Download as doc, pdf, or txt

You might also like

- Food PandaDocument22 pagesFood PandaShakil56% (9)

- HW 1-SolnDocument8 pagesHW 1-SolnZhaohui ChenNo ratings yet

- 8a. Responsibility and Segment Accounting CRDocument20 pages8a. Responsibility and Segment Accounting CRAngelica Gaspay EstalillaNo ratings yet

- Valle Quiz AbcDocument6 pagesValle Quiz Abclorie anne valle100% (2)

- PEST Analysis On Mutual FundsDocument17 pagesPEST Analysis On Mutual Fundsrishu0075352490% (10)

- Bfc44602 Engineering Economy: Title: Development of A New Private College Worth RM100 MillionDocument64 pagesBfc44602 Engineering Economy: Title: Development of A New Private College Worth RM100 Millionyap chee keongNo ratings yet

- Consolidated FS QuizDocument4 pagesConsolidated FS QuizCattleya0% (2)

- Solutions Manual Financial Statement AnalysisDocument14 pagesSolutions Manual Financial Statement AnalysisLimNo ratings yet

- Answer Jerry Rice and Grain StoresDocument2 pagesAnswer Jerry Rice and Grain StoresJken OrtizNo ratings yet

- Question - FS and FADocument4 pagesQuestion - FS and FAPhương NhungNo ratings yet

- C. Wolken Issued New Common Stock in 2013Document4 pagesC. Wolken Issued New Common Stock in 2013Talha JavedNo ratings yet

- Final RequirementDocument18 pagesFinal RequirementZandra GonzalesNo ratings yet

- 317 Midterm 1 Practice Exam SolutionsDocument9 pages317 Midterm 1 Practice Exam Solutionskinyuadavid000No ratings yet

- Answer Key ABM2Document6 pagesAnswer Key ABM2Elle Alorra RubenfieldNo ratings yet

- Chapter 3Document73 pagesChapter 3Mark Arceo50% (2)

- BKM 10e Chap014Document8 pagesBKM 10e Chap014jl123123No ratings yet

- Practice Questions AFS1Document12 pagesPractice Questions AFS1yasirNo ratings yet

- PracDocument3 pagesPracJohn BernieNo ratings yet

- Tugas AF 3Document8 pagesTugas AF 3Rival RmcNo ratings yet

- Managerial Accounting - BADM 2010 F18 Assignment 6 Chapter 11Document4 pagesManagerial Accounting - BADM 2010 F18 Assignment 6 Chapter 11Judy1928No ratings yet

- Financial Analysis CPT 3 2024Document29 pagesFinancial Analysis CPT 3 2024Nazmul HasanNo ratings yet

- Question 1-1-1Document14 pagesQuestion 1-1-1Aqsa AnumNo ratings yet

- ACCT 213 Exercise (Chapter 18) STDocument5 pagesACCT 213 Exercise (Chapter 18) STMohammedNo ratings yet

- Cases ChapterDocument15 pagesCases Chaptermariam.ahmed03No ratings yet

- Name: Nurul Sari NIM: 1101002048 Case 7.1 7.2 7.7: Case 7.1: Investment Center Problems (A)Document4 pagesName: Nurul Sari NIM: 1101002048 Case 7.1 7.2 7.7: Case 7.1: Investment Center Problems (A)Eigha apriliaNo ratings yet

- Review of Financial Statements and Its Analysis: Rheena B. Delos Santos BSBA-1A (FM2)Document12 pagesReview of Financial Statements and Its Analysis: Rheena B. Delos Santos BSBA-1A (FM2)RHIAN B.No ratings yet

- Final Exam Essay QuestionsDocument4 pagesFinal Exam Essay Questionsapi-408647155No ratings yet

- Midterm Revision AnswersDocument10 pagesMidterm Revision AnswersAhmed IsmaelNo ratings yet

- Assignment FM I (2020)Document11 pagesAssignment FM I (2020)ShaggYNo ratings yet

- Lecture 1 - Analysis of Financial Performance - QDocument3 pagesLecture 1 - Analysis of Financial Performance - Q1231402960No ratings yet

