Download as docx, pdf, or txt

You might also like

- Nick Murray, Robert A. Stanger (Editor) - Serious Money - The Art of Marketing Mutual Funds-Robert A Stanger & Co (1991)Document360 pagesNick Murray, Robert A. Stanger (Editor) - Serious Money - The Art of Marketing Mutual Funds-Robert A Stanger & Co (1991)KALPESH SHAH100% (1)

- Case Paper - 2 - SituationalDocument1 pageCase Paper - 2 - SituationalUtsav Raj Pant100% (1)

- Laughing at Wall Street How I Beat The Pros at Investing (By Reading Tabloids, Shopping at The Mall, and Connecting On Facebook) and How You Can, TooDocument10 pagesLaughing at Wall Street How I Beat The Pros at Investing (By Reading Tabloids, Shopping at The Mall, and Connecting On Facebook) and How You Can, TooMacmillan Publishers0% (2)

- AMFEIX - Monthly Report (August 2019)Document5 pagesAMFEIX - Monthly Report (August 2019)PoolBTCNo ratings yet

- Peachtree Securities Inc. (A) Answers - Irish JuneDocument8 pagesPeachtree Securities Inc. (A) Answers - Irish Juneish juneNo ratings yet

- Tri-Cities Community Bank Case Study SolutionDocument2 pagesTri-Cities Community Bank Case Study SolutionJohn Marthin ReformaNo ratings yet

- Marathon Runners Case, 19324, UTSAV RAJ PANTDocument6 pagesMarathon Runners Case, 19324, UTSAV RAJ PANTUtsav Raj PantNo ratings yet

- Political Events and Stock MarketsDocument3 pagesPolitical Events and Stock MarketsUtsav Raj PantNo ratings yet

- Content Marketing Proposal TemplateDocument7 pagesContent Marketing Proposal TemplateMahmoud HasanNo ratings yet

- Does the Capital Asset Pricing Model Really Work_2011Document6 pagesDoes the Capital Asset Pricing Model Really Work_2011farid.ilishkinNo ratings yet

- Task 5 Example AnswerDocument7 pagesTask 5 Example AnswerMaisha JainNo ratings yet

- Risk Return GraphDocument2 pagesRisk Return GraphShakhawat RahmanNo ratings yet

- Result Update Presentation (Company Update)Document24 pagesResult Update Presentation (Company Update)Shyam SunderNo ratings yet

- AMFEIX - Monthly Report (October 2019)Document15 pagesAMFEIX - Monthly Report (October 2019)PoolBTCNo ratings yet

- Ubl FMR April 2021 - Compressed 3Document28 pagesUbl FMR April 2021 - Compressed 3Hassan AliNo ratings yet

- Bajaj Finserv and Manappuram Finance Acquisition IdeaDocument13 pagesBajaj Finserv and Manappuram Finance Acquisition IdeaRUSHIL GUPTANo ratings yet

- Bank Lending Rates As of 12-01-19Document1 pageBank Lending Rates As of 12-01-19Uhudhu AhmedNo ratings yet

- AMFEIX - Monthly Report (May 2020)Document17 pagesAMFEIX - Monthly Report (May 2020)PoolBTCNo ratings yet

- UBL FMR December 2022 1Document31 pagesUBL FMR December 2022 1MUHAMMAD QASIMNo ratings yet

- Giguere hw4Document4 pagesGiguere hw4api-554525839No ratings yet

- All Products PayoutDocument24 pagesAll Products PayoutAshwani KumarNo ratings yet

- Global Div Inv Grade Income Trust II-IndyMac 2005-AR14!3!31-10Document17 pagesGlobal Div Inv Grade Income Trust II-IndyMac 2005-AR14!3!31-10Barbara J. FordeNo ratings yet

- Max Money Market FundDocument1 pageMax Money Market FundChetan GuptaNo ratings yet

- Potential Inflationary PressuresDocument5 pagesPotential Inflationary PressuresKamran BayramovNo ratings yet

- Empirical Testing of Quantity Theory of Money in IndiaDocument16 pagesEmpirical Testing of Quantity Theory of Money in IndiarwalimbeNo ratings yet

- Email Optimization TrackerDocument5 pagesEmail Optimization TrackerVikNo ratings yet

- 22 Upper Brook Street, London, United Kingdom W1K 7PZDocument1 page22 Upper Brook Street, London, United Kingdom W1K 7PZapi-26055241No ratings yet

