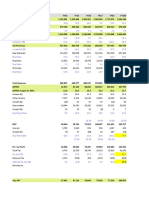

Appendix 1 Conservative Approach: (In FFR Million)

Appendix 1 Conservative Approach: (In FFR Million)

You might also like

- Case 11 Horniman Horticulture 20170504Document16 pagesCase 11 Horniman Horticulture 20170504Chittisa Charoenpanich100% (4)

- Beat The System - How To Get Out of Chexsystems!Document6 pagesBeat The System - How To Get Out of Chexsystems!moneyjunkieNo ratings yet

- Sample Plaint-Suit For Recovery of DebtDocument6 pagesSample Plaint-Suit For Recovery of DebtAAnmol Narang100% (1)

- Visa Consulting and AnalyticsDocument20 pagesVisa Consulting and AnalyticsKristen NguyenNo ratings yet

- Is Excel Participant - Simplified v2Document10 pagesIs Excel Participant - Simplified v2Aaron Pool0% (2)

- Peng Plasma Solutions Tables PDFDocument12 pagesPeng Plasma Solutions Tables PDFDanielle WalkerNo ratings yet

- Marketing ManagementDocument5 pagesMarketing ManagementSarvagya JhaNo ratings yet

- FX Risk Hedging at EADS: Group 1-Prachi Gupta Pranav Gupta Sarvagya Jha Harshvardhan Singh Puneet GargDocument9 pagesFX Risk Hedging at EADS: Group 1-Prachi Gupta Pranav Gupta Sarvagya Jha Harshvardhan Singh Puneet GargSarvagya JhaNo ratings yet

- Corporate ParentingDocument32 pagesCorporate ParentingSarvagya Jha100% (1)

- (In $ Million) : WHX Corporation (WHX)Document3 pages(In $ Million) : WHX Corporation (WHX)Amit JainNo ratings yet

- RatioDocument11 pagesRatioAnant BothraNo ratings yet

- Werner - Financial Model - Final VersionDocument2 pagesWerner - Financial Model - Final VersionAmit JainNo ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2animecommunity04No ratings yet

- M1 12-BZ2 PACIFIC - BlankDocument4 pagesM1 12-BZ2 PACIFIC - BlankKhushi singhalNo ratings yet

- Masonite Corp DCF Analysis FinalDocument5 pagesMasonite Corp DCF Analysis FinaladiNo ratings yet

- BLUE STAR LTD - Quantamental Equity Research Report-1Document1 pageBLUE STAR LTD - Quantamental Equity Research Report-1Vivek NambiarNo ratings yet

- Is Excel Participant Samarth - Simplified v2Document9 pagesIs Excel Participant Samarth - Simplified v2samarth halliNo ratings yet

- Key Performance Indicators Y/E MarchDocument1 pageKey Performance Indicators Y/E Marchretrov androsNo ratings yet

- Cost of Capital - NikeDocument6 pagesCost of Capital - NikeAditi KhaitanNo ratings yet

- M1 14-AZ2 PENROSE Part 1 (Analysis) - BlankDocument5 pagesM1 14-AZ2 PENROSE Part 1 (Analysis) - BlankKhushi singhalNo ratings yet

- Momo Operating Report 2Q20Document5 pagesMomo Operating Report 2Q20Wong Kai WenNo ratings yet

- IIFL Finance Q1FY24 Data BookDocument11 pagesIIFL Finance Q1FY24 Data Bookvishwesheswaran1No ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2Art Euphoria100% (1)

- DL 2023 Geschaeftsbericht enDocument313 pagesDL 2023 Geschaeftsbericht endobojNo ratings yet

- Discounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No FormulasDocument2 pagesDiscounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No Formulasrito2005No ratings yet

- Gymboree LBO Model ComDocument7 pagesGymboree LBO Model ComrolandsudhofNo ratings yet

- 2009 Annual Financial ReportDocument287 pages2009 Annual Financial Reportpcelica77No ratings yet

- A E L (AEL) : Mber Nterprises TDDocument8 pagesA E L (AEL) : Mber Nterprises TDdarshanmadeNo ratings yet

