Comprehensive Pack - Retail

Comprehensive Pack - Retail

You might also like

- Branding a Store: How To Build Successful Retail Brands In A Changing MarketplaceFrom EverandBranding a Store: How To Build Successful Retail Brands In A Changing MarketplaceRating: 3 out of 5 stars3/5 (2)

- Marketing NestoDocument9 pagesMarketing NestoMyassignmentPro VideoNo ratings yet

- AI For Analytics: Written By: Brooke LynchDocument12 pagesAI For Analytics: Written By: Brooke LynchPera PericNo ratings yet

- Porter's Five Forces and SWOT: Retail IndustryDocument38 pagesPorter's Five Forces and SWOT: Retail Industryvintosh_pNo ratings yet

- 100 Mark Project On SupermarketDocument97 pages100 Mark Project On SupermarketGaurav Mane82% (11)

- Presentation 2Document15 pagesPresentation 2hhaiderNo ratings yet

- Store Wars: The Worldwide Battle for Mindspace and Shelfspace, Online and In-storeFrom EverandStore Wars: The Worldwide Battle for Mindspace and Shelfspace, Online and In-storeNo ratings yet

- Marketing Concept - 5 Concepts of Marketing Explained With ExamplesDocument5 pagesMarketing Concept - 5 Concepts of Marketing Explained With ExamplesGirish Jadhav83% (6)

- Retail ManagementDocument40 pagesRetail ManagementAditya GowriNo ratings yet

- Overview of Retail SectorDocument10 pagesOverview of Retail SectorShahid YousufNo ratings yet

- RetailingDocument53 pagesRetailingvipinNo ratings yet

- I-1 - The Future of Retail - Sachin Bansal - Ver1.1Document24 pagesI-1 - The Future of Retail - Sachin Bansal - Ver1.1rockachi1782No ratings yet

- RetailDocument45 pagesRetailvaibhav1987100% (1)

- New Delhi Institute of ManagementDocument40 pagesNew Delhi Institute of ManagementAmit SaxenaNo ratings yet

- Chapter 2: Types of Retailers: HDCS 3303 - Section 12711 Introduction To Merchandising Evangeline CaridasDocument45 pagesChapter 2: Types of Retailers: HDCS 3303 - Section 12711 Introduction To Merchandising Evangeline Caridasvenkat_guezzNo ratings yet

- Retailing Module 1Document47 pagesRetailing Module 1VIRAJ MODINo ratings yet

- Shopping Mall - Project 2Document100 pagesShopping Mall - Project 2Awadhesh YadavNo ratings yet

- "Retail" and "Retail Stores" Redirect Here. For The Comic Strip by Norm FeutiDocument5 pages"Retail" and "Retail Stores" Redirect Here. For The Comic Strip by Norm Feutipritesh105No ratings yet

- ChapterDocument44 pagesChapterKithir Sahul HameedNo ratings yet

- Title: Phoenix of Retail Sector in India and Scope of FDI in RetailDocument15 pagesTitle: Phoenix of Retail Sector in India and Scope of FDI in RetailKhushi KothariNo ratings yet

- Chapter 1-2Document11 pagesChapter 1-2Danyal RizviNo ratings yet

- RM - Pre MidsDocument239 pagesRM - Pre MidsasniNo ratings yet

- Retail MGMT 1 - MergedDocument188 pagesRetail MGMT 1 - MergedasniNo ratings yet

- Retailing:: Retail Consists of The Sale of Goods or Merchandise From A Fixed Location, Such As A DepartmentDocument12 pagesRetailing:: Retail Consists of The Sale of Goods or Merchandise From A Fixed Location, Such As A DepartmentRavi Nandan KumarNo ratings yet

- Ii History &evolution Iii Challenges Faced by FMCG Iv Swot Analysis V Products Vi Overall Working of The Sector Vii SummaryDocument20 pagesIi History &evolution Iii Challenges Faced by FMCG Iv Swot Analysis V Products Vi Overall Working of The Sector Vii SummaryradhikaNo ratings yet

- Retail Management: Unit 1Document54 pagesRetail Management: Unit 1Vijayakumar Jadhav100% (1)

- Food Retail (Biscuit Industry) : Group 6Document48 pagesFood Retail (Biscuit Industry) : Group 6Bibhas MondalNo ratings yet

