Download as pdf or txt

You might also like

- Sap IhcDocument19 pagesSap IhcPrateekNo ratings yet

- Final Project Reports SBI POSDocument83 pagesFinal Project Reports SBI POSTarun Kathiriya80% (5)

- 34 - AML KYC-RP-Final - 20200527Document7 pages34 - AML KYC-RP-Final - 20200527RISHI KESHNo ratings yet

- Atm 123Document40 pagesAtm 123ahmedtaniNo ratings yet

- Waw 1 1 Atm For hg22Document40 pagesWaw 1 1 Atm For hg22ahmedtaniNo ratings yet

- 1 Atm For hg22Document40 pages1 Atm For hg22ahmedtaniNo ratings yet

- Banking ProductsDocument9 pagesBanking Productsbeena antuNo ratings yet

- Banking in 21st CenturyDocument4 pagesBanking in 21st CenturyDr. Ashish Kumar ChaurasiaNo ratings yet

- Introduction About ATM: NamesDocument29 pagesIntroduction About ATM: Namesakashbrar0612No ratings yet

- ATM BankingDocument13 pagesATM BankingMAHALAKSHMI100% (1)

- Unit 2 - Sbaa7001 Banking Products and ServicesDocument38 pagesUnit 2 - Sbaa7001 Banking Products and ServicesGracyNo ratings yet

- Hardware Devices Form 3Document13 pagesHardware Devices Form 3Mapiye GabrielNo ratings yet

- Banking Products and ServicesDocument5 pagesBanking Products and ServicesAikya GandhiNo ratings yet

- L-7 Alternate Channels of BankingDocument21 pagesL-7 Alternate Channels of BankingVinay SudaniNo ratings yet

- Out Sources of ATMDocument55 pagesOut Sources of ATMRadhaNo ratings yet

- Delivery Channels in Retail BankingDocument5 pagesDelivery Channels in Retail BankingSahibaNo ratings yet

- Report On RoborticsDocument22 pagesReport On Roborticsasma246No ratings yet

- Banking Awareness: AtmDocument2 pagesBanking Awareness: Atmparam_pasrichaNo ratings yet

- Final ReportDocument28 pagesFinal ReportBishwo Kiran Bhattarai100% (1)

- Popular Services Under E-Banking in IndiaDocument5 pagesPopular Services Under E-Banking in IndiaPramil AnandNo ratings yet

- Electronic Banking 01Document21 pagesElectronic Banking 01Azizul Islam Rahat100% (1)

- RatesDocument4 pagesRatesashukundanNo ratings yet

- Banking PresentationDocument6 pagesBanking PresentationAgustino BatistaNo ratings yet

- ATM Modes of Banking Transactions and Usage in Coimbatore CityDocument12 pagesATM Modes of Banking Transactions and Usage in Coimbatore CityRishi 86No ratings yet

- Marketing PlanDocument25 pagesMarketing PlanSyed JunaidNo ratings yet

- What Is An Automated Teller MachineDocument9 pagesWhat Is An Automated Teller Machine719d0011No ratings yet

- ATM'sDocument36 pagesATM'sPooja More100% (1)

- RatesDocument4 pagesRatesashukundanNo ratings yet

- PCBL - Prime Cash (ATM)Document38 pagesPCBL - Prime Cash (ATM)Saadat KhanNo ratings yet

- AtmDocument2 pagesAtmjasminnaurNo ratings yet

- Banking and FinanceDocument107 pagesBanking and FinanceVikas PabaleNo ratings yet

- Module 3Document11 pagesModule 3pavithran selvamNo ratings yet

- Tabish AssignmentDocument10 pagesTabish AssignmenttabishalizahidNo ratings yet

- Ict Group Assignment For Grade 12Document9 pagesIct Group Assignment For Grade 12KaddunNo ratings yet

- Debit Cards & Credit CardsDocument28 pagesDebit Cards & Credit CardsullasNo ratings yet

- Commercial BankingDocument74 pagesCommercial BankingShishir N VNo ratings yet

- 04.technology in Banking - Unit Iii Part Ii - Prof. Dr. Rajesh MankaniDocument14 pages04.technology in Banking - Unit Iii Part Ii - Prof. Dr. Rajesh MankaniGame ProfileNo ratings yet

