Download as pdf or txt

You might also like

- Condominium Contract of Lease SampleDocument5 pagesCondominium Contract of Lease SampleAbel MontejoNo ratings yet

- ATM Response CodesDocument5 pagesATM Response CodesSenthil KarthiNo ratings yet

- Postmodern Music - Postmodern ThoughtDocument389 pagesPostmodern Music - Postmodern ThoughtMadalina Hotoran100% (1)

- Unit 1 MiniMatura - Answer KeyDocument1 pageUnit 1 MiniMatura - Answer KeyŁukasz Gil67% (3)

- 34 - AML KYC-RP-Final - 20200527Document7 pages34 - AML KYC-RP-Final - 20200527RISHI KESHNo ratings yet

- Cheque Truncation System (CTS)Document2 pagesCheque Truncation System (CTS)Stan leeNo ratings yet

- Truncated Cheque Clearance ProceduresDocument31 pagesTruncated Cheque Clearance Proceduresjhanvi75% (4)

- E-Cheque (MICR Cheque) in Bangladesh Back GroundDocument6 pagesE-Cheque (MICR Cheque) in Bangladesh Back GroundLenin VincentNo ratings yet

- NACH Direct Debit New Mandate Form SCB PDFDocument1 pageNACH Direct Debit New Mandate Form SCB PDFKAIVAL MEHTA100% (1)

- Cheque Clearing - An OverviewDocument20 pagesCheque Clearing - An OverviewGiridhaaran.VNo ratings yet

- 01 - Clearing ActivtiesDocument14 pages01 - Clearing ActivtiesBarjesh_Lamba_2009No ratings yet

- DMS in Banking SectorDocument86 pagesDMS in Banking SectorSoodesh BeegunNo ratings yet

- Uniform Regulations and Rules For Bankers Clearing House PDFDocument40 pagesUniform Regulations and Rules For Bankers Clearing House PDFSathyanarayanaRaoRNo ratings yet

- MicrDocument3 pagesMicrharyy1234567No ratings yet

- PayWay API Developers GuideDocument48 pagesPayWay API Developers GuideSimbwa PhillipNo ratings yet

- SMS Internet Banking FormDocument4 pagesSMS Internet Banking FormSayed InsanNo ratings yet

- MICRDocument29 pagesMICRmantyame100% (1)

- Cash and Cash Equivalents: Print EmailDocument11 pagesCash and Cash Equivalents: Print EmailRobert PangitNo ratings yet

- Unit 3: Commercial Bank Sources of Funds: 1. Transaction DepositsDocument9 pagesUnit 3: Commercial Bank Sources of Funds: 1. Transaction Depositsመስቀል ኃይላችን ነውNo ratings yet

- Suresh Gyan Vihar University: Department of Ceit SynopsisDocument8 pagesSuresh Gyan Vihar University: Department of Ceit SynopsisAbodh KumarNo ratings yet

- Study of Cash Management at Standard Chartered BankDocument115 pagesStudy of Cash Management at Standard Chartered BankVishnu Prasad100% (2)

- CAMSDocument39 pagesCAMSSterling FincapNo ratings yet

- ACH Return Item File Reference GuideDocument44 pagesACH Return Item File Reference GuideJackson J. Melo da SilvaNo ratings yet

- Electronic Bank TransferDocument6 pagesElectronic Bank Transfergeorgebates1979No ratings yet

- Clearing House Lectureupdated - June11 2013Document35 pagesClearing House Lectureupdated - June11 2013dushakilNo ratings yet

- National Electronic Funds Transfer (NEFT) Is A Nation-Wide System That FacilitatesDocument5 pagesNational Electronic Funds Transfer (NEFT) Is A Nation-Wide System That FacilitatesMounika TadikondaNo ratings yet

- Functional Requirements Matrix - Accounts PayableDocument58 pagesFunctional Requirements Matrix - Accounts PayableEden Solutions LtdNo ratings yet

- REPORT (Treasuty MGT)Document15 pagesREPORT (Treasuty MGT)Hazel HizoleNo ratings yet

- Electronic Fund Transfer SystemDocument7 pagesElectronic Fund Transfer SystemJatin BhatiaNo ratings yet

- 01 07-VpisDocument19 pages01 07-Vpishell_hello11No ratings yet

- SRS For ATM SystemDocument21 pagesSRS For ATM SystemUrja DhabardeNo ratings yet