- Big BazaarDocument41 pagesBig Bazaarron_mumNo ratings yet

- Retail Management Unit2 - Retail Development and Internationlization & Business ModelDocument38 pagesRetail Management Unit2 - Retail Development and Internationlization & Business ModelGautam DongaNo ratings yet

- Retail Environment - Unit 2-1Document59 pagesRetail Environment - Unit 2-1cinemaasuraNo ratings yet

- Retail: Sectoral AnalysisDocument26 pagesRetail: Sectoral AnalysisNishant SrivastavaNo ratings yet

- RelianceDocument13 pagesRelianceRishita MalaniNo ratings yet

- RM Chapter 1Document40 pagesRM Chapter 1abhisekh dasNo ratings yet

- Retail by BharathDocument12 pagesRetail by BharathVISHU.SANDYNo ratings yet

- Industry Analysis LT F-03Document22 pagesIndustry Analysis LT F-03Prashant PalNo ratings yet

- MK 0012Document75 pagesMK 0012Rohan FernandesNo ratings yet

- Fdi in Retail IndustryDocument41 pagesFdi in Retail IndustryjohnrichardjasmineNo ratings yet

- Retail Theories and Life CycleDocument29 pagesRetail Theories and Life Cycletc23No ratings yet

- Carrefour - FINALDocument7 pagesCarrefour - FINALAmritanshu MehraNo ratings yet

- Specialized Stores V/S Discount Stores: WillyzDocument20 pagesSpecialized Stores V/S Discount Stores: Willyzhimanshubhola_510No ratings yet

- Presentation On Big Bazaar: Presentation by - Gurdeep Singh - Pushpak Pandey - Shaleen Agarwal - Rohan Tandon - Richa KohliDocument40 pagesPresentation On Big Bazaar: Presentation by - Gurdeep Singh - Pushpak Pandey - Shaleen Agarwal - Rohan Tandon - Richa KohliBabu SeeworldNo ratings yet

- TYBMS SEM VI Retail Management TYBMS Marketing Unit IDocument26 pagesTYBMS SEM VI Retail Management TYBMS Marketing Unit IDhiraj PalNo ratings yet

- Unit - 1: Retailing, Retail Format and Growth & ChallengesDocument41 pagesUnit - 1: Retailing, Retail Format and Growth & ChallengesNancy50% (2)

- Retail Management: Ivb02RemDocument84 pagesRetail Management: Ivb02RemAbrar MansuriNo ratings yet

- SMU A S: Retail MarketingDocument27 pagesSMU A S: Retail MarketingGYANENDRA KUMAR MISHRANo ratings yet

- 5.TCS Retail Doc2003Document44 pages5.TCS Retail Doc2003ankitkapoor333No ratings yet

- Retailing Notes - MidsDocument30 pagesRetailing Notes - Midsfilza kaziNo ratings yet

- Rapidly Expanding Garment Retail SectorDocument10 pagesRapidly Expanding Garment Retail SectorzswxwszNo ratings yet

- A Study On Consumer Buying Behaviour in Malls: Created By: Bhavesh Somanathan Rakesh Darji Tushar PatelDocument44 pagesA Study On Consumer Buying Behaviour in Malls: Created By: Bhavesh Somanathan Rakesh Darji Tushar PatelBhavesh SomanathanNo ratings yet

- Global Retailing Scenario: & Its FutureDocument38 pagesGlobal Retailing Scenario: & Its FutureAnkit MehtaNo ratings yet

- Final Report 2Document84 pagesFinal Report 2antecgaming010No ratings yet

- 14 RetailingDocument8 pages14 RetailingSarthak GuptaNo ratings yet

- What Is Retail?Document15 pagesWhat Is Retail?Nishit ShauryaNo ratings yet

- Retail Trade IndustryDocument25 pagesRetail Trade IndustryJerry de LeonNo ratings yet

- Types of Intermediaries - L3Document55 pagesTypes of Intermediaries - L3vijaikumarankamNo ratings yet

- Group 5 Section A Phase 1Document15 pagesGroup 5 Section A Phase 1drsravya reddyNo ratings yet

- Types of RetailersDocument46 pagesTypes of RetailersDr. Neelam Shrivastava (SAP Professor)0% (1)