- PPT18Document27 pagesPPT18Dev KumarNo ratings yet

- Innovation in Indian Banking SectorDocument3 pagesInnovation in Indian Banking SectorSandeep MishraNo ratings yet

- II Sem BOIDocument36 pagesII Sem BOINeha ShuklaNo ratings yet

- Digital Payment SolutionDocument8 pagesDigital Payment SolutionBerkti GetuNo ratings yet

- CH 2 - E-Banking ServicesDocument20 pagesCH 2 - E-Banking Serviceschintan vadgamaNo ratings yet

- Retail Banking ChannelsDocument6 pagesRetail Banking Channelsbeena antuNo ratings yet

- Institute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingDocument5 pagesInstitute of Managment Studies, Davv, Indore Finance and Administration - Semester Iv Credit Management and Retail BankingSNo ratings yet

- Mod 1 Mbfs PDF NewDocument22 pagesMod 1 Mbfs PDF NewWalidahmad AlamNo ratings yet

- ATM DescriptionDocument8 pagesATM DescriptionKomal SrivastavNo ratings yet

- ATM White Label ATM PDFDocument2 pagesATM White Label ATM PDFSURENDRA SAHUNo ratings yet

- RealizeDocument9 pagesRealizeNabuteNo ratings yet

- 12 Chapter2Document36 pages12 Chapter2lucasNo ratings yet

- AtmDocument29 pagesAtmShilpa Jayaram JNo ratings yet

- Electronic BankingDocument5 pagesElectronic Bankingrakibul islam rakibNo ratings yet

- Final Project ReportDocument7 pagesFinal Project Reporthifza shahzadNo ratings yet

- What Is An Automated Teller Machine (ATM) ?Document2 pagesWhat Is An Automated Teller Machine (ATM) ?DavidNo ratings yet

- CH 13 Rtgs Neft It Products and ServicesDocument27 pagesCH 13 Rtgs Neft It Products and ServicesSoumya Ranjan NayakNo ratings yet

- Uom Synopsis-Project 15704 Synopsis 1 1703513293956Document3 pagesUom Synopsis-Project 15704 Synopsis 1 1703513293956mohammed eidrees razaNo ratings yet

- Automated System in BankingDocument60 pagesAutomated System in BankingMewati GaneshNo ratings yet

- E-Banking in India: Services Provided by The Bank ThroughDocument21 pagesE-Banking in India: Services Provided by The Bank ThroughKomal SahuNo ratings yet

- Internet Banking in India:) Information Only SystemDocument6 pagesInternet Banking in India:) Information Only SystemRohan Freako RawalNo ratings yet

- Chapter 4Document11 pagesChapter 4vivek kumarNo ratings yet

- Meaning of E-Banking: 3.2 Automated Teller MachineDocument16 pagesMeaning of E-Banking: 3.2 Automated Teller Machinehuneet SinghNo ratings yet

- Summary of Ahmed Siddiqui & Nicholas Straight's The Anatomy of the SwipeFrom EverandSummary of Ahmed Siddiqui & Nicholas Straight's The Anatomy of the SwipeNo ratings yet

- Review of Some Online Banks and Visa/Master Cards IssuersFrom EverandReview of Some Online Banks and Visa/Master Cards IssuersNo ratings yet

- Press Release - Dec 2019Document2 pagesPress Release - Dec 2019RISHI KESHNo ratings yet

- L052-Cheque Truncation SystemDocument21 pagesL052-Cheque Truncation SystemRISHI KESHNo ratings yet

- Website Schedule For RPE Aug-Sep-2020Document2 pagesWebsite Schedule For RPE Aug-Sep-2020RISHI KESHNo ratings yet

- CRN 3361042732Document3 pagesCRN 3361042732ComacNo ratings yet

- Demand PerformaDocument12 pagesDemand PerformaMuhammad Asif LillaNo ratings yet

- KX072867 Invoice/Credit: Miss Margarita Pantelidou (200073769) Pooley 21I Pooley House Westfield Way London E1 4PUDocument1 pageKX072867 Invoice/Credit: Miss Margarita Pantelidou (200073769) Pooley 21I Pooley House Westfield Way London E1 4PUMarita PantelNo ratings yet

