Download as docx, pdf, or txt

You might also like

- Inferential Statistics For TourismDocument3 pagesInferential Statistics For TourismGeorges OtienoNo ratings yet

- Exploratory Factor AnalysisDocument12 pagesExploratory Factor AnalysisAtiqah IsmailNo ratings yet

- Field Artillery (Part One)Document817 pagesField Artillery (Part One)sithusoemoe100% (2)

- S U R J S S: Indh Niversity Esearch Ournal (Cience Eries)Document6 pagesS U R J S S: Indh Niversity Esearch Ournal (Cience Eries)leostarz05No ratings yet

- Research MethodologyDocument3 pagesResearch MethodologyMunaiyatwinkle JumaNo ratings yet

- Screenshot 2023-09-07 at 22.35.34Document2 pagesScreenshot 2023-09-07 at 22.35.34malijessica907No ratings yet

- Relationship Between Treasury Bill Rate and NEPSE Index in NepalDocument8 pagesRelationship Between Treasury Bill Rate and NEPSE Index in NepalDistro MusicNo ratings yet

- Causal Correlation Between Exchange Rate and Stock PDFDocument13 pagesCausal Correlation Between Exchange Rate and Stock PDFAtaur Rahman HashmiNo ratings yet

- 89 175 1 SMDocument11 pages89 175 1 SMemkaysubhaNo ratings yet

- Measuring Security Price PerformanceDocument2 pagesMeasuring Security Price PerformanceAbdul Wahab ShahidNo ratings yet

- Data and MethodologyDocument5 pagesData and MethodologyAdnan RashidNo ratings yet

- A New Approach For Evaluating Economic Forecasts: Tara M. SinclairDocument13 pagesA New Approach For Evaluating Economic Forecasts: Tara M. SinclairKim-Bich LongNo ratings yet

- PR 2Document11 pagesPR 2vcutph24No ratings yet

- Economic Modelling: Jing Huang, Yougui WangDocument5 pagesEconomic Modelling: Jing Huang, Yougui WangVincent Adrianne CaragNo ratings yet

- Causes of InflationDocument5 pagesCauses of InflationJaved KhanNo ratings yet

- KGEMM MethodologyDocument4 pagesKGEMM MethodologyKING EMRAANNo ratings yet

- Application of Adaptive Neuro-Fuzzy Inference System in Interest Rates Effects On Stock ReturnsDocument13 pagesApplication of Adaptive Neuro-Fuzzy Inference System in Interest Rates Effects On Stock Returnsgiovanis95No ratings yet

- Inflation Impact SpendingDocument11 pagesInflation Impact SpendingMinh NghiêmNo ratings yet

- Demonstrating The Use of Vector Error Correction Models Using Simulated DataDocument17 pagesDemonstrating The Use of Vector Error Correction Models Using Simulated DataChetan KumarNo ratings yet

- Estimation and Forecasting of Stock Volatility With Range - Based EstimatorsDocument22 pagesEstimation and Forecasting of Stock Volatility With Range - Based EstimatorsRahul PinnamaneniNo ratings yet

- Impact of Money Supply On Current Account: Extent of PakistanDocument9 pagesImpact of Money Supply On Current Account: Extent of Pakistanhuma788No ratings yet

- The Analysis of Economic Data Using Multivariate and Time Series TechniqueDocument5 pagesThe Analysis of Economic Data Using Multivariate and Time Series TechniqueKobayashi2014No ratings yet

- Chapter 4 and 5 (2003)Document21 pagesChapter 4 and 5 (2003)zahidkhanoooNo ratings yet

- The Model-Free Implied Volatility and Its Information ContentDocument39 pagesThe Model-Free Implied Volatility and Its Information ContentNikhil AroraNo ratings yet

- NAQIBDocument3 pagesNAQIBAreeb KhanNo ratings yet

- Content ServenbrDocument8 pagesContent Servenbrmuzammal555No ratings yet

- Export Growth and Output GrowthDocument11 pagesExport Growth and Output GrowthMOHD NOR HIDAYAT MELBINNo ratings yet

