Download as docx, pdf, or txt

You might also like

- Update To Doc 8335 - : Manual of Procedures For Operations Inspection, Certification and Continued SurveillanceDocument10 pagesUpdate To Doc 8335 - : Manual of Procedures For Operations Inspection, Certification and Continued SurveillanceAbdul Aziz Abdul HalimNo ratings yet

- Abm Applied Economics Reading MaterialsDocument5 pagesAbm Applied Economics Reading MaterialsNardsdel Rivera100% (1)

- Economic Analysis For Business, Managerial Economics, MBA EconomicsDocument215 pagesEconomic Analysis For Business, Managerial Economics, MBA EconomicsSaravananSrvn90% (10)

- Suyash Kulkarni Section - D Roll No.-2017143137: Assignment 1Document11 pagesSuyash Kulkarni Section - D Roll No.-2017143137: Assignment 1Suyash KulkarniNo ratings yet

- Module 1 Introduction To Economic DevtDocument35 pagesModule 1 Introduction To Economic Devtur.luna82997No ratings yet

- Module 1 Week 1&2Document28 pagesModule 1 Week 1&2Love JcwNo ratings yet

- MODULE 1-Introduction in EconomicsDocument17 pagesMODULE 1-Introduction in EconomicsJohnmar Dela CruzNo ratings yet

- Basic MicroeconomicsDocument219 pagesBasic Microeconomicsloc dinhNo ratings yet

- SHS ModulesDocument13 pagesSHS ModulesJecca JamonNo ratings yet

- Applied Economics - Module 1 - 3rd QuarterDocument4 pagesApplied Economics - Module 1 - 3rd QuarterMs.Muriel MorongNo ratings yet

- Chap 1Document7 pagesChap 1Annie DuolingoNo ratings yet

- Introduction To EconomicsDocument37 pagesIntroduction To Economicsnunyu bidnesNo ratings yet

- Applied Economics Module 1Document13 pagesApplied Economics Module 1CESTINA, KIM LIANNE, B.No ratings yet

- EconomicsDocument3 pagesEconomicsStar ShineNo ratings yet

- Inbound 5117552937865489854Document5 pagesInbound 5117552937865489854beronaclarkNo ratings yet

- Economics Assingment HiteshDocument20 pagesEconomics Assingment Hiteshhitesh kashyapNo ratings yet

- What Is Economics.s02Document75 pagesWhat Is Economics.s02GenNo ratings yet

- Merged File of All Units EDITEDDocument170 pagesMerged File of All Units EDITEDvinit tandel100% (1)

- APPLIED-ECONOMICS Mod12Qtr1Document79 pagesAPPLIED-ECONOMICS Mod12Qtr1Julie CabusaoNo ratings yet

- Economics and Significance PDFDocument8 pagesEconomics and Significance PDFJeswaanth GogulaNo ratings yet

- Micro EconomicsDocument128 pagesMicro EconomicsfeisalNo ratings yet

- Me Chapter OneDocument6 pagesMe Chapter OneSherefedin AdemNo ratings yet

- Applied EconomicsDocument184 pagesApplied EconomicsMichael ZinampanNo ratings yet

- Econ 2Document4 pagesEcon 2Joy LibeeNo ratings yet

- Unit 1: Introduction To Economics: Page 1 of 7Document7 pagesUnit 1: Introduction To Economics: Page 1 of 7Efeninge MarthaNo ratings yet

- APPLIED ECON Unit 1 Basic ConceptsDocument22 pagesAPPLIED ECON Unit 1 Basic ConceptsAJ DatuNo ratings yet

- Central Concepts of EconomicsDocument21 pagesCentral Concepts of EconomicsREHANRAJNo ratings yet

- Micro-Economics - IDocument147 pagesMicro-Economics - IWamek NuraNo ratings yet

- Applied Economics-Chapter 1Document57 pagesApplied Economics-Chapter 1Trixie Ruvi AlmiñeNo ratings yet

- ECON Week1Document7 pagesECON Week1ocsapwaketsNo ratings yet

- Microeconomics IDocument160 pagesMicroeconomics Iselomonbrhane17171No ratings yet