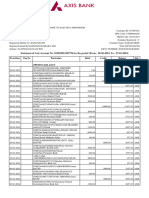

- Account Statement From 1 Jun 2020 To 10 Jun 2020: TXN Date Value Description Ref No./Cheque Debit Credit Balance Date NoDocument2 pagesAccount Statement From 1 Jun 2020 To 10 Jun 2020: TXN Date Value Description Ref No./Cheque Debit Credit Balance Date NonKajaNo ratings yet

- Payment Settlement System in Us: Presented By: Heninle Magh ROLL-7Document24 pagesPayment Settlement System in Us: Presented By: Heninle Magh ROLL-7Henny SebNo ratings yet

- Order 111-3369545-5506652Document1 pageOrder 111-3369545-5506652can kayarNo ratings yet

- Provide A Brief Description of Each of The Three Main Returns and Lodgements That Are Required by GSDocument1 pageProvide A Brief Description of Each of The Three Main Returns and Lodgements That Are Required by GSStephanie NGNo ratings yet

- Road Transportation Time Table: To GulbargaDocument2 pagesRoad Transportation Time Table: To GulbargaNarendra RajurkarNo ratings yet

- RMC 17 2011 Notes To FS Taxes PDFDocument3 pagesRMC 17 2011 Notes To FS Taxes PDFMarie Vea RamosNo ratings yet

- P21 Balancing Statement 2021 1919455700005Document3 pagesP21 Balancing Statement 2021 1919455700005Mo IbrahimNo ratings yet

- HSBC Third Party Transfer Activate FormDocument1 pageHSBC Third Party Transfer Activate FormPankaj Batra100% (2)

- Forever New New Catalogue May 2021.1621849133950Document41 pagesForever New New Catalogue May 2021.1621849133950Carolina PrayogoNo ratings yet

- Wells Fargo: Transaction History (Continued)Document1 pageWells Fargo: Transaction History (Continued)Meyonka WestNo ratings yet

- Statement 28949Document4 pagesStatement 28949niyameddinagayev53No ratings yet

- TDS Rate With Section FY 2019-2020Document22 pagesTDS Rate With Section FY 2019-2020Iftekhar SaikatNo ratings yet

- Account STMT XX1794 27032024Document8 pagesAccount STMT XX1794 27032024A M Painters - interior decoratorsNo ratings yet

- Credit CardDocument15 pagesCredit Cardsrdagpnt100% (1)

- Singapore: Tackling Future Mobility Demand: Waqas CheemaDocument60 pagesSingapore: Tackling Future Mobility Demand: Waqas CheemaCiise Cali HaybeNo ratings yet

- Transfer Information DocumentDocument2 pagesTransfer Information Documentshahzeel khanNo ratings yet

- Estmt - 2024 01 05Document8 pagesEstmt - 2024 01 05alejandro860510No ratings yet

- RocketDocument5 pagesRocketFariha Mehzabin NoshinNo ratings yet

- (0021) Non Company Deductees BPLJ01048F: T.D.S./T.C.S. Tax Challan Challan No./ ITNS 281 2021-22 BPLJ01048FDocument1 page(0021) Non Company Deductees BPLJ01048F: T.D.S./T.C.S. Tax Challan Challan No./ ITNS 281 2021-22 BPLJ01048FAngad MundraNo ratings yet

- BB Noytg Idpvi 1552.00: Type Catogary ClassDocument1 pageBB Noytg Idpvi 1552.00: Type Catogary ClassDilip KumarNo ratings yet

- Picasso Inn - 10012021Document2 pagesPicasso Inn - 10012021Safin RNo ratings yet

- T24 Model Bank - R12 Feature List PDFDocument58 pagesT24 Model Bank - R12 Feature List PDFtayuta100% (1)

- FM 55-17 Chapter 8 Loading and Discharging Cargo VesselsDocument52 pagesFM 55-17 Chapter 8 Loading and Discharging Cargo VesselsRishabh SinghNo ratings yet

- Online Payment PortalDocument2 pagesOnline Payment PortalArjunNo ratings yet

- Account Statement From 1 Jun 2021 To 1 Dec 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument9 pagesAccount Statement From 1 Jun 2021 To 1 Dec 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceसोनू जगतापNo ratings yet

- CH 1Document40 pagesCH 1khawla2789No ratings yet