- CHP 1-Intro RM PDFDocument23 pagesCHP 1-Intro RM PDFKalpita DhuriNo ratings yet

- FMCG 2020 - The Game ChangerDocument24 pagesFMCG 2020 - The Game Changerpallavipant_22No ratings yet

- The Online Marketplace Advantage: Sell More, Scale Faster, and Create a World-Class Digital Customer ExperienceFrom EverandThe Online Marketplace Advantage: Sell More, Scale Faster, and Create a World-Class Digital Customer ExperienceNo ratings yet

- The Competitive Power of the Product Lifecycle: Revolutionise the way you sell your productsFrom EverandThe Competitive Power of the Product Lifecycle: Revolutionise the way you sell your productsNo ratings yet

- Gilles Lipovetsky: Selected Summaries: SELECTED SUMMARIESFrom EverandGilles Lipovetsky: Selected Summaries: SELECTED SUMMARIESNo ratings yet

- Comprehensive Pack - RMGDocument83 pagesComprehensive Pack - RMGAmit RajNo ratings yet

- Siebel Systems Case Analysis: Group 10 - Section BDocument7 pagesSiebel Systems Case Analysis: Group 10 - Section BAmit RajNo ratings yet

- Snapshot-Retail IndustryDocument5 pagesSnapshot-Retail IndustryAmit RajNo ratings yet

- Comprehensive Pack - MicrofinanceDocument73 pagesComprehensive Pack - MicrofinanceAmit RajNo ratings yet

- Comprehensive Pack - HotelsDocument68 pagesComprehensive Pack - HotelsAmit RajNo ratings yet

- Snapshot Pack - HotelsDocument10 pagesSnapshot Pack - HotelsAmit RajNo ratings yet

- Power Pack - HotelsDocument37 pagesPower Pack - HotelsAmit RajNo ratings yet

- 4) Session 4 PDFDocument40 pages4) Session 4 PDFAmit RajNo ratings yet

- 2) Session 2 PDFDocument21 pages2) Session 2 PDFAmit RajNo ratings yet

- Power Pack - IT ServicesDocument34 pagesPower Pack - IT ServicesAmit RajNo ratings yet

- Power Pack - Household AppliancesDocument30 pagesPower Pack - Household AppliancesAmit RajNo ratings yet

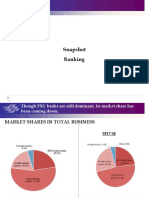

- Snapshot BankingDocument7 pagesSnapshot BankingAmit RajNo ratings yet

- Comprehensive Pack - Household AppliancesDocument66 pagesComprehensive Pack - Household AppliancesAmit RajNo ratings yet

- Tehcnology Entrepreneurship (ENT600) Case Study: ShiseidoDocument26 pagesTehcnology Entrepreneurship (ENT600) Case Study: ShiseidoShafiqahFazyaziqahNo ratings yet

- Group Assigment MarketingDocument5 pagesGroup Assigment MarketingNor Nadiah Najwa Binti AzizanNo ratings yet

- Impulse Buying Li 2023Document21 pagesImpulse Buying Li 2023Catur Panjalu PutraNo ratings yet

- Moneygram Case StudyDocument4 pagesMoneygram Case StudyPaolo TolentinoNo ratings yet

- Business DiagnosisDocument6 pagesBusiness DiagnosisEyob Light WorkuNo ratings yet

- SHS Entrep - Module 1BDocument34 pagesSHS Entrep - Module 1BJeydibi Mharjom100% (1)

- STRAMA CHP 13Document56 pagesSTRAMA CHP 13Tiffany Shane GantuangcoNo ratings yet

- 268 Simran MeenaDocument73 pages268 Simran Meenapassportdecember2024No ratings yet

- Somnath Banerjee: Sales & Business Development - Channel ManagementDocument2 pagesSomnath Banerjee: Sales & Business Development - Channel ManagementDivya NinaweNo ratings yet

- City Branding - VanGelder, AllanDocument36 pagesCity Branding - VanGelder, AllanAurora UabcNo ratings yet

- The Relationship of Service Quality On Consumer Satisfaction in Shipyard IndustryDocument11 pagesThe Relationship of Service Quality On Consumer Satisfaction in Shipyard IndustryDhanaNo ratings yet

