesDefination of TermsDenimNo ratings yet

- Taxation Remuneration IncomeDocument10 pagesTaxation Remuneration IncomeDenimNo ratings yet

- Survey On "Employee Satisfaction of Janata Bank Nepal Limited"Document29 pagesSurvey On "Employee Satisfaction of Janata Bank Nepal Limited"DenimNo ratings yet

- Damodar Lamsal: Concept of Employment or RemunerationDocument12 pagesDamodar Lamsal: Concept of Employment or RemunerationDenimNo ratings yet

- Integrated Marketing Communication StrategyDocument11 pagesIntegrated Marketing Communication StrategyDenimNo ratings yet

- Tourism Policy, Planning and Sustainable DevelopmentDocument13 pagesTourism Policy, Planning and Sustainable DevelopmentDenimNo ratings yet

- Pricing Products: Pricing Considerations and ApproachesDocument31 pagesPricing Products: Pricing Considerations and ApproachesDenimNo ratings yet

- Tourism in NepalDocument26 pagesTourism in NepalDenimNo ratings yet

- Ecommerce Project ReportDocument15 pagesEcommerce Project ReportDenimNo ratings yet

- Future of TourismDocument11 pagesFuture of TourismDenimNo ratings yet

- Cakes Inside: Biratnagar, NepalDocument23 pagesCakes Inside: Biratnagar, NepalDenimNo ratings yet

- 1.1 Background of The StudyDocument7 pages1.1 Background of The StudyDenimNo ratings yet

- Management Accounting - NotebookDocument15 pagesManagement Accounting - NotebookDenimNo ratings yet

- Business Development Plan For V2 Travel: Submitted To: Sohan Babu KhatriDocument58 pagesBusiness Development Plan For V2 Travel: Submitted To: Sohan Babu KhatriDenimNo ratings yet

- Benefits of Internet To Business - 2Document3 pagesBenefits of Internet To Business - 2DenimNo ratings yet

- Choosing Payments MethodDocument3 pagesChoosing Payments MethodDenimNo ratings yet

- Assignment of International Finance Management: Q.N. 26) What Is Emerging Markets MSCI?Document2 pagesAssignment of International Finance Management: Q.N. 26) What Is Emerging Markets MSCI?DenimNo ratings yet

- What Is Business Intelligence?Document5 pagesWhat Is Business Intelligence?DenimNo ratings yet

- Labour Act, 1992: Chapter - 1Document5 pagesLabour Act, 1992: Chapter - 1DenimNo ratings yet

- Benefits of Internet To Business - 1Document1 pageBenefits of Internet To Business - 1DenimNo ratings yet

- Mas 1Document12 pagesMas 1HURLY BALANCARNo ratings yet

- Account Formats and Statements LayoutsDocument5 pagesAccount Formats and Statements LayoutsCynNo ratings yet

- To RSA - ERDB AOM 2019-06 (2018) Non-Submission of ReportsDocument5 pagesTo RSA - ERDB AOM 2019-06 (2018) Non-Submission of ReportsJean Monique Oabel-TolentinoNo ratings yet

- Adjusting Entries ProblemsDocument5 pagesAdjusting Entries ProblemsSharmaine manobanNo ratings yet

- Acctg 102 - Prelim Exams - 3048Document3 pagesAcctg 102 - Prelim Exams - 3048AYAME MALINAO BSA19No ratings yet

- AT Quizzer 6 - Planning and Risk Assessment PDFDocument18 pagesAT Quizzer 6 - Planning and Risk Assessment PDFJimmyChao0% (1)

- Recognition of Construction Contract Revenue Based On PSAK 34 at PT Tunggal Jaya RayaDocument8 pagesRecognition of Construction Contract Revenue Based On PSAK 34 at PT Tunggal Jaya RayamegakadirNo ratings yet

- Activity 1 Home Office and Branch Accounting - General ProceduresDocument4 pagesActivity 1 Home Office and Branch Accounting - General ProceduresDaenielle EspinozaNo ratings yet

- Scientific Application of SCS in Manufacturing IndustriesDocument7 pagesScientific Application of SCS in Manufacturing IndustrieskrisNo ratings yet

- Cash FlowDocument81 pagesCash FlowRoy Van de SimanjuntakNo ratings yet

- Accounting For Property, Plant and Equipment - ACCA Global - 1621239130982Document13 pagesAccounting For Property, Plant and Equipment - ACCA Global - 1621239130982Farhan Osman ahmedNo ratings yet

- Principles of Auditing - Chapter - 2Document33 pagesPrinciples of Auditing - Chapter - 2Wijdan Saleem EdwanNo ratings yet

- Henry David Thoreau Civil Disobedience EssayDocument3 pagesHenry David Thoreau Civil Disobedience Essaydunqfacaf100% (2)

- 3 Accounting MechanicsDocument50 pages3 Accounting MechanicsVasu Narang100% (1)

- FAR-4105 INVENTORIES - Part 2Document3 pagesFAR-4105 INVENTORIES - Part 2music niNo ratings yet

- ACC 100 EXERCISES Topic 1 and 2 - 2024Document5 pagesACC 100 EXERCISES Topic 1 and 2 - 2024deklerkkimberey45No ratings yet

- Notes To Coursework 1314Document15 pagesNotes To Coursework 1314Quynh TranNo ratings yet

- Assignment #2 FABMDocument5 pagesAssignment #2 FABMIce Voltaire B. Guiang100% (1)

- Group 6 - Audit of The Acquisition and Payment CycleDocument20 pagesGroup 6 - Audit of The Acquisition and Payment CycleEsti SetianingsihNo ratings yet

- (New Client Acceptance) Comprehensive Case: Mt. Hood Furniture, Inc. Company Background Information: Your Employer, Reddy & Abel, LLP, CertifiedDocument5 pages(New Client Acceptance) Comprehensive Case: Mt. Hood Furniture, Inc. Company Background Information: Your Employer, Reddy & Abel, LLP, CertifiedRandy KuswantoNo ratings yet

- R12 GL StudyDocument60 pagesR12 GL StudySingh Anish K.No ratings yet

- Olaf Distributing Company Completed The Following Merchandising PDFDocument1 pageOlaf Distributing Company Completed The Following Merchandising PDFAnbu jaromiaNo ratings yet

- Going ConcernDocument3 pagesGoing Concernstejar123No ratings yet

- p1 Mo - Bak.unlockedDocument48 pagesp1 Mo - Bak.unlockedUmer PrinceNo ratings yet

- Fundamentals of Accountancy Business and Management II 2nd QDocument14 pagesFundamentals of Accountancy Business and Management II 2nd QAnonymousNo ratings yet

- Classified2018 1 28759349Document9 pagesClassified2018 1 28759349maheshNo ratings yet

- Acc Quizzes ZZZDocument22 pagesAcc Quizzes ZZZagspurealNo ratings yet

- New Syllabus PDFDocument251 pagesNew Syllabus PDFsunethraa swamyNo ratings yet