- Proformaquestionspart 1Document3 pagesProformaquestionspart 1Kevser BozoğluNo ratings yet

- CH 3 Probset - Analysis of Fin Stmts 15ed - MasterDocument5 pagesCH 3 Probset - Analysis of Fin Stmts 15ed - MasterCharleene GutierrezNo ratings yet

- M&a Paper ACTG421Document11 pagesM&a Paper ACTG421Alex AdamovNo ratings yet

- Profitability & Market Value Analysis IIDocument8 pagesProfitability & Market Value Analysis IIasad malickNo ratings yet

- Question - BS and FADocument6 pagesQuestion - BS and FANguyễn Thùy LinhNo ratings yet

- Question - FS and FADocument6 pagesQuestion - FS and FANguyễn Thùy LinhNo ratings yet

- Answers To End-Of-Chapter QuestionsDocument4 pagesAnswers To End-Of-Chapter QuestionsQuenie De la CruzNo ratings yet

- Casos Analisis de PerformanceDocument4 pagesCasos Analisis de PerformanceJohan UsecheNo ratings yet

- Finman Q2Document14 pagesFinman Q2Rhn SbdNo ratings yet

- A. All of The AboveDocument11 pagesA. All of The AbovetikaNo ratings yet

- Analysis and Interpretetion of Financial StatementsDocument4 pagesAnalysis and Interpretetion of Financial StatementsRida AzamNo ratings yet

- Chapter 12 ProblemsDocument40 pagesChapter 12 ProblemsInciaNo ratings yet

- Financial Statement AnalysisDocument48 pagesFinancial Statement AnalysisCheryl LowNo ratings yet

- HI 5020 Corporate Accounting: Session 8b Intra-Group TransactionsDocument16 pagesHI 5020 Corporate Accounting: Session 8b Intra-Group TransactionsFeku RamNo ratings yet

- CB Chapter 15 AnswerDocument5 pagesCB Chapter 15 AnswerSim Pei YingNo ratings yet

- Capmark Group 1Document20 pagesCapmark Group 1Rhoney GabrielNo ratings yet

- Ratios AssignmentDocument3 pagesRatios AssignmentDiana SaidNo ratings yet

- Tarea Taller 1 FINA 503Document4 pagesTarea Taller 1 FINA 503Hugo LombardiNo ratings yet

- Mill A N CH A Pter 1 Business Combin A Tion P A RT 3 CompressDocument5 pagesMill A N CH A Pter 1 Business Combin A Tion P A RT 3 CompressAubrey Shaiyne OfianaNo ratings yet

- Business Finance - Tutorial QuestionsDocument2 pagesBusiness Finance - Tutorial QuestionsButhaina HNo ratings yet

- Business Finance - Tutorial QuestionsDocument2 pagesBusiness Finance - Tutorial QuestionsButhaina HNo ratings yet

- Financial Statement Analysis: Practice Exercises PE 15Document29 pagesFinancial Statement Analysis: Practice Exercises PE 15Samuel EtanaNo ratings yet

- Mid-Term Test Preparation QuestionsDocument5 pagesMid-Term Test Preparation QuestionsDurjoy SharmaNo ratings yet

- C5B Profitability AnalysisDocument6 pagesC5B Profitability AnalysisSteeeeeeeephNo ratings yet

- Financial Statements and Cash Flow: Solutions To Questions and ProblemsDocument10 pagesFinancial Statements and Cash Flow: Solutions To Questions and ProblemsTing-An KuoNo ratings yet

- Segment Reporting, Decentralization and The Balanced ScorecardDocument20 pagesSegment Reporting, Decentralization and The Balanced ScorecardSneha SureshNo ratings yet

- Managerial Finance - Midterm ExamDocument4 pagesManagerial Finance - Midterm ExamNerissaNo ratings yet

- Fs Analysis MC ProblemsDocument7 pagesFs Analysis MC ProblemsarkishaNo ratings yet

- Common Size Balance SheetDocument16 pagesCommon Size Balance SheetNinaMartirezNo ratings yet

