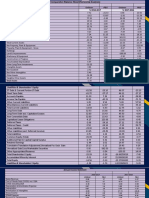

Hieu Nguyen Valuation Description: Domino Pizza (DPZ)

Hieu Nguyen Valuation Description: Domino Pizza (DPZ)

You might also like

- AQA A Level Business Topic 3.5 Unit AssessmentDocument4 pagesAQA A Level Business Topic 3.5 Unit AssessmentGeorge Butler67% (3)

- Sample Audited Financial Statements For Sole Proprietorship PDFDocument16 pagesSample Audited Financial Statements For Sole Proprietorship PDFKristen100% (3)

- Walmart Valuation ModelDocument179 pagesWalmart Valuation ModelHiếu Nguyễn Minh HoàngNo ratings yet

- Diageo Case Write UpDocument10 pagesDiageo Case Write UpAmandeep AroraNo ratings yet

- Word Note California Pizza KitchenDocument7 pagesWord Note California Pizza Kitchenalka murarka100% (16)

- Assess Boston Chicken's Business Strategy by Identifying Its Critical Success FactorsDocument4 pagesAssess Boston Chicken's Business Strategy by Identifying Its Critical Success FactorsArindam PalNo ratings yet

- Investment Thesis PDFDocument1 pageInvestment Thesis PDFchatuuuu123No ratings yet

- Boston ChickenDocument4 pagesBoston ChickenSaurabh SinghalNo ratings yet

- Horniman HorticultureDocument11 pagesHorniman Horticultureangela4620100% (2)

- Finmar Quiz 4Document10 pagesFinmar Quiz 4Roderica RegorisNo ratings yet

- California Kitchen Case StudyDocument9 pagesCalifornia Kitchen Case StudyBYQNo ratings yet

- How To Start A Pizza Business: A Complete Pizza Parlor & Pizza Delivery Business PlanFrom EverandHow To Start A Pizza Business: A Complete Pizza Parlor & Pizza Delivery Business PlanNo ratings yet

- 2fa3 Group Project 1Document15 pages2fa3 Group Project 1api-588408469No ratings yet

- End To End Predictive Analysis On ZomatoDocument21 pagesEnd To End Predictive Analysis On ZomatoAmit SinghNo ratings yet

- 01.1 - Small Business - 090121Document10 pages01.1 - Small Business - 090121Xcill EnzeNo ratings yet

- PolarSports Solution PDFDocument8 pagesPolarSports Solution PDFaotorres99No ratings yet

- T 8Document3 pagesT 8Hamayoon AhmedNo ratings yet

- Security Industry Analysis Report Final DraftDocument17 pagesSecurity Industry Analysis Report Final Draftapi-663792863No ratings yet

- Forecast of Balance Sheet 2.1 Assets Cash and Cash EquivalentDocument4 pagesForecast of Balance Sheet 2.1 Assets Cash and Cash EquivalentQuyên HoàngNo ratings yet

- AssumptionsDocument4 pagesAssumptionsNIMESH BHATTNo ratings yet

- O.M. Scott & SonsDocument7 pagesO.M. Scott & Sonsstig2lufetNo ratings yet

- Case SolutionDocument9 pagesCase Solutiontiko100% (1)

- California Pizza KitchenDocument3 pagesCalifornia Pizza KitchenTommy HaleyNo ratings yet

- American Apparel. Drowning in Debt?Document7 pagesAmerican Apparel. Drowning in Debt?Ojas GuptaNo ratings yet

- FAUE InterpretationDocument4 pagesFAUE InterpretationAnkit PatidarNo ratings yet

- Ratio Analysis: Mari Perolum Company LimitiedDocument5 pagesRatio Analysis: Mari Perolum Company LimitiedNuman AhmedNo ratings yet

- Boston ChickenDocument10 pagesBoston ChickenRoptaNo ratings yet

- Dominos ReportDocument20 pagesDominos ReportDisha HalderNo ratings yet

- Dominos ReportDocument20 pagesDominos Reportkuntaljariwala100% (1)

- Assignment-2 (New) PDFDocument12 pagesAssignment-2 (New) PDFminnie908No ratings yet

- 2024 04 24 Chipotle Announces First Quarter 2024 ResultsDocument8 pages2024 04 24 Chipotle Announces First Quarter 2024 Resultsanujdas173No ratings yet

