Download as pdf or txt

You might also like

- PFRS 15 Revenue From Contracts With CustomersDocument7 pagesPFRS 15 Revenue From Contracts With Customerspanda 1100% (2)

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- AFAR-04: PFRS 15 - Revenue From Contracts With Customers & Other TopicsDocument14 pagesAFAR-04: PFRS 15 - Revenue From Contracts With Customers & Other TopicsJenver BuenaventuraNo ratings yet

- Chapter 3 PracticesDocument21 pagesChapter 3 Practiceskakao50% (2)

- (AFAR) (S05) - PFRS 15, Installment Sales, and Consignment SalesDocument6 pages(AFAR) (S05) - PFRS 15, Installment Sales, and Consignment SalesPolinar Paul MarbenNo ratings yet

- PFRS 15, MarbellaDocument3 pagesPFRS 15, MarbellaDazzelle BasarteNo ratings yet

- IFRS 15 Revenue From Contracts With CustomersDocument5 pagesIFRS 15 Revenue From Contracts With CustomersADEYANJU AKEEMNo ratings yet

- Chapter 7 Revenue From Contracts With Customers SVDocument21 pagesChapter 7 Revenue From Contracts With Customers SV21073141No ratings yet

- Chap 2 Mod 1 Rev Rec Part I V2Document24 pagesChap 2 Mod 1 Rev Rec Part I V2hmaz.roid91No ratings yet

- Chapter 12 Revenue From Contracts With CustomersDocument24 pagesChapter 12 Revenue From Contracts With CustomersJane DizonNo ratings yet

- CFAS Unit 1 - Module 5.1Document11 pagesCFAS Unit 1 - Module 5.1Ralph Lefrancis DomingoNo ratings yet

- Accounting For Franchise Operations2Document21 pagesAccounting For Franchise Operations2Jaira Mae AustriaNo ratings yet

- Chapter 3 - RevenueDocument4 pagesChapter 3 - RevenuejasonNo ratings yet

- Revenues From Contracts With CustomersDocument8 pagesRevenues From Contracts With CustomersSandia EspejoNo ratings yet

- Ifrs 15Document6 pagesIfrs 15v0524 vNo ratings yet

- Revenue Ind AS 115Document54 pagesRevenue Ind AS 115amitguptasidNo ratings yet

- Chapter 6 Accounting For Franchise Operations - Franchisor-PROFE01Document7 pagesChapter 6 Accounting For Franchise Operations - Franchisor-PROFE01Steffany RoqueNo ratings yet

- Ifrs 15: Revenue From Contracts With CustomersDocument8 pagesIfrs 15: Revenue From Contracts With CustomersAira Nhaira MecateNo ratings yet

- MODULE 8 (Part 2)Document6 pagesMODULE 8 (Part 2)trixie maeNo ratings yet

- Ifrs 15 - Chapter 1Document7 pagesIfrs 15 - Chapter 1LumingNo ratings yet

- Engage - Revenue Recognition-1Document129 pagesEngage - Revenue Recognition-1Johhahawie jajwiNo ratings yet

- Ifrs 15: Revenue From Contracts With CustomersDocument4 pagesIfrs 15: Revenue From Contracts With CustomersALMA MORENA100% (2)

- IFRS 15 - Revenue From Contracts With CustomersDocument5 pagesIFRS 15 - Revenue From Contracts With CustomersAnkur MittalNo ratings yet

- Group 6-Psak 72 (Makalah) PDFDocument25 pagesGroup 6-Psak 72 (Makalah) PDFdwi davisNo ratings yet

- PFRS15Document14 pagesPFRS15cris allea catacutanNo ratings yet

- Accounting Theory - Revenue RecognitionDocument5 pagesAccounting Theory - Revenue RecognitionHeather Hudson100% (1)

- MODULE 1 - Revenue From Contracts With CustomersDocument12 pagesMODULE 1 - Revenue From Contracts With CustomersEdison Salgado CastigadorNo ratings yet

- Revenue From Contracts With CustomersDocument5 pagesRevenue From Contracts With Customers70fugnayjanetNo ratings yet

- IFRS 15 - Revenue From Contracts With CustomersDocument7 pagesIFRS 15 - Revenue From Contracts With CustomersamananandxNo ratings yet

- PWC Reportinginbrief Companies Indian Accounting Standards Amendment Rules 2018Document12 pagesPWC Reportinginbrief Companies Indian Accounting Standards Amendment Rules 2018sourabhbansal108No ratings yet

- PFRS 15Document3 pagesPFRS 15Micaella DanoNo ratings yet

- Construction ContractsDocument33 pagesConstruction ContractsJaira Mae AustriaNo ratings yet