- Chapter 123456 MASDocument19 pagesChapter 123456 MASabygaelreyesNo ratings yet

- Applied Econ - Chapter 1Document7 pagesApplied Econ - Chapter 1MattJigenAnoreNo ratings yet

- Introduction To Economicsnotesweek1 2Document16 pagesIntroduction To Economicsnotesweek1 2Ras EurhylNo ratings yet

- Lesson 1 - Introduction To Applied EconomicsDocument9 pagesLesson 1 - Introduction To Applied EconomicsLaila RodaviaNo ratings yet

- Module in MacroeconomicsDocument70 pagesModule in MacroeconomicsElizabeth HeartfeltNo ratings yet

- Benedicto, Kim Gabriel M. ECO 101 Bsmt32 - B1 Os Split Sir Delos Reyes Quiz #1 1. What Is Economics?Document5 pagesBenedicto, Kim Gabriel M. ECO 101 Bsmt32 - B1 Os Split Sir Delos Reyes Quiz #1 1. What Is Economics?Kim GabrielNo ratings yet

- Lesson 1 Nature of Economics PDFDocument13 pagesLesson 1 Nature of Economics PDFJabez Tyron CalzaNo ratings yet

- APPLIED ECONOMICS Lesson 1 Introduction To Economics 2Document35 pagesAPPLIED ECONOMICS Lesson 1 Introduction To Economics 2Aleah Miles Vista EspañolaNo ratings yet

- Applied Economics: Absolute Scarcity Is When A Good Is Scarce Compared To Its Demand. For Example, Coconuts AreDocument4 pagesApplied Economics: Absolute Scarcity Is When A Good Is Scarce Compared To Its Demand. For Example, Coconuts AreRoma MalasarteNo ratings yet

- Ssed 11 Module 1 Lesson 1Document11 pagesSsed 11 Module 1 Lesson 1Shiela IgnacioNo ratings yet

- A Module in Bac 101 (Basic Microeconomics) Module 1, Week 1 To 2 Fundamental Concepts in Economics Learning OutcomesDocument23 pagesA Module in Bac 101 (Basic Microeconomics) Module 1, Week 1 To 2 Fundamental Concepts in Economics Learning OutcomesSabrina ChangNo ratings yet

- Principles of EconomicsDocument20 pagesPrinciples of EconomicsEmilia JacobNo ratings yet

- Module 1 - MicroeconomicsDocument10 pagesModule 1 - Microeconomicsrhea crystal regenciaNo ratings yet

- (Sales) Economics NotesDocument68 pages(Sales) Economics NotesFerdy (Ferdy)No ratings yet

- Module 1 The Nature and Process of Economics Demand Supply and EquilibriumDocument11 pagesModule 1 The Nature and Process of Economics Demand Supply and EquilibriumIrish Jane PalasinNo ratings yet

- What Is EconomicsDocument4 pagesWhat Is EconomicsDaniyal AhmedNo ratings yet

- The Concept of ScarcityDocument9 pagesThe Concept of ScarcityJayson LlamasaresNo ratings yet

- Material No. 1Document18 pagesMaterial No. 1rhbqztqbzyNo ratings yet

- Module 2-APPLIED ECONDocument5 pagesModule 2-APPLIED ECONMae EnteroNo ratings yet

- Applied EconomicsDocument13 pagesApplied EconomicsFriedrich MarivelesNo ratings yet

- EcoDev Module 1 PDFDocument10 pagesEcoDev Module 1 PDFJoseph Prado FernandezNo ratings yet

- Applied Economics Module 1Document6 pagesApplied Economics Module 1HUMSS 11-BNo ratings yet

- AppEcon Module1Document10 pagesAppEcon Module1Ian Eldrick Dela CruzNo ratings yet

- Microeconomics: Worktext BookDocument13 pagesMicroeconomics: Worktext BookLanie CarcidoNo ratings yet

- Slide 01-Economic ConceptsDocument103 pagesSlide 01-Economic Conceptscomputer masterNo ratings yet