- Zomato Limited ( Zomato' or Company') - IPO Valuation: "Scaling-Up Challenge"Document7 pagesZomato Limited ( Zomato' or Company') - IPO Valuation: "Scaling-Up Challenge"Rajesh KumarNo ratings yet

- Lloyds Banking Group PLC - Q1 2019 Interim Management Statement - TranscriptDocument14 pagesLloyds Banking Group PLC - Q1 2019 Interim Management Statement - TranscriptsaxobobNo ratings yet

- Ar&Inventory ManagementDocument10 pagesAr&Inventory ManagementKarlo D. ReclaNo ratings yet

- Summery of California Pizza Kitchen CaseDocument1 pageSummery of California Pizza Kitchen CaseAbid Ullah67% (3)

- Ar ManagementDocument6 pagesAr ManagementKarlo D. ReclaNo ratings yet

- 1 Https://indianceo - In/business/buzz-Zomato-ValuationDocument3 pages1 Https://indianceo - In/business/buzz-Zomato-ValuationAnkit JaiNo ratings yet

- Financial Management Test BankDocument2 pagesFinancial Management Test BankRenalyn SanchezNo ratings yet

- Zomato IPO DRHP Takeaways JST InvestmentsDocument21 pagesZomato IPO DRHP Takeaways JST InvestmentsJoel MenezesNo ratings yet

- DENN Jan 2016 Investor PresentationDocument30 pagesDENN Jan 2016 Investor PresentationAla BasterNo ratings yet

- Capital Structure and Leverage Quiz # 3Document4 pagesCapital Structure and Leverage Quiz # 3Maurice Hanellete EspirituNo ratings yet

- Edited Transcript: Thomson Reuters StreeteventsDocument17 pagesEdited Transcript: Thomson Reuters Streeteventspe_canNo ratings yet

- Final ReportDocument46 pagesFinal ReportAndrew GilmanNo ratings yet

- California Pizza Kitchen - AnalysisDocument6 pagesCalifornia Pizza Kitchen - AnalysisVasili RabshtynaNo ratings yet

- Integrated Case 3-20Document5 pagesIntegrated Case 3-20Cayden BrookeNo ratings yet

- FIN 302 Notes 1Document55 pagesFIN 302 Notes 1Tekego TlakaleNo ratings yet

- Assignment BBA 2004Document19 pagesAssignment BBA 2004ChaiNo ratings yet

- Alphacom - Maha Tayyab TestDocument8 pagesAlphacom - Maha Tayyab TestMaha TayyabNo ratings yet

- Q3FY24 Shareholders' Letter and ResultsDocument21 pagesQ3FY24 Shareholders' Letter and ResultsDhaval 181No ratings yet

- Financing NetflixDocument16 pagesFinancing Netflix10oandreaNo ratings yet

- Brief IntroductionDocument4 pagesBrief Introductionc.trang99No ratings yet

- 00-Text-Ch3 Additional Problems UpdatedDocument6 pages00-Text-Ch3 Additional Problems Updatedzombies_meNo ratings yet

- Case: Debt Policy at UST Inc. - Protagonist: Vincent GiererDocument2 pagesCase: Debt Policy at UST Inc. - Protagonist: Vincent GiererSu_NeilNo ratings yet

- Aud TheoDocument2 pagesAud Theonivea gumayagayNo ratings yet

- HDFC Standard Life Insurance Company Limited: Six Months Ended September 2010Document22 pagesHDFC Standard Life Insurance Company Limited: Six Months Ended September 2010Dilip RajNo ratings yet

- Name: - Date: - QuizDocument4 pagesName: - Date: - QuizKatrine Clarisse BlanquiscoNo ratings yet

- Fit Co. InterpretationDocument3 pagesFit Co. InterpretationAbishek GuptaNo ratings yet

- A Complete Pizza Restaurant Business Plan: A Key Part Of How To Start A Pizza Parlor & Delivery BusinessFrom EverandA Complete Pizza Restaurant Business Plan: A Key Part Of How To Start A Pizza Parlor & Delivery BusinessRating: 5 out of 5 stars5/5 (1)

- How To Start A Payroll & Bookkeeping Service: A Complete Payroll & Bookkeeping Service Business PlanFrom EverandHow To Start A Payroll & Bookkeeping Service: A Complete Payroll & Bookkeeping Service Business PlanNo ratings yet

