Download as pdf or txt

You might also like

- 31 CFR 363-Definitions For TDA Acct - Minor Acct, Delinking Acct., GAIN CONTROLDocument7 pages31 CFR 363-Definitions For TDA Acct - Minor Acct, Delinking Acct., GAIN CONTROLSteveManning100% (6)

- Final Income TaxDocument3 pagesFinal Income Taxloonie tunesNo ratings yet

- Six Step Checklist W Chart PDFDocument14 pagesSix Step Checklist W Chart PDFShakes SM100% (3)

- Reduction in Rate of Tax Deduction at Source (TDS) & Tax Collection at Source (TCS)Document6 pagesReduction in Rate of Tax Deduction at Source (TDS) & Tax Collection at Source (TCS)Kranthi Kumar KatamreddyNo ratings yet

- Tax Deduction at SourceDocument13 pagesTax Deduction at SourceSwati SumanNo ratings yet

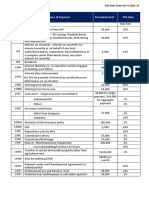

- TDS Rate Chart FY 2020-2021 (Covid-19) : Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) (Covid-19)Document4 pagesTDS Rate Chart FY 2020-2021 (Covid-19) : Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) (Covid-19)Sahay AlokNo ratings yet

- Revised TDS TCS Rate ChartDocument3 pagesRevised TDS TCS Rate ChartMandar KadamNo ratings yet

- TDS RATE CHART FY 2021-22-FinalDocument5 pagesTDS RATE CHART FY 2021-22-FinalLeenaNo ratings yet

- Tds Rate Chart Fy 2021-22Document3 pagesTds Rate Chart Fy 2021-22Kadambari ShelkeNo ratings yet

- Tax and Duties 2020-2021 at A GlanceDocument24 pagesTax and Duties 2020-2021 at A GlanceIbrahim ZachariaNo ratings yet

- Tds Rate Chart Fy 2020Document4 pagesTds Rate Chart Fy 2020KAUTUK KOLINo ratings yet

- TDS Rate Chart FY 2021-2022: Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) Indv/HUF OthersDocument7 pagesTDS Rate Chart FY 2021-2022: Section Code Nature of Payment Threshold (In RS.) TDS Rate (In %) Indv/HUF OthersRajNo ratings yet

- Section 192:: Payment of SalaryDocument7 pagesSection 192:: Payment of SalaryCacptCoachingNo ratings yet

- Income Tax Update: Budget 2019-20: TDS - Tax Deduction at SourceDocument6 pagesIncome Tax Update: Budget 2019-20: TDS - Tax Deduction at SourceAjeet KumarNo ratings yet

- TDS Rate Chart FY 2024-25Document4 pagesTDS Rate Chart FY 2024-25MOQADDARNo ratings yet

- Karvy Group TDS Rates W.E.F. 01.04.2010 Rate of TDS Rate of TDS If PAN Providedif PAN Not ProvidedDocument1 pageKarvy Group TDS Rates W.E.F. 01.04.2010 Rate of TDS Rate of TDS If PAN Providedif PAN Not Providedarjun_cwaNo ratings yet

- Tax Deduction at Source: Subject NameDocument7 pagesTax Deduction at Source: Subject Nameharshita23hrNo ratings yet

- Deduction of Tax at Source With Regard To Salary Income Section 192 1. 2. 3Document4 pagesDeduction of Tax at Source With Regard To Salary Income Section 192 1. 2. 3Vidit GuptaNo ratings yet

- Particulars TDS Rates (In %) : Section 192 Section 192A Section 193Document9 pagesParticulars TDS Rates (In %) : Section 192 Section 192A Section 193ajayNo ratings yet

- TDS Rate Chart For FY 2022-2023Document15 pagesTDS Rate Chart For FY 2022-2023leelathecaNo ratings yet

- 56 Tds Tcs Rate Chart W e F 01 10 09Document1 page56 Tds Tcs Rate Chart W e F 01 10 09Shankar BidadiNo ratings yet

- TDS Rate Chart For Financial Year 2020 21Document1 pageTDS Rate Chart For Financial Year 2020 21Arun RajaNo ratings yet

- Withholding Tax Deduction Chart: Dividend (In Cash or in Specie)Document6 pagesWithholding Tax Deduction Chart: Dividend (In Cash or in Specie)Ahmed BilalNo ratings yet

- WithholdingRatesCards 2022-2023Document17 pagesWithholdingRatesCards 2022-2023ausafhaider5345No ratings yet

- TDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Document3 pagesTDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Prince RaichandNo ratings yet

- TDS SummaryDocument4 pagesTDS Summaryshubhamsingh143deepNo ratings yet

- TDS Rate Chart'Document8 pagesTDS Rate Chart'PUSHKAR GARGNo ratings yet

- Ghana Fiscal Guide 2015 2016Document10 pagesGhana Fiscal Guide 2015 2016batuchemNo ratings yet

