Download as docx, pdf, or txt

You might also like

- Dialogues With The Masters Amarananda Bhairavan: Hysical TherapyDocument19 pagesDialogues With The Masters Amarananda Bhairavan: Hysical Therapysjuluris100% (1)

- Teacher Migrants SelectionDocument116 pagesTeacher Migrants Selectionrakesh tickooNo ratings yet

- Social WorkDocument12 pagesSocial WorkAshutosh SharmaNo ratings yet

- Customer DetailsDocument138 pagesCustomer Detailspawandubey933% (3)

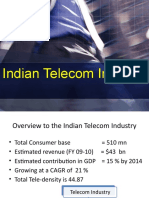

- Wapcos Esanchar August 22Document17 pagesWapcos Esanchar August 22gauravNo ratings yet

- LP 10 - 160 kVA - BrochureDocument2 pagesLP 10 - 160 kVA - BrochureSaheer AANo ratings yet

- Hyderabad BrochureDocument6 pagesHyderabad BrochureDausori SatishNo ratings yet

- Edelweiss Annual Report 2017Document220 pagesEdelweiss Annual Report 2017Kunj ShahNo ratings yet

- PES PresentationDocument67 pagesPES PresentationJustinNo ratings yet

- Map India Class 12 2019-20Document21 pagesMap India Class 12 2019-20Shivam JainNo ratings yet

- Child Sex Ratio - India and Odisha: Data Source: Census 2011Document12 pagesChild Sex Ratio - India and Odisha: Data Source: Census 2011Amol DhanvijNo ratings yet

- Channel Partners and DistributorsDocument1 pageChannel Partners and Distributorsmana builderNo ratings yet

- Opportunities in Food Processing Sector in IndiaDocument24 pagesOpportunities in Food Processing Sector in IndiaPrakash KcNo ratings yet

- Opportunitiesin Cold Chain Sectorin IndiaDocument20 pagesOpportunitiesin Cold Chain Sectorin IndiaStanley TimothyNo ratings yet

- Monsoon in India-16 Jul 2021Document5 pagesMonsoon in India-16 Jul 2021Diksha ShrinetNo ratings yet

- India Compressors MarketDocument19 pagesIndia Compressors MarketRajshekar LokamNo ratings yet

- India Map: 0 260 520 780 1,040 130 KilometersDocument1 pageIndia Map: 0 260 520 780 1,040 130 KilometersFrank JohnNo ratings yet

- About MaharashtraDocument20 pagesAbout MaharashtraPrasad RahateNo ratings yet

- Tiger ReservesDocument12 pagesTiger ReservesdvsdguNo ratings yet

- Kalhans Rajput ExtentsDocument1 pageKalhans Rajput ExtentsVaibhav Kumar Singh kalhans thakur kshatriyasNo ratings yet

- India Election Prayer Book New 2023 - EngDocument20 pagesIndia Election Prayer Book New 2023 - EngSolomonraj GorripatiNo ratings yet

- Geographic Heat Map (India) : State/UT Name DataDocument1 pageGeographic Heat Map (India) : State/UT Name DataShubham GuptaNo ratings yet

- Mines in IndiaDocument2 pagesMines in Indiadharan511No ratings yet

- Ayushman PDFDocument8 pagesAyushman PDFRajeshNo ratings yet

- Pashtun, Pathan: Peoples of South AsiaDocument1 pagePashtun, Pathan: Peoples of South AsiaFarid Ullah KhanNo ratings yet

- GarodaDocument1 pageGarodadev_84No ratings yet

- Map Meena TribesDocument1 pageMap Meena Tribeskaushal meenaNo ratings yet

- Indian RiversDocument3 pagesIndian RivershimanshuNo ratings yet

- Indian Rivers: Please Visit: For More DetailsDocument3 pagesIndian Rivers: Please Visit: For More DetailsGhanshyam SharmaNo ratings yet

- Investor Presentaion - Q1 FY21 - DAA - 202009 - 1Document31 pagesInvestor Presentaion - Q1 FY21 - DAA - 202009 - 1rustedchainsawNo ratings yet

- Investor Presentaion - March 2018Document30 pagesInvestor Presentaion - March 2018rustedchainsawNo ratings yet

- Indian States - Capitals, Chief Ministers & Governors 2019 - BankExamsTodayDocument5 pagesIndian States - Capitals, Chief Ministers & Governors 2019 - BankExamsTodayShubham AryaNo ratings yet

- Regional RuralDocument3 pagesRegional RuralheartlyhiteshNo ratings yet

- Regional RuralDocument3 pagesRegional RuralheartlyhiteshNo ratings yet

- Foodgrains Sector in IndiaDocument4 pagesFoodgrains Sector in IndiaAbhiNo ratings yet