- A Complete Payroll & Bookkeeping Service Business Plan: A Key Part Of How To Start A Payroll & BookkeepingFrom EverandA Complete Payroll & Bookkeeping Service Business Plan: A Key Part Of How To Start A Payroll & BookkeepingNo ratings yet

- Guide to Japan-Born Inventory and Accounts Receivable Freshness Control for Managers 2017 (English Version)From EverandGuide to Japan-Born Inventory and Accounts Receivable Freshness Control for Managers 2017 (English Version)No ratings yet

- Seven Components of Strategic Staffing Workforce Planning DescriptionDocument6 pagesSeven Components of Strategic Staffing Workforce Planning DescriptionHiếu Nguyễn Minh HoàngNo ratings yet

- HR QuestionsDocument2 pagesHR QuestionsHiếu Nguyễn Minh HoàngNo ratings yet

- Name: Hieu Nguyen FIN 516: Managerial Macroeconomic Prof. Jessica RutledgeDocument10 pagesName: Hieu Nguyen FIN 516: Managerial Macroeconomic Prof. Jessica RutledgeHiếu Nguyễn Minh HoàngNo ratings yet

- Market Risk PremiumDocument1 pageMarket Risk PremiumHiếu Nguyễn Minh HoàngNo ratings yet

- HieuNguyen - ACTG 560 - Written Analysis 2Document1 pageHieuNguyen - ACTG 560 - Written Analysis 2Hiếu Nguyễn Minh HoàngNo ratings yet

- Prepare Standard and Customized Investment Performance Reports Communicate With Internal and External Clients Collect, Input, Analyze, and Reconcile Data Market ResearchDocument2 pagesPrepare Standard and Customized Investment Performance Reports Communicate With Internal and External Clients Collect, Input, Analyze, and Reconcile Data Market ResearchHiếu Nguyễn Minh HoàngNo ratings yet

- MGMT 471 Final Paper RubricDocument3 pagesMGMT 471 Final Paper RubricHiếu Nguyễn Minh HoàngNo ratings yet

- ACGT Term PaperDocument11 pagesACGT Term PaperHiếu Nguyễn Minh HoàngNo ratings yet

- Hieu Nguyen Cutting Through The Fog-Case OverviewDocument2 pagesHieu Nguyen Cutting Through The Fog-Case OverviewHiếu Nguyễn Minh HoàngNo ratings yet

- Total Factors Supplyings Reserve Funds: Securities Held OutrightDocument3 pagesTotal Factors Supplyings Reserve Funds: Securities Held OutrightHiếu Nguyễn Minh HoàngNo ratings yet

- Walgreens Boots Alliance, Inc. and Subsidiaries: Capitalize STMT of Op Lease ReclassDocument7 pagesWalgreens Boots Alliance, Inc. and Subsidiaries: Capitalize STMT of Op Lease ReclassHiếu Nguyễn Minh HoàngNo ratings yet

- MidtermDocument8 pagesMidtermHiếu Nguyễn Minh HoàngNo ratings yet

- Final Exam PreparationDocument4 pagesFinal Exam PreparationHiếu Nguyễn Minh HoàngNo ratings yet

- FIN 456 International Financial Management: The Market For Foreign ExchangeDocument35 pagesFIN 456 International Financial Management: The Market For Foreign ExchangeHiếu Nguyễn Minh HoàngNo ratings yet

- PSU Code of Student Conduct: School of Business Honors Program - Student Behavior ExpectationsDocument2 pagesPSU Code of Student Conduct: School of Business Honors Program - Student Behavior ExpectationsHiếu Nguyễn Minh HoàngNo ratings yet

- Additional Instructions For Mailing Your Package: Drop Off LocatorDocument1 pageAdditional Instructions For Mailing Your Package: Drop Off LocatorHiếu Nguyễn Minh HoàngNo ratings yet

- Ms Finance EssayDocument1 pageMs Finance EssayHiếu Nguyễn Minh HoàngNo ratings yet

- Chapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDocument47 pagesChapter 5: Option Pricing Models: The Black-Scholes-Merton ModelHiếu Nguyễn Minh HoàngNo ratings yet

- Odel Canvas: Key Partners Key Activities Value Proposition Customer Relationships Customer SegmentsDocument2 pagesOdel Canvas: Key Partners Key Activities Value Proposition Customer Relationships Customer SegmentsHiếu Nguyễn Minh HoàngNo ratings yet

