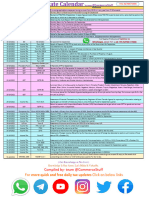

Tax Filing And/or Payment Guide During The Quarantine

Tax Filing And/or Payment Guide During The Quarantine

You might also like

- Guzman Cruz Cpas and Co.: Guideline For BIR Tax Deadlines During Enhanced Community Quarantine (ECQ) PeriodDocument2 pagesGuzman Cruz Cpas and Co.: Guideline For BIR Tax Deadlines During Enhanced Community Quarantine (ECQ) PeriodGerald SantosNo ratings yet

- Evolution of Braking SystemDocument3 pagesEvolution of Braking SystemRaghav NanyaNo ratings yet

- Supplement CAB 2020 002B 1Document8 pagesSupplement CAB 2020 002B 1Bella San JuanNo ratings yet

- Matrix of Deadlines Extended Due To COVID-19 Situation: Revenue Memorandum Circular (RMC) No. 27-2020Document14 pagesMatrix of Deadlines Extended Due To COVID-19 Situation: Revenue Memorandum Circular (RMC) No. 27-2020Brevin PerezNo ratings yet

- 1 STP Q E, 0: MemorandumDocument1 page1 STP Q E, 0: MemorandumQuinciano MorilloNo ratings yet

- Auditor LichflDocument11 pagesAuditor LichflPRABU ASHOKNo ratings yet

- COVID 19 and Its Tax Implications 20200508 - v1.0Document108 pagesCOVID 19 and Its Tax Implications 20200508 - v1.0Richard CaneteNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Santosh IyerNo ratings yet

- Bir Form Name of Form Period Type of Transaction/ Document Original Due DateDocument14 pagesBir Form Name of Form Period Type of Transaction/ Document Original Due DateClea C. LagcoNo ratings yet

- Extension of Deadlines Based On RR 11-2020 (For EBIR Users) : BIR Form Particular Period Extended DeadlineDocument2 pagesExtension of Deadlines Based On RR 11-2020 (For EBIR Users) : BIR Form Particular Period Extended DeadlineFelix Eraño Pakinggan UyNo ratings yet

- Jan 2022 Bir Tax CalendarDocument1 pageJan 2022 Bir Tax Calendarmypinoy taxNo ratings yet

- PWC News Alert 6 April 2020 Cbic Issues Notifications and Circulars To ImplementDocument3 pagesPWC News Alert 6 April 2020 Cbic Issues Notifications and Circulars To ImplementsunshineNo ratings yet

- Compliance Calendar 2020-2021: Due Dates - After Covid-19Document21 pagesCompliance Calendar 2020-2021: Due Dates - After Covid-19ABC 123No ratings yet

- Compliance Calendar For June 2020Document8 pagesCompliance Calendar For June 2020corporate partnersNo ratings yet

- IC and SEC Reportorial RequirementsDocument8 pagesIC and SEC Reportorial RequirementsSanta NinaNo ratings yet

- Khumani Final Rehab Plan 2020 FINAL For Submission CombinedDocument219 pagesKhumani Final Rehab Plan 2020 FINAL For Submission Combinedbryon6281No ratings yet

- Due Date After Covid19Document20 pagesDue Date After Covid19sandjkNo ratings yet

- Various Due DatesDocument21 pagesVarious Due DatesCA AravindNo ratings yet

- Rush of Expenditure in The Last Quarter of Financial Year 2019-20 - Central Government Employees NewsDocument2 pagesRush of Expenditure in The Last Quarter of Financial Year 2019-20 - Central Government Employees NewsbimlapalNo ratings yet

- Feb 2022-Bir-Tax-CalendarDocument1 pageFeb 2022-Bir-Tax-Calendarmypinoy taxNo ratings yet

- Tax Code and Period CodeDocument1 pageTax Code and Period CodeThiruNo ratings yet

- Aino Communique PDFDocument14 pagesAino Communique PDFSwathi JainNo ratings yet

- Letter and Shareholder - MCA Affidavit - FinancialsDocument2 pagesLetter and Shareholder - MCA Affidavit - Financialsskarshad007.saNo ratings yet

- Due Date Calendar June 22Document1 pageDue Date Calendar June 22HAKIMI MZNNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961ghss chinniNo ratings yet

- (2021 Tax Memo) Year-End Tax Compliance RemindersDocument2 pages(2021 Tax Memo) Year-End Tax Compliance RemindersMary Joy BautistaNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Ashutosh SinhaNo ratings yet

- Bank Payment VoucherDocument4 pagesBank Payment Voucherhrkhan390No ratings yet

- 1 MondayDocument6 pages1 MondayCeline Marie Libatique AntonioNo ratings yet

- Statement of Account / Tax Invoice: Hammad KhanDocument1 pageStatement of Account / Tax Invoice: Hammad Khanhammad78No ratings yet