- Akbar2012 100 200Document101 pagesAkbar2012 100 200Dhea AuwinaNo ratings yet

- ICCBIF2012 KulhanekDocument12 pagesICCBIF2012 KulhanekViet HoangNo ratings yet

- MPRA Paper 33301Document18 pagesMPRA Paper 33301zamirNo ratings yet

- Stock Returns, Quantile Autocorrelation, and Volatility ForecastingDocument50 pagesStock Returns, Quantile Autocorrelation, and Volatility ForecastingShaan Yeat Amin RatulNo ratings yet

- Chapter ThreeDocument5 pagesChapter ThreeeranyigiNo ratings yet

- Macroeconomic Determinants of Exchange Rate Pass-Through in India?Document15 pagesMacroeconomic Determinants of Exchange Rate Pass-Through in India?Hogo DewenNo ratings yet

- 018 Icber2012 N10017Document5 pages018 Icber2012 N10017Anggi BoomNo ratings yet

- Inflation and Economic Growth in Kuwait: 1985-2005 Evidence From Co-Integration and Error Correction ModelDocument13 pagesInflation and Economic Growth in Kuwait: 1985-2005 Evidence From Co-Integration and Error Correction ModelShahbaz ArtsNo ratings yet

- Money, Inflation and Growth Relationship: The Turkish CaseDocument7 pagesMoney, Inflation and Growth Relationship: The Turkish CaseJennifer WijayaNo ratings yet

- Relationship Between Stock Market and Foreign Exchange Market in India: An Empirical StudyDocument7 pagesRelationship Between Stock Market and Foreign Exchange Market in India: An Empirical StudySudeep SureshNo ratings yet

- Chapter 3 MethodologyDocument11 pagesChapter 3 Methodologyassignment helpNo ratings yet

- Biodiesel in IndonesiaDocument10 pagesBiodiesel in IndonesiaHanif Indrastoto WidiawanNo ratings yet

- Assignment3 BscProjectDocument12 pagesAssignment3 BscProjectBernard BrinkelNo ratings yet

- Roughing It Up: Including Jump Components in The Measurement, Modeling, and Forecasting of Return VolatilityDocument20 pagesRoughing It Up: Including Jump Components in The Measurement, Modeling, and Forecasting of Return VolatilityAkhil NekkantiNo ratings yet

- J Jbef 2018 01 005Document14 pagesJ Jbef 2018 01 005inkaNo ratings yet

- Assignment 2 Group 1 ReportDocument13 pagesAssignment 2 Group 1 Reportseksenbaeva.nurgulNo ratings yet

- Returns-Earnings Regressions: An Integrated Approach: Ebartov@stern - Nyu.eduDocument58 pagesReturns-Earnings Regressions: An Integrated Approach: Ebartov@stern - Nyu.eduwirodihardjoNo ratings yet

- 1 PDFDocument14 pages1 PDFAnum AhmedNo ratings yet

- Bai and NG 2002Document31 pagesBai and NG 2002Milan MartinovicNo ratings yet

- Lee Wooldridge 20230720Document45 pagesLee Wooldridge 20230720basirunjie86No ratings yet

- Jurnal 2Document11 pagesJurnal 2devinaNo ratings yet

- Do Liquidity Measures Measure Liquidity by Goyenko, Holden, and Trzcinka (JFE 2009)Document29 pagesDo Liquidity Measures Measure Liquidity by Goyenko, Holden, and Trzcinka (JFE 2009)Eleanor RigbyNo ratings yet

- Essay On Exchange Rates and in Ation: February 2020Document20 pagesEssay On Exchange Rates and in Ation: February 2020LaraibNo ratings yet

- Writeup PseDocument42 pagesWriteup PseFred Nyll TupasNo ratings yet

- Earnings Losses of Displaced Workers Revisited: Kenneth A. Couch and Dana W. PlaczekDocument29 pagesEarnings Losses of Displaced Workers Revisited: Kenneth A. Couch and Dana W. PlaczekRatchanon ChotiputsilpNo ratings yet