- Investor Presentation 30.09.2023Document30 pagesInvestor Presentation 30.09.2023amitsbhatiNo ratings yet

- 2008 Annual Financial ReportDocument268 pages2008 Annual Financial Reportpcelica77No ratings yet

- Cummins India Financial ModelDocument52 pagesCummins India Financial ModelJitendra YadavNo ratings yet

- 2008 Annual ReportDocument224 pages2008 Annual Reportpcelica77No ratings yet

- KKCL - Investor Presentation Q2 & H1FY24Document45 pagesKKCL - Investor Presentation Q2 & H1FY24Variable SeperableNo ratings yet

- Is Excel Participant - Simplified v2Document9 pagesIs Excel Participant - Simplified v2dikshapatil6789No ratings yet

- News Release INDY Result 6M22Document7 pagesNews Release INDY Result 6M22Rama Usaha MandiriNo ratings yet

- Cost of Capital - NikeDocument6 pagesCost of Capital - NikeAnuj SaxenaNo ratings yet

- Atherine S OnfectioneryDocument3 pagesAtherine S OnfectioneryVanshika SinghNo ratings yet

- 2006 Annual ReportDocument196 pages2006 Annual Reportpcelica77No ratings yet

- Purchases / Average Payables Revenue / Average Total AssetsDocument7 pagesPurchases / Average Payables Revenue / Average Total AssetstannuNo ratings yet

- News Release INDY Result 3M22Document7 pagesNews Release INDY Result 3M22M Rizky PermanaNo ratings yet

- BoeingDocument11 pagesBoeingPreksha GulatiNo ratings yet

- DCF ConeDocument37 pagesDCF Conejustinbui85No ratings yet

- Manaal - Commercial Banking W J.P MorganDocument9 pagesManaal - Commercial Banking W J.P Morganmanaal.murtaza1No ratings yet

- DCF ModellDocument7 pagesDCF ModellziuziNo ratings yet

- Monmouth Inc Figures in Million $Document3 pagesMonmouth Inc Figures in Million $amanNo ratings yet

- Nike - Case Study MeenalDocument9 pagesNike - Case Study MeenalAnchal ChokhaniNo ratings yet

- Nike - Case StudyDocument9 pagesNike - Case StudyAnchal ChokhaniNo ratings yet

- Super Project AnalysisDocument6 pagesSuper Project AnalysisDHRUV SONAGARANo ratings yet

- DCF ModellDocument7 pagesDCF Modellsandeep0604No ratings yet

- Exhibit 1 Selected Pinkerton's Financial Data (In $millions)Document1 pageExhibit 1 Selected Pinkerton's Financial Data (In $millions)Abhishek KumarNo ratings yet

- Financial Analysis: ITC Ltd. Ticker: ITC: Prepared By: EdualphaDocument13 pagesFinancial Analysis: ITC Ltd. Ticker: ITC: Prepared By: EdualphaParas LodayaNo ratings yet

- Max S Group Inc PSE MAXS FinancialsDocument36 pagesMax S Group Inc PSE MAXS FinancialsJasper Andrew AdjaraniNo ratings yet

- Ten Year Review - Standalone: Asian Paints LimitedDocument10 pagesTen Year Review - Standalone: Asian Paints Limitedmaruthi631No ratings yet

- 2007 Annual ReportDocument152 pages2007 Annual Reportpcelica77No ratings yet

- Comcast Model ShareableDocument27 pagesComcast Model Shareablep44153No ratings yet

- Y-Y Growth (%) Y-Y Growth (%) Y-Y Growth (%) Utilization (%) Y-Y Growth (%) % of Sales % of Sales % of SalesDocument45 pagesY-Y Growth (%) Y-Y Growth (%) Y-Y Growth (%) Utilization (%) Y-Y Growth (%) % of Sales % of Sales % of SalesSHIKHA CHAUHANNo ratings yet