- Bài tập FRA - FRCDocument12 pagesBài tập FRA - FRCThủy VũNo ratings yet

- No 4Document14 pagesNo 4Adistya QoshiratuthorfiNo ratings yet

- Fin Exam 1Document14 pagesFin Exam 1tahaalkibsiNo ratings yet

- Financial Planning Working Capital Management Cash ManagementDocument22 pagesFinancial Planning Working Capital Management Cash ManagementDeniz OnalNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Total Quality Management (TQM) Practices Toward Product Quality Performance: Case at Food and Beverage Industry in Makassar, IndonesiaDocument2 pagesTotal Quality Management (TQM) Practices Toward Product Quality Performance: Case at Food and Beverage Industry in Makassar, IndonesiaShakilNo ratings yet

- Guidelines Template For Business Plan (For Window 3)Document14 pagesGuidelines Template For Business Plan (For Window 3)ShakilNo ratings yet

- Template For Concept Note (For Window 2 & 3) Important Notes For ApplicantsDocument19 pagesTemplate For Concept Note (For Window 2 & 3) Important Notes For ApplicantsShakilNo ratings yet

- Final Assignment - Sahadat Hossain - 1930948Document8 pagesFinal Assignment - Sahadat Hossain - 1930948ShakilNo ratings yet

- Credit Management System of Uttara Bank Limited. 1 - PageDocument73 pagesCredit Management System of Uttara Bank Limited. 1 - PageShakilNo ratings yet

- Email Body - Alim HaiderDocument1 pageEmail Body - Alim HaiderShakilNo ratings yet

- Cost Accounting MathsDocument15 pagesCost Accounting MathsShakilNo ratings yet

- Virat Singh 7 C: St. Mary's Convent Inter College Manak Nagar, LucknowDocument21 pagesVirat Singh 7 C: St. Mary's Convent Inter College Manak Nagar, LucknowShakilNo ratings yet

- Email Body Leather, Footwear & TanneryDocument1 pageEmail Body Leather, Footwear & TanneryShakilNo ratings yet

- Email Body Leather, Footwear & TanneryDocument1 pageEmail Body Leather, Footwear & TanneryShakilNo ratings yet

- Email BodyDocument1 pageEmail BodyShakilNo ratings yet

- A Ready Made Garments (RMG) Company in Bangladesh.Document25 pagesA Ready Made Garments (RMG) Company in Bangladesh.ShakilNo ratings yet

- Email Body - Alim HaiderDocument1 pageEmail Body - Alim HaiderShakilNo ratings yet

- Email Body - Light EngineeringDocument1 pageEmail Body - Light EngineeringShakilNo ratings yet

- Email Body - FaridulDocument1 pageEmail Body - FaridulShakilNo ratings yet

- Macro Economics: MBA 510 Section: 3 A Comparative Analysis The Unemployment Scenario of BangladeshDocument16 pagesMacro Economics: MBA 510 Section: 3 A Comparative Analysis The Unemployment Scenario of BangladeshShakilNo ratings yet

- Financial Management, MBA511, Section: 01 Chapter 3: ProblemsDocument2 pagesFinancial Management, MBA511, Section: 01 Chapter 3: ProblemsShakilNo ratings yet

- Financial Management, MBA511, Section: 01 Chapter 3: ProblemsDocument1 pageFinancial Management, MBA511, Section: 01 Chapter 3: ProblemsShakilNo ratings yet

- Do You Think Using Sexist and Discriminatory Words in Your Writing Is Really ProblemDocument3 pagesDo You Think Using Sexist and Discriminatory Words in Your Writing Is Really ProblemShakilNo ratings yet

- To Basic Concepts in FinanceDocument14 pagesTo Basic Concepts in FinanceShakilNo ratings yet

- Independent University, Bangladesh (IUB)Document1 pageIndependent University, Bangladesh (IUB)ShakilNo ratings yet

- Managerial Economics MBA 505 Section-1 InfinityDocument12 pagesManagerial Economics MBA 505 Section-1 InfinityShakilNo ratings yet

- Winfo Bangladesh Limited: 1.0 Project TitleDocument13 pagesWinfo Bangladesh Limited: 1.0 Project TitleShakilNo ratings yet

