Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- FIN304 Assignment 1 (5th FIN C) Group 3Document24 pagesFIN304 Assignment 1 (5th FIN C) Group 3Rajesh MongerNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 240 Bob StatementDocument4 pages240 Bob Statementdebroy8282No ratings yet

- La Nota de Divulgación Acerca de Las Políticas de Contabilidad Está en La Página 85 y El Detalle Del Inventario Está en La Página 109.Document67 pagesLa Nota de Divulgación Acerca de Las Políticas de Contabilidad Está en La Página 85 y El Detalle Del Inventario Está en La Página 109.Rodrigo Lopez GarciaNo ratings yet

- Disposicion de Activos No CorrientesDocument5 pagesDisposicion de Activos No CorrientesRodrigo Lopez GarciaNo ratings yet

- Financial Accounting: Courseware Help and SupportDocument2 pagesFinancial Accounting: Courseware Help and SupportRodrigo Lopez GarciaNo ratings yet

- Vocabulary 1 PDFDocument1 pageVocabulary 1 PDFRodrigo Lopez GarciaNo ratings yet

- FFA-F3.X Financial Accounting - Grading Policy Grade RangeDocument3 pagesFFA-F3.X Financial Accounting - Grading Policy Grade RangeRodrigo Lopez GarciaNo ratings yet

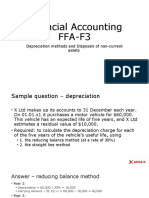

- Financial Accounting FFA-F3: Depreciation Methods and Disposals of Non-Current AssetsDocument7 pagesFinancial Accounting FFA-F3: Depreciation Methods and Disposals of Non-Current AssetsRodrigo Lopez GarciaNo ratings yet

- Money Market SolutionDocument6 pagesMoney Market SolutionAnkit Poudel100% (2)

- AFAR-01 (Partnership Formation & Operations)Document6 pagesAFAR-01 (Partnership Formation & Operations)Maricris Alilin100% (1)

- Montgo - EPGP 14A - ClassDocument3 pagesMontgo - EPGP 14A - ClasswantANo ratings yet

- UPSA 2019 Tutorial Questions Fs WITH ANSWERSDocument14 pagesUPSA 2019 Tutorial Questions Fs WITH ANSWERSLaud ListowellNo ratings yet

- MTP (TVM Questikon)Document11 pagesMTP (TVM Questikon)prashanttiwari155282No ratings yet

- Lecture Note-Cash and Cash EquivalentDocument14 pagesLecture Note-Cash and Cash EquivalentLeneNo ratings yet

- Contoh ResitDocument1 pageContoh ResitshahNo ratings yet

- Business CombinationDocument24 pagesBusiness CombinationArifinNo ratings yet

- Interbank GIRO (IBG) : Transaction FeesDocument4 pagesInterbank GIRO (IBG) : Transaction FeesHafizAceNo ratings yet

- Security DB by LinkedinDocument2 pagesSecurity DB by LinkedinNazim KhanNo ratings yet

- Ict 2 Finals Quiz 1Document2 pagesIct 2 Finals Quiz 1Dmzjmb SaadNo ratings yet

- Charles Schwab Stock - Consider SCHW For Market-Beating Returns - Seeking AlphaDocument3 pagesCharles Schwab Stock - Consider SCHW For Market-Beating Returns - Seeking AlphateppeiNo ratings yet

- Risk & InsuranceDocument8 pagesRisk & InsuranceAlan100% (2)

- Chapter 3. Solution Exercises Income StatementDocument13 pagesChapter 3. Solution Exercises Income StatementHECTOR ORTEGANo ratings yet

- Advanced Accounting 13th Edition Hoyle Solutions ManualDocument25 pagesAdvanced Accounting 13th Edition Hoyle Solutions ManualErikKeithnwmp100% (56)

- December Dhamaka - Dec 23 IC ContestDocument23 pagesDecember Dhamaka - Dec 23 IC ContestAnant PandeyNo ratings yet

- NILEX Listing Brochure-ArDocument10 pagesNILEX Listing Brochure-Arبكرة جاىNo ratings yet

- CFA Level II - Equity - Equity Valuation Applications and ProcessesDocument10 pagesCFA Level II - Equity - Equity Valuation Applications and ProcessesQuy Cuong BuiNo ratings yet

- Negotiated Dealing System (NDS) :: Submitted by Roll NODocument12 pagesNegotiated Dealing System (NDS) :: Submitted by Roll NOKartik VariyaNo ratings yet

- Summer Internship Report of CGC College, Punjab Technical UniversityDocument51 pagesSummer Internship Report of CGC College, Punjab Technical UniversityDumy AccountNo ratings yet

- Nanna MESCOM Payment Receipt-2110405DMCL2787-1949541Document1 pageNanna MESCOM Payment Receipt-2110405DMCL2787-1949541Lijesh MathewNo ratings yet

- Financial Summary Model Answer v03Document1 pageFinancial Summary Model Answer v03Ayesha RehmanNo ratings yet

- HDFCDocument345 pagesHDFCPrakhar AwasthiNo ratings yet

- India: Asia-Pacific'S Next Mutual Funds Giant: Markets and Securities Services - 1Document10 pagesIndia: Asia-Pacific'S Next Mutual Funds Giant: Markets and Securities Services - 1EdifyNo ratings yet

- Debt Funding in India, Nishith Desai Associates, Available At, Last Visited On 8 April, 2019 External Commercial Borrowings & Trade Credits, Available at Last Visited On 9 April 2019Document3 pagesDebt Funding in India, Nishith Desai Associates, Available At, Last Visited On 8 April, 2019 External Commercial Borrowings & Trade Credits, Available at Last Visited On 9 April 2019Kunwar AbhudayNo ratings yet

- Cash Flow Forecasting TemplateDocument41 pagesCash Flow Forecasting Templatejose miguel baezNo ratings yet

- Unit2.Project IvanRivera6 MT481 Financial MarketsDocument4 pagesUnit2.Project IvanRivera6 MT481 Financial MarketsRashiNo ratings yet

- Pradhan Mantri Jeevan Jyoti Bima Yojana: Consent-Cum-Declaration Form For Office UseDocument7 pagesPradhan Mantri Jeevan Jyoti Bima Yojana: Consent-Cum-Declaration Form For Office UseChanduNo ratings yet