- Class Activity - Bus685Document7 pagesClass Activity - Bus685bonna1234567890No ratings yet

- The Media Evolution, The Digital RevolutionDocument4 pagesThe Media Evolution, The Digital RevolutionKabir Ariff SultanNo ratings yet

- Avendus Pharmaworld Jan 11 PDFDocument19 pagesAvendus Pharmaworld Jan 11 PDFaguptagNo ratings yet

- 贝恩杯初赛历年题目Document3 pages贝恩杯初赛历年题目sylviashang21No ratings yet

- Professional Remodeler - September 2015 USADocument76 pagesProfessional Remodeler - September 2015 USAMarius NicolaeNo ratings yet

- Presentation: Group Members AreDocument34 pagesPresentation: Group Members AreMuhammad Farooq SiddiquiNo ratings yet

- ReinventingtheOrganization A5Document6 pagesReinventingtheOrganization A5Randi MakmurNo ratings yet

- 8 A Study On Sales Promotion Activities of Reliance RetaillDocument4 pages8 A Study On Sales Promotion Activities of Reliance RetaillShubhangi KesharwaniNo ratings yet

- Ey Alm Pacesetter Research Enterprise Risk Management 2020 2021 FullDocument51 pagesEy Alm Pacesetter Research Enterprise Risk Management 2020 2021 FullMeet PanchalNo ratings yet

- Process Domain 2 - ProcurementDocument56 pagesProcess Domain 2 - ProcurementpaulaNo ratings yet

- Project Stepup - Prospectus (v.2) (ICA Circle-Ups)Document76 pagesProject Stepup - Prospectus (v.2) (ICA Circle-Ups)devesh moreNo ratings yet

- Chap 3 LmsDocument36 pagesChap 3 LmsLAN BUI THI YNo ratings yet

- 3Document2 pages3askkNo ratings yet

- Ethics in Business Functional AreasDocument5 pagesEthics in Business Functional AreasFouzia imz0% (2)

- Final Exam-MKTG 3208: Multiple Choice QuestionsDocument11 pagesFinal Exam-MKTG 3208: Multiple Choice QuestionsLady BirdNo ratings yet

- AD-Times CapgeminiDocument12 pagesAD-Times CapgeminiAkash GoyalNo ratings yet

Download as pdf or txt

You might also like

- Branding a Store: How To Build Successful Retail Brands In A Changing MarketplaceFrom EverandBranding a Store: How To Build Successful Retail Brands In A Changing MarketplaceRating: 3 out of 5 stars3/5 (2)

- Marketing NestoDocument9 pagesMarketing NestoMyassignmentPro VideoNo ratings yet

- AI For Analytics: Written By: Brooke LynchDocument12 pagesAI For Analytics: Written By: Brooke LynchPera PericNo ratings yet

- Porter's Five Forces and SWOT: Retail IndustryDocument38 pagesPorter's Five Forces and SWOT: Retail Industryvintosh_pNo ratings yet

- 100 Mark Project On SupermarketDocument97 pages100 Mark Project On SupermarketGaurav Mane82% (11)

- Presentation 2Document15 pagesPresentation 2hhaiderNo ratings yet

- Store Wars: The Worldwide Battle for Mindspace and Shelfspace, Online and In-storeFrom EverandStore Wars: The Worldwide Battle for Mindspace and Shelfspace, Online and In-storeNo ratings yet

- Marketing Concept - 5 Concepts of Marketing Explained With ExamplesDocument5 pagesMarketing Concept - 5 Concepts of Marketing Explained With ExamplesGirish Jadhav83% (6)

- Retail ManagementDocument40 pagesRetail ManagementAditya GowriNo ratings yet

- Overview of Retail SectorDocument10 pagesOverview of Retail SectorShahid YousufNo ratings yet

- RetailingDocument53 pagesRetailingvipinNo ratings yet

- I-1 - The Future of Retail - Sachin Bansal - Ver1.1Document24 pagesI-1 - The Future of Retail - Sachin Bansal - Ver1.1rockachi1782No ratings yet

- RetailDocument45 pagesRetailvaibhav1987100% (1)

- New Delhi Institute of ManagementDocument40 pagesNew Delhi Institute of ManagementAmit SaxenaNo ratings yet