- 4Q09 Earnings Eng v8 Final LGDocument19 pages4Q09 Earnings Eng v8 Final LGAmit DepaniNo ratings yet

- UDC RevisedDocument13 pagesUDC RevisedAbdul QayumNo ratings yet

- Ekonomi Global: Willem A. Makaliwe (Lembaga Management FEBUI) 2021Document14 pagesEkonomi Global: Willem A. Makaliwe (Lembaga Management FEBUI) 2021Irma SuryaniNo ratings yet

- ML Stragegic Balance INDEX - FACT SHEETDocument3 pagesML Stragegic Balance INDEX - FACT SHEETRaj JarNo ratings yet

- Tata CommunicationDocument5 pagesTata CommunicationkmmohammedroshanNo ratings yet

- MacrodurDocument41 pagesMacrodurnoel_manroeNo ratings yet

- Fixed Income - Part II SolutionsDocument50 pagesFixed Income - Part II SolutionsJohnNo ratings yet

- SG Volatility Trading Index: Monthly Return For: Jun 2020Document2 pagesSG Volatility Trading Index: Monthly Return For: Jun 2020medit_99No ratings yet

- Chapter 3 Part 3Document30 pagesChapter 3 Part 3Aditya GhoshNo ratings yet

- Long Lasting ResourcesDocument41 pagesLong Lasting ResourcesOsmar ZayasNo ratings yet

- AMFEIX - Monthly Report (April 2020)Document16 pagesAMFEIX - Monthly Report (April 2020)PoolBTCNo ratings yet

- Depozite Bancare Feb 2021Document7 pagesDepozite Bancare Feb 2021Mihaela DumitritaNo ratings yet

- Public Disclosure For LI BDocument1 pagePublic Disclosure For LI BShashankNo ratings yet

- Rafeeqa Begum (DPR)Document13 pagesRafeeqa Begum (DPR)syedNo ratings yet

- Financial Statement Analysis FIN3111Document9 pagesFinancial Statement Analysis FIN3111Zile MoazzamNo ratings yet

- Balanced Scorecard Report: Corporate Owner Fresnillo OperationsDocument4 pagesBalanced Scorecard Report: Corporate Owner Fresnillo OperationsShun De VazNo ratings yet

- CF Report Fall 2018Document24 pagesCF Report Fall 2018Tamal GhoshNo ratings yet

- Mean and Standard Deviation SolutionDocument4 pagesMean and Standard Deviation SolutionC.E.O AnnieNo ratings yet

- UBL FMR May 24 1Document34 pagesUBL FMR May 24 1Zubair RahimNo ratings yet

- Rdy Mad e Pmegp 5lacsDocument12 pagesRdy Mad e Pmegp 5lacssyedNo ratings yet

- Weekly Report As of 30th Dec'18Document1 pageWeekly Report As of 30th Dec'18MohdSirajul IslamNo ratings yet

- EPGPX02 Group 3 - Strategic Decisions and ToolsDocument14 pagesEPGPX02 Group 3 - Strategic Decisions and ToolsrishiNo ratings yet

- Technology Incentive Plan - TECHIP: Year 2019-20Document4 pagesTechnology Incentive Plan - TECHIP: Year 2019-20vikasarya044No ratings yet

- Mortgage Delinquency Rates: Mba Commercial/MultifamilyDocument10 pagesMortgage Delinquency Rates: Mba Commercial/MultifamilyZerohedgeNo ratings yet

- Weekly 1000 0.1 LotDocument39 pagesWeekly 1000 0.1 LotLukas BastianNo ratings yet

- Portfolio's KPIs Calculations TemplateDocument7 pagesPortfolio's KPIs Calculations TemplateGARVIT GoyalNo ratings yet

- High Performance Beverages Co. (TBEV)Document27 pagesHigh Performance Beverages Co. (TBEV)MNM MahmuddinNo ratings yet

- Net Revenue Cost of Sales Gross Profit Ebit - Operating Result Ebitda Net IncomeDocument15 pagesNet Revenue Cost of Sales Gross Profit Ebit - Operating Result Ebitda Net IncomevhibeeNo ratings yet

- This Session: Financial Status of BankDocument63 pagesThis Session: Financial Status of BankR CHUNGNo ratings yet

- Kongkaikai 10 Writing Materials#Document7 pagesKongkaikai 10 Writing Materials#abiramieNo ratings yet