- RR-No. 7-2020Document27 pagesRR-No. 7-2020April CaringalNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Xen Operation DPHNo ratings yet

- TaXavvy-Movement Control Order PDFDocument6 pagesTaXavvy-Movement Control Order PDFBritish Malaysian Chamber of CommerceNo ratings yet

- Mar 2022 Bir Tax CalendarDocument1 pageMar 2022 Bir Tax Calendarmypinoy taxNo ratings yet

- TRAIN Law - Taxation of Self-Employed IndividualsDocument8 pagesTRAIN Law - Taxation of Self-Employed IndividualsCora EleazarNo ratings yet

- Transactions by Account: Tipco Estates CorporationDocument3 pagesTransactions by Account: Tipco Estates CorporationJa'maine ManguerraNo ratings yet

- Highlights of Relief Measures & Other Amendments Under GST: ASC Legal, Solicitors and Advocates April 2020Document4 pagesHighlights of Relief Measures & Other Amendments Under GST: ASC Legal, Solicitors and Advocates April 2020Pulkit AgarwalNo ratings yet

- X Compliance MergedDocument46 pagesX Compliance MergedAnnah Caponpon GalorNo ratings yet

- Aaefk7065p 2020Document18 pagesAaefk7065p 2020Vineet KhuranaNo ratings yet

- GO Salary Related HOADocument2 pagesGO Salary Related HOALiving LifeNo ratings yet

- Company Tax Return (CT600)Document28 pagesCompany Tax Return (CT600)Maria HeaveyNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Ahamed UmarNo ratings yet

- Due Date Calendar Oct 22Document1 pageDue Date Calendar Oct 22Kushal DabhadkarNo ratings yet

- GST Portaloct 31, 2020Document2 pagesGST Portaloct 31, 2020Ajay KumarNo ratings yet

- GST Times - Vol.1, Issue-3Document22 pagesGST Times - Vol.1, Issue-3Milna JosephNo ratings yet

- Summary of TotalsDocument1 pageSummary of Totalsrene nonatoNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Daman SharmaNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Madhukar GuptaNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Kapil KaroliyaNo ratings yet

- Accounting 2020 P1 Info BookDocument9 pagesAccounting 2020 P1 Info BookodiantumbaNo ratings yet

- Middletown Budget 2020Document73 pagesMiddletown Budget 2020Asbury Park PressNo ratings yet

- Ekxps0001n 2021Document4 pagesEkxps0001n 2021SiddharthNo ratings yet

- Atlpr9507m 2021Document4 pagesAtlpr9507m 2021chandra DiveshNo ratings yet

- Annual Information Statement (AIS) : BNNPM9483N XXXX XXX X 86 93 Mohd Arshad Mohd Aslam QureshiDocument2 pagesAnnual Information Statement (AIS) : BNNPM9483N XXXX XXX X 86 93 Mohd Arshad Mohd Aslam QureshiKamalalakshmi NarayananNo ratings yet

- Aino Communique 100th Edition - Feb 2022 PDFDocument22 pagesAino Communique 100th Edition - Feb 2022 PDFSwathi JainNo ratings yet

- SEC MC 17 AFS DeadlinesDocument3 pagesSEC MC 17 AFS DeadlinesjvpvillanuevaNo ratings yet

- Psa PDFDocument32 pagesPsa PDFBingNo ratings yet

- Ramesh GPFDocument2 pagesRamesh GPFSHARANUNo ratings yet

- Itr Deadline Extended ITR Filing, Tax Audit Report Deadlines For FY 2020-21 Extended by CBDT - The Economic TimesDocument1 pageItr Deadline Extended ITR Filing, Tax Audit Report Deadlines For FY 2020-21 Extended by CBDT - The Economic TimesVittal TalwarNo ratings yet

- A New Dawn for Global Value Chain Participation in the PhilippinesFrom EverandA New Dawn for Global Value Chain Participation in the PhilippinesNo ratings yet

- Overcoming COVID-19 in Bhutan: Lessons from Coping with the Pandemic in a Tourism-Dependent EconomyFrom EverandOvercoming COVID-19 in Bhutan: Lessons from Coping with the Pandemic in a Tourism-Dependent EconomyNo ratings yet

- DDDDDDDDDDDDDDDDDDocument28 pagesDDDDDDDDDDDDDDDDDMaria Rose Giltendez - BartianaNo ratings yet

- Steel Beam Using GearDocument2 pagesSteel Beam Using GearMaria Rose Giltendez - BartianaNo ratings yet

- Beam Design Using GearDocument3 pagesBeam Design Using GearMaria Rose Giltendez - BartianaNo ratings yet