- Chapter 2: Types of Retailers: HDCS 3303 - Section 12711 Introduction To Merchandising Evangeline CaridasDocument45 pagesChapter 2: Types of Retailers: HDCS 3303 - Section 12711 Introduction To Merchandising Evangeline Caridasvenkat_guezzNo ratings yet

- Retailing Module 1Document47 pagesRetailing Module 1VIRAJ MODINo ratings yet

- Shopping Mall - Project 2Document100 pagesShopping Mall - Project 2Awadhesh YadavNo ratings yet

- "Retail" and "Retail Stores" Redirect Here. For The Comic Strip by Norm FeutiDocument5 pages"Retail" and "Retail Stores" Redirect Here. For The Comic Strip by Norm Feutipritesh105No ratings yet

- ChapterDocument44 pagesChapterKithir Sahul HameedNo ratings yet

- Title: Phoenix of Retail Sector in India and Scope of FDI in RetailDocument15 pagesTitle: Phoenix of Retail Sector in India and Scope of FDI in RetailKhushi KothariNo ratings yet

- Chapter 1-2Document11 pagesChapter 1-2Danyal RizviNo ratings yet

- RM - Pre MidsDocument239 pagesRM - Pre MidsasniNo ratings yet

- Retail MGMT 1 - MergedDocument188 pagesRetail MGMT 1 - MergedasniNo ratings yet

- Retailing:: Retail Consists of The Sale of Goods or Merchandise From A Fixed Location, Such As A DepartmentDocument12 pagesRetailing:: Retail Consists of The Sale of Goods or Merchandise From A Fixed Location, Such As A DepartmentRavi Nandan KumarNo ratings yet

- Ii History &evolution Iii Challenges Faced by FMCG Iv Swot Analysis V Products Vi Overall Working of The Sector Vii SummaryDocument20 pagesIi History &evolution Iii Challenges Faced by FMCG Iv Swot Analysis V Products Vi Overall Working of The Sector Vii SummaryradhikaNo ratings yet

- Retail Management: Unit 1Document54 pagesRetail Management: Unit 1Vijayakumar Jadhav100% (1)

- Food Retail (Biscuit Industry) : Group 6Document48 pagesFood Retail (Biscuit Industry) : Group 6Bibhas MondalNo ratings yet

- Big BazaarDocument41 pagesBig Bazaarron_mumNo ratings yet

- Retail Management Unit2 - Retail Development and Internationlization & Business ModelDocument38 pagesRetail Management Unit2 - Retail Development and Internationlization & Business ModelGautam DongaNo ratings yet

- Retail Environment - Unit 2-1Document59 pagesRetail Environment - Unit 2-1cinemaasuraNo ratings yet

- Retail: Sectoral AnalysisDocument26 pagesRetail: Sectoral AnalysisNishant SrivastavaNo ratings yet

- RelianceDocument13 pagesRelianceRishita MalaniNo ratings yet

- RM Chapter 1Document40 pagesRM Chapter 1abhisekh dasNo ratings yet

- Retail by BharathDocument12 pagesRetail by BharathVISHU.SANDYNo ratings yet

- Industry Analysis LT F-03Document22 pagesIndustry Analysis LT F-03Prashant PalNo ratings yet

- MK 0012Document75 pagesMK 0012Rohan FernandesNo ratings yet

- Fdi in Retail IndustryDocument41 pagesFdi in Retail IndustryjohnrichardjasmineNo ratings yet

- Retail Theories and Life CycleDocument29 pagesRetail Theories and Life Cycletc23No ratings yet

- Carrefour - FINALDocument7 pagesCarrefour - FINALAmritanshu MehraNo ratings yet

- Specialized Stores V/S Discount Stores: WillyzDocument20 pagesSpecialized Stores V/S Discount Stores: Willyzhimanshubhola_510No ratings yet

- Presentation On Big Bazaar: Presentation by - Gurdeep Singh - Pushpak Pandey - Shaleen Agarwal - Rohan Tandon - Richa KohliDocument40 pagesPresentation On Big Bazaar: Presentation by - Gurdeep Singh - Pushpak Pandey - Shaleen Agarwal - Rohan Tandon - Richa KohliBabu SeeworldNo ratings yet

- TYBMS SEM VI Retail Management TYBMS Marketing Unit IDocument26 pagesTYBMS SEM VI Retail Management TYBMS Marketing Unit IDhiraj PalNo ratings yet