- Investment Banking Valuation Leveraged Buyouts and Mergers and Acquisitions 2Nd Edition Rosenbaum Test Bank Full Chapter PDFDocument43 pagesInvestment Banking Valuation Leveraged Buyouts and Mergers and Acquisitions 2Nd Edition Rosenbaum Test Bank Full Chapter PDFWilliamCartersafg100% (14)

- Philippine Postal Corporation Notes To Financial Statements 1. Agency ProfileDocument15 pagesPhilippine Postal Corporation Notes To Financial Statements 1. Agency ProfileJD BallosNo ratings yet

- LedgerDocument3 pagesLedgerAnonnNo ratings yet

- FS Preparation and Correcting A TBDocument11 pagesFS Preparation and Correcting A TBJulia Mae AlbanoNo ratings yet

- Npo NotesDocument12 pagesNpo Notesmukeshadm123No ratings yet

- Financial Management R. KitDocument241 pagesFinancial Management R. KitDamaris100% (1)

- FFS - NumericalsDocument5 pagesFFS - NumericalsFunny ManNo ratings yet

- Financial Analysis of Everest BankDocument27 pagesFinancial Analysis of Everest BankRazel TercinoNo ratings yet

- GR 12 Accounting P2 Eng - x5Document12 pagesGR 12 Accounting P2 Eng - x5lnaidoo2006No ratings yet

- Acca Supplementary NotesDocument185 pagesAcca Supplementary NotesSuniel JamilNo ratings yet

- Specific Project WorkDocument70 pagesSpecific Project Workajay meenaNo ratings yet

- Ch.12 - 13ed Fin Planning & ForecastingMasterDocument47 pagesCh.12 - 13ed Fin Planning & ForecastingMasterKelly HermanNo ratings yet

- Questions On Net Profit Before Tax and Extraordinary ItemsDocument3 pagesQuestions On Net Profit Before Tax and Extraordinary ItemspuxvashuklaNo ratings yet

- ACT 1600 Fundamental of Financial Accounting The Basic Accounting EquationDocument34 pagesACT 1600 Fundamental of Financial Accounting The Basic Accounting EquationAbu AhmedNo ratings yet

- Introduction To Financial Management: GROUP PROJECT: Ratio Analysis ofDocument34 pagesIntroduction To Financial Management: GROUP PROJECT: Ratio Analysis ofJahida Akter LovnaNo ratings yet

- Corporate Finance Group Assigment - Case Study 2Document24 pagesCorporate Finance Group Assigment - Case Study 2PK LNo ratings yet

- CH 13 Capital Budgeting DecisionsDocument9 pagesCH 13 Capital Budgeting DecisionsChesley MoralesNo ratings yet

- 2 Inventory Cost Flow Intermediate Accounting ReviewerDocument3 pages2 Inventory Cost Flow Intermediate Accounting ReviewerDalia ElarabyNo ratings yet

- PDF Financial Management Theory and Practice 10Th 10Th Edition Prasanna Chandra Ebook Full ChapterDocument53 pagesPDF Financial Management Theory and Practice 10Th 10Th Edition Prasanna Chandra Ebook Full Chaptervalerie.pittman785100% (3)

- ATC Case SolutionDocument3 pagesATC Case SolutionAbiNo ratings yet

- 9419 - Joint ArrangementDocument4 pages9419 - Joint Arrangementjsmozol3434qcNo ratings yet

- Unilever P&G Unilever P&G Assets: Add A Footer 1Document4 pagesUnilever P&G Unilever P&G Assets: Add A Footer 1Kathreen Aya ExcondeNo ratings yet

- Strat Final RequirementDocument6 pagesStrat Final RequirementMJ Navida RiveraNo ratings yet

- Basic Accounting ReviewerDocument35 pagesBasic Accounting ReviewerJhane MarieNo ratings yet

- Chapter-15-Earnings Per ShareDocument85 pagesChapter-15-Earnings Per Shareellyzamae quiraoNo ratings yet

- Adv. Fin. Acct Test-2Document4 pagesAdv. Fin. Acct Test-2Samuel DebebeNo ratings yet

- Balance Sheet - ConsolidatedDocument239 pagesBalance Sheet - ConsolidatedBhagwan BachaiNo ratings yet

- Partnership Formation and OperationDocument41 pagesPartnership Formation and OperationJay Ann DomeNo ratings yet

