Download as docx, pdf, or txt

You might also like

- Canadian Tax Principles, 2019-2020 Edition Clarence Byrd Ida Chen Test Bank and Solution ManualDocument9 pagesCanadian Tax Principles, 2019-2020 Edition Clarence Byrd Ida Chen Test Bank and Solution ManualAdam Kramer0% (2)

- Acc CH2Document4 pagesAcc CH2Trickster TwelveNo ratings yet

- Income Tax - Notice of Assessment (Original) : What Do You Need To Do?Document1 pageIncome Tax - Notice of Assessment (Original) : What Do You Need To Do?tehtarikNo ratings yet

- 14 AdjustmentsssDocument7 pages14 AdjustmentsssZaheer Ahmed SwatiNo ratings yet

- CH 02Document5 pagesCH 02Tien Thanh Dang0% (1)

- BUS 591 WK 6 Template - 092417Document43 pagesBUS 591 WK 6 Template - 092417kapil sharma100% (2)

- 4 Completing The Accounting Cycle PartDocument1 page4 Completing The Accounting Cycle PartTalionNo ratings yet

- Final Exam QuestionDocument4 pagesFinal Exam QuestionHồng XuânNo ratings yet

- Configuration Example: SAP Electronic Bank Statement (SAP - EBS)From EverandConfiguration Example: SAP Electronic Bank Statement (SAP - EBS)Rating: 3 out of 5 stars3/5 (1)

- Council Tax Demand Notice 2020/2021: :-U-Can) 82®Document2 pagesCouncil Tax Demand Notice 2020/2021: :-U-Can) 82®Amruta Lambat Daulatkar100% (1)

- The Accounting Cycle: Capturing Economic EventsDocument37 pagesThe Accounting Cycle: Capturing Economic EventsMasood MehmoodNo ratings yet

- Micolob - Tla 2 - Answers SheetDocument18 pagesMicolob - Tla 2 - Answers SheetHaries MicolobNo ratings yet

- Chapter 4Document109 pagesChapter 4nadima behzadNo ratings yet

- Accounting Principles 10th Edition Weygandt Kimmel Chapter 4 and 5Document14 pagesAccounting Principles 10th Edition Weygandt Kimmel Chapter 4 and 5NiizamUddinBhuiyan100% (1)

- MGMT 600 SAMPLE Midterm Exam 1Document9 pagesMGMT 600 SAMPLE Midterm Exam 1Enkhbadral UlaanhuuNo ratings yet

- Accounting Principles Manual Chapter 5 (Brief Exercises)Document5 pagesAccounting Principles Manual Chapter 5 (Brief Exercises)Dani SaputraNo ratings yet

- Acc 201 CH3Document7 pagesAcc 201 CH3Trickster TwelveNo ratings yet

- 3 Midterm A - AnswerDocument12 pages3 Midterm A - AnswerAllison0% (1)

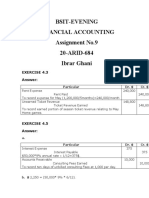

- Bsit-Evening Financial Accounting Assignment No.9 20-ARID-684 Ibrar GhaniDocument3 pagesBsit-Evening Financial Accounting Assignment No.9 20-ARID-684 Ibrar Ghaniibrar ghani100% (1)

- 250 Question PaperDocument3 pages250 Question PaperSam NayakNo ratings yet

- Exam Revision - Chapter 3 4Document6 pagesExam Revision - Chapter 3 4Vũ Thị NgoanNo ratings yet

- Chapter 3 Current Liability PayrollDocument39 pagesChapter 3 Current Liability PayrollAbdi Mucee Tube100% (1)

- Preparing Financial Statements: Key Terms and Concepts To KnowDocument27 pagesPreparing Financial Statements: Key Terms and Concepts To KnowMohammed AkramNo ratings yet