- TDS Rates Chart Fy 2020 21 Ay 2021 22Document6 pagesTDS Rates Chart Fy 2020 21 Ay 2021 22Brijendra SinghNo ratings yet

- AIT Matrix Expanded Withholding TaxDocument1 pageAIT Matrix Expanded Withholding TaxSherleen GallardoNo ratings yet

- Union Budget FY2024Document15 pagesUnion Budget FY2024Sathiyamoorthy RethinamNo ratings yet

- Budget Synopsis Fy 2078-79 - TDSDocument1 pageBudget Synopsis Fy 2078-79 - TDSSahu BhaiNo ratings yet

- W14 Module 12withholding TaxesDocument7 pagesW14 Module 12withholding Taxescamille ducutNo ratings yet

- Percentage Taxes: Line of Business/ Activity Tax Base Tax RateDocument2 pagesPercentage Taxes: Line of Business/ Activity Tax Base Tax RateMae MaupoNo ratings yet

- Tax For SupplyDocument4 pagesTax For Supplyashikur rahmanNo ratings yet

- Tax Rate SummaryDocument3 pagesTax Rate SummaryPamela Jean CuyaNo ratings yet

- TDS Rates and ReturnsDocument4 pagesTDS Rates and ReturnsMohanlal BishnoiNo ratings yet

- Regular Business/Corporate Tax: DC RFC NRFCDocument2 pagesRegular Business/Corporate Tax: DC RFC NRFCGrace Angelie C. Asio-SalihNo ratings yet

- Latest Provisions TDS and CSDocument74 pagesLatest Provisions TDS and CShimesh amibrokerNo ratings yet

- Withholding Taxes Learning ObjectivesDocument8 pagesWithholding Taxes Learning ObjectivesAce AlquinNo ratings yet

- Particulars TDS Rates (In %)Document6 pagesParticulars TDS Rates (In %)Amiy Anand PandeyNo ratings yet

- TDS Rate Chart For FY 2022-2023 (AY 2023-2024) Including Budget 2022 Amendments - Taxguru - inDocument15 pagesTDS Rate Chart For FY 2022-2023 (AY 2023-2024) Including Budget 2022 Amendments - Taxguru - inSachin GuptaNo ratings yet

- Tax RatesDocument2 pagesTax RatesSalma GurarNo ratings yet

- TDS Rates On The Income Tax of Bangladesh For 2019-20Document19 pagesTDS Rates On The Income Tax of Bangladesh For 2019-20Muhammad Asaduzzaman MonaNo ratings yet

- Sierra Leone Fiscal Guide 2020 PDFDocument10 pagesSierra Leone Fiscal Guide 2020 PDFMAlek AMARANo ratings yet

- BLGF MC No. 002.2021 - BLGF Electronic Financial Reporting Tool - 02 Feb 2021Document4 pagesBLGF MC No. 002.2021 - BLGF Electronic Financial Reporting Tool - 02 Feb 2021Gian Bayaras100% (1)

- C.H. Padliya & Co.: Chartered AccountantsDocument11 pagesC.H. Padliya & Co.: Chartered AccountantsSarat KumarNo ratings yet

- Important Changes in TDS Chart: Section No. Description Cutoff Rate of TDS ExamplesDocument1 pageImportant Changes in TDS Chart: Section No. Description Cutoff Rate of TDS ExamplesDaljeet SinghNo ratings yet

- Taxes and Duties at A Glance 2018/2019: Tanzania Revenue AuthorityDocument24 pagesTaxes and Duties at A Glance 2018/2019: Tanzania Revenue AuthorityInnocent IssackNo ratings yet

- Particulars TDS Rates (In %) : Section 192 Section 192A Section 193Document7 pagesParticulars TDS Rates (In %) : Section 192 Section 192A Section 193ABHISHEKNo ratings yet

- Mwide Analyst Briefing Fy2019 1q2020 FinalDocument40 pagesMwide Analyst Briefing Fy2019 1q2020 FinalJasper BryanNo ratings yet

- Tds Rate Chart AY 21 22Document1 pageTds Rate Chart AY 21 22Keerthana.M MuruganNo ratings yet

- TAX 401 Percentage Tax Part 1Document7 pagesTAX 401 Percentage Tax Part 1Juan Miguel UngsodNo ratings yet

- Final TDS and Tax ExemptionsDocument4 pagesFinal TDS and Tax Exemptionsdpak bhusalNo ratings yet

- OPT NotesDocument2 pagesOPT NotesMei Leen DanielesNo ratings yet

- TDS Notes in Hindi PDFDocument8 pagesTDS Notes in Hindi PDFRohit VermaNo ratings yet

- FTX (LSO) Examinable Documents 2019Document2 pagesFTX (LSO) Examinable Documents 2019Mokoena RalesupiNo ratings yet

- Chap 11 - Percentage Taxes ValenciaDocument23 pagesChap 11 - Percentage Taxes ValenciaDanzen Bueno Imus0% (1)

- Taxation Hightlights FY 2077-78Document2 pagesTaxation Hightlights FY 2077-78RajibDahalNo ratings yet