- Assignment 1Document14 pagesAssignment 1azimlitamellaNo ratings yet

Download as docx, pdf, or txt

You might also like

- AQA A Level Business Topic 3.5 Unit AssessmentDocument4 pagesAQA A Level Business Topic 3.5 Unit AssessmentGeorge Butler67% (3)

- Sample Audited Financial Statements For Sole Proprietorship PDFDocument16 pagesSample Audited Financial Statements For Sole Proprietorship PDFKristen100% (3)

- Walmart Valuation ModelDocument179 pagesWalmart Valuation ModelHiếu Nguyễn Minh HoàngNo ratings yet

- Diageo Case Write UpDocument10 pagesDiageo Case Write UpAmandeep AroraNo ratings yet

- Word Note California Pizza KitchenDocument7 pagesWord Note California Pizza Kitchenalka murarka100% (16)

- Assess Boston Chicken's Business Strategy by Identifying Its Critical Success FactorsDocument4 pagesAssess Boston Chicken's Business Strategy by Identifying Its Critical Success FactorsArindam PalNo ratings yet

- Investment Thesis PDFDocument1 pageInvestment Thesis PDFchatuuuu123No ratings yet

- Boston ChickenDocument4 pagesBoston ChickenSaurabh SinghalNo ratings yet

- Horniman HorticultureDocument11 pagesHorniman Horticultureangela4620100% (2)

- Finmar Quiz 4Document10 pagesFinmar Quiz 4Roderica RegorisNo ratings yet

- California Kitchen Case StudyDocument9 pagesCalifornia Kitchen Case StudyBYQNo ratings yet

- How To Start A Pizza Business: A Complete Pizza Parlor & Pizza Delivery Business PlanFrom EverandHow To Start A Pizza Business: A Complete Pizza Parlor & Pizza Delivery Business PlanNo ratings yet

- 2fa3 Group Project 1Document15 pages2fa3 Group Project 1api-588408469No ratings yet

- End To End Predictive Analysis On ZomatoDocument21 pagesEnd To End Predictive Analysis On ZomatoAmit SinghNo ratings yet

- 01.1 - Small Business - 090121Document10 pages01.1 - Small Business - 090121Xcill EnzeNo ratings yet

- PolarSports Solution PDFDocument8 pagesPolarSports Solution PDFaotorres99No ratings yet

- T 8Document3 pagesT 8Hamayoon AhmedNo ratings yet

- Security Industry Analysis Report Final DraftDocument17 pagesSecurity Industry Analysis Report Final Draftapi-663792863No ratings yet

- Forecast of Balance Sheet 2.1 Assets Cash and Cash EquivalentDocument4 pagesForecast of Balance Sheet 2.1 Assets Cash and Cash EquivalentQuyên HoàngNo ratings yet

- AssumptionsDocument4 pagesAssumptionsNIMESH BHATTNo ratings yet

- O.M. Scott & SonsDocument7 pagesO.M. Scott & Sonsstig2lufetNo ratings yet

- Case SolutionDocument9 pagesCase Solutiontiko100% (1)

- California Pizza KitchenDocument3 pagesCalifornia Pizza KitchenTommy HaleyNo ratings yet

- American Apparel. Drowning in Debt?Document7 pagesAmerican Apparel. Drowning in Debt?Ojas GuptaNo ratings yet

- FAUE InterpretationDocument4 pagesFAUE InterpretationAnkit PatidarNo ratings yet

- Ratio Analysis: Mari Perolum Company LimitiedDocument5 pagesRatio Analysis: Mari Perolum Company LimitiedNuman AhmedNo ratings yet

- Boston ChickenDocument10 pagesBoston ChickenRoptaNo ratings yet

- Dominos ReportDocument20 pagesDominos ReportDisha HalderNo ratings yet

- Dominos ReportDocument20 pagesDominos Reportkuntaljariwala100% (1)

- Assignment-2 (New) PDFDocument12 pagesAssignment-2 (New) PDFminnie908No ratings yet

- 2024 04 24 Chipotle Announces First Quarter 2024 ResultsDocument8 pages2024 04 24 Chipotle Announces First Quarter 2024 Resultsanujdas173No ratings yet

- Zomato Limited ( Zomato' or Company') - IPO Valuation: "Scaling-Up Challenge"Document7 pagesZomato Limited ( Zomato' or Company') - IPO Valuation: "Scaling-Up Challenge"Rajesh KumarNo ratings yet