- Preparing Financial Statements: Key Terms and Concepts To KnowDocument27 pagesPreparing Financial Statements: Key Terms and Concepts To KnowTrisha Monique VillaNo ratings yet

- Steps in The Accounting Cycle of A Service Business (Preparing Adjusting Journal Entries)Document26 pagesSteps in The Accounting Cycle of A Service Business (Preparing Adjusting Journal Entries)Zybel RosalesNo ratings yet

- Exam Revision - 3 & 4 SolDocument6 pagesExam Revision - 3 & 4 SolNguyễn Minh ĐứcNo ratings yet

- Cebu CPAR Center: C.C.P.A.R. Practical Accounting Problems 1 - PreweekDocument23 pagesCebu CPAR Center: C.C.P.A.R. Practical Accounting Problems 1 - PreweekIzzy BNo ratings yet

- Student Name: Class: Student No.: .Document5 pagesStudent Name: Class: Student No.: .Thao LeNo ratings yet

- ACCT 735 ICQ For Module 04 SOLUTIONSDocument7 pagesACCT 735 ICQ For Module 04 SOLUTIONSSiopao JolavidezNo ratings yet

- CH 4: Apply Your Knowledge Decision Case 4-1: Accounting 9/e Solutions Manual 392Document15 pagesCH 4: Apply Your Knowledge Decision Case 4-1: Accounting 9/e Solutions Manual 392Loany Martinez100% (1)

- Topic: Adjusting Entries / Adjustments Compiled By: Sir Ghalib HussainDocument8 pagesTopic: Adjusting Entries / Adjustments Compiled By: Sir Ghalib HussainGhalib HussainNo ratings yet

- Multiple Choices and Exercises Chapter 2Document4 pagesMultiple Choices and Exercises Chapter 2Mi Đỗ Thị KhảNo ratings yet

- Lecture 6 The Accounting Cycle Preparing Annual Reports BsafDocument98 pagesLecture 6 The Accounting Cycle Preparing Annual Reports BsafShahzad C7No ratings yet

- Adjusting Entries: Q1: Pass The Necessary Adjusting Entries For The FollowingDocument9 pagesAdjusting Entries: Q1: Pass The Necessary Adjusting Entries For The FollowingHassan AliNo ratings yet

- Spring Semester 2019 Final Exam Closed Notes: INSTRUCTOR: Marios MavridesDocument4 pagesSpring Semester 2019 Final Exam Closed Notes: INSTRUCTOR: Marios MavridesyandaveNo ratings yet

- Far ExercisesDocument34 pagesFar ExercisesTrisha Mae CorpuzNo ratings yet

- Principles Seifu Work SheetDocument5 pagesPrinciples Seifu Work SheetYonas85% (13)

- ACTG 240 - Solutions 01Document4 pagesACTG 240 - Solutions 01xxmbetaNo ratings yet

- Bài Tập Lớn - Môn Principle 14 ĐềDocument29 pagesBài Tập Lớn - Môn Principle 14 Đềp7q27hht77No ratings yet

- Dokumen - Tips 4brief-Ex4Document4 pagesDokumen - Tips 4brief-Ex4Feby NurdianaNo ratings yet

- Chapter 2 Problems and Solutions EnglishDocument8 pagesChapter 2 Problems and Solutions EnglishyandaveNo ratings yet

- Accounting Mid Term RevisionDocument4 pagesAccounting Mid Term Revisionkareem abozeedNo ratings yet

- Accounting Mid Term RevisionDocument4 pagesAccounting Mid Term Revisionkareem abozeedNo ratings yet

- Acc101 - Chapter 2: Accounting For TransactionsDocument16 pagesAcc101 - Chapter 2: Accounting For TransactionsMauricio AceNo ratings yet

- Examples Ch3 SolutionDocument7 pagesExamples Ch3 SolutionNajwa Al-khateebNo ratings yet