- A Case Study of TanzaniaDocument15 pagesA Case Study of TanzaniaVladGrigoreNo ratings yet

- CHAPTER THREE DnialDocument5 pagesCHAPTER THREE DnialAlakaNo ratings yet

- Forecasting S&P 100 Volatility: The Incremental Information Content of Implied Volatilities and High Frequency Index ReturnsDocument35 pagesForecasting S&P 100 Volatility: The Incremental Information Content of Implied Volatilities and High Frequency Index ReturnskshitijsaxenaNo ratings yet

- Export-Led Growth Hypothesis in Malaysia: An Investigation Using Bounds TestDocument10 pagesExport-Led Growth Hypothesis in Malaysia: An Investigation Using Bounds TestSunway UniversityNo ratings yet

- Andersen EtalDocument15 pagesAndersen EtalEu VeronicaNo ratings yet

- PHD Thesis Using Exploratory Factor AnalysisDocument8 pagesPHD Thesis Using Exploratory Factor Analysiskatrinaduartetulsa100% (2)

- IR System EvaluationDocument8 pagesIR System Evaluationlr.indrayanti7330No ratings yet

- Introduction To Business Statistics Through R Software: SoftwareFrom EverandIntroduction To Business Statistics Through R Software: SoftwareNo ratings yet

- Inventory and SCM MCQsDocument20 pagesInventory and SCM MCQsSyed Abdul Wahab Gilani100% (3)

- Inflation and GDP DeflatorDocument1 pageInflation and GDP DeflatorSyed Abdul Wahab GilaniNo ratings yet

- Nps EBD9Document11 pagesNps EBD9Syed Abdul Wahab GilaniNo ratings yet

- Pakistan International Human Development IndicatorsDocument5 pagesPakistan International Human Development IndicatorsSyed Abdul Wahab GilaniNo ratings yet

- Cultural ExchangeDocument3 pagesCultural ExchangeSyed Abdul Wahab GilaniNo ratings yet

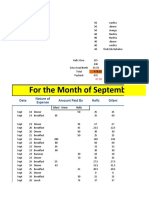

- For The Month of September Only: Date Amount Paid by Hafiz Gilani Nature of ExpenseDocument17 pagesFor The Month of September Only: Date Amount Paid by Hafiz Gilani Nature of ExpenseSyed Abdul Wahab GilaniNo ratings yet

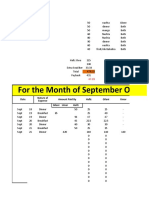

- For The Month of September Only: Date Amount Paid by Hafiz Gilani Umar Gilani Umar Haifz Nature of ExpenseDocument4 pagesFor The Month of September Only: Date Amount Paid by Hafiz Gilani Umar Gilani Umar Haifz Nature of ExpenseSyed Abdul Wahab GilaniNo ratings yet

- GL005 PIPE ROUTING GUIDELINE Rev 2Document22 pagesGL005 PIPE ROUTING GUIDELINE Rev 2MIlan100% (1)

- Kirkpatrick Evaluation A ThoughtDocument2 pagesKirkpatrick Evaluation A ThoughtJYOTSNA ENTERPRISES100% (1)

- Christopher MontoyaDocument1 pageChristopher MontoyaUF Student GovernmentNo ratings yet

- Forget No MoreDocument14 pagesForget No MoreSheeqin Mn100% (2)

- WPP2019 Pop F01 2 Total Population MaleDocument547 pagesWPP2019 Pop F01 2 Total Population MaleMaria BozhkoNo ratings yet

- PHREEQ C Modelling Tool Application To Determine The Effect of Anions On Speciation of Selected Metals in Water Systems Within Kajiado North Constituency in KenyaDocument71 pagesPHREEQ C Modelling Tool Application To Determine The Effect of Anions On Speciation of Selected Metals in Water Systems Within Kajiado North Constituency in KenyaInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Teacher Should Be Very Strict in ClassDocument1 pageTeacher Should Be Very Strict in ClassAbdul ArifNo ratings yet