- Lloyds Banking Group PLC - Q1 2019 Interim Management Statement - TranscriptDocument14 pagesLloyds Banking Group PLC - Q1 2019 Interim Management Statement - TranscriptsaxobobNo ratings yet

- Ar&Inventory ManagementDocument10 pagesAr&Inventory ManagementKarlo D. ReclaNo ratings yet

- Summery of California Pizza Kitchen CaseDocument1 pageSummery of California Pizza Kitchen CaseAbid Ullah67% (3)

- Ar ManagementDocument6 pagesAr ManagementKarlo D. ReclaNo ratings yet

- 1 Https://indianceo - In/business/buzz-Zomato-ValuationDocument3 pages1 Https://indianceo - In/business/buzz-Zomato-ValuationAnkit JaiNo ratings yet

- Financial Management Test BankDocument2 pagesFinancial Management Test BankRenalyn SanchezNo ratings yet

- Zomato IPO DRHP Takeaways JST InvestmentsDocument21 pagesZomato IPO DRHP Takeaways JST InvestmentsJoel MenezesNo ratings yet

- DENN Jan 2016 Investor PresentationDocument30 pagesDENN Jan 2016 Investor PresentationAla BasterNo ratings yet

- Capital Structure and Leverage Quiz # 3Document4 pagesCapital Structure and Leverage Quiz # 3Maurice Hanellete EspirituNo ratings yet

- Edited Transcript: Thomson Reuters StreeteventsDocument17 pagesEdited Transcript: Thomson Reuters Streeteventspe_canNo ratings yet

- Final ReportDocument46 pagesFinal ReportAndrew GilmanNo ratings yet

- California Pizza Kitchen - AnalysisDocument6 pagesCalifornia Pizza Kitchen - AnalysisVasili RabshtynaNo ratings yet

- Integrated Case 3-20Document5 pagesIntegrated Case 3-20Cayden BrookeNo ratings yet

- FIN 302 Notes 1Document55 pagesFIN 302 Notes 1Tekego TlakaleNo ratings yet

- Assignment BBA 2004Document19 pagesAssignment BBA 2004ChaiNo ratings yet

- Alphacom - Maha Tayyab TestDocument8 pagesAlphacom - Maha Tayyab TestMaha TayyabNo ratings yet

- Q3FY24 Shareholders' Letter and ResultsDocument21 pagesQ3FY24 Shareholders' Letter and ResultsDhaval 181No ratings yet

- Financing NetflixDocument16 pagesFinancing Netflix10oandreaNo ratings yet

- Brief IntroductionDocument4 pagesBrief Introductionc.trang99No ratings yet

- 00-Text-Ch3 Additional Problems UpdatedDocument6 pages00-Text-Ch3 Additional Problems Updatedzombies_meNo ratings yet

- Case: Debt Policy at UST Inc. - Protagonist: Vincent GiererDocument2 pagesCase: Debt Policy at UST Inc. - Protagonist: Vincent GiererSu_NeilNo ratings yet

- Aud TheoDocument2 pagesAud Theonivea gumayagayNo ratings yet

- HDFC Standard Life Insurance Company Limited: Six Months Ended September 2010Document22 pagesHDFC Standard Life Insurance Company Limited: Six Months Ended September 2010Dilip RajNo ratings yet

- Name: - Date: - QuizDocument4 pagesName: - Date: - QuizKatrine Clarisse BlanquiscoNo ratings yet

- Fit Co. InterpretationDocument3 pagesFit Co. InterpretationAbishek GuptaNo ratings yet

- A Complete Pizza Restaurant Business Plan: A Key Part Of How To Start A Pizza Parlor & Delivery BusinessFrom EverandA Complete Pizza Restaurant Business Plan: A Key Part Of How To Start A Pizza Parlor & Delivery BusinessRating: 5 out of 5 stars5/5 (1)

- How To Start A Payroll & Bookkeeping Service: A Complete Payroll & Bookkeeping Service Business PlanFrom EverandHow To Start A Payroll & Bookkeeping Service: A Complete Payroll & Bookkeeping Service Business PlanNo ratings yet

- A Complete Payroll & Bookkeeping Service Business Plan: A Key Part Of How To Start A Payroll & BookkeepingFrom EverandA Complete Payroll & Bookkeeping Service Business Plan: A Key Part Of How To Start A Payroll & BookkeepingNo ratings yet