- Exercise 1,8Document1 pageExercise 1,8trangdoan.31221023445No ratings yet

- Chapter 1 QuizDocument6 pagesChapter 1 Quizhantu hantuNo ratings yet

- Adjustments (Part 3) : Subject-Descriptive Title Subject - CodeDocument17 pagesAdjustments (Part 3) : Subject-Descriptive Title Subject - CodeRose LaureanoNo ratings yet

- Chapter 2 AccountingDocument12 pagesChapter 2 Accountingmoon loverNo ratings yet

- FABM1 LAS 7 Adjusting-EntriesDocument12 pagesFABM1 LAS 7 Adjusting-EntriesVenus AriateNo ratings yet

- Accounting - The Recording ProcessDocument10 pagesAccounting - The Recording ProcessThuy TruongNo ratings yet

- ACCY901 Accounting Foundations For ProfessionalsDocument40 pagesACCY901 Accounting Foundations For Professionalsvenkatachalam radhakrishnan100% (1)

- Quiz No. 1: Intermediate Accounting, Part 4Document3 pagesQuiz No. 1: Intermediate Accounting, Part 4Paula BautistaNo ratings yet

- RTP June 2018 AnsDocument29 pagesRTP June 2018 AnsbinuNo ratings yet

- Quiz 1Document3 pagesQuiz 1White LeafNo ratings yet

- Financial Problems Jan 19Document17 pagesFinancial Problems Jan 19ledmabaya23No ratings yet

- Fundamentals of Accountancy Business and Management 1Document4 pagesFundamentals of Accountancy Business and Management 1Glaiza FloresNo ratings yet

- Xi-2002 RegularfDocument13 pagesXi-2002 Regularfzohaib anwarNo ratings yet

- Axia College Material: Adjusting Entries, Posting, and Preparing An Adjusted Trial BalanceDocument8 pagesAxia College Material: Adjusting Entries, Posting, and Preparing An Adjusted Trial Balancetgibson621No ratings yet

- ACCT 3001 Exams 1 and 2 All QuestionsDocument7 pagesACCT 3001 Exams 1 and 2 All QuestionsRegine VegaNo ratings yet

- 03 Posting in The General Ledger and Preparation of The Unadjusted Trial BalanceDocument6 pages03 Posting in The General Ledger and Preparation of The Unadjusted Trial BalanceLilian LagrimasNo ratings yet

- Sheet (6) Tegara English First Year Financial Accounting: GroubDocument11 pagesSheet (6) Tegara English First Year Financial Accounting: Groubmagdy kamelNo ratings yet

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- HRM Assignment 1Document4 pagesHRM Assignment 1Muhammad AwaisNo ratings yet

- Muhammad Awais (Roll No. 13669) BBA 2 Years Mor MicroDocument5 pagesMuhammad Awais (Roll No. 13669) BBA 2 Years Mor MicroMuhammad AwaisNo ratings yet

- Muhammad Awais (Roll No. 13669) BBA 2 Years Mor MicroDocument5 pagesMuhammad Awais (Roll No. 13669) BBA 2 Years Mor MicroMuhammad AwaisNo ratings yet

- 8612 Assignment No 2 PDFDocument14 pages8612 Assignment No 2 PDFMuhammad AwaisNo ratings yet

- Assignment No.2: Muhammad Awais (Sys ID: NUML-S20-11149)Document10 pagesAssignment No.2: Muhammad Awais (Sys ID: NUML-S20-11149)Muhammad AwaisNo ratings yet

- Assignemnt 1 Muhammad Awais (NUML-S20-11149)Document40 pagesAssignemnt 1 Muhammad Awais (NUML-S20-11149)Muhammad AwaisNo ratings yet

- Assignment No 1 FinalDocument13 pagesAssignment No 1 FinalMuhammad AwaisNo ratings yet

- HR Manual of Orient Paper MillsDocument104 pagesHR Manual of Orient Paper MillsMuhammad AwaisNo ratings yet