- VeloCT 3.1 DocumentationDocument18 pagesVeloCT 3.1 DocumentationGayCanuckNo ratings yet

- Jumpstart Credit Card Processing (Version 1)Document15 pagesJumpstart Credit Card Processing (Version 1)Oleksiy KovyrinNo ratings yet

- Bank ManagementDocument198 pagesBank ManagementSooraj Kallooppara0% (1)

- 1.2 Scope: 1.1 PurposeDocument21 pages1.2 Scope: 1.1 PurposemohitNo ratings yet

- ErrorsDocument17 pagesErrorsurstannuNo ratings yet

- SBI MiniBank User Manual PPT PresentationDocument75 pagesSBI MiniBank User Manual PPT PresentationMayur KhichiNo ratings yet

- Ecommerce PresentationDocument9 pagesEcommerce PresentationSurabhi AgrawalNo ratings yet

- Online Bank SynopsisDocument7 pagesOnline Bank SynopsisPrashant VermaNo ratings yet

- Banking ProjectDocument13 pagesBanking Projectlalitsurana0% (1)

- Transfer of Funds-User Guide-SEWDocument23 pagesTransfer of Funds-User Guide-SEWkommineni11No ratings yet

- E PaymentDocument15 pagesE PaymentRohan KirpekarNo ratings yet

- Credit Card Application Processing Assignment Spr2013 v1-1Document4 pagesCredit Card Application Processing Assignment Spr2013 v1-1c.enekwe8981No ratings yet

- PPT18Document27 pagesPPT18Dev KumarNo ratings yet

- Electronic Funds Transfers: 10 November 2019Document30 pagesElectronic Funds Transfers: 10 November 2019Chandan kumar singhNo ratings yet

- Credit Management: Adeel Nasir Lecturer (Commerce) Punjab University Jhelum CampusDocument34 pagesCredit Management: Adeel Nasir Lecturer (Commerce) Punjab University Jhelum CampusZindgiKiKhatirNo ratings yet

- Very Easy Money Transfer: E-ChequeDocument15 pagesVery Easy Money Transfer: E-ChequeKartheek AldiNo ratings yet

- E BankingDocument8 pagesE BankingAnonymous BWTBnGNo ratings yet

- The Electronic Clearing Service in IndiaDocument3 pagesThe Electronic Clearing Service in Indiamax_dcostaNo ratings yet

- ATM DescriptionDocument8 pagesATM DescriptionKomal SrivastavNo ratings yet

- Bangladesh Automated Clearing HouseDocument24 pagesBangladesh Automated Clearing HouseMorium ZafarNo ratings yet

- ATM Reporting System ReportDocument6 pagesATM Reporting System ReportTabish AlmasNo ratings yet

- 01.09-User System ManagementDocument12 pages01.09-User System Managementmevrick_guyNo ratings yet

- Lockbox Power PointDocument19 pagesLockbox Power Pointasrinu88881125100% (1)

- MasterCard JJDocument7 pagesMasterCard JJjohnjamgochianNo ratings yet

- Check Reprint Fch8 IN SAPDocument16 pagesCheck Reprint Fch8 IN SAPPromoth JaidevNo ratings yet

- Usbank Sig CardDocument3 pagesUsbank Sig CardlilvprNo ratings yet

- "The Automated Teller Machine": Engineering College BikanerDocument12 pages"The Automated Teller Machine": Engineering College BikanerRajesh BishnoiNo ratings yet

- Jana Bank General Terms and Conditions For AccountsDocument18 pagesJana Bank General Terms and Conditions For AccountsArc En CielNo ratings yet

- ATM-BNA-Recycler BGL ReconDocument41 pagesATM-BNA-Recycler BGL ReconNishant RoyNo ratings yet

- Review of Some Online Banks and Visa/Master Cards IssuersFrom EverandReview of Some Online Banks and Visa/Master Cards IssuersNo ratings yet

- Methods to Overcome the Financial and Money Transfer Blockade against Palestine and any Country Suffering from Financial BlockadeFrom EverandMethods to Overcome the Financial and Money Transfer Blockade against Palestine and any Country Suffering from Financial BlockadeNo ratings yet

- Press Release - Dec 2019Document2 pagesPress Release - Dec 2019RISHI KESHNo ratings yet