- Choanal Polyp Originating From The Nasal Septum: Septochoanal PolypDocument4 pagesChoanal Polyp Originating From The Nasal Septum: Septochoanal PolypMaria Rose Giltendez - BartianaNo ratings yet

- Combined Footing Using GearDocument3 pagesCombined Footing Using GearMaria Rose Giltendez - BartianaNo ratings yet

- Two Way Slab Using GearDocument2 pagesTwo Way Slab Using GearMaria Rose Giltendez - BartianaNo ratings yet

- Quota 4Document13 pagesQuota 4Maria Rose Giltendez - BartianaNo ratings yet

- GRASP - Graphical Rapid Analysis of Structures Program Version 1.17 Licenced To: PRMDPDocument1 pageGRASP - Graphical Rapid Analysis of Structures Program Version 1.17 Licenced To: PRMDPMaria Rose Giltendez - BartianaNo ratings yet

- Using Long Span Color RoofDocument3 pagesUsing Long Span Color RoofMaria Rose Giltendez - BartianaNo ratings yet

- My Final Lesson PlanDocument4 pagesMy Final Lesson PlanMaria Rose Giltendez - BartianaNo ratings yet

- Names Should Be in Alphabetical Order: Guttierez, Richard F. Coach Quinto Ruffa Mae ChaperonDocument3 pagesNames Should Be in Alphabetical Order: Guttierez, Richard F. Coach Quinto Ruffa Mae ChaperonMaria Rose Giltendez - BartianaNo ratings yet

- GearDocument1 pageGearMaria Rose Giltendez - BartianaNo ratings yet

- Certificate-For The Top Pupils... JGBDocument2 pagesCertificate-For The Top Pupils... JGBMaria Rose Giltendez - BartianaNo ratings yet

- CARPENTRYDocument6 pagesCARPENTRYMaria Rose Giltendez - BartianaNo ratings yet

- MORGA, Maria Bianca S. CE522-M01 Iii. Masonry: 4sp 2 1sp SQ QC 2Document8 pagesMORGA, Maria Bianca S. CE522-M01 Iii. Masonry: 4sp 2 1sp SQ QC 2Maria Rose Giltendez - BartianaNo ratings yet

- L Spacing: 8 M 0.30 M 12 4 M 27 3 Cuts Per LengthDocument4 pagesL Spacing: 8 M 0.30 M 12 4 M 27 3 Cuts Per LengthMaria Rose Giltendez - BartianaNo ratings yet

- CPM 1Document160 pagesCPM 1Maria Rose Giltendez - BartianaNo ratings yet

- Viiii. Doors and Windows: A. Material CostDocument1 pageViiii. Doors and Windows: A. Material CostMaria Rose Giltendez - BartianaNo ratings yet

- Design and Analysis of Isolated Footings: Project InformationDocument2 pagesDesign and Analysis of Isolated Footings: Project InformationMaria Rose Giltendez - BartianaNo ratings yet

- 761.60 SQ .M - 25.0 SQ - M - Per Gallon: MORGA, Maria Bianca S. CE522-M01 V. FinishesDocument4 pages761.60 SQ .M - 25.0 SQ - M - Per Gallon: MORGA, Maria Bianca S. CE522-M01 V. FinishesMaria Rose Giltendez - BartianaNo ratings yet

- Design and Analysis of Isolated Footings: Project InformationDocument2 pagesDesign and Analysis of Isolated Footings: Project InformationMaria Rose Giltendez - BartianaNo ratings yet

- Vi. Roofing: Total Roof Area Effective WidthDocument3 pagesVi. Roofing: Total Roof Area Effective WidthMaria Rose Giltendez - BartianaNo ratings yet

- Design and Analysis of Isolated Footings: Project InformationDocument2 pagesDesign and Analysis of Isolated Footings: Project InformationMaria Rose Giltendez - BartianaNo ratings yet

- Project Information:: ACECOMS GEAR: RC Column Section Design Version: 3.0 (Rev. 1)Document3 pagesProject Information:: ACECOMS GEAR: RC Column Section Design Version: 3.0 (Rev. 1)Maria Rose Giltendez - BartianaNo ratings yet

- Frame 1X: GRASP Version 1.21 Licenced To: Cebu Institute of TechnologyDocument1 pageFrame 1X: GRASP Version 1.21 Licenced To: Cebu Institute of TechnologyMaria Rose Giltendez - BartianaNo ratings yet

- I. Earthworks:: A. ExcavationDocument10 pagesI. Earthworks:: A. ExcavationMaria Rose Giltendez - BartianaNo ratings yet