- Payslip December 2023Document1 pagePayslip December 2023rajusingh05071992No ratings yet

- CLWETAX Finals Module 5 7Document12 pagesCLWETAX Finals Module 5 7johndanielsantosNo ratings yet

- Duties of A Withholding AgentDocument2 pagesDuties of A Withholding AgentAnselmo Rodiel IV100% (1)

- We Have Received Your Premium: Rahul PahadeDocument1 pageWe Have Received Your Premium: Rahul PahaderahulpahadeNo ratings yet

- Chapter 16 NotesDocument10 pagesChapter 16 NotesDa GoatNo ratings yet

- Income Tax Statement For Financial Year 2023-24 (Assessment Year 2024-25)Document1 pageIncome Tax Statement For Financial Year 2023-24 (Assessment Year 2024-25)ikbalbahar1992No ratings yet

- Time of SupplyDocument21 pagesTime of SupplyKetan DedhaNo ratings yet

- 26ASDocument4 pages26ASAnubhav AsatiNo ratings yet

- Revision Q&ADocument5 pagesRevision Q&ADylan Rabin PereiraNo ratings yet

- ICWAI Inter Direct Tax Solved June 2011Document15 pagesICWAI Inter Direct Tax Solved June 2011rk_rkaushikNo ratings yet

- Tax Invoice #29Q72Z: Date Ref Tour Pax Gross NettDocument1 pageTax Invoice #29Q72Z: Date Ref Tour Pax Gross NettKiran PNo ratings yet

- 2316 Jan 2018 ENCS Final2Document1 page2316 Jan 2018 ENCS Final2Rafael DizonNo ratings yet

- Business TaxationDocument6 pagesBusiness TaxationMandy BloomNo ratings yet

- Individual Income Taxation Notes PDFDocument23 pagesIndividual Income Taxation Notes PDFNelson BJ OstiqueNo ratings yet

- Pre Board Examination Paper: Faculty of Business & AccountancyDocument4 pagesPre Board Examination Paper: Faculty of Business & AccountancyPuja GahatrajNo ratings yet

- Golden RamaDocument1 pageGolden RamaRaditya JuliantoroNo ratings yet

- Tata Motors: PrintDocument2 pagesTata Motors: Printprathamesh tawareNo ratings yet

- 1511256898711park Cubix Price Sheet 2 9 17 PDFDocument1 page1511256898711park Cubix Price Sheet 2 9 17 PDFManjunathNo ratings yet

- Tax On CorporationDocument2 pagesTax On CorporationMervidelleNo ratings yet

- Comparative Income Statement For The Year 17-18 & 18-19 Profit & Loss - Reliance Industries LTDDocument23 pagesComparative Income Statement For The Year 17-18 & 18-19 Profit & Loss - Reliance Industries LTDManan Suchak100% (1)

- Case 31: Maynard Company (B) : DR Ashish Varma / IMTDocument4 pagesCase 31: Maynard Company (B) : DR Ashish Varma / IMTAranhav SinghNo ratings yet

- Exercise 4.3.1Document2 pagesExercise 4.3.1Seth Jarl G. Agustin100% (1)

- Lisa Ortega Operates Ortega Riding Academy The Academy S Primar PDFDocument1 pageLisa Ortega Operates Ortega Riding Academy The Academy S Primar PDFAnbu jaromiaNo ratings yet

- Natsu Co Follows The Practice of Recording Prepaid Expenses andDocument1 pageNatsu Co Follows The Practice of Recording Prepaid Expenses andtrilocksp SinghNo ratings yet

- Income Tax 20220119Document56 pagesIncome Tax 20220119asadazhar002No ratings yet

- Residential Status DC 2023-24Document11 pagesResidential Status DC 2023-24avinashhpv7785No ratings yet

- Taxation Law Review Prelims Finals PeriodDocument118 pagesTaxation Law Review Prelims Finals Periodmarcus.pebenitojrNo ratings yet