- Financial GAPsDocument5 pagesFinancial GAPsGabriel FernandesNo ratings yet

- Edgestone Capital Equity FundDocument2 pagesEdgestone Capital Equity Fund/jncjdncjdnNo ratings yet

- Performance Evaluation of Pharmacetical IndustryDocument9 pagesPerformance Evaluation of Pharmacetical IndustryReport AnalysisNo ratings yet

- Lit. Review1Document1 pageLit. Review1Jalpesh BavishiNo ratings yet

- View BenchmarkDocument12 pagesView BenchmarkIoana StoicescuNo ratings yet

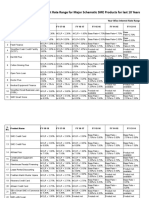

- Interest Rates For Last 10 Yr For Major SME ProductsDocument6 pagesInterest Rates For Last 10 Yr For Major SME Productssharad1996No ratings yet

- Samsung Electronics: Earnings Release Q2 2016Document8 pagesSamsung Electronics: Earnings Release Q2 2016Syed Mohd AliNo ratings yet

- AMFEIX - Monthly Report (March 2020)Document17 pagesAMFEIX - Monthly Report (March 2020)PoolBTCNo ratings yet

- Guide to Management Accounting CCC for managers 2020 EditionFrom EverandGuide to Management Accounting CCC for managers 2020 EditionNo ratings yet

- Financial Access in Nepal: (Exploring The Feature of Deposit Accounts of A, B, C Class Bfis)Document25 pagesFinancial Access in Nepal: (Exploring The Feature of Deposit Accounts of A, B, C Class Bfis)Utsav Raj PantNo ratings yet

- Executive SummaryDocument3 pagesExecutive SummaryUtsav Raj PantNo ratings yet

- Derivatives Final ReportDocument6 pagesDerivatives Final ReportUtsav Raj PantNo ratings yet

- Final Exam Marks Individual Assignment Cases ProjectDocument1 pageFinal Exam Marks Individual Assignment Cases ProjectUtsav Raj PantNo ratings yet

- M&A As A Driver of Global Competition in The Brewing IndustryDocument24 pagesM&A As A Driver of Global Competition in The Brewing IndustryUtsav Raj PantNo ratings yet

- Analyze The Current Nepali Market Situation by Analyzing A Slide Posted With This AssignmentDocument6 pagesAnalyze The Current Nepali Market Situation by Analyzing A Slide Posted With This AssignmentUtsav Raj PantNo ratings yet

- Stock Market Experience: Utsav Raj Pant Roll: 19324Document7 pagesStock Market Experience: Utsav Raj Pant Roll: 19324Utsav Raj PantNo ratings yet

- Behaviour Finance LEGAL ENVIROMENTDocument10 pagesBehaviour Finance LEGAL ENVIROMENTUtsav Raj PantNo ratings yet

- Session 8 PDFDocument12 pagesSession 8 PDFUtsav Raj PantNo ratings yet

- Format For Business Model DevelopmentDocument1 pageFormat For Business Model DevelopmentUtsav Raj PantNo ratings yet

- Kathmandu University School of ManagementDocument15 pagesKathmandu University School of ManagementUtsav Raj PantNo ratings yet

- Strategic Resources A. Core Competencies 1. Constant InnovationDocument11 pagesStrategic Resources A. Core Competencies 1. Constant InnovationUtsav Raj PantNo ratings yet

- Consciousness and How The Brain Works To Be Fascinating Utsav Raj Pant, 19324Document3 pagesConsciousness and How The Brain Works To Be Fascinating Utsav Raj Pant, 19324Utsav Raj PantNo ratings yet

- Stock Cumulative Abnormal Return (CAR) T-Statistics P-Value SignificanceDocument5 pagesStock Cumulative Abnormal Return (CAR) T-Statistics P-Value SignificanceUtsav Raj PantNo ratings yet

- Behaviour Finance Replacement1Document4 pagesBehaviour Finance Replacement1Utsav Raj PantNo ratings yet

- The Emergence of IMC: A Theoretical PerspectiveDocument6 pagesThe Emergence of IMC: A Theoretical PerspectiveUtsav Raj PantNo ratings yet