- Maria Bianca S. Morga CE 522-M01 I. Earthworks: 0.50+0.74 2 X 12m X 0.50mDocument8 pagesMaria Bianca S. Morga CE 522-M01 I. Earthworks: 0.50+0.74 2 X 12m X 0.50mMaria Rose Giltendez - BartianaNo ratings yet

- Urban PlanBrochure Parkview 253 NEW PDFDocument2 pagesUrban PlanBrochure Parkview 253 NEW PDFMaria Rose Giltendez - BartianaNo ratings yet

- Clearfrac Co2 SchlumbergerDocument2 pagesClearfrac Co2 SchlumbergerSohaibSeidNo ratings yet

- An Introduction To T-TestsDocument5 pagesAn Introduction To T-Testsbernadith tolinginNo ratings yet

- Taxonomy of Driving Automation: Module 1, Lesson 1Document26 pagesTaxonomy of Driving Automation: Module 1, Lesson 1Nikita ShakyaNo ratings yet

- Skill 103 Administering A Large-Volume Cleansing EnemaDocument3 pagesSkill 103 Administering A Large-Volume Cleansing EnemaHarley Justiniani Dela CruzNo ratings yet

- StatisticsDocument116 pagesStatisticsRAIZA GRACE OAMILNo ratings yet

- Cinema Italiano PDFDocument327 pagesCinema Italiano PDFArch HallNo ratings yet

- Maths For PracticeDocument129 pagesMaths For PracticeSaeed KhanNo ratings yet

- Research Capsule - FINALDocument3 pagesResearch Capsule - FINALAndrew FernandezNo ratings yet

- Culvert Pipe Liner Guide July2005Document169 pagesCulvert Pipe Liner Guide July2005Anonymous MklNL77No ratings yet

- Rubber Band Thermo EssayDocument2 pagesRubber Band Thermo Essayapi-249615264No ratings yet

- Presentación Luca MeiniDocument31 pagesPresentación Luca MeiniSebastian Ariel ObrequeNo ratings yet

- Clinical ListingDocument21 pagesClinical ListingBassem AhmedNo ratings yet

- Towards Learning 3d Object Detection and 6d Pose Estimation From Synthetic DataDocument4 pagesTowards Learning 3d Object Detection and 6d Pose Estimation From Synthetic Dataraxx666No ratings yet

- An Improved Method of Matching Response Spectra of Recorded Earthquake Ground Motion Using WaveletsDocument23 pagesAn Improved Method of Matching Response Spectra of Recorded Earthquake Ground Motion Using WaveletszerlopezNo ratings yet

- Indian Steel Ministry - Steel Scrap PolicyDocument14 pagesIndian Steel Ministry - Steel Scrap PolicySameer DhumaleNo ratings yet

- An Impedance-Matching Technique For Increasing The Bandwidth of Microstrip AntennasDocument10 pagesAn Impedance-Matching Technique For Increasing The Bandwidth of Microstrip Antennasverdun6No ratings yet

- Device Comment 12/6/2021 Data Name: COMMENTDocument17 pagesDevice Comment 12/6/2021 Data Name: COMMENTRio WicakNo ratings yet

- Department of Social Welfare Services: Republic of The Philippines City of CebuDocument2 pagesDepartment of Social Welfare Services: Republic of The Philippines City of CebuadoptifyNo ratings yet

- Updated Manual 1 To 18Document53 pagesUpdated Manual 1 To 18mybestfriendgrewalNo ratings yet

- Spandan HR ManualDocument46 pagesSpandan HR ManualBotanic Hair Oil100% (1)

- Kipor KDE Silent GeneratorDocument4 pagesKipor KDE Silent GeneratorbacNo ratings yet

- API 579 SI Handouts PDFDocument196 pagesAPI 579 SI Handouts PDFshakeelahmadjsr100% (1)

- Bai DaynDocument5 pagesBai DaynSiti AsyiqinNo ratings yet

- Iso 9001Document17 pagesIso 9001Paula . EsNo ratings yet

- IAL New Syllabus and Old Syllabus Exam Sitiing Centre-comms-ial-2018-Transition-february-2018-UpdateDocument6 pagesIAL New Syllabus and Old Syllabus Exam Sitiing Centre-comms-ial-2018-Transition-february-2018-UpdateAbhiKhanNo ratings yet

- 08cDocument78 pages08cDan FarrisNo ratings yet

- GEE 2 Cover Page and PreliminariesDocument6 pagesGEE 2 Cover Page and PreliminariesVio Mae CastillanoNo ratings yet

- OOP SE-203: Submitted By: - ANUJ 2K20/SE/21 - Anurag Munshi 2K20/Se/25Document9 pagesOOP SE-203: Submitted By: - ANUJ 2K20/SE/21 - Anurag Munshi 2K20/Se/25Anurag Munshi 25No ratings yet