- An Inquiry Into The Nature and Causes of The Wealth of NationsDocument16 pagesAn Inquiry Into The Nature and Causes of The Wealth of NationsNahrozNo ratings yet

- Basic Economics With LRTDocument4 pagesBasic Economics With LRTtrix catorceNo ratings yet

- Economics NotesDocument58 pagesEconomics NotesMuhammad Akmal HossainNo ratings yet

- Ae ReviewerDocument8 pagesAe ReviewerChristine Mae SorianoNo ratings yet

- Laroche Landscaping Has Collected The Following Data For The December PDFDocument1 pageLaroche Landscaping Has Collected The Following Data For The December PDFhassan taimourNo ratings yet

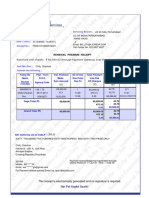

- Received With Thanks ' 60,569.62 Through Payment Gateway Over The Internet FromDocument1 pageReceived With Thanks ' 60,569.62 Through Payment Gateway Over The Internet FromCSK100% (1)

- Demek Resume Fifth SemesterDocument2 pagesDemek Resume Fifth Semesterapi-317605141No ratings yet

- Iibf Jaiib ApplicationDocument4 pagesIibf Jaiib Applicationreachtorajan700No ratings yet

- Ictk MCQ PDFDocument24 pagesIctk MCQ PDFExtra Account100% (1)

- Automatic Plaster MachineDocument4 pagesAutomatic Plaster MachineIJMTST-Online JournalNo ratings yet

- Globalization L7Document42 pagesGlobalization L7Cherrie Chu SiuwanNo ratings yet

- Philately GlossaryDocument10 pagesPhilately GlossaryJoaoNo ratings yet

- Introduction To Temple ArtDocument31 pagesIntroduction To Temple ArtaakashNo ratings yet

- Final ProjectDocument5 pagesFinal ProjectAkshayNo ratings yet

- Item of Work: D (JCM) SectionDocument23 pagesItem of Work: D (JCM) SectionDevendra KumarNo ratings yet

- IET Automotive Cyber-Security TLR LR PDFDocument16 pagesIET Automotive Cyber-Security TLR LR PDFPanneerselvam KolandaivelNo ratings yet

- ContractDocument3 pagesContractrodelyn ubalubaoNo ratings yet

- Axis Bank - WikipediaDocument68 pagesAxis Bank - Wikipediahnair_3No ratings yet

- 2 Jurnal Jenis RacunDocument17 pages2 Jurnal Jenis RacunRifky NovanNo ratings yet

- Jesus of Levi and JudahDocument40 pagesJesus of Levi and JudahAntony Hylton100% (1)

- The Tragical History of Doctor Faustus by Christopher MarloweDocument8 pagesThe Tragical History of Doctor Faustus by Christopher MarloweJOSUE BARRIOSNo ratings yet

- Introduction e CommerceDocument84 pagesIntroduction e CommerceMohd FirdausNo ratings yet

- DOH-HHRDB Healthcare Workers (Physicians)Document41 pagesDOH-HHRDB Healthcare Workers (Physicians)VERA FilesNo ratings yet

- Kofax Installation GuideDocument258 pagesKofax Installation GuideCharles ObodoNo ratings yet

- Micro ReviewDocument134 pagesMicro ReviewNiki NourNo ratings yet

- Presentation On NAFTADocument11 pagesPresentation On NAFTAagrawalkrunalNo ratings yet

- Reading Response - Poverty and Policy by Paul SlackDocument3 pagesReading Response - Poverty and Policy by Paul Slackaibrahi2No ratings yet

- UntitledDocument2 pagesUntitledapi-1549565660% (1)

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument16 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancevedhasai198No ratings yet

- CVDocument1 pageCVarvindkNo ratings yet

- Model Answer - Final Revision SEC.1 - Term 2Document5 pagesModel Answer - Final Revision SEC.1 - Term 2Mahmoud IbrahimNo ratings yet

- Krattworks Drone AI RescueDocument13 pagesKrattworks Drone AI RescueSaeful AnwarNo ratings yet

- Resume ExampleDocument1 pageResume ExampleK I0NNo ratings yet