- An Invitation ToDocument1 pageAn Invitation ToUtsav Raj PantNo ratings yet

- Nepalese Foreign Trade: Growth, Composition, and Direction: Vol. 4, No. 1Document6 pagesNepalese Foreign Trade: Growth, Composition, and Direction: Vol. 4, No. 1Utsav Raj PantNo ratings yet

- List of All SWIFT-ISO MessagesDocument47 pagesList of All SWIFT-ISO Messagessanjayjogs50% (2)

- Trading Rules English Wealth Multiplier - Google Docs 2023 31 08 03 59 26Document31 pagesTrading Rules English Wealth Multiplier - Google Docs 2023 31 08 03 59 26Sunny KhetarpalNo ratings yet

- 3 Chart Patterns Cheat SheetDocument7 pages3 Chart Patterns Cheat SheetAka Akou Jean-Jacques LouisNo ratings yet

- Case SynopsisDocument3 pagesCase SynopsisManu BhikshamNo ratings yet

- Dabur Strategy FinalDocument22 pagesDabur Strategy FinalDesktop PCNo ratings yet

- Marketing Mix Marketing Strategies of Nagarjuna Fertilizers and Chemical LimitedDocument6 pagesMarketing Mix Marketing Strategies of Nagarjuna Fertilizers and Chemical LimitedpawanNo ratings yet

- Derivatives NotesDocument194 pagesDerivatives NotesnirleshtiwariNo ratings yet

- Assignment4 SolutionsDocument13 pagesAssignment4 SolutionsLetícia S. RezendeNo ratings yet

- HDFC Bank - We Understand Your World - Stock Analysis & ValuationDocument93 pagesHDFC Bank - We Understand Your World - Stock Analysis & ValuationDeep SukhwaniNo ratings yet

- Options Animal 2011 Event NotesDocument3 pagesOptions Animal 2011 Event NotesvajrapNo ratings yet

- Baby Food in India DatagraphicsDocument7 pagesBaby Food in India DatagraphicsRaheetha AhmedNo ratings yet

- Keys To Trading Gold USDocument15 pagesKeys To Trading Gold USMo AlamNo ratings yet

- International Financial Management 11 Edition: by Jeff MaduraDocument33 pagesInternational Financial Management 11 Edition: by Jeff MaduraCorolla SedanNo ratings yet

- SHAREHOLDERSDocument6 pagesSHAREHOLDERSJoana MarieNo ratings yet

- Dissertation On Stock Market in IndiaDocument5 pagesDissertation On Stock Market in IndiaBuyPsychologyPapersUK100% (1)

- Profit and Loss: Type I - Basic QuestionsDocument4 pagesProfit and Loss: Type I - Basic QuestionsSanskruti KhedkarNo ratings yet

- Seminar 3 2017Document85 pagesSeminar 3 2017Stephanie XieNo ratings yet

- There Are Six Basic Elements in Promotion Mix and Toilet Soap Industries Can Use Those Elements To Promote Their BrandsDocument7 pagesThere Are Six Basic Elements in Promotion Mix and Toilet Soap Industries Can Use Those Elements To Promote Their BrandsdhivagarNo ratings yet

- (Download PDF) Corporate Finance For Business The Essential Concepts Ronny Manos Full Chapter PDFDocument69 pages(Download PDF) Corporate Finance For Business The Essential Concepts Ronny Manos Full Chapter PDFgidneyaruci100% (10)

- GRP5 Fur Fect Match Final SIGNEDDocument150 pagesGRP5 Fur Fect Match Final SIGNEDJaezar Philip Francisco GragasinNo ratings yet

- Market Research IndustryDocument8 pagesMarket Research IndustryMEERA MEHTANo ratings yet

- Module 9Document12 pagesModule 9Johanna RullanNo ratings yet

- Futures and Options On Foreign Exchange: International Financial ManagementDocument50 pagesFutures and Options On Foreign Exchange: International Financial ManagementvijiNo ratings yet

- Distributing Services Through Physical and Electronic ChannelsDocument25 pagesDistributing Services Through Physical and Electronic ChannelsAnoshia AdnanNo ratings yet

- Bba Chapter 4 Pricing Under Various Market ConditionsDocument21 pagesBba Chapter 4 Pricing Under Various Market ConditionsDr-Abu Hasan Sonai SheikhNo ratings yet

- Zomato Part 2Document6 pagesZomato Part 2bestalok.001No ratings yet

- Market ResearchDocument44 pagesMarket ResearchNafi100% (1)