Download as pdf or txt

You might also like

- CSR Sample ProposalDocument19 pagesCSR Sample Proposalrichard200000020% (5)

- Advanced Financial Management PDFDocument205 pagesAdvanced Financial Management PDFaponojecy100% (5)

- OCR GCSE 9-1 Business: My Revision GuideDocument113 pagesOCR GCSE 9-1 Business: My Revision GuideAnya Johal100% (1)

- Burke y Logsdon (1996)Document8 pagesBurke y Logsdon (1996)Johan Sebastian Chaves GarciaNo ratings yet

- The Stakeholder Strategy: Profiting from Collaborative Business RelationshipsFrom EverandThe Stakeholder Strategy: Profiting from Collaborative Business RelationshipsNo ratings yet

- Printable Conference Programme, Paris July 2012Document15 pagesPrintable Conference Programme, Paris July 2012tprugNo ratings yet

- Corporate Social Responsibility of TESCODocument22 pagesCorporate Social Responsibility of TESCOPanigrahi AbhaNo ratings yet

- Business Models and Corporate Social ResponsibilityDocument36 pagesBusiness Models and Corporate Social ResponsibilityKatalin Kokai SzaboNo ratings yet

- Corporate Social Responsibility in PrivaDocument15 pagesCorporate Social Responsibility in PrivaElianaNo ratings yet

- Moser Ar13 A-Broader-Perspective-on-CSRDocument10 pagesMoser Ar13 A-Broader-Perspective-on-CSRAnnisa AuliaNo ratings yet

- Broader and DeeperDocument11 pagesBroader and DeeperViswa Chandra ReddyNo ratings yet

- CSR in Banking Sector: International Journal of Economics, Commerce and ManagementDocument22 pagesCSR in Banking Sector: International Journal of Economics, Commerce and ManagementmustafaNo ratings yet

- Corporate Social Responsibility and Financialperformance Relationship A Review Ofmeasurement ApproachesDocument19 pagesCorporate Social Responsibility and Financialperformance Relationship A Review Ofmeasurement ApproachesdessyNo ratings yet

- Research Proposal - CSR - The Voice of The StakeholderDocument13 pagesResearch Proposal - CSR - The Voice of The StakeholderAmany HamzaNo ratings yet

- This Content Downloaded From 83.253.247.117 On Fri, 28 Apr 2023 21:13:05 +00:00Document11 pagesThis Content Downloaded From 83.253.247.117 On Fri, 28 Apr 2023 21:13:05 +00:00ahmed sharkasNo ratings yet

- 2010 Russo Perrini Investigating Stakeholder Theory and Social Capital CSR in Large Firms and SmesDocument15 pages2010 Russo Perrini Investigating Stakeholder Theory and Social Capital CSR in Large Firms and SmesAlexandre RipamontiNo ratings yet

- Victoria University of Wellington, New Zealand: Judy.A.Brown@vuw - Ac.nzDocument29 pagesVictoria University of Wellington, New Zealand: Judy.A.Brown@vuw - Ac.nzshumon2657No ratings yet

- Beurden and Gossling 2009 JBE The Worth of Values A Literature Review On The Relation Between Corporate Social and Financial PerformanceDocument18 pagesBeurden and Gossling 2009 JBE The Worth of Values A Literature Review On The Relation Between Corporate Social and Financial PerformanceKwaku Ohene-Asare100% (1)

- International Journal of Accounting: Suresh Radhakrishnan, Albert Tsang, Rubing LiuDocument21 pagesInternational Journal of Accounting: Suresh Radhakrishnan, Albert Tsang, Rubing LiuHutama Putra JuniriansyahNo ratings yet

- CSR 2Document7 pagesCSR 2Shravan RamsurrunNo ratings yet

- Brand Equity and CSR Final DraftDocument30 pagesBrand Equity and CSR Final Drafthussein elmahdyNo ratings yet

- Recognizing The Effective Factors in Social Responsibility Promotion of Saipa Automobile-Manufacturing GroupDocument5 pagesRecognizing The Effective Factors in Social Responsibility Promotion of Saipa Automobile-Manufacturing GroupInternational Organization of Scientific Research (IOSR)No ratings yet

- 382754.soukopova Duskova Bakic-TomicDocument5 pages382754.soukopova Duskova Bakic-TomicErra PeñafloridaNo ratings yet

- Chapter 4 Driversfor CSR11Document40 pagesChapter 4 Driversfor CSR11krish bhatiaNo ratings yet

- SA-1035 Chapter 1 and 2-1Document16 pagesSA-1035 Chapter 1 and 2-1Muhammad Hamza NaseemNo ratings yet

- Corporate Governance, Business Ethics and CSR CourseworkDocument17 pagesCorporate Governance, Business Ethics and CSR CourseworkoladoyinsolaNo ratings yet