- Victron Battery Charger ManualDocument30 pagesVictron Battery Charger ManualJERINsmile100% (1)

Download as pdf or txt

You might also like

- Guzman Cruz Cpas and Co.: Guideline For BIR Tax Deadlines During Enhanced Community Quarantine (ECQ) PeriodDocument2 pagesGuzman Cruz Cpas and Co.: Guideline For BIR Tax Deadlines During Enhanced Community Quarantine (ECQ) PeriodGerald SantosNo ratings yet

- Evolution of Braking SystemDocument3 pagesEvolution of Braking SystemRaghav NanyaNo ratings yet

- Supplement CAB 2020 002B 1Document8 pagesSupplement CAB 2020 002B 1Bella San JuanNo ratings yet

- Matrix of Deadlines Extended Due To COVID-19 Situation: Revenue Memorandum Circular (RMC) No. 27-2020Document14 pagesMatrix of Deadlines Extended Due To COVID-19 Situation: Revenue Memorandum Circular (RMC) No. 27-2020Brevin PerezNo ratings yet

- 1 STP Q E, 0: MemorandumDocument1 page1 STP Q E, 0: MemorandumQuinciano MorilloNo ratings yet

- Auditor LichflDocument11 pagesAuditor LichflPRABU ASHOKNo ratings yet

- COVID 19 and Its Tax Implications 20200508 - v1.0Document108 pagesCOVID 19 and Its Tax Implications 20200508 - v1.0Richard CaneteNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Santosh IyerNo ratings yet

- Bir Form Name of Form Period Type of Transaction/ Document Original Due DateDocument14 pagesBir Form Name of Form Period Type of Transaction/ Document Original Due DateClea C. LagcoNo ratings yet

- Extension of Deadlines Based On RR 11-2020 (For EBIR Users) : BIR Form Particular Period Extended DeadlineDocument2 pagesExtension of Deadlines Based On RR 11-2020 (For EBIR Users) : BIR Form Particular Period Extended DeadlineFelix Eraño Pakinggan UyNo ratings yet

- Jan 2022 Bir Tax CalendarDocument1 pageJan 2022 Bir Tax Calendarmypinoy taxNo ratings yet

- PWC News Alert 6 April 2020 Cbic Issues Notifications and Circulars To ImplementDocument3 pagesPWC News Alert 6 April 2020 Cbic Issues Notifications and Circulars To ImplementsunshineNo ratings yet

- Compliance Calendar 2020-2021: Due Dates - After Covid-19Document21 pagesCompliance Calendar 2020-2021: Due Dates - After Covid-19ABC 123No ratings yet

- Compliance Calendar For June 2020Document8 pagesCompliance Calendar For June 2020corporate partnersNo ratings yet

- IC and SEC Reportorial RequirementsDocument8 pagesIC and SEC Reportorial RequirementsSanta NinaNo ratings yet

- Khumani Final Rehab Plan 2020 FINAL For Submission CombinedDocument219 pagesKhumani Final Rehab Plan 2020 FINAL For Submission Combinedbryon6281No ratings yet

- Due Date After Covid19Document20 pagesDue Date After Covid19sandjkNo ratings yet

- Various Due DatesDocument21 pagesVarious Due DatesCA AravindNo ratings yet

- Rush of Expenditure in The Last Quarter of Financial Year 2019-20 - Central Government Employees NewsDocument2 pagesRush of Expenditure in The Last Quarter of Financial Year 2019-20 - Central Government Employees NewsbimlapalNo ratings yet

- Feb 2022-Bir-Tax-CalendarDocument1 pageFeb 2022-Bir-Tax-Calendarmypinoy taxNo ratings yet

- Tax Code and Period CodeDocument1 pageTax Code and Period CodeThiruNo ratings yet

- Aino Communique PDFDocument14 pagesAino Communique PDFSwathi JainNo ratings yet

- Letter and Shareholder - MCA Affidavit - FinancialsDocument2 pagesLetter and Shareholder - MCA Affidavit - Financialsskarshad007.saNo ratings yet

- Due Date Calendar June 22Document1 pageDue Date Calendar June 22HAKIMI MZNNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961ghss chinniNo ratings yet

- (2021 Tax Memo) Year-End Tax Compliance RemindersDocument2 pages(2021 Tax Memo) Year-End Tax Compliance RemindersMary Joy BautistaNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Ashutosh SinhaNo ratings yet

- Bank Payment VoucherDocument4 pagesBank Payment Voucherhrkhan390No ratings yet

- 1 MondayDocument6 pages1 MondayCeline Marie Libatique AntonioNo ratings yet

- Statement of Account / Tax Invoice: Hammad KhanDocument1 pageStatement of Account / Tax Invoice: Hammad Khanhammad78No ratings yet