- Unit - 1: Retailing, Retail Format and Growth & ChallengesDocument41 pagesUnit - 1: Retailing, Retail Format and Growth & ChallengesNancy50% (2)

- Retail Management: Ivb02RemDocument84 pagesRetail Management: Ivb02RemAbrar MansuriNo ratings yet

- SMU A S: Retail MarketingDocument27 pagesSMU A S: Retail MarketingGYANENDRA KUMAR MISHRANo ratings yet

- 5.TCS Retail Doc2003Document44 pages5.TCS Retail Doc2003ankitkapoor333No ratings yet

- Retailing Notes - MidsDocument30 pagesRetailing Notes - Midsfilza kaziNo ratings yet

- Rapidly Expanding Garment Retail SectorDocument10 pagesRapidly Expanding Garment Retail SectorzswxwszNo ratings yet

- A Study On Consumer Buying Behaviour in Malls: Created By: Bhavesh Somanathan Rakesh Darji Tushar PatelDocument44 pagesA Study On Consumer Buying Behaviour in Malls: Created By: Bhavesh Somanathan Rakesh Darji Tushar PatelBhavesh SomanathanNo ratings yet

- Global Retailing Scenario: & Its FutureDocument38 pagesGlobal Retailing Scenario: & Its FutureAnkit MehtaNo ratings yet

- Final Report 2Document84 pagesFinal Report 2antecgaming010No ratings yet

- 14 RetailingDocument8 pages14 RetailingSarthak GuptaNo ratings yet

- What Is Retail?Document15 pagesWhat Is Retail?Nishit ShauryaNo ratings yet

- Retail Trade IndustryDocument25 pagesRetail Trade IndustryJerry de LeonNo ratings yet

- Types of Intermediaries - L3Document55 pagesTypes of Intermediaries - L3vijaikumarankamNo ratings yet

- Group 5 Section A Phase 1Document15 pagesGroup 5 Section A Phase 1drsravya reddyNo ratings yet

- Types of RetailersDocument46 pagesTypes of RetailersDr. Neelam Shrivastava (SAP Professor)0% (1)

- CHP 1-Intro RM PDFDocument23 pagesCHP 1-Intro RM PDFKalpita DhuriNo ratings yet

- FMCG 2020 - The Game ChangerDocument24 pagesFMCG 2020 - The Game Changerpallavipant_22No ratings yet

- The Online Marketplace Advantage: Sell More, Scale Faster, and Create a World-Class Digital Customer ExperienceFrom EverandThe Online Marketplace Advantage: Sell More, Scale Faster, and Create a World-Class Digital Customer ExperienceNo ratings yet

- The Competitive Power of the Product Lifecycle: Revolutionise the way you sell your productsFrom EverandThe Competitive Power of the Product Lifecycle: Revolutionise the way you sell your productsNo ratings yet

- Gilles Lipovetsky: Selected Summaries: SELECTED SUMMARIESFrom EverandGilles Lipovetsky: Selected Summaries: SELECTED SUMMARIESNo ratings yet

- Comprehensive Pack - RMGDocument83 pagesComprehensive Pack - RMGAmit RajNo ratings yet

- Siebel Systems Case Analysis: Group 10 - Section BDocument7 pagesSiebel Systems Case Analysis: Group 10 - Section BAmit RajNo ratings yet

- Snapshot-Retail IndustryDocument5 pagesSnapshot-Retail IndustryAmit RajNo ratings yet

- Comprehensive Pack - MicrofinanceDocument73 pagesComprehensive Pack - MicrofinanceAmit RajNo ratings yet

- Comprehensive Pack - HotelsDocument68 pagesComprehensive Pack - HotelsAmit RajNo ratings yet

- Snapshot Pack - HotelsDocument10 pagesSnapshot Pack - HotelsAmit RajNo ratings yet

- Power Pack - HotelsDocument37 pagesPower Pack - HotelsAmit RajNo ratings yet

- 4) Session 4 PDFDocument40 pages4) Session 4 PDFAmit RajNo ratings yet

- 2) Session 2 PDFDocument21 pages2) Session 2 PDFAmit RajNo ratings yet

- Power Pack - IT ServicesDocument34 pagesPower Pack - IT ServicesAmit RajNo ratings yet