- Galant and Cade Z 2017 ErpDocument19 pagesGalant and Cade Z 2017 ErpHarshika VermaNo ratings yet

- Economic Perspectives On CSRDocument34 pagesEconomic Perspectives On CSRPinkz JanabanNo ratings yet

- Academy of Management The Academy of Management ReviewDocument12 pagesAcademy of Management The Academy of Management ReviewJip van AmerongenNo ratings yet

- The Impact of Recession On The Implementation of Corporate Social Responsibility in CompaniesDocument16 pagesThe Impact of Recession On The Implementation of Corporate Social Responsibility in CompaniesKhan Musarrat BegumNo ratings yet

- Corporate Social ResponsibilityDocument15 pagesCorporate Social ResponsibilityTimNo ratings yet

- Communication of Corporate Social Responsibility: A Study of The Views of Management Teams in Large CompaniesDocument16 pagesCommunication of Corporate Social Responsibility: A Study of The Views of Management Teams in Large CompaniesGurmani ChadhaNo ratings yet

- CF Conceptual Paper PerasadDocument17 pagesCF Conceptual Paper PerasadRajendiraperasad ManiamNo ratings yet

- CSR and Firm PerformanceDocument14 pagesCSR and Firm PerformanceRicky RomuloNo ratings yet

- CSR Research Paper TopicsDocument8 pagesCSR Research Paper Topicsd0f1lowufam3100% (1)

- CSR Disclosure and Equity Market Liquidity FactsDocument4 pagesCSR Disclosure and Equity Market Liquidity Factshiruni nishadiNo ratings yet

- CSR IntroductionDocument7 pagesCSR IntroductionBG GoelNo ratings yet

- A Review of Esg and CSR - GillanDocument51 pagesA Review of Esg and CSR - GillanXuân ĐỗNo ratings yet

- Corporate Social ResponsibilityDocument13 pagesCorporate Social ResponsibilityabdullahNo ratings yet

- PHD Thesis Lucely VargasDocument259 pagesPHD Thesis Lucely VargasBelur Baxi100% (1)

- An Institution of Corporate Social Responsibility (CSR) in Multi-National Corporations (MNCS) : Form and ImplicationsDocument44 pagesAn Institution of Corporate Social Responsibility (CSR) in Multi-National Corporations (MNCS) : Form and ImplicationsJhovany Amastal MolinaNo ratings yet

- Information About Social Corporate ResponsibilitiesDocument21 pagesInformation About Social Corporate ResponsibilitiesMohammed Al-hashediNo ratings yet

- Does Corporate Social Responsibility Affect The Cost of Capital?Document63 pagesDoes Corporate Social Responsibility Affect The Cost of Capital?dimpi singhNo ratings yet

- Brooks 2017Document43 pagesBrooks 2017khusnul hayatiNo ratings yet

- AbstractDocument11 pagesAbstractJagruti AcharyaNo ratings yet

- Souza & Vasconcellos, 2011Document15 pagesSouza & Vasconcellos, 2011Chantal DeLarentaNo ratings yet

- Brown and FraserDocument16 pagesBrown and FraserAlvyonitha Ratu RambaNo ratings yet

- Anna Witek PreprintDocument29 pagesAnna Witek PreprintdittoNo ratings yet

- Corporate Social Responsibility and TourismDocument16 pagesCorporate Social Responsibility and TourismFirasNo ratings yet

- Components Theories and The Business Case For Corporate Social ResponsibilityDocument29 pagesComponents Theories and The Business Case For Corporate Social Responsibilityhuneet SinghNo ratings yet

- 23E54000 A Review of The Theories of Corporate Social ResponsibilityDocument21 pages23E54000 A Review of The Theories of Corporate Social ResponsibilityRicardo MiguéisNo ratings yet

- Oxfordhb 9780199211593 e 004Document37 pagesOxfordhb 9780199211593 e 004Andra ModreanuNo ratings yet

- Corporate Social Responsibility: Moving Beyond Investment Towards Measuring OutcomesDocument9 pagesCorporate Social Responsibility: Moving Beyond Investment Towards Measuring Outcomesዝምታ ተሻለNo ratings yet

- Assignment 2 (Set 2)Document7 pagesAssignment 2 (Set 2)sashaNo ratings yet

- 5.0 Predicting The Future Approach of Corporate Finance: The New Financial ParadigmDocument5 pages5.0 Predicting The Future Approach of Corporate Finance: The New Financial ParadigmsyaidatulNo ratings yet

- Sustainability 12 06398Document20 pagesSustainability 12 06398Hien Quoc VuNo ratings yet