- Guide to Japan-Born Inventory and Accounts Receivable Freshness Control for Managers 2017 (English Version)From EverandGuide to Japan-Born Inventory and Accounts Receivable Freshness Control for Managers 2017 (English Version)No ratings yet

- Seven Components of Strategic Staffing Workforce Planning DescriptionDocument6 pagesSeven Components of Strategic Staffing Workforce Planning DescriptionHiếu Nguyễn Minh HoàngNo ratings yet

- HR QuestionsDocument2 pagesHR QuestionsHiếu Nguyễn Minh HoàngNo ratings yet

- Name: Hieu Nguyen FIN 516: Managerial Macroeconomic Prof. Jessica RutledgeDocument10 pagesName: Hieu Nguyen FIN 516: Managerial Macroeconomic Prof. Jessica RutledgeHiếu Nguyễn Minh HoàngNo ratings yet

- Market Risk PremiumDocument1 pageMarket Risk PremiumHiếu Nguyễn Minh HoàngNo ratings yet

- HieuNguyen - ACTG 560 - Written Analysis 2Document1 pageHieuNguyen - ACTG 560 - Written Analysis 2Hiếu Nguyễn Minh HoàngNo ratings yet

- Prepare Standard and Customized Investment Performance Reports Communicate With Internal and External Clients Collect, Input, Analyze, and Reconcile Data Market ResearchDocument2 pagesPrepare Standard and Customized Investment Performance Reports Communicate With Internal and External Clients Collect, Input, Analyze, and Reconcile Data Market ResearchHiếu Nguyễn Minh HoàngNo ratings yet

- MGMT 471 Final Paper RubricDocument3 pagesMGMT 471 Final Paper RubricHiếu Nguyễn Minh HoàngNo ratings yet

- ACGT Term PaperDocument11 pagesACGT Term PaperHiếu Nguyễn Minh HoàngNo ratings yet

- Hieu Nguyen Cutting Through The Fog-Case OverviewDocument2 pagesHieu Nguyen Cutting Through The Fog-Case OverviewHiếu Nguyễn Minh HoàngNo ratings yet

- Total Factors Supplyings Reserve Funds: Securities Held OutrightDocument3 pagesTotal Factors Supplyings Reserve Funds: Securities Held OutrightHiếu Nguyễn Minh HoàngNo ratings yet

- Walgreens Boots Alliance, Inc. and Subsidiaries: Capitalize STMT of Op Lease ReclassDocument7 pagesWalgreens Boots Alliance, Inc. and Subsidiaries: Capitalize STMT of Op Lease ReclassHiếu Nguyễn Minh HoàngNo ratings yet

- MidtermDocument8 pagesMidtermHiếu Nguyễn Minh HoàngNo ratings yet

- Final Exam PreparationDocument4 pagesFinal Exam PreparationHiếu Nguyễn Minh HoàngNo ratings yet

- FIN 456 International Financial Management: The Market For Foreign ExchangeDocument35 pagesFIN 456 International Financial Management: The Market For Foreign ExchangeHiếu Nguyễn Minh HoàngNo ratings yet

- PSU Code of Student Conduct: School of Business Honors Program - Student Behavior ExpectationsDocument2 pagesPSU Code of Student Conduct: School of Business Honors Program - Student Behavior ExpectationsHiếu Nguyễn Minh HoàngNo ratings yet

- Additional Instructions For Mailing Your Package: Drop Off LocatorDocument1 pageAdditional Instructions For Mailing Your Package: Drop Off LocatorHiếu Nguyễn Minh HoàngNo ratings yet

- Ms Finance EssayDocument1 pageMs Finance EssayHiếu Nguyễn Minh HoàngNo ratings yet

- Chapter 5: Option Pricing Models: The Black-Scholes-Merton ModelDocument47 pagesChapter 5: Option Pricing Models: The Black-Scholes-Merton ModelHiếu Nguyễn Minh HoàngNo ratings yet

- Odel Canvas: Key Partners Key Activities Value Proposition Customer Relationships Customer SegmentsDocument2 pagesOdel Canvas: Key Partners Key Activities Value Proposition Customer Relationships Customer SegmentsHiếu Nguyễn Minh HoàngNo ratings yet