- TCS Provisions For The FY 2021-22 AY 2022-23Document11 pagesTCS Provisions For The FY 2021-22 AY 2022-23Hardik gabaNo ratings yet

- Tax Table Corporations 2022Document4 pagesTax Table Corporations 2022Xandredg Sumpt LatogNo ratings yet

- Middle East and North Africa Quarterly Economic Brief, January 2014: Growth Slowdown Heightens the Need for ReformsFrom EverandMiddle East and North Africa Quarterly Economic Brief, January 2014: Growth Slowdown Heightens the Need for ReformsNo ratings yet

- Beams9esm Ch01Document13 pagesBeams9esm Ch01zandra SumbarNo ratings yet

- Task # 01 LP - Formulation, Graphical & Simplex SolutionDocument5 pagesTask # 01 LP - Formulation, Graphical & Simplex Solutionmaya0% (1)

- Intercompany Profit Transactions - Inventories: Transactions Within The Affiliated GroupDocument60 pagesIntercompany Profit Transactions - Inventories: Transactions Within The Affiliated GroupPhil MO JoeNo ratings yet

- Liz MotorsDocument4 pagesLiz Motorstanyapatel79No ratings yet

- Lagos State Audited Financial Statements, 2018Document62 pagesLagos State Audited Financial Statements, 2018Justus OhakanuNo ratings yet

- Internship Report AICDocument4 pagesInternship Report AICgod of thunder ThorNo ratings yet

- About The HarambeansDocument3 pagesAbout The HarambeansJustusNo ratings yet

- Does CAPM Hold Good For Indian Stocks A Case Study of CNX Nifty ConstituentsDocument14 pagesDoes CAPM Hold Good For Indian Stocks A Case Study of CNX Nifty Constituentsarcherselevators100% (1)

- CEC 314-CE Laws, Ethics and Contracts: Aironne Karl S. ValdezDocument56 pagesCEC 314-CE Laws, Ethics and Contracts: Aironne Karl S. ValdezAironne ValdezNo ratings yet

- Chapter 06 PDFDocument24 pagesChapter 06 PDFadarshNo ratings yet

- Economic Activities in EthiopiaDocument4 pagesEconomic Activities in Ethiopiaeyerusalem tesfaye100% (4)

- 2018 Quarter 2 Financials PDFDocument1 page2018 Quarter 2 Financials PDFKaystain Chris IhemeNo ratings yet

- Notice For AD - Re RegistartionDocument2 pagesNotice For AD - Re RegistartionAnujanNo ratings yet

- Write An Essay About Your Understanding of Corporate Governance, Its Importance and Impact To You As An Individual. (At Least 500 Words)Document1 pageWrite An Essay About Your Understanding of Corporate Governance, Its Importance and Impact To You As An Individual. (At Least 500 Words)Jade jade jadeNo ratings yet

- Account Statement 300123 290423Document32 pagesAccount Statement 300123 290423Yash SiwachNo ratings yet

- Hugutan Mo Ang Puto Ko Snack Treats: A Business Plan To Be Presented To The Faculty of STI College TanayDocument4 pagesHugutan Mo Ang Puto Ko Snack Treats: A Business Plan To Be Presented To The Faculty of STI College TanayRica DomingoNo ratings yet

- Planning and RoutingDocument50 pagesPlanning and RoutingAnand DubeyNo ratings yet

- Floating in Chocolate: A Case Analysis OnDocument6 pagesFloating in Chocolate: A Case Analysis OnRohanNo ratings yet

- Goat-Sheep 10010 Hills GenDocument5 pagesGoat-Sheep 10010 Hills GenRaj kumar PatelNo ratings yet

- Commercial Lease Letter of TO Lease Excess Lot From Commercial UnitDocument3 pagesCommercial Lease Letter of TO Lease Excess Lot From Commercial UnitMiriam M. RamirezNo ratings yet

- MEPCO ONLINE BILLL - PDF OctDocument2 pagesMEPCO ONLINE BILLL - PDF OctRehan SaleemNo ratings yet

- Alnuaimi, A. S., & Mohsin, M. (2013) - Causes of Delay in Completion of Construction Projects in OmanDocument4 pagesAlnuaimi, A. S., & Mohsin, M. (2013) - Causes of Delay in Completion of Construction Projects in OmandimlouNo ratings yet

- The Common Stock Market PPT at Mba FinanceDocument59 pagesThe Common Stock Market PPT at Mba FinanceBabasab Patil (Karrisatte)No ratings yet

- Fact Finders Report Greater Egg Harbor PDFDocument109 pagesFact Finders Report Greater Egg Harbor PDFGallowayTwpNewsNo ratings yet

- JordanDocument91 pagesJordanshanshan700No ratings yet

- About The Asset Partner OpportunityDocument1 pageAbout The Asset Partner OpportunitykaranNo ratings yet

- Artikel 5Document14 pagesArtikel 5Agus ArwaniNo ratings yet

- Manufacturing ProcessDocument23 pagesManufacturing ProcessSombwit KabasiNo ratings yet