- RR-No. 7-2020Document27 pagesRR-No. 7-2020April CaringalNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Xen Operation DPHNo ratings yet

- TaXavvy-Movement Control Order PDFDocument6 pagesTaXavvy-Movement Control Order PDFBritish Malaysian Chamber of CommerceNo ratings yet

- Mar 2022 Bir Tax CalendarDocument1 pageMar 2022 Bir Tax Calendarmypinoy taxNo ratings yet

- TRAIN Law - Taxation of Self-Employed IndividualsDocument8 pagesTRAIN Law - Taxation of Self-Employed IndividualsCora EleazarNo ratings yet

- Transactions by Account: Tipco Estates CorporationDocument3 pagesTransactions by Account: Tipco Estates CorporationJa'maine ManguerraNo ratings yet

- Highlights of Relief Measures & Other Amendments Under GST: ASC Legal, Solicitors and Advocates April 2020Document4 pagesHighlights of Relief Measures & Other Amendments Under GST: ASC Legal, Solicitors and Advocates April 2020Pulkit AgarwalNo ratings yet

- X Compliance MergedDocument46 pagesX Compliance MergedAnnah Caponpon GalorNo ratings yet

- Aaefk7065p 2020Document18 pagesAaefk7065p 2020Vineet KhuranaNo ratings yet

- GO Salary Related HOADocument2 pagesGO Salary Related HOALiving LifeNo ratings yet

- Company Tax Return (CT600)Document28 pagesCompany Tax Return (CT600)Maria HeaveyNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Ahamed UmarNo ratings yet

- Due Date Calendar Oct 22Document1 pageDue Date Calendar Oct 22Kushal DabhadkarNo ratings yet

- GST Portaloct 31, 2020Document2 pagesGST Portaloct 31, 2020Ajay KumarNo ratings yet

- GST Times - Vol.1, Issue-3Document22 pagesGST Times - Vol.1, Issue-3Milna JosephNo ratings yet

- Summary of TotalsDocument1 pageSummary of Totalsrene nonatoNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Daman SharmaNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Madhukar GuptaNo ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Kapil KaroliyaNo ratings yet

- Accounting 2020 P1 Info BookDocument9 pagesAccounting 2020 P1 Info BookodiantumbaNo ratings yet

- Middletown Budget 2020Document73 pagesMiddletown Budget 2020Asbury Park PressNo ratings yet

- Ekxps0001n 2021Document4 pagesEkxps0001n 2021SiddharthNo ratings yet

- Atlpr9507m 2021Document4 pagesAtlpr9507m 2021chandra DiveshNo ratings yet

- Annual Information Statement (AIS) : BNNPM9483N XXXX XXX X 86 93 Mohd Arshad Mohd Aslam QureshiDocument2 pagesAnnual Information Statement (AIS) : BNNPM9483N XXXX XXX X 86 93 Mohd Arshad Mohd Aslam QureshiKamalalakshmi NarayananNo ratings yet

- Aino Communique 100th Edition - Feb 2022 PDFDocument22 pagesAino Communique 100th Edition - Feb 2022 PDFSwathi JainNo ratings yet

- SEC MC 17 AFS DeadlinesDocument3 pagesSEC MC 17 AFS DeadlinesjvpvillanuevaNo ratings yet

- Psa PDFDocument32 pagesPsa PDFBingNo ratings yet

- Ramesh GPFDocument2 pagesRamesh GPFSHARANUNo ratings yet

- Itr Deadline Extended ITR Filing, Tax Audit Report Deadlines For FY 2020-21 Extended by CBDT - The Economic TimesDocument1 pageItr Deadline Extended ITR Filing, Tax Audit Report Deadlines For FY 2020-21 Extended by CBDT - The Economic TimesVittal TalwarNo ratings yet

- A New Dawn for Global Value Chain Participation in the PhilippinesFrom EverandA New Dawn for Global Value Chain Participation in the PhilippinesNo ratings yet

- Overcoming COVID-19 in Bhutan: Lessons from Coping with the Pandemic in a Tourism-Dependent EconomyFrom EverandOvercoming COVID-19 in Bhutan: Lessons from Coping with the Pandemic in a Tourism-Dependent EconomyNo ratings yet

- DDDDDDDDDDDDDDDDDDocument28 pagesDDDDDDDDDDDDDDDDDMaria Rose Giltendez - BartianaNo ratings yet

- Steel Beam Using GearDocument2 pagesSteel Beam Using GearMaria Rose Giltendez - BartianaNo ratings yet

- Beam Design Using GearDocument3 pagesBeam Design Using GearMaria Rose Giltendez - BartianaNo ratings yet