- Βequity = Βasset (1+ (1-Tc) X B/S) : Asset Beta 0.71 0.63 0.8 Average 0.725 Tax 40%Document10 pagesΒequity = Βasset (1+ (1-Tc) X B/S) : Asset Beta 0.71 0.63 0.8 Average 0.725 Tax 40%AkashNachraniNo ratings yet

- DCF ModelDocument6 pagesDCF ModelKatherine ChouNo ratings yet

- DCF PDFDocument2 pagesDCF PDFMd Rasel Uddin ACMANo ratings yet

- IS Excel Participant (Risit Savani) - Simplified v2Document9 pagesIS Excel Participant (Risit Savani) - Simplified v2risitsavaniNo ratings yet

- Tutorial On How To Use The DCF Model. Good Luck!: DateDocument9 pagesTutorial On How To Use The DCF Model. Good Luck!: DateTanya SinghNo ratings yet

- Beta Apparel Inc. Always-Glory International Inc. B-II Apparel Group Cambridge Inds. Petty Belly Inc. Avg of Peer GroupDocument21 pagesBeta Apparel Inc. Always-Glory International Inc. B-II Apparel Group Cambridge Inds. Petty Belly Inc. Avg of Peer GroupDamion KenwoodNo ratings yet

- Investment Banking, 3E: Valuation, Lbos, M&A, and IposDocument10 pagesInvestment Banking, 3E: Valuation, Lbos, M&A, and IposBook SittiwatNo ratings yet

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- Dr. Daisy Chauhan Associate Professor: Management Development Institute, Gurgaon Daisy@mdi - Ac.inDocument20 pagesDr. Daisy Chauhan Associate Professor: Management Development Institute, Gurgaon Daisy@mdi - Ac.inSarvagya JhaNo ratings yet

- Designation:: Parents For 2 LakhsDocument1 pageDesignation:: Parents For 2 LakhsSarvagya JhaNo ratings yet

- The Absolut Initiative: Deirdre RyanDocument30 pagesThe Absolut Initiative: Deirdre RyanSarvagya JhaNo ratings yet

- Introduction To OB & Its RelevanceDocument20 pagesIntroduction To OB & Its RelevanceSarvagya JhaNo ratings yet

- Motivation: Concepts & ApplicationDocument29 pagesMotivation: Concepts & ApplicationSarvagya JhaNo ratings yet

- Understanding Personality TypesDocument28 pagesUnderstanding Personality TypesSarvagya JhaNo ratings yet

- 19P044 - PGPM - Sarvagya Jha - Risk and Financial AdvisoryDocument3 pages19P044 - PGPM - Sarvagya Jha - Risk and Financial AdvisorySarvagya JhaNo ratings yet

- 19P044 - PGPM - Sarvagya Jha - Risk and Financial AdvisoryDocument3 pages19P044 - PGPM - Sarvagya Jha - Risk and Financial AdvisorySarvagya JhaNo ratings yet

- Project Titles and Briefs: Consumer InsightsDocument47 pagesProject Titles and Briefs: Consumer InsightsSarvagya JhaNo ratings yet

- Measures of CRMDocument21 pagesMeasures of CRMSarvagya JhaNo ratings yet

- Tchibo Ideas: Leveraging The Creativity of CustomersDocument14 pagesTchibo Ideas: Leveraging The Creativity of CustomersSarvagya JhaNo ratings yet

- Course Title: Consumer Behavior: PGPM 2019-21 Term IVDocument10 pagesCourse Title: Consumer Behavior: PGPM 2019-21 Term IVSarvagya JhaNo ratings yet

- Corporate Level StrategyDocument24 pagesCorporate Level StrategySarvagya JhaNo ratings yet

- Citi PDFDocument20 pagesCiti PDFSarvagya JhaNo ratings yet

- Group 5 - Sec - A - AGH Vs Aravind Eye CareDocument2 pagesGroup 5 - Sec - A - AGH Vs Aravind Eye CareSarvagya JhaNo ratings yet

- Group1 - Section C - LEGO and India PostDocument2 pagesGroup1 - Section C - LEGO and India PostSarvagya JhaNo ratings yet