- Power Pack - Household AppliancesDocument30 pagesPower Pack - Household AppliancesAmit RajNo ratings yet

- Snapshot BankingDocument7 pagesSnapshot BankingAmit RajNo ratings yet

- Comprehensive Pack - Household AppliancesDocument66 pagesComprehensive Pack - Household AppliancesAmit RajNo ratings yet

- Tehcnology Entrepreneurship (ENT600) Case Study: ShiseidoDocument26 pagesTehcnology Entrepreneurship (ENT600) Case Study: ShiseidoShafiqahFazyaziqahNo ratings yet

- Group Assigment MarketingDocument5 pagesGroup Assigment MarketingNor Nadiah Najwa Binti AzizanNo ratings yet

- Impulse Buying Li 2023Document21 pagesImpulse Buying Li 2023Catur Panjalu PutraNo ratings yet

- Moneygram Case StudyDocument4 pagesMoneygram Case StudyPaolo TolentinoNo ratings yet

- Business DiagnosisDocument6 pagesBusiness DiagnosisEyob Light WorkuNo ratings yet

- SHS Entrep - Module 1BDocument34 pagesSHS Entrep - Module 1BJeydibi Mharjom100% (1)

- STRAMA CHP 13Document56 pagesSTRAMA CHP 13Tiffany Shane GantuangcoNo ratings yet

- 268 Simran MeenaDocument73 pages268 Simran Meenapassportdecember2024No ratings yet

- Somnath Banerjee: Sales & Business Development - Channel ManagementDocument2 pagesSomnath Banerjee: Sales & Business Development - Channel ManagementDivya NinaweNo ratings yet

- City Branding - VanGelder, AllanDocument36 pagesCity Branding - VanGelder, AllanAurora UabcNo ratings yet

- The Relationship of Service Quality On Consumer Satisfaction in Shipyard IndustryDocument11 pagesThe Relationship of Service Quality On Consumer Satisfaction in Shipyard IndustryDhanaNo ratings yet

- Class Activity - Bus685Document7 pagesClass Activity - Bus685bonna1234567890No ratings yet

- The Media Evolution, The Digital RevolutionDocument4 pagesThe Media Evolution, The Digital RevolutionKabir Ariff SultanNo ratings yet

- Avendus Pharmaworld Jan 11 PDFDocument19 pagesAvendus Pharmaworld Jan 11 PDFaguptagNo ratings yet

- 贝恩杯初赛历年题目Document3 pages贝恩杯初赛历年题目sylviashang21No ratings yet

- Professional Remodeler - September 2015 USADocument76 pagesProfessional Remodeler - September 2015 USAMarius NicolaeNo ratings yet

- Presentation: Group Members AreDocument34 pagesPresentation: Group Members AreMuhammad Farooq SiddiquiNo ratings yet

- ReinventingtheOrganization A5Document6 pagesReinventingtheOrganization A5Randi MakmurNo ratings yet

- 8 A Study On Sales Promotion Activities of Reliance RetaillDocument4 pages8 A Study On Sales Promotion Activities of Reliance RetaillShubhangi KesharwaniNo ratings yet

- Ey Alm Pacesetter Research Enterprise Risk Management 2020 2021 FullDocument51 pagesEy Alm Pacesetter Research Enterprise Risk Management 2020 2021 FullMeet PanchalNo ratings yet

- Process Domain 2 - ProcurementDocument56 pagesProcess Domain 2 - ProcurementpaulaNo ratings yet

- Project Stepup - Prospectus (v.2) (ICA Circle-Ups)Document76 pagesProject Stepup - Prospectus (v.2) (ICA Circle-Ups)devesh moreNo ratings yet

- Chap 3 LmsDocument36 pagesChap 3 LmsLAN BUI THI YNo ratings yet

- 3Document2 pages3askkNo ratings yet

- Ethics in Business Functional AreasDocument5 pagesEthics in Business Functional AreasFouzia imz0% (2)

- Final Exam-MKTG 3208: Multiple Choice QuestionsDocument11 pagesFinal Exam-MKTG 3208: Multiple Choice QuestionsLady BirdNo ratings yet

- AD-Times CapgeminiDocument12 pagesAD-Times CapgeminiAkash GoyalNo ratings yet