- Ind As 115 VS Ind As 18Document7 pagesInd As 115 VS Ind As 18Yogendrasinh RaoNo ratings yet

- Revenue Revisited: The Global Body For Professional AccountantsDocument3 pagesRevenue Revisited: The Global Body For Professional AccountantsPANTUGNo ratings yet

- IFRS 15 Revenue From Contracts With CustomersDocument18 pagesIFRS 15 Revenue From Contracts With CustomersHamza JavaidNo ratings yet

- Revenue From Contracts With Customers: Pfrs 15Document23 pagesRevenue From Contracts With Customers: Pfrs 15Marimel TizonNo ratings yet

- Reviewer Pfrs 15 Revenue From Contracts With CustomersDocument4 pagesReviewer Pfrs 15 Revenue From Contracts With CustomersMaria TheresaNo ratings yet

- Advanced Financial Reporting ProjectDocument22 pagesAdvanced Financial Reporting ProjectAlen JoseNo ratings yet

- NFRS 15 - Revenue From Contracts With CustomerDocument18 pagesNFRS 15 - Revenue From Contracts With CustomerApilNo ratings yet

- IFRS 15 Revenue From Contracts With Customers-2Document8 pagesIFRS 15 Revenue From Contracts With Customers-2abbyNo ratings yet

- AFAR-06 (Revenue From Customer Contracts - Other Topics)Document26 pagesAFAR-06 (Revenue From Customer Contracts - Other Topics)mysweet surrenderNo ratings yet

- Week 3 IFRS 15-Revenue From Contracts With CustomersDocument20 pagesWeek 3 IFRS 15-Revenue From Contracts With CustomerskoketsoNo ratings yet

- Module 1 - PDFDocument4 pagesModule 1 - PDFMelanie SamsonaNo ratings yet

- Reviewer PFRS 15 Revenue From Contracts With CustomersDocument4 pagesReviewer PFRS 15 Revenue From Contracts With CustomersJezela CastilloNo ratings yet

- Chapter 6 - IFRS 15Document21 pagesChapter 6 - IFRS 15SaiNo ratings yet

- MODULE 3 - NotesDocument5 pagesMODULE 3 - NotesAravind YogeshNo ratings yet

- IFRS 15 RevenueDocument8 pagesIFRS 15 RevenueCatalin BlesnocNo ratings yet

- IFRS 15 (IAS) - Revenue From Contracts With CustomersDocument10 pagesIFRS 15 (IAS) - Revenue From Contracts With CustomersAngie MagnayeNo ratings yet

- AFAR-06 (Revenue From Contracts With Customers - Other Topics)Document26 pagesAFAR-06 (Revenue From Contracts With Customers - Other Topics)MABI ESPENIDONo ratings yet

- PSAK 72 - Revenue From Contracts With Customers: Alya Khaira Nazhifa (1710531009) Amelia Rahmadani P.A (1710531019)Document31 pagesPSAK 72 - Revenue From Contracts With Customers: Alya Khaira Nazhifa (1710531009) Amelia Rahmadani P.A (1710531019)ameNo ratings yet

- Cfas Revenue Recognition - StudentsDocument41 pagesCfas Revenue Recognition - StudentsMiel Viason CañeteNo ratings yet

- IFRS 15 RevenueDocument8 pagesIFRS 15 RevenueEmezi Francis ObisikeNo ratings yet

- Key Definitions: The Five-Step Model FrameworkDocument9 pagesKey Definitions: The Five-Step Model FrameworkKATHRYN CLAUDETTE RESENTENo ratings yet

- Ind AS 115 - Revenue From Contracts With Customers: CA Vivekanand PoteDocument9 pagesInd AS 115 - Revenue From Contracts With Customers: CA Vivekanand PoteAjit SharmaNo ratings yet

- Ifrs 15Document7 pagesIfrs 15Shariful HoqueNo ratings yet

- Revenue From ContractsDocument92 pagesRevenue From ContractssharifNo ratings yet

- Revenue From Contracts With Customers (Ind As-115) : Applicable From May 2019 Exam OnwardsDocument5 pagesRevenue From Contracts With Customers (Ind As-115) : Applicable From May 2019 Exam OnwardsVM educationzNo ratings yet

- Pfrs 15 Summary NotesDocument5 pagesPfrs 15 Summary NotesSHARON SAMSONNo ratings yet

- Lesson 9 Long Term ConstructionDocument13 pagesLesson 9 Long Term ConstructionheyheyNo ratings yet

- Mega Project Assurance: Volume One - The Terminological DictionaryFrom EverandMega Project Assurance: Volume One - The Terminological DictionaryNo ratings yet