- PMKVY Assessment ReportDocument400 pagesPMKVY Assessment ReportAjay KaushikNo ratings yet

- Investor - Presentaion - Q4 FY21Document34 pagesInvestor - Presentaion - Q4 FY21rustedchainsawNo ratings yet

- India FreeZones AtlasDocument74 pagesIndia FreeZones Atlasappao vidyasagarNo ratings yet

- Investor Presentaion Q3 FY22 DAA 202202 1 (04-04)Document1 pageInvestor Presentaion Q3 FY22 DAA 202202 1 (04-04)PowerNo ratings yet

- IndexDocument8 pagesIndexGopi MecheriNo ratings yet

- Bharat Petroleum Corporation LimitedDocument15 pagesBharat Petroleum Corporation LimitedFavourite CartoonsNo ratings yet

- New Microsoft Power Point PresentationDocument27 pagesNew Microsoft Power Point PresentationRahul MittalNo ratings yet

- List of Indian Cities On Rivers - Wikipedia, The Free EncyclopediaDocument2 pagesList of Indian Cities On Rivers - Wikipedia, The Free EncyclopediaAbhishek KumarNo ratings yet

- Uttar-Pradesh PMKK ListDocument170 pagesUttar-Pradesh PMKK ListMANOJNo ratings yet

- Wurth Anchor Technology Catalogue 2019Document71 pagesWurth Anchor Technology Catalogue 2019nunnaraoNo ratings yet

- River Map of India River System in India Himalayan Rivers, Peninsular RiversDocument1 pageRiver Map of India River System in India Himalayan Rivers, Peninsular Riversankitmalan32No ratings yet

- Indian Cities On The Banks of Rivers: City River StateDocument2 pagesIndian Cities On The Banks of Rivers: City River Statepodila lavanya lavanyaNo ratings yet

- States and Union Territories of India - WikipediaDocument20 pagesStates and Union Territories of India - WikipediaArjunNo ratings yet

- ABDUL - Resume - 927Document3 pagesABDUL - Resume - 927vishalb9892No ratings yet

- Geography Part 9 Soils in IndiaDocument3 pagesGeography Part 9 Soils in IndiaServant of ALLAHNo ratings yet

- Geography Class 10 Chapter 4 ChartDocument3 pagesGeography Class 10 Chapter 4 ChartAshutosh Karn100% (1)

- Eco Adventure SportsDocument7 pagesEco Adventure Sports034isha galiawalaNo ratings yet

- Investor Presentaion - Dec 2019 - DAA - 202002 - 1Document30 pagesInvestor Presentaion - Dec 2019 - DAA - 202002 - 1rustedchainsawNo ratings yet

- Corporate Deck - Innovsource - BKT Tires LimitedDocument24 pagesCorporate Deck - Innovsource - BKT Tires LimitedRhishikeshNo ratings yet

- GBC List For WebsiteDocument5 pagesGBC List For WebsiteAyush OjhaNo ratings yet

- Cities MineralsDocument2 pagesCities Mineralspushpa121yajaNo ratings yet

- Wayside Amenity: Development Opportunity Across IndiaDocument18 pagesWayside Amenity: Development Opportunity Across IndiasravanNo ratings yet

- Hypo WorldDocument6 pagesHypo WorldEthan HuntNo ratings yet

- Kalai - B15Document45 pagesKalai - B15KALAINo ratings yet

- States & UT Along With CapDocument9 pagesStates & UT Along With CapAkshat ChoudharyNo ratings yet

- Dear Esteemed Academic Partner, Greetings From TCS!Document4 pagesDear Esteemed Academic Partner, Greetings From TCS!Md Mohioddin MohiNo ratings yet

- India MapDocument1 pageIndia MapMo KhanNo ratings yet

- Capability Deck - BSH Household AppliancesDocument29 pagesCapability Deck - BSH Household Appliancesakshy28aprNo ratings yet

- 13 Days 6000 KMs: A photographic journey through beautiful landscapes of Himachal Pradesh and Jammu & Kashmir, IndiaFrom Everand13 Days 6000 KMs: A photographic journey through beautiful landscapes of Himachal Pradesh and Jammu & Kashmir, IndiaNo ratings yet

- New Doc 2020-02-10 11.58.34 - 20200210121011 - 03 PDFDocument1 pageNew Doc 2020-02-10 11.58.34 - 20200210121011 - 03 PDFVikhyat SharmaNo ratings yet

- Infrastructure in India: A Vast Land of Construction OpportunityDocument27 pagesInfrastructure in India: A Vast Land of Construction OpportunityVikhyat SharmaNo ratings yet

