Download as docx, pdf, or txt

You might also like

- Gitman Chapter 3 SolutionDocument21 pagesGitman Chapter 3 SolutionNauman Iqbal75% (4)

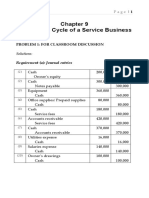

- Sol. Man. - Chapter 9 - Acctg Cycle of A Service BusinessDocument52 pagesSol. Man. - Chapter 9 - Acctg Cycle of A Service Businesscan't yujout80% (5)

- Toy Factory Worksheet For The Year Ended Dec. 31, 20X4 Account Titles Trial Balance Adjustments Debit Credit DebitDocument12 pagesToy Factory Worksheet For The Year Ended Dec. 31, 20X4 Account Titles Trial Balance Adjustments Debit Credit DebitShiela EscobarNo ratings yet

- Case 4 2Document5 pagesCase 4 2Marjorie Morada67% (3)

- 1.0 Question 1 (CLO 1) : 2 External Users of Accounting InvestorsDocument2 pages1.0 Question 1 (CLO 1) : 2 External Users of Accounting InvestorsSufian Abd RahimNo ratings yet

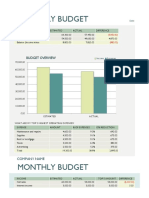

- Monthly Business Budget1Document1 pageMonthly Business Budget1Vu PhungNo ratings yet

- Windowlux - Case SolutionDocument2 pagesWindowlux - Case SolutionanisaNo ratings yet

- Monthly Budget: Company NameDocument2 pagesMonthly Budget: Company NameJo ReenNo ratings yet

- Budget ControllingDocument1 pageBudget ControllingLester ErlanoNo ratings yet

- Basic Accounting ExerciseDocument5 pagesBasic Accounting ExercisechubbybunbunNo ratings yet

- Answers To CH 2 - FTW ProblemsDocument14 pagesAnswers To CH 2 - FTW ProblemsJuanito Jr. LagnoNo ratings yet

- Corporate Tax Return Project Book-Tax Reconciliation (Adrian Purnama)Document6 pagesCorporate Tax Return Project Book-Tax Reconciliation (Adrian Purnama)akpNo ratings yet

- Budget Template With ChartsDocument1 pageBudget Template With ChartsAli ErlanggaNo ratings yet

- Group 2 - ContinuingProblem - Chapter 2Document14 pagesGroup 2 - ContinuingProblem - Chapter 2Jude TumamposNo ratings yet

- Assignment Ex 21-22Document9 pagesAssignment Ex 21-22charmvielNo ratings yet

- ABC 10-ColumnDocument1 pageABC 10-Columnpor wansNo ratings yet

- Itax Solutions Philippines Income Statement Working Paper No. of Client Ave. Rate Per Client Frequency /year 2023 449,000.00Document13 pagesItax Solutions Philippines Income Statement Working Paper No. of Client Ave. Rate Per Client Frequency /year 2023 449,000.00Rose CastilloNo ratings yet

- Computation For Exercise 1Document10 pagesComputation For Exercise 1Xyzra AlfonsoNo ratings yet

- IA Chapter-11-14Document7 pagesIA Chapter-11-14Christine Joyce EnriquezNo ratings yet

- LabChapt 4 Meisya Vianqa ADocument7 pagesLabChapt 4 Meisya Vianqa AMeisya VianqaNo ratings yet

- Sample Problems Solutions On BE, & SensitivityDocument5 pagesSample Problems Solutions On BE, & SensitivityJedrek DyNo ratings yet

- Accounting RefresherDocument2 pagesAccounting RefresherAlbert MorenoNo ratings yet

- ASSIGNMENT BBAW2103 - Financial AccountingDocument13 pagesASSIGNMENT BBAW2103 - Financial AccountingMUHAMMAD NAJIB BIN HAMBALI STUDENTNo ratings yet

- MC Problems Chap 2Document4 pagesMC Problems Chap 2AlexandriteNo ratings yet

- (Bme - Group 3) Financial-Transaction-Worksheet-Sweet-Sea-Restaurant-Answers-1-4Document13 pages(Bme - Group 3) Financial-Transaction-Worksheet-Sweet-Sea-Restaurant-Answers-1-4Kyla Marie BayanNo ratings yet

- Exercises On Implementation of DCF ApproachDocument10 pagesExercises On Implementation of DCF ApproachVincenzoPizzulliNo ratings yet

- Account Debit CreditDocument4 pagesAccount Debit CreditMcKenzie WNo ratings yet