- Choanal Polyp Originating From The Nasal Septum: Septochoanal PolypDocument4 pagesChoanal Polyp Originating From The Nasal Septum: Septochoanal PolypMaria Rose Giltendez - BartianaNo ratings yet

- Combined Footing Using GearDocument3 pagesCombined Footing Using GearMaria Rose Giltendez - BartianaNo ratings yet

- Two Way Slab Using GearDocument2 pagesTwo Way Slab Using GearMaria Rose Giltendez - BartianaNo ratings yet

- Quota 4Document13 pagesQuota 4Maria Rose Giltendez - BartianaNo ratings yet

- GRASP - Graphical Rapid Analysis of Structures Program Version 1.17 Licenced To: PRMDPDocument1 pageGRASP - Graphical Rapid Analysis of Structures Program Version 1.17 Licenced To: PRMDPMaria Rose Giltendez - BartianaNo ratings yet

- Using Long Span Color RoofDocument3 pagesUsing Long Span Color RoofMaria Rose Giltendez - BartianaNo ratings yet

- My Final Lesson PlanDocument4 pagesMy Final Lesson PlanMaria Rose Giltendez - BartianaNo ratings yet

- Names Should Be in Alphabetical Order: Guttierez, Richard F. Coach Quinto Ruffa Mae ChaperonDocument3 pagesNames Should Be in Alphabetical Order: Guttierez, Richard F. Coach Quinto Ruffa Mae ChaperonMaria Rose Giltendez - BartianaNo ratings yet

- GearDocument1 pageGearMaria Rose Giltendez - BartianaNo ratings yet

- Certificate-For The Top Pupils... JGBDocument2 pagesCertificate-For The Top Pupils... JGBMaria Rose Giltendez - BartianaNo ratings yet

- CARPENTRYDocument6 pagesCARPENTRYMaria Rose Giltendez - BartianaNo ratings yet

- MORGA, Maria Bianca S. CE522-M01 Iii. Masonry: 4sp 2 1sp SQ QC 2Document8 pagesMORGA, Maria Bianca S. CE522-M01 Iii. Masonry: 4sp 2 1sp SQ QC 2Maria Rose Giltendez - BartianaNo ratings yet

- L Spacing: 8 M 0.30 M 12 4 M 27 3 Cuts Per LengthDocument4 pagesL Spacing: 8 M 0.30 M 12 4 M 27 3 Cuts Per LengthMaria Rose Giltendez - BartianaNo ratings yet

- CPM 1Document160 pagesCPM 1Maria Rose Giltendez - BartianaNo ratings yet

- Viiii. Doors and Windows: A. Material CostDocument1 pageViiii. Doors and Windows: A. Material CostMaria Rose Giltendez - BartianaNo ratings yet

- Design and Analysis of Isolated Footings: Project InformationDocument2 pagesDesign and Analysis of Isolated Footings: Project InformationMaria Rose Giltendez - BartianaNo ratings yet

- 761.60 SQ .M - 25.0 SQ - M - Per Gallon: MORGA, Maria Bianca S. CE522-M01 V. FinishesDocument4 pages761.60 SQ .M - 25.0 SQ - M - Per Gallon: MORGA, Maria Bianca S. CE522-M01 V. FinishesMaria Rose Giltendez - BartianaNo ratings yet

- Design and Analysis of Isolated Footings: Project InformationDocument2 pagesDesign and Analysis of Isolated Footings: Project InformationMaria Rose Giltendez - BartianaNo ratings yet

- Vi. Roofing: Total Roof Area Effective WidthDocument3 pagesVi. Roofing: Total Roof Area Effective WidthMaria Rose Giltendez - BartianaNo ratings yet

- Design and Analysis of Isolated Footings: Project InformationDocument2 pagesDesign and Analysis of Isolated Footings: Project InformationMaria Rose Giltendez - BartianaNo ratings yet

- Project Information:: ACECOMS GEAR: RC Column Section Design Version: 3.0 (Rev. 1)Document3 pagesProject Information:: ACECOMS GEAR: RC Column Section Design Version: 3.0 (Rev. 1)Maria Rose Giltendez - BartianaNo ratings yet

- Frame 1X: GRASP Version 1.21 Licenced To: Cebu Institute of TechnologyDocument1 pageFrame 1X: GRASP Version 1.21 Licenced To: Cebu Institute of TechnologyMaria Rose Giltendez - BartianaNo ratings yet

- I. Earthworks:: A. ExcavationDocument10 pagesI. Earthworks:: A. ExcavationMaria Rose Giltendez - BartianaNo ratings yet

- Maria Bianca S. Morga CE 522-M01 I. Earthworks: 0.50+0.74 2 X 12m X 0.50mDocument8 pagesMaria Bianca S. Morga CE 522-M01 I. Earthworks: 0.50+0.74 2 X 12m X 0.50mMaria Rose Giltendez - BartianaNo ratings yet