- L047-Alternate Delivery ChannelsDocument36 pagesL047-Alternate Delivery ChannelsRISHI KESHNo ratings yet

- Website Schedule For RPE Aug-Sep-2020Document2 pagesWebsite Schedule For RPE Aug-Sep-2020RISHI KESHNo ratings yet

- Blue StrategyDocument22 pagesBlue StrategyshivanthikaNo ratings yet

- Evidence Cases IIDocument94 pagesEvidence Cases IIAiken Alagban LadinesNo ratings yet

- Green HRMDocument7 pagesGreen HRMpdaagarwal100% (1)

- EMPIREFILM With ISBN PDFDocument89 pagesEMPIREFILM With ISBN PDFBryan WatermanNo ratings yet

- GastronomyDocument3 pagesGastronomyGHERSON OSTIANo ratings yet

- Bill of LadingDocument1 pageBill of LadingJohn Mark VerarNo ratings yet

- The Tragical History of Doctor Faustus by Christopher MarloweDocument8 pagesThe Tragical History of Doctor Faustus by Christopher MarloweJOSUE BARRIOSNo ratings yet

- Ikenberry, John (2014) - The Illusion of Geopolitics.Document9 pagesIkenberry, John (2014) - The Illusion of Geopolitics.David RamírezNo ratings yet

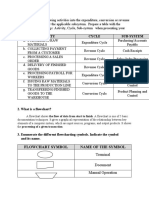

- Activity Cycle Sub-System: Flowchart Symbol Name of The SymbolDocument3 pagesActivity Cycle Sub-System: Flowchart Symbol Name of The SymbolALLIAH CARL MANUELLE PASCASIONo ratings yet

- Spes Reviewer 2023Document3 pagesSpes Reviewer 2023moneciaashleycate100% (2)

- Figures of SpeechDocument3 pagesFigures of SpeechLyka Isabel TanNo ratings yet

- NuissanceDocument8 pagesNuissancedaisy felizardoNo ratings yet

- Table of FIDIC Cases - 03 07 2023Document49 pagesTable of FIDIC Cases - 03 07 2023Vyom VakhariyaNo ratings yet

- Environment Position PaperDocument6 pagesEnvironment Position PaperJenlisa KimanobanNo ratings yet

- Approaches To The Study of Social Problems: The Person-Blame ApproachDocument4 pagesApproaches To The Study of Social Problems: The Person-Blame ApproachsnehaoctNo ratings yet

- The Paralympic Games Is A Major International MultiDocument1 pageThe Paralympic Games Is A Major International MultiKamaRaj SundaramoorthyNo ratings yet

- Class Notes On Agrobiodiversity Conservation and Climate Change 022Document156 pagesClass Notes On Agrobiodiversity Conservation and Climate Change 022Kabir Singh100% (1)

- SHS MIL Q1 W3 Responsible Use of Media and InformationDocument6 pagesSHS MIL Q1 W3 Responsible Use of Media and InformationChristina Paule Gordolan100% (1)

- The Conquistadors Always Start From The South in Square 28 and On The Track The Aztecs Always Start in Square 13Document9 pagesThe Conquistadors Always Start From The South in Square 28 and On The Track The Aztecs Always Start in Square 13Joshua ReyesNo ratings yet

- Ojoyoshu by Genshin, Translated From Japanese by A.K. ReischauerDocument136 pagesOjoyoshu by Genshin, Translated From Japanese by A.K. ReischauerJōshō Adrian Cirlea100% (6)

- Case DigestDocument2 pagesCase DigestJennycel SueltoNo ratings yet

- REV - U3C1L2A2 - Exercise 2 - PersonalDocument1 pageREV - U3C1L2A2 - Exercise 2 - Personaledward taylor100% (1)

- GP Sheet Stock HosurDocument4 pagesGP Sheet Stock HosurSURANA1973No ratings yet

- Eminent Domain AfDocument12 pagesEminent Domain AfSaumya MotwaniNo ratings yet

- Constitutional Philosophies: Synopsis of Book Review " "Document2 pagesConstitutional Philosophies: Synopsis of Book Review " "sani_454296177No ratings yet

- TheNewLink AWESNAretreat2018ADocument32 pagesTheNewLink AWESNAretreat2018ALaurence Tabanao GayaoNo ratings yet

- MacarioDocument5 pagesMacarioNeil Isaac PerezNo ratings yet