- MCFP SWOT and Early EntryDocument3 pagesMCFP SWOT and Early EntrySarvagya JhaNo ratings yet

- Q & A - Insurance Act, 1938 (Scanner)Document5 pagesQ & A - Insurance Act, 1938 (Scanner)Rohit GargNo ratings yet

- 23si0055 - Ace WaterDocument1 page23si0055 - Ace WaterDeshan SingNo ratings yet

- Jaypee Business School: Page 1 of 1Document1 pageJaypee Business School: Page 1 of 1NAVYA BANSAL BBG220461No ratings yet

- P1 Exams Set ADocument10 pagesP1 Exams Set Aerica lamsenNo ratings yet

- Salary Slip Format in PDF All PDFDocument3 pagesSalary Slip Format in PDF All PDFRajeev GunasekaranNo ratings yet

- Section 2 - Personal+Budget+TemplateDocument3 pagesSection 2 - Personal+Budget+TemplateZain KhanNo ratings yet

- Financial Projections and BudgetsDocument53 pagesFinancial Projections and BudgetsRaquel Sibal RodriguezNo ratings yet

- Mutual: FundsDocument20 pagesMutual: FundsNitin GuptaNo ratings yet

- SiomaiDocument27 pagesSiomaiChristine Margoux SiriosNo ratings yet

- 100 Percent Financial Inclusion - Gulbarga District InitiativeDocument7 pages100 Percent Financial Inclusion - Gulbarga District InitiativeBasavaraj MtNo ratings yet

- Partnership Agreement Between Two Limited CompaniesDocument7 pagesPartnership Agreement Between Two Limited CompaniesSam Ta0% (1)

- Shehroz Walji Eliazar Kolachi: Engro FertilizersDocument24 pagesShehroz Walji Eliazar Kolachi: Engro FertilizersWajiha FatimaNo ratings yet

- Branch Accounting QuestionsDocument8 pagesBranch Accounting QuestionsFikru KajelaNo ratings yet

- CDCS Specimen Paper A - 2017-18Document35 pagesCDCS Specimen Paper A - 2017-18LêTrungHiếuNo ratings yet

- Indian Bond MarketDocument4 pagesIndian Bond MarketAmritangshu BanerjeeNo ratings yet

- CV Hardik Shah AnalystDocument2 pagesCV Hardik Shah AnalystRahul KhursijaNo ratings yet

- InsDocument5 pagesInsJM MathewNo ratings yet

- Invoice CT-2237144Document2 pagesInvoice CT-2237144ABALUNo ratings yet

- Anna Brockle PDFDocument1 pageAnna Brockle PDFNoticias FarándulasNo ratings yet

- ACCN08B. Module 3 - Statement of Comprehensive IncomeDocument6 pagesACCN08B. Module 3 - Statement of Comprehensive IncomeYolly DiazNo ratings yet

- Project Financial ServicesDocument71 pagesProject Financial ServicesPardeep YadavNo ratings yet

- Pas 40 Concept MapDocument1 pagePas 40 Concept MapJohn Steve VasalloNo ratings yet

- Thompson-DeWitt Financial Group's New York Advisory Office Jumps Into The Asset-Based Lending ArenaDocument3 pagesThompson-DeWitt Financial Group's New York Advisory Office Jumps Into The Asset-Based Lending ArenaPR.comNo ratings yet

- Multiple Choice Questions 1 The Random Walk Theory Suggests ADocument2 pagesMultiple Choice Questions 1 The Random Walk Theory Suggests Atrilocksp SinghNo ratings yet

- Mechanics of Futures MarketDocument11 pagesMechanics of Futures MarketSUMIT JANKARNo ratings yet

- Powers & Authority of The Commissioner of Internal Revenue Under Sec. 4-7, Title 1 of The Tax CodeDocument24 pagesPowers & Authority of The Commissioner of Internal Revenue Under Sec. 4-7, Title 1 of The Tax CodeRovi PatinoNo ratings yet

- Systematic Risk Vs Unsystematic RiskDocument2 pagesSystematic Risk Vs Unsystematic RiskJayesh PatelNo ratings yet

