Download as pdf or txt

You might also like

- SIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2024 Edition)From EverandSIE Exam Practice Question Workbook: Seven Full-Length Practice Exams (2024 Edition)Rating: 5 out of 5 stars5/5 (1)

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2024 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2024 Edition)No ratings yet

- Liabilities - QuizDocument7 pagesLiabilities - Quizkarenmae intangNo ratings yet

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Managerial Economics II - Demand & SupplyDocument35 pagesManagerial Economics II - Demand & SupplyNikhil PathakNo ratings yet

- Sem - 3 Advanced Corporate Accounting - 1 MCQ Accounting Standards (As) /lease AccountingDocument11 pagesSem - 3 Advanced Corporate Accounting - 1 MCQ Accounting Standards (As) /lease Accountinglol67% (3)

- Amex STMTDocument1 pageAmex STMTMark GalantyNo ratings yet

- Issue of Debentures (H.W)Document8 pagesIssue of Debentures (H.W)krisshlohia5No ratings yet

- Attachments - Rainbow RowellDocument29 pagesAttachments - Rainbow RowellAlvin Yerc0% (1)

- DebenturesDocument3 pagesDebenturesprintcopyxerox printcopyxeroxNo ratings yet

- Xii Mcqs CH - 10 Issue of DebenturesDocument4 pagesXii Mcqs CH - 10 Issue of DebenturesJoanna GarciaNo ratings yet

- Second Semester 2020 Second Year University of Assuit Faculty of Commerce English Program " Corporation" "Test Bank"Document10 pagesSecond Semester 2020 Second Year University of Assuit Faculty of Commerce English Program " Corporation" "Test Bank"Magdy KamelNo ratings yet

- 153b First Grading ExamDocument7 pages153b First Grading ExamJungie Mablay WalacNo ratings yet

- 3 Sem-Corp Acc 2019 QBDocument11 pages3 Sem-Corp Acc 2019 QBDynamic RefrigerationsNo ratings yet

- 7Document14 pages7obadfaisal24No ratings yet

- 2Document14 pages2MARIANo ratings yet

- Class Xii CH 7 MCQ AccountancyDocument16 pagesClass Xii CH 7 MCQ AccountancyhanaNo ratings yet

- (D) The Liability Is Payable To A Specifically Identified PayeeDocument13 pages(D) The Liability Is Payable To A Specifically Identified PayeeAngela Luz de LimaNo ratings yet

- Issue of DebenturesDocument39 pagesIssue of Debenturesyashwanth86No ratings yet

- SFA Solved Question Bank As Per July 2022Document19 pagesSFA Solved Question Bank As Per July 2022Abhijat MittalNo ratings yet

- Quiz Ak2Document23 pagesQuiz Ak2Andhika YogaraksaNo ratings yet

- QuizDocument7 pagesQuizNina ReyesNo ratings yet

- Chapter 5Document13 pagesChapter 5phan hàNo ratings yet

- Mid-Term Examination Financial Accounting II Duration:90mnDocument3 pagesMid-Term Examination Financial Accounting II Duration:90mnDavin HornNo ratings yet

- Corporate Accounting MCQDocument10 pagesCorporate Accounting MCQKumareshg GctkumareshNo ratings yet

- Off-Balance Sheet Financing & Financial AnalysisDocument10 pagesOff-Balance Sheet Financing & Financial AnalysisEvan AzizNo ratings yet

- Jaiib Sample QuestionsDocument4 pagesJaiib Sample Questionskubpyg100% (1)

- Chapter-2 Issue of Debentures BY: G Arun Kumar Mcom Mba Net Asst Professor in Commerce GDC Men SrikakulamDocument39 pagesChapter-2 Issue of Debentures BY: G Arun Kumar Mcom Mba Net Asst Professor in Commerce GDC Men SrikakulamgeddadaarunNo ratings yet

- MCQ - Part 01 Students - Intermediate Accounting IIDocument6 pagesMCQ - Part 01 Students - Intermediate Accounting IIAbdulaziz FaisalNo ratings yet

- ACTG 4 Modules 1 3 PRELIMS Multiple Choice Theories 1 100Document15 pagesACTG 4 Modules 1 3 PRELIMS Multiple Choice Theories 1 100Palomo, Kyla GabrielleNo ratings yet

- Chapter 4 and 5.Document7 pagesChapter 4 and 5.cumar maxamuud samatarNo ratings yet

- Securities or Financial Assets Sample PaperDocument19 pagesSecurities or Financial Assets Sample PaperShreyas IndurkarNo ratings yet

- Quiz Pension SHEDocument8 pagesQuiz Pension SHEErine ContranoNo ratings yet

- Financial Accounting V Question Bank: UnderwriterDocument5 pagesFinancial Accounting V Question Bank: UnderwriterMayuri More-KadamNo ratings yet

- II Sem. - Financial AccountingDocument16 pagesII Sem. - Financial Accountingakhterparveen50896No ratings yet

- Test Your Progress BookDocument14 pagesTest Your Progress BookarunapecNo ratings yet

- Chapter 7 Bond MarketsDocument15 pagesChapter 7 Bond MarketsDianne BallonNo ratings yet

- CH 9Document43 pagesCH 9anjo hosmerNo ratings yet

- REDEMPTION OF SHARES & DEBENTURES MCQsDocument7 pagesREDEMPTION OF SHARES & DEBENTURES MCQsChetan StoresNo ratings yet

- Financial Markets and Institutions Test Bank (051 060)Document10 pagesFinancial Markets and Institutions Test Bank (051 060)Thị Ba PhạmNo ratings yet

- To Print 1Document15 pagesTo Print 1Scrunchies AvenueNo ratings yet

- UntitledDocument20 pagesUntitledPatience AkpanNo ratings yet

- EXAM - IA2 ReviewerDocument17 pagesEXAM - IA2 ReviewerMohammad Raffe GuroNo ratings yet

- Acctg Integ 3b Prelim ExamDocument6 pagesAcctg Integ 3b Prelim ExamKathrine Gayle BautistaNo ratings yet

- Colegio de San Juan de Letran: NAME - SECTIONDocument9 pagesColegio de San Juan de Letran: NAME - SECTIONmaria evangelistaNo ratings yet

- Jaiib NewDocument18 pagesJaiib NewShreyas NatialaNo ratings yet

- Current Liabilities Management: Multiple Choice QuestionsDocument24 pagesCurrent Liabilities Management: Multiple Choice QuestionsRodNo ratings yet

- Dysas Center For Cpa ReviewDocument12 pagesDysas Center For Cpa ReviewAngela Luz de LimaNo ratings yet

- Appropriate Factor(s) From The Tables Provided. Do Not Round Interest Rate Factors.)Document11 pagesAppropriate Factor(s) From The Tables Provided. Do Not Round Interest Rate Factors.)ZNo ratings yet

- CPT Sample Question PaperDocument41 pagesCPT Sample Question PaperAshraf ValappilNo ratings yet

- Finac 2Document18 pagesFinac 2annewilsonNo ratings yet

- ExamView Pro - DEBT FINANCING - TST PDFDocument15 pagesExamView Pro - DEBT FINANCING - TST PDFShannon ElizaldeNo ratings yet

- Inv PLNGDocument78 pagesInv PLNGapi-38145570% (1)

- Answers to Chapter 6Document3 pagesAnswers to Chapter 6Charisse AbordoNo ratings yet

- Exam ReviewerDocument10 pagesExam Reviewerjoseph christopher vicenteNo ratings yet

- Corp AccDocument19 pagesCorp Acckamala_kannan_22No ratings yet

- QUIZ Bonds PayableDocument