- CNS-Classifications by Dr-Islahkhan (Humble Pharmacist)Document24 pagesCNS-Classifications by Dr-Islahkhan (Humble Pharmacist)M Ils Meteor Pharmacist0% (1)

- Solar Power PlantDocument23 pagesSolar Power Plantmadhu_bedi12No ratings yet

- Coconut: Donesian Export Pro IleDocument39 pagesCoconut: Donesian Export Pro Ile764fqbbnf2No ratings yet

- The Wild BunchDocument2 pagesThe Wild BuncharnoldNo ratings yet

- Commercial Paper: Presented by Dharani Dharan.m Vijaya Kumar S.BDocument16 pagesCommercial Paper: Presented by Dharani Dharan.m Vijaya Kumar S.Budaya37No ratings yet

- Cyctocyle - Care PlanDocument22 pagesCyctocyle - Care Planarchana vermaNo ratings yet

- Notre Dame of Masiag, Inc.: What Formativ e Question S Shall Lead To The Completi On of Efaa? ToDocument2 pagesNotre Dame of Masiag, Inc.: What Formativ e Question S Shall Lead To The Completi On of Efaa? ToLANY T. CATAMINNo ratings yet

- Bill of Ladding ExampleDocument1 pageBill of Ladding ExampleNguyen LinhNo ratings yet

- Instructor: Nguyen Hoang Khue Tu, PH.D, PharmDocument24 pagesInstructor: Nguyen Hoang Khue Tu, PH.D, PharmChaoswind_Ka_2673No ratings yet

- Central Administration Building: Technical Specifications General DiscriptionDocument7 pagesCentral Administration Building: Technical Specifications General DiscriptionDarcy stylesNo ratings yet

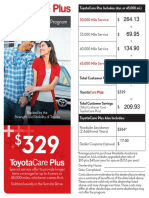

- ToyotaCare Plus CalculationDocument2 pagesToyotaCare Plus CalculationShao MaNo ratings yet

- Bendix Actuator Competitive Cross Reference ListDocument1 pageBendix Actuator Competitive Cross Reference ListFernando PadillaNo ratings yet

- Assignment2 Santos CarlosJoaquin MECp1Document8 pagesAssignment2 Santos CarlosJoaquin MECp1Jake SantosNo ratings yet

- Financial Summary Statement Period 03/10/23 - 04/09/23: Deposit Accounts Total DepositsDocument14 pagesFinancial Summary Statement Period 03/10/23 - 04/09/23: Deposit Accounts Total DepositsLuis RodríguezNo ratings yet

- Pmkvy Guidelines Junior Software DeveloperDocument4 pagesPmkvy Guidelines Junior Software DeveloperJitendra KumarNo ratings yet

- CRING Bank Facilitator by SPE - BNIDocument28 pagesCRING Bank Facilitator by SPE - BNIDaniel AdrianNo ratings yet

- Institutions and Regional Integration in AfricaDocument24 pagesInstitutions and Regional Integration in AfricaOrnela FabaniNo ratings yet

- Fukien Tea Care Sheet: Repo NG: Every 2-3 Years, in Early Spring. ReduceDocument2 pagesFukien Tea Care Sheet: Repo NG: Every 2-3 Years, in Early Spring. Reducecastaneda1No ratings yet

- Interfacing Seven Segment Display To 8051Document16 pagesInterfacing Seven Segment Display To 8051Virang PatelNo ratings yet

- Data Analysis PDFDocument10 pagesData Analysis PDFKenny Stephen CruzNo ratings yet

- Cost Justifying HRIS InvestmentsDocument19 pagesCost Justifying HRIS InvestmentsJessierene ManceraNo ratings yet

- Asterisk For Dumb MeDocument164 pagesAsterisk For Dumb MeAndy CockroftNo ratings yet