- Cibil ScoreDocument2 pagesCibil ScoreAjay BaranwalNo ratings yet

- Western Mindanao Adventist Academy 7028 Dumingag, Zamboanga Del Sur, PhilippinesDocument9 pagesWestern Mindanao Adventist Academy 7028 Dumingag, Zamboanga Del Sur, PhilippinesJoyce Torres100% (1)

- Finals NegoDocument6 pagesFinals NegoHoward UntalanNo ratings yet

- Report On Home Loan Process in Different Financial Institutions of NepalDocument31 pagesReport On Home Loan Process in Different Financial Institutions of NepalDipesh PandeyNo ratings yet

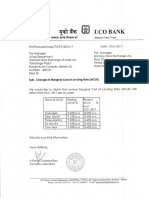

- Changes in Marginal Cost of Lending Rate (MCLR) (Company Update)Document1 pageChanges in Marginal Cost of Lending Rate (MCLR) (Company Update)Shyam SunderNo ratings yet

- Solved Sixteen Years Ago Ms Cole Purchased A 500 000 Insurance PolicyDocument1 pageSolved Sixteen Years Ago Ms Cole Purchased A 500 000 Insurance PolicyAnbu jaromiaNo ratings yet

- Jaiib Made Simple Paper 3Document192 pagesJaiib Made Simple Paper 3kanarendranNo ratings yet

- Í (Zkfè Pagayunan Lemuelâââââ R Ç 3) 24lî Mr. Lemuel Rutaquio PagayunanDocument4 pagesÍ (Zkfè Pagayunan Lemuelâââââ R Ç 3) 24lî Mr. Lemuel Rutaquio PagayunanJohn Robertson DayaoNo ratings yet

- Book 1Document25 pagesBook 1jessa.delacruzNo ratings yet

- Grievance Redressal MechanismDocument4 pagesGrievance Redressal MechanismParikshit SachdevNo ratings yet

- Risk Management PolicyDocument10 pagesRisk Management Policymahak guptaNo ratings yet

- 07 - Petty Cash Fund and Bank ReconciliationDocument2 pages07 - Petty Cash Fund and Bank ReconciliationCy Miolata100% (2)

- Simple and Compound InterestDocument4 pagesSimple and Compound InterestVivek PatelNo ratings yet

- Report On The Standard Bank LTD.: Submitted byDocument14 pagesReport On The Standard Bank LTD.: Submitted bysalman kabirNo ratings yet

- Venue: Pioneer Campus & Leopards Hill.: - 15 DECEMBER, 2021Document3 pagesVenue: Pioneer Campus & Leopards Hill.: - 15 DECEMBER, 2021Twaambo PhiriNo ratings yet

- Meta 2019Document120 pagesMeta 2019NATALIA TYAS ANDRIANINo ratings yet

- Landrith V Bank of New York Mellon RICO ComplaintDocument48 pagesLandrith V Bank of New York Mellon RICO ComplaintBret Landrith100% (1)

- Gen MathDocument2 pagesGen MathLorbie Castañeda FrigillanoNo ratings yet

- QUIZDocument2 pagesQUIZjomarvaldezconabacaniNo ratings yet

- Revised LECPA Syllabi Effective May 2019 and October 2022 ComparisonDocument49 pagesRevised LECPA Syllabi Effective May 2019 and October 2022 ComparisonLloyd ReglosNo ratings yet

- Money Market Mutual FundsDocument4 pagesMoney Market Mutual FundsShreesh ChandraNo ratings yet

- Belize Bank StatementDocument2 pagesBelize Bank StatementJecky SrabonNo ratings yet

- IIFL - SL5134283 - Welcome LetterDocument3 pagesIIFL - SL5134283 - Welcome LetteriiflfincopltdNo ratings yet

- Profit and Loss P&L Statement StatementDocument3 pagesProfit and Loss P&L Statement StatementShreepathi AdigaNo ratings yet

- Visa-Payment-Method DERIVDocument1 pageVisa-Payment-Method DERIVKennedy Kenzo Ken ObochelengNo ratings yet

- MSR Leathers vs. S. Palaniappan and AnrDocument4 pagesMSR Leathers vs. S. Palaniappan and AnrShihabAkhandNo ratings yet

- Business Communication: AssignmentDocument21 pagesBusiness Communication: AssignmentNilesh kumarNo ratings yet

- Principles of Business For CSEC®: 2nd EditionDocument3 pagesPrinciples of Business For CSEC®: 2nd Editionyuvita prasadNo ratings yet

- 4 5868236919153887449-1Document49 pages4 5868236919153887449-1Fasiko Asmaro100% (1)