- Thesis IUDocument19 pagesThesis IUsneha sNo ratings yet

- Empirical Literature Review On Corporate Social ResponsibilityDocument9 pagesEmpirical Literature Review On Corporate Social Responsibilityc5t9rejgNo ratings yet

- Patrycjagulaklipka,+018 KsiezakDocument16 pagesPatrycjagulaklipka,+018 KsiezakSheriff SheriffNo ratings yet

- CSR in HotelDocument24 pagesCSR in HotelJordan CabaguingNo ratings yet

- ORDER 3530 fILEDocument29 pagesORDER 3530 fILEMuhammad WaqasNo ratings yet

- Sustainability in Business: A Financial Economics AnalysisFrom EverandSustainability in Business: A Financial Economics AnalysisNo ratings yet

- Disclosure on sustainable development, CSR environmental disclosure and greater value recognized to the company by usersFrom EverandDisclosure on sustainable development, CSR environmental disclosure and greater value recognized to the company by usersNo ratings yet

- 05 Land Use PlanningDocument55 pages05 Land Use PlanningArch. Jan EchiverriNo ratings yet

- Consumer Behavior Towards Credit Card in IndiaDocument14 pagesConsumer Behavior Towards Credit Card in IndiaAyush KNo ratings yet

- Rubco Organizational Study....Document62 pagesRubco Organizational Study....Bensy MariamNo ratings yet

- What Is Contract FarmingDocument8 pagesWhat Is Contract FarmingSri HimajaNo ratings yet

- 4A. HDFC July2019 EstatementDocument9 pages4A. HDFC July2019 EstatementNanu PatelNo ratings yet

- Reflection ReportDocument2 pagesReflection ReportMateo MascardoNo ratings yet

- Financial Statement Analysis of Kohat Cement Company LimitedDocument67 pagesFinancial Statement Analysis of Kohat Cement Company LimitedSaif Ali Khan BalouchNo ratings yet

- Advertisement Impact On ConsumerDocument6 pagesAdvertisement Impact On ConsumerChandan Kumar Singh33% (3)

- Smith-Dikolli - 1995 - Customer Profitability Analysis - An ABC ApproachDocument6 pagesSmith-Dikolli - 1995 - Customer Profitability Analysis - An ABC Approachsyahirshafiq23No ratings yet

- Internship ReportDocument12 pagesInternship Reportapi-463578527No ratings yet

- Glacier Fish AnnouncementDocument2 pagesGlacier Fish AnnouncementDeckbossNo ratings yet

- Spice House Business PlanDocument9 pagesSpice House Business Plananon_22054856No ratings yet

- MWG CEO Bai Thuyet Trinh FINAL BAN TIENG ANHDocument21 pagesMWG CEO Bai Thuyet Trinh FINAL BAN TIENG ANHRandyNo ratings yet

- PRIA FAR - 016 Share-Based Payments (PFRS 2) Notes and SolutionDocument4 pagesPRIA FAR - 016 Share-Based Payments (PFRS 2) Notes and SolutionEnrique Hills RiveraNo ratings yet

- VRIN - VRIO Analysis of FedExDocument9 pagesVRIN - VRIO Analysis of FedExnona nada damanikNo ratings yet

- Cfo AgendaDocument7 pagesCfo AgendaMOORTHY.KENo ratings yet

- Unit 2-1Document39 pagesUnit 2-1LOOPY GAMINGNo ratings yet

- Actc Vex Robotics Donation Letter 2013-14Document2 pagesActc Vex Robotics Donation Letter 2013-14api-98204538No ratings yet

- What Is EconometricsDocument6 pagesWhat Is Econometricsmirika3shirin50% (2)

- BBM 462 Nairobi and Mombasa CAT 1.Document6 pagesBBM 462 Nairobi and Mombasa CAT 1.BENSON CHANGAWANo ratings yet

- Financial ManagementDocument40 pagesFinancial ManagementDennis Esik MaligayaNo ratings yet

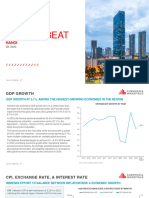

- Vietnam 2023q4 CW Market Beat Hanoi - en CombinedDocument36 pagesVietnam 2023q4 CW Market Beat Hanoi - en CombinedVu Ha NguyenNo ratings yet

- Back Start UpDocument11 pagesBack Start UpekaNo ratings yet

- MKT AssDocument2 pagesMKT AssAmir KashroNo ratings yet

- CCAPM EPP 2017 Final SlidesDocument52 pagesCCAPM EPP 2017 Final SlidesEbenezerNo ratings yet

- Chapter 3 Evaluating A Company S External Environment: Basic QuestionsDocument2 pagesChapter 3 Evaluating A Company S External Environment: Basic QuestionsAlma CoronadoNo ratings yet