- Infrastructure Infographic June 2020Document1 pageInfrastructure Infographic June 2020Vikhyat SharmaNo ratings yet

- Real Estate Infographic June 2020Document2 pagesReal Estate Infographic June 2020Vikhyat SharmaNo ratings yet

- Infrastructure IndiaDocument35 pagesInfrastructure IndiaVikhyat SharmaNo ratings yet

- List of Cos in AhmedabadDocument559 pagesList of Cos in AhmedabadVikhyat SharmaNo ratings yet

- Unit - 1 Changing Trends and Career in Physical EducatinDocument20 pagesUnit - 1 Changing Trends and Career in Physical EducatinPeyush NeneNo ratings yet

- A059 Shivaji Hindu King in Islamic IndiaDocument8 pagesA059 Shivaji Hindu King in Islamic IndiaAlok pathakNo ratings yet

- Interpreting Vimshottari DasaDocument2 pagesInterpreting Vimshottari DasaANANTHPADMANABHANNo ratings yet

- Ananda K. Coomaraswamy - The-Dance-of-SivaDocument13 pagesAnanda K. Coomaraswamy - The-Dance-of-SivaRoger MayenNo ratings yet

- Communal Riots in HyderabadDocument72 pagesCommunal Riots in Hyderabadabhas123No ratings yet

- First Year ReportDocument294 pagesFirst Year Reportakshatraj875No ratings yet

- Allpreferences PGD PrefnoDocument94 pagesAllpreferences PGD PrefnognansekarNo ratings yet

- Kishoresatsangparichay EngDocument122 pagesKishoresatsangparichay Engapi-287811173No ratings yet

- DestDocument67 pagesDestnidhi tripathiNo ratings yet

- Jain Religion Explained by Tantrik Astrologer Vastuvid Sanjay Jain of Bikaner RajasthanDocument3 pagesJain Religion Explained by Tantrik Astrologer Vastuvid Sanjay Jain of Bikaner Rajasthanjain.tk7825No ratings yet

- JOSHI Aspects of Buddhism in Indian History PDFDocument26 pagesJOSHI Aspects of Buddhism in Indian History PDFadikarmikaNo ratings yet

- Indian BeautyDocument11 pagesIndian Beautyadithya4rajNo ratings yet

- SL No. NH No. Nomenclature Length in KM Carriageway Width Single Lane Intermediate Lane Two Lane Four LaneDocument25 pagesSL No. NH No. Nomenclature Length in KM Carriageway Width Single Lane Intermediate Lane Two Lane Four LanerajaanwarNo ratings yet

- Rahasya Thrayam III-Moorthi RahasyamDocument7 pagesRahasya Thrayam III-Moorthi RahasyamSuresh DNo ratings yet

- Paper 07Document207 pagesPaper 07MAZID TTNo ratings yet

- Cult of The Black SunDocument5 pagesCult of The Black SunFull Equip50% (4)

- Surya AshtakamDocument2 pagesSurya AshtakamAnonymous 5mSMeP2jNo ratings yet

- Animal Sacrifice and Sanatana Dharma - by Vedic SocietyDocument51 pagesAnimal Sacrifice and Sanatana Dharma - by Vedic Societyanil shuklaNo ratings yet

- Cap Ma Film SDocument10 pagesCap Ma Film SMd IstiakNo ratings yet

- West BengalDocument4 pagesWest BengalnirajvirendrasinghNo ratings yet

- Defence Colony DineshDocument2 pagesDefence Colony DineshBibhash singh rana0% (2)

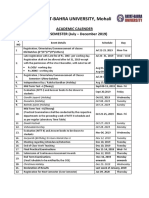

- Academic Calender July - Dec 2019Document2 pagesAcademic Calender July - Dec 2019Nikhil ManhasNo ratings yet

- Navamsa Chart PDFDocument19 pagesNavamsa Chart PDFhappyrag100% (4)

- Andhra Pradesh: India Fourth Largest State by Area Fifth Largest by Population Hyderabad Telugu Urdu English Tamil HindiDocument30 pagesAndhra Pradesh: India Fourth Largest State by Area Fifth Largest by Population Hyderabad Telugu Urdu English Tamil HindiAnshul PorwalNo ratings yet

- Lakshmi Puja Vidhi: 1. Dhyana (ध्यान)Document10 pagesLakshmi Puja Vidhi: 1. Dhyana (ध्यान)Yogeshwar Sharma 219467No ratings yet

- Cbi Vs Sri Krishan Bahadur On 27 November, 2015 PDFDocument75 pagesCbi Vs Sri Krishan Bahadur On 27 November, 2015 PDFsubhash IngoleNo ratings yet