- Urban PlanBrochure Parkview 253 NEW PDFDocument2 pagesUrban PlanBrochure Parkview 253 NEW PDFMaria Rose Giltendez - BartianaNo ratings yet

- Clearfrac Co2 SchlumbergerDocument2 pagesClearfrac Co2 SchlumbergerSohaibSeidNo ratings yet

- An Introduction To T-TestsDocument5 pagesAn Introduction To T-Testsbernadith tolinginNo ratings yet

- Taxonomy of Driving Automation: Module 1, Lesson 1Document26 pagesTaxonomy of Driving Automation: Module 1, Lesson 1Nikita ShakyaNo ratings yet

- Skill 103 Administering A Large-Volume Cleansing EnemaDocument3 pagesSkill 103 Administering A Large-Volume Cleansing EnemaHarley Justiniani Dela CruzNo ratings yet

- StatisticsDocument116 pagesStatisticsRAIZA GRACE OAMILNo ratings yet

- Cinema Italiano PDFDocument327 pagesCinema Italiano PDFArch HallNo ratings yet

- Maths For PracticeDocument129 pagesMaths For PracticeSaeed KhanNo ratings yet

- Research Capsule - FINALDocument3 pagesResearch Capsule - FINALAndrew FernandezNo ratings yet

- Culvert Pipe Liner Guide July2005Document169 pagesCulvert Pipe Liner Guide July2005Anonymous MklNL77No ratings yet

- Rubber Band Thermo EssayDocument2 pagesRubber Band Thermo Essayapi-249615264No ratings yet

- Presentación Luca MeiniDocument31 pagesPresentación Luca MeiniSebastian Ariel ObrequeNo ratings yet

- Clinical ListingDocument21 pagesClinical ListingBassem AhmedNo ratings yet

- Towards Learning 3d Object Detection and 6d Pose Estimation From Synthetic DataDocument4 pagesTowards Learning 3d Object Detection and 6d Pose Estimation From Synthetic Dataraxx666No ratings yet

- An Improved Method of Matching Response Spectra of Recorded Earthquake Ground Motion Using WaveletsDocument23 pagesAn Improved Method of Matching Response Spectra of Recorded Earthquake Ground Motion Using WaveletszerlopezNo ratings yet

- Indian Steel Ministry - Steel Scrap PolicyDocument14 pagesIndian Steel Ministry - Steel Scrap PolicySameer DhumaleNo ratings yet

- An Impedance-Matching Technique For Increasing The Bandwidth of Microstrip AntennasDocument10 pagesAn Impedance-Matching Technique For Increasing The Bandwidth of Microstrip Antennasverdun6No ratings yet

- Device Comment 12/6/2021 Data Name: COMMENTDocument17 pagesDevice Comment 12/6/2021 Data Name: COMMENTRio WicakNo ratings yet

- Department of Social Welfare Services: Republic of The Philippines City of CebuDocument2 pagesDepartment of Social Welfare Services: Republic of The Philippines City of CebuadoptifyNo ratings yet

- Updated Manual 1 To 18Document53 pagesUpdated Manual 1 To 18mybestfriendgrewalNo ratings yet

- Spandan HR ManualDocument46 pagesSpandan HR ManualBotanic Hair Oil100% (1)

- Kipor KDE Silent GeneratorDocument4 pagesKipor KDE Silent GeneratorbacNo ratings yet

- API 579 SI Handouts PDFDocument196 pagesAPI 579 SI Handouts PDFshakeelahmadjsr100% (1)

- Bai DaynDocument5 pagesBai DaynSiti AsyiqinNo ratings yet

- Iso 9001Document17 pagesIso 9001Paula . EsNo ratings yet

- IAL New Syllabus and Old Syllabus Exam Sitiing Centre-comms-ial-2018-Transition-february-2018-UpdateDocument6 pagesIAL New Syllabus and Old Syllabus Exam Sitiing Centre-comms-ial-2018-Transition-february-2018-UpdateAbhiKhanNo ratings yet

- 08cDocument78 pages08cDan FarrisNo ratings yet

- GEE 2 Cover Page and PreliminariesDocument6 pagesGEE 2 Cover Page and PreliminariesVio Mae CastillanoNo ratings yet

- OOP SE-203: Submitted By: - ANUJ 2K20/SE/21 - Anurag Munshi 2K20/Se/25Document9 pagesOOP SE-203: Submitted By: - ANUJ 2K20/SE/21 - Anurag Munshi 2K20/Se/25Anurag Munshi 25No ratings yet

- Victron Battery Charger ManualDocument30 pagesVictron Battery Charger ManualJERINsmile100% (1)