- Royal Mail CaseDocument5 pagesRoyal Mail Casedf0% (1)

- SBR Study Notes - 2018 - Updated - PDF Downloaded FromDocument293 pagesSBR Study Notes - 2018 - Updated - PDF Downloaded FromBruce100% (4)

- The Global Capital Market: International BusinessDocument15 pagesThe Global Capital Market: International Businesssonia_hun885443No ratings yet

- Rishikesh Raj Singh (Muthoot Group)Document58 pagesRishikesh Raj Singh (Muthoot Group)Rishikesh Raj SinghNo ratings yet

- Private Equity PHD ThesisDocument7 pagesPrivate Equity PHD Thesisafknikfgd100% (2)

- Financial Valuation of Summit Alliance Port LTDDocument15 pagesFinancial Valuation of Summit Alliance Port LTDAnik DeyNo ratings yet

- Komparasi Capital Asset Pricing Model Versus Arbitrage Pricing Theory Model Atas Volatilitas Return SahamDocument19 pagesKomparasi Capital Asset Pricing Model Versus Arbitrage Pricing Theory Model Atas Volatilitas Return SahamIDFL IDFLNo ratings yet

- QNFS31Dec2013 25 2 14 400pm2Document60 pagesQNFS31Dec2013 25 2 14 400pm2AamirKhanNo ratings yet

- Chapter-24 IpmDocument75 pagesChapter-24 IpmĐặng Thùy HươngNo ratings yet

- Atlas Copco Annual Report 2009 - tcm10-1201956Document144 pagesAtlas Copco Annual Report 2009 - tcm10-1201956Siva Nageswara Rao Chebrolu0% (1)

- Preparation of A Financial Model To Calculate Unit Cost by Using MS ExcelDocument37 pagesPreparation of A Financial Model To Calculate Unit Cost by Using MS ExcelNiranjan NoelNo ratings yet

- School of Law III Internals: Submitted To: Awadhesh Pathak Sir Submitted By: Isha Verma (2020/16)Document15 pagesSchool of Law III Internals: Submitted To: Awadhesh Pathak Sir Submitted By: Isha Verma (2020/16)Isha VermaNo ratings yet

- Fin204 Ca 2Document12 pagesFin204 Ca 2DEEWAKAR KUMARNo ratings yet

- ICICI Direct - Research ReportDocument4 pagesICICI Direct - Research ReportMudit KediaNo ratings yet

- Solution Ipa Week 1 Chapter 3Document47 pagesSolution Ipa Week 1 Chapter 3Aura MaghfiraNo ratings yet

- Financial Analysis M&PDocument34 pagesFinancial Analysis M&Panastasia_kalliNo ratings yet

- Freak TradeDocument14 pagesFreak Tradejeet_singh_deepNo ratings yet

- Thrive Form Convertible Note Purchase AgreementDocument33 pagesThrive Form Convertible Note Purchase AgreementSangram SabatNo ratings yet

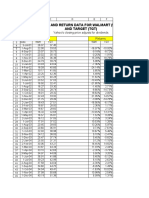

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument19 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahNo ratings yet

- Chapter 4Document11 pagesChapter 4Seid KassawNo ratings yet

- What Is The Philippine Stock Exchange, Inc.?Document2 pagesWhat Is The Philippine Stock Exchange, Inc.?Genelle SorianoNo ratings yet

- Dabur Financial Ratio AnalysisDocument16 pagesDabur Financial Ratio AnalysisLakshmi Srinivasan100% (1)

- Assignment FPADocument5 pagesAssignment FPAsuwilanji nachilombeNo ratings yet

- Business Finance Assignment No. 4Document2 pagesBusiness Finance Assignment No. 4Afghan TvNo ratings yet

- Monthly Unicorn Report - Jan 2021Document95 pagesMonthly Unicorn Report - Jan 2021Tulasi Ram BoddetiNo ratings yet

- Essentials of Private Real Estate International BrochureDocument16 pagesEssentials of Private Real Estate International BrochureNNo ratings yet

- Course Part4 Demat Basics PDFDocument7 pagesCourse Part4 Demat Basics PDFKirankumarNo ratings yet