- Investment Banking Valuation Leveraged Buyouts and Mergers and Acquisitions 2Nd Edition Rosenbaum Test Bank Full Chapter PDFDocument43 pagesInvestment Banking Valuation Leveraged Buyouts and Mergers and Acquisitions 2Nd Edition Rosenbaum Test Bank Full Chapter PDFWilliamCartersafg100% (14)

- Philippine Postal Corporation Notes To Financial Statements 1. Agency ProfileDocument15 pagesPhilippine Postal Corporation Notes To Financial Statements 1. Agency ProfileJD BallosNo ratings yet

- LedgerDocument3 pagesLedgerAnonnNo ratings yet

- FS Preparation and Correcting A TBDocument11 pagesFS Preparation and Correcting A TBJulia Mae AlbanoNo ratings yet

- Npo NotesDocument12 pagesNpo Notesmukeshadm123No ratings yet

- Financial Management R. KitDocument241 pagesFinancial Management R. KitDamaris100% (1)

- FFS - NumericalsDocument5 pagesFFS - NumericalsFunny ManNo ratings yet

- Financial Analysis of Everest BankDocument27 pagesFinancial Analysis of Everest BankRazel TercinoNo ratings yet

- GR 12 Accounting P2 Eng - x5Document12 pagesGR 12 Accounting P2 Eng - x5lnaidoo2006No ratings yet

- Acca Supplementary NotesDocument185 pagesAcca Supplementary NotesSuniel JamilNo ratings yet

- Specific Project WorkDocument70 pagesSpecific Project Workajay meenaNo ratings yet

- Ch.12 - 13ed Fin Planning & ForecastingMasterDocument47 pagesCh.12 - 13ed Fin Planning & ForecastingMasterKelly HermanNo ratings yet

- Questions On Net Profit Before Tax and Extraordinary ItemsDocument3 pagesQuestions On Net Profit Before Tax and Extraordinary ItemspuxvashuklaNo ratings yet

- ACT 1600 Fundamental of Financial Accounting The Basic Accounting EquationDocument34 pagesACT 1600 Fundamental of Financial Accounting The Basic Accounting EquationAbu AhmedNo ratings yet

- Introduction To Financial Management: GROUP PROJECT: Ratio Analysis ofDocument34 pagesIntroduction To Financial Management: GROUP PROJECT: Ratio Analysis ofJahida Akter LovnaNo ratings yet

- Corporate Finance Group Assigment - Case Study 2Document24 pagesCorporate Finance Group Assigment - Case Study 2PK LNo ratings yet

- CH 13 Capital Budgeting DecisionsDocument9 pagesCH 13 Capital Budgeting DecisionsChesley MoralesNo ratings yet

- 2 Inventory Cost Flow Intermediate Accounting ReviewerDocument3 pages2 Inventory Cost Flow Intermediate Accounting ReviewerDalia ElarabyNo ratings yet

- PDF Financial Management Theory and Practice 10Th 10Th Edition Prasanna Chandra Ebook Full ChapterDocument53 pagesPDF Financial Management Theory and Practice 10Th 10Th Edition Prasanna Chandra Ebook Full Chaptervalerie.pittman785100% (3)

- ATC Case SolutionDocument3 pagesATC Case SolutionAbiNo ratings yet

- 9419 - Joint ArrangementDocument4 pages9419 - Joint Arrangementjsmozol3434qcNo ratings yet

- Unilever P&G Unilever P&G Assets: Add A Footer 1Document4 pagesUnilever P&G Unilever P&G Assets: Add A Footer 1Kathreen Aya ExcondeNo ratings yet

- Strat Final RequirementDocument6 pagesStrat Final RequirementMJ Navida RiveraNo ratings yet

- Basic Accounting ReviewerDocument35 pagesBasic Accounting ReviewerJhane MarieNo ratings yet

- Chapter-15-Earnings Per ShareDocument85 pagesChapter-15-Earnings Per Shareellyzamae quiraoNo ratings yet

- Adv. Fin. Acct Test-2Document4 pagesAdv. Fin. Acct Test-2Samuel DebebeNo ratings yet

- Balance Sheet - ConsolidatedDocument239 pagesBalance Sheet - ConsolidatedBhagwan BachaiNo ratings yet

- Partnership Formation and OperationDocument41 pagesPartnership Formation and OperationJay Ann DomeNo ratings yet

- Assignment 1Document14 pagesAssignment 1azimlitamellaNo ratings yet