Download as xls, pdf, or txt

You might also like

- Case 11 Horniman Horticulture 20170504Document16 pagesCase 11 Horniman Horticulture 20170504Chittisa Charoenpanich100% (4)

- Beat The System - How To Get Out of Chexsystems!Document6 pagesBeat The System - How To Get Out of Chexsystems!moneyjunkieNo ratings yet

- Sample Plaint-Suit For Recovery of DebtDocument6 pagesSample Plaint-Suit For Recovery of DebtAAnmol Narang100% (1)

- Visa Consulting and AnalyticsDocument20 pagesVisa Consulting and AnalyticsKristen NguyenNo ratings yet

- Is Excel Participant - Simplified v2Document10 pagesIs Excel Participant - Simplified v2Aaron Pool0% (2)

- Peng Plasma Solutions Tables PDFDocument12 pagesPeng Plasma Solutions Tables PDFDanielle WalkerNo ratings yet

- Marketing ManagementDocument5 pagesMarketing ManagementSarvagya JhaNo ratings yet

- FX Risk Hedging at EADS: Group 1-Prachi Gupta Pranav Gupta Sarvagya Jha Harshvardhan Singh Puneet GargDocument9 pagesFX Risk Hedging at EADS: Group 1-Prachi Gupta Pranav Gupta Sarvagya Jha Harshvardhan Singh Puneet GargSarvagya JhaNo ratings yet

- Corporate ParentingDocument32 pagesCorporate ParentingSarvagya Jha100% (1)

- (In $ Million) : WHX Corporation (WHX)Document3 pages(In $ Million) : WHX Corporation (WHX)Amit JainNo ratings yet

- RatioDocument11 pagesRatioAnant BothraNo ratings yet

- Werner - Financial Model - Final VersionDocument2 pagesWerner - Financial Model - Final VersionAmit JainNo ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2animecommunity04No ratings yet

- M1 12-BZ2 PACIFIC - BlankDocument4 pagesM1 12-BZ2 PACIFIC - BlankKhushi singhalNo ratings yet

- Masonite Corp DCF Analysis FinalDocument5 pagesMasonite Corp DCF Analysis FinaladiNo ratings yet

- BLUE STAR LTD - Quantamental Equity Research Report-1Document1 pageBLUE STAR LTD - Quantamental Equity Research Report-1Vivek NambiarNo ratings yet

- Is Excel Participant Samarth - Simplified v2Document9 pagesIs Excel Participant Samarth - Simplified v2samarth halliNo ratings yet

- Key Performance Indicators Y/E MarchDocument1 pageKey Performance Indicators Y/E Marchretrov androsNo ratings yet

- Cost of Capital - NikeDocument6 pagesCost of Capital - NikeAditi KhaitanNo ratings yet

- M1 14-AZ2 PENROSE Part 1 (Analysis) - BlankDocument5 pagesM1 14-AZ2 PENROSE Part 1 (Analysis) - BlankKhushi singhalNo ratings yet

- Momo Operating Report 2Q20Document5 pagesMomo Operating Report 2Q20Wong Kai WenNo ratings yet

- IIFL Finance Q1FY24 Data BookDocument11 pagesIIFL Finance Q1FY24 Data Bookvishwesheswaran1No ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2Art Euphoria100% (1)

- DL 2023 Geschaeftsbericht enDocument313 pagesDL 2023 Geschaeftsbericht endobojNo ratings yet

- Discounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No FormulasDocument2 pagesDiscounted Cash Flow (DCF) Valuation: This Model Is For Illustrative Purposes Only and Contains No Formulasrito2005No ratings yet

- Gymboree LBO Model ComDocument7 pagesGymboree LBO Model ComrolandsudhofNo ratings yet

- 2009 Annual Financial ReportDocument287 pages2009 Annual Financial Reportpcelica77No ratings yet

- A E L (AEL) : Mber Nterprises TDDocument8 pagesA E L (AEL) : Mber Nterprises TDdarshanmadeNo ratings yet