- Chapter 2 DoneDocument30 pagesChapter 2 Doneellyzamae quiraoNo ratings yet

- Practice Problems2Document48 pagesPractice Problems2vipinkala1100% (1)

- Answer Sheet Work RelatedDocument41 pagesAnswer Sheet Work RelatedjoyhhazelNo ratings yet

- Monthly Company Budget1Document4 pagesMonthly Company Budget1Brian SetterNo ratings yet

- AE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBDocument7 pagesAE 315 FM Sum2021 Week 3 Capital Budgeting Quiz Anserki B FOR DISTRIBArly Kurt TorresNo ratings yet

- Financial Statements AnalysisDocument1 pageFinancial Statements AnalysisDELA CRUZ Jesseca V.No ratings yet

- Cleaners WorksheetDocument1 pageCleaners WorksheetSeijuro Akashi100% (1)

- Cleaners WorksheetDocument1 pageCleaners WorksheetSeijuro AkashiNo ratings yet

- Monthly Budget: Company NameDocument2 pagesMonthly Budget: Company NameMalleshNo ratings yet

- Cleaners WorksheetDocument1 pageCleaners WorksheetCracklings Gacuma100% (3)

- Solutions To End-Of-Chapter ProblemsDocument4 pagesSolutions To End-Of-Chapter ProblemsRab RakhaNo ratings yet

- Preparing The Working PaperDocument5 pagesPreparing The Working PaperChriszel Dianne DamasingNo ratings yet

- Presentation 1Document2 pagesPresentation 1apolsoftNo ratings yet

- FPQ1 - Answer KeyDocument6 pagesFPQ1 - Answer KeyJi YuNo ratings yet

- The Accounting Cycle PHASE 1 - RECORDING AND CLASSIFYING PROCESS (During The Accounting Period)Document19 pagesThe Accounting Cycle PHASE 1 - RECORDING AND CLASSIFYING PROCESS (During The Accounting Period)Allondra DapengNo ratings yet

- Accn 101 Assignment Group WorkDocument8 pagesAccn 101 Assignment Group WorkkumbiraidavidNo ratings yet

- Please Kindly Joint With Us For More:: - Facebook Group: Cambodia Accounting and TaxDocument2 pagesPlease Kindly Joint With Us For More:: - Facebook Group: Cambodia Accounting and TaxLay TekchhayNo ratings yet

- Financial Trial BalanceDocument3 pagesFinancial Trial BalanceOnaderu Oluwagbenga EnochNo ratings yet

- Assignment 2 FAC2601 RevisionDocument5 pagesAssignment 2 FAC2601 RevisionmisslxmasherNo ratings yet

- Practice Problem SolutionDocument15 pagesPractice Problem SolutionTherese Noelle R. ARMADA100% (1)

- Spring Day Company Statement of Financial Position For 20x1 and 20x2Document2 pagesSpring Day Company Statement of Financial Position For 20x1 and 20x2Printing PandaNo ratings yet

- BT Tổng Hợp Topic 7 8 2Document12 pagesBT Tổng Hợp Topic 7 8 2Man Tran Y NhiNo ratings yet

- Book 110Document10 pagesBook 110Maria Dana BrillantesNo ratings yet

- Financial Transaction WorksheetDocument3 pagesFinancial Transaction WorksheetRachel OtazaNo ratings yet

- Chapter 14Document5 pagesChapter 14Kiminosunoo LelNo ratings yet

- Tutorial 7Document3 pagesTutorial 7Steven CHONGNo ratings yet

- Tahbeer Financial Plan - Financial PlanDocument7 pagesTahbeer Financial Plan - Financial PlanSonam GulzarNo ratings yet

- Drew SicatDocument1 pageDrew SicatShaine Cabualan SeroyNo ratings yet

- Monthly Budget Test: Company NameDocument4 pagesMonthly Budget Test: Company NameveeraaaNo ratings yet

- H.W ch4q7 Acc418Document4 pagesH.W ch4q7 Acc418SARA ALKHODAIRNo ratings yet

- Transaction Analysis Janelle'SRESTAURANTDocument2 pagesTransaction Analysis Janelle'SRESTAURANTReana ReyesNo ratings yet

- Monthly Business BudgetDocument4 pagesMonthly Business BudgetOkasha HafeezNo ratings yet

- Assessment 1 - Assignment 1Document5 pagesAssessment 1 - Assignment 1Ten NineNo ratings yet

- Exercise #11 (Sue Feria) DehnieceMangawangDocument3 pagesExercise #11 (Sue Feria) DehnieceMangawangPhaelyn YambaoNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Take Home Examination: May 2021 SemesterDocument3 pagesTake Home Examination: May 2021 SemesterSufian Abd RahimNo ratings yet

- Take Home Examination: May 2021 SemesterDocument2 pagesTake Home Examination: May 2021 SemesterSufian Abd RahimNo ratings yet

- Take Home Examination: May 2021 SemesterDocument4 pagesTake Home Examination: May 2021 SemesterSufian Abd RahimNo ratings yet

- Take Home Examination Bbma3203Document6 pagesTake Home Examination Bbma3203Sufian Abd RahimNo ratings yet

- 1.0 Question 1 (CLO 1) : 2 External Users of Accounting InvestorsDocument2 pages1.0 Question 1 (CLO 1) : 2 External Users of Accounting InvestorsSufian Abd RahimNo ratings yet

- Chapter 3. Gross IncomeDocument6 pagesChapter 3. Gross IncomeAlyssa Joy TercenioNo ratings yet

- BDEK2203 Introductory Macroeconomics - Smay19 (MREP)Document187 pagesBDEK2203 Introductory Macroeconomics - Smay19 (MREP)Sanjay KumarNo ratings yet

- Chapter No.40Document6 pagesChapter No.40Kamal SinghNo ratings yet

- Proc NO. 286-2002 Income TaxDocument39 pagesProc NO. 286-2002 Income TaxZelalemtil88% (8)

- TASK 3 - Activity 1Document2 pagesTASK 3 - Activity 1Jose LopezNo ratings yet

- Corporate Finance Core Principles and Applications 3rd Edition Ross Test BankDocument65 pagesCorporate Finance Core Principles and Applications 3rd Edition Ross Test BankChristopherDyerkczqw100% (20)

- Financial Analysis DFPCLDocument13 pagesFinancial Analysis DFPCLSiddharth Rohilla (M22MS074)No ratings yet

- Accounting End Semester ProjectDocument32 pagesAccounting End Semester ProjectGulzar JamalNo ratings yet

- Responsibility Accounting and Transfer PricingDocument11 pagesResponsibility Accounting and Transfer PricingMaryane AngelaNo ratings yet

- 4801-Article Text-19217-1-10-20110701Document8 pages4801-Article Text-19217-1-10-20110701David BriggsNo ratings yet

- PDF 298947820220321Document1 pagePDF 298947820220321savitakant13600No ratings yet

- Henok Tekle Wholesale of CerealsDocument16 pagesHenok Tekle Wholesale of Cerealsterefe kassaNo ratings yet

- Return On Invested Capital (ROIC) or Return On Investment (ROI)Document5 pagesReturn On Invested Capital (ROIC) or Return On Investment (ROI)AmelieNo ratings yet

- Neral Format: Photo (Affix For Each Applic Ant)Document6 pagesNeral Format: Photo (Affix For Each Applic Ant)Vasan DivNo ratings yet

- Grade 12 EconomicsDocument7 pagesGrade 12 EconomicsAditya GoyalNo ratings yet

- Weekly Income and Expenses ofDocument23 pagesWeekly Income and Expenses ofKevin Rey CaballeroNo ratings yet

- Chapter 10Document12 pagesChapter 10Villanueva, Jane G.No ratings yet

- EA EA1 SU2 OutlineDocument23 pagesEA EA1 SU2 OutlineAashu AntilNo ratings yet

- CA Inter Taxation Suggested Answer May 2022Document30 pagesCA Inter Taxation Suggested Answer May 2022ileshrathod0No ratings yet

- Talisaysay Jomar A. Report On Unit VIII A BudgetingDocument32 pagesTalisaysay Jomar A. Report On Unit VIII A Budgetingnaiar kramNo ratings yet

- Deutsche Finan ExcelDocument6 pagesDeutsche Finan ExcelAnonymous VVSLkDOAC1No ratings yet

- The Rationale of Financing EducationDocument15 pagesThe Rationale of Financing Educationmuna moonoNo ratings yet

- SCCO LKT Per 31 Des 2022Document87 pagesSCCO LKT Per 31 Des 2022Jefri Formen PangaribuanNo ratings yet

- Deferred Tax Accounting - Lecture NotesDocument6 pagesDeferred Tax Accounting - Lecture Notesmax pNo ratings yet

- Financial Ratio AnalysisDocument85 pagesFinancial Ratio AnalysisSarah PontinesNo ratings yet

- Jan 2023Document13 pagesJan 2023Aina OyenNo ratings yet

- TaxmannPPT Impact of Ind AS On Corporate Tax 1686937084Document32 pagesTaxmannPPT Impact of Ind AS On Corporate Tax 1686937084Praveen KumarNo ratings yet

- Mohali Juice T-ShirtsDocument6 pagesMohali Juice T-ShirtsSubhash MishraNo ratings yet