- Investor Presentation 30.09.2023Document30 pagesInvestor Presentation 30.09.2023amitsbhatiNo ratings yet

- 2008 Annual Financial ReportDocument268 pages2008 Annual Financial Reportpcelica77No ratings yet

- Cummins India Financial ModelDocument52 pagesCummins India Financial ModelJitendra YadavNo ratings yet

- 2008 Annual ReportDocument224 pages2008 Annual Reportpcelica77No ratings yet

- KKCL - Investor Presentation Q2 & H1FY24Document45 pagesKKCL - Investor Presentation Q2 & H1FY24Variable SeperableNo ratings yet

- Is Excel Participant - Simplified v2Document9 pagesIs Excel Participant - Simplified v2dikshapatil6789No ratings yet

- News Release INDY Result 6M22Document7 pagesNews Release INDY Result 6M22Rama Usaha MandiriNo ratings yet

- Cost of Capital - NikeDocument6 pagesCost of Capital - NikeAnuj SaxenaNo ratings yet

- Atherine S OnfectioneryDocument3 pagesAtherine S OnfectioneryVanshika SinghNo ratings yet

- 2006 Annual ReportDocument196 pages2006 Annual Reportpcelica77No ratings yet

- Purchases / Average Payables Revenue / Average Total AssetsDocument7 pagesPurchases / Average Payables Revenue / Average Total AssetstannuNo ratings yet

- News Release INDY Result 3M22Document7 pagesNews Release INDY Result 3M22M Rizky PermanaNo ratings yet

- BoeingDocument11 pagesBoeingPreksha GulatiNo ratings yet

- DCF ConeDocument37 pagesDCF Conejustinbui85No ratings yet

- Manaal - Commercial Banking W J.P MorganDocument9 pagesManaal - Commercial Banking W J.P Morganmanaal.murtaza1No ratings yet

- DCF ModellDocument7 pagesDCF ModellziuziNo ratings yet

- Monmouth Inc Figures in Million $Document3 pagesMonmouth Inc Figures in Million $amanNo ratings yet

- Nike - Case Study MeenalDocument9 pagesNike - Case Study MeenalAnchal ChokhaniNo ratings yet

- Nike - Case StudyDocument9 pagesNike - Case StudyAnchal ChokhaniNo ratings yet

- Super Project AnalysisDocument6 pagesSuper Project AnalysisDHRUV SONAGARANo ratings yet

- DCF ModellDocument7 pagesDCF Modellsandeep0604No ratings yet

- Exhibit 1 Selected Pinkerton's Financial Data (In $millions)Document1 pageExhibit 1 Selected Pinkerton's Financial Data (In $millions)Abhishek KumarNo ratings yet

- Financial Analysis: ITC Ltd. Ticker: ITC: Prepared By: EdualphaDocument13 pagesFinancial Analysis: ITC Ltd. Ticker: ITC: Prepared By: EdualphaParas LodayaNo ratings yet

- Max S Group Inc PSE MAXS FinancialsDocument36 pagesMax S Group Inc PSE MAXS FinancialsJasper Andrew AdjaraniNo ratings yet

- Ten Year Review - Standalone: Asian Paints LimitedDocument10 pagesTen Year Review - Standalone: Asian Paints Limitedmaruthi631No ratings yet

- 2007 Annual ReportDocument152 pages2007 Annual Reportpcelica77No ratings yet

- Comcast Model ShareableDocument27 pagesComcast Model Shareablep44153No ratings yet

- Y-Y Growth (%) Y-Y Growth (%) Y-Y Growth (%) Utilization (%) Y-Y Growth (%) % of Sales % of Sales % of SalesDocument45 pagesY-Y Growth (%) Y-Y Growth (%) Y-Y Growth (%) Utilization (%) Y-Y Growth (%) % of Sales % of Sales % of SalesSHIKHA CHAUHANNo ratings yet

- Βequity = Βasset (1+ (1-Tc) X B/S) : Asset Beta 0.71 0.63 0.8 Average 0.725 Tax 40%Document10 pagesΒequity = Βasset (1+ (1-Tc) X B/S) : Asset Beta 0.71 0.63 0.8 Average 0.725 Tax 40%AkashNachraniNo ratings yet

- DCF ModelDocument6 pagesDCF ModelKatherine ChouNo ratings yet

- DCF PDFDocument2 pagesDCF PDFMd Rasel Uddin ACMANo ratings yet

- IS Excel Participant (Risit Savani) - Simplified v2Document9 pagesIS Excel Participant (Risit Savani) - Simplified v2risitsavaniNo ratings yet

- Tutorial On How To Use The DCF Model. Good Luck!: DateDocument9 pagesTutorial On How To Use The DCF Model. Good Luck!: DateTanya SinghNo ratings yet

- Beta Apparel Inc. Always-Glory International Inc. B-II Apparel Group Cambridge Inds. Petty Belly Inc. Avg of Peer GroupDocument21 pagesBeta Apparel Inc. Always-Glory International Inc. B-II Apparel Group Cambridge Inds. Petty Belly Inc. Avg of Peer GroupDamion KenwoodNo ratings yet

- Investment Banking, 3E: Valuation, Lbos, M&A, and IposDocument10 pagesInvestment Banking, 3E: Valuation, Lbos, M&A, and IposBook SittiwatNo ratings yet

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- Dr. Daisy Chauhan Associate Professor: Management Development Institute, Gurgaon Daisy@mdi - Ac.inDocument20 pagesDr. Daisy Chauhan Associate Professor: Management Development Institute, Gurgaon Daisy@mdi - Ac.inSarvagya JhaNo ratings yet

- Designation:: Parents For 2 LakhsDocument1 pageDesignation:: Parents For 2 LakhsSarvagya JhaNo ratings yet

- The Absolut Initiative: Deirdre RyanDocument30 pagesThe Absolut Initiative: Deirdre RyanSarvagya JhaNo ratings yet

- Introduction To OB & Its RelevanceDocument20 pagesIntroduction To OB & Its RelevanceSarvagya JhaNo ratings yet

- Motivation: Concepts & ApplicationDocument29 pagesMotivation: Concepts & ApplicationSarvagya JhaNo ratings yet

- Understanding Personality TypesDocument28 pagesUnderstanding Personality TypesSarvagya JhaNo ratings yet

- 19P044 - PGPM - Sarvagya Jha - Risk and Financial AdvisoryDocument3 pages19P044 - PGPM - Sarvagya Jha - Risk and Financial AdvisorySarvagya JhaNo ratings yet

- 19P044 - PGPM - Sarvagya Jha - Risk and Financial AdvisoryDocument3 pages19P044 - PGPM - Sarvagya Jha - Risk and Financial AdvisorySarvagya JhaNo ratings yet

- Project Titles and Briefs: Consumer InsightsDocument47 pagesProject Titles and Briefs: Consumer InsightsSarvagya JhaNo ratings yet

- Measures of CRMDocument21 pagesMeasures of CRMSarvagya JhaNo ratings yet

- Tchibo Ideas: Leveraging The Creativity of CustomersDocument14 pagesTchibo Ideas: Leveraging The Creativity of CustomersSarvagya JhaNo ratings yet

- Course Title: Consumer Behavior: PGPM 2019-21 Term IVDocument10 pagesCourse Title: Consumer Behavior: PGPM 2019-21 Term IVSarvagya JhaNo ratings yet

- Corporate Level StrategyDocument24 pagesCorporate Level StrategySarvagya JhaNo ratings yet

- Citi PDFDocument20 pagesCiti PDFSarvagya JhaNo ratings yet

- Group 5 - Sec - A - AGH Vs Aravind Eye CareDocument2 pagesGroup 5 - Sec - A - AGH Vs Aravind Eye CareSarvagya JhaNo ratings yet

- Group1 - Section C - LEGO and India PostDocument2 pagesGroup1 - Section C - LEGO and India PostSarvagya JhaNo ratings yet

- MCFP SWOT and Early EntryDocument3 pagesMCFP SWOT and Early EntrySarvagya JhaNo ratings yet

- Q & A - Insurance Act, 1938 (Scanner)Document5 pagesQ & A - Insurance Act, 1938 (Scanner)Rohit GargNo ratings yet

- 23si0055 - Ace WaterDocument1 page23si0055 - Ace WaterDeshan SingNo ratings yet

- Jaypee Business School: Page 1 of 1Document1 pageJaypee Business School: Page 1 of 1NAVYA BANSAL BBG220461No ratings yet

- P1 Exams Set ADocument10 pagesP1 Exams Set Aerica lamsenNo ratings yet

- Salary Slip Format in PDF All PDFDocument3 pagesSalary Slip Format in PDF All PDFRajeev GunasekaranNo ratings yet

- Section 2 - Personal+Budget+TemplateDocument3 pagesSection 2 - Personal+Budget+TemplateZain KhanNo ratings yet

- Financial Projections and BudgetsDocument53 pagesFinancial Projections and BudgetsRaquel Sibal RodriguezNo ratings yet

- Mutual: FundsDocument20 pagesMutual: FundsNitin GuptaNo ratings yet

- SiomaiDocument27 pagesSiomaiChristine Margoux SiriosNo ratings yet

- 100 Percent Financial Inclusion - Gulbarga District InitiativeDocument7 pages100 Percent Financial Inclusion - Gulbarga District InitiativeBasavaraj MtNo ratings yet

- Partnership Agreement Between Two Limited CompaniesDocument7 pagesPartnership Agreement Between Two Limited CompaniesSam Ta0% (1)

- Shehroz Walji Eliazar Kolachi: Engro FertilizersDocument24 pagesShehroz Walji Eliazar Kolachi: Engro FertilizersWajiha FatimaNo ratings yet

- Branch Accounting QuestionsDocument8 pagesBranch Accounting QuestionsFikru KajelaNo ratings yet

- CDCS Specimen Paper A - 2017-18Document35 pagesCDCS Specimen Paper A - 2017-18LêTrungHiếuNo ratings yet

- Indian Bond MarketDocument4 pagesIndian Bond MarketAmritangshu BanerjeeNo ratings yet

- CV Hardik Shah AnalystDocument2 pagesCV Hardik Shah AnalystRahul KhursijaNo ratings yet

- InsDocument5 pagesInsJM MathewNo ratings yet

- Invoice CT-2237144Document2 pagesInvoice CT-2237144ABALUNo ratings yet

- Anna Brockle PDFDocument1 pageAnna Brockle PDFNoticias FarándulasNo ratings yet

- ACCN08B. Module 3 - Statement of Comprehensive IncomeDocument6 pagesACCN08B. Module 3 - Statement of Comprehensive IncomeYolly DiazNo ratings yet

- Project Financial ServicesDocument71 pagesProject Financial ServicesPardeep YadavNo ratings yet

- Pas 40 Concept MapDocument1 pagePas 40 Concept MapJohn Steve VasalloNo ratings yet

- Thompson-DeWitt Financial Group's New York Advisory Office Jumps Into The Asset-Based Lending ArenaDocument3 pagesThompson-DeWitt Financial Group's New York Advisory Office Jumps Into The Asset-Based Lending ArenaPR.comNo ratings yet

- Multiple Choice Questions 1 The Random Walk Theory Suggests ADocument2 pagesMultiple Choice Questions 1 The Random Walk Theory Suggests Atrilocksp SinghNo ratings yet

- Mechanics of Futures MarketDocument11 pagesMechanics of Futures MarketSUMIT JANKARNo ratings yet

- Powers & Authority of The Commissioner of Internal Revenue Under Sec. 4-7, Title 1 of The Tax CodeDocument24 pagesPowers & Authority of The Commissioner of Internal Revenue Under Sec. 4-7, Title 1 of The Tax CodeRovi PatinoNo ratings yet

- Systematic Risk Vs Unsystematic RiskDocument2 pagesSystematic Risk Vs Unsystematic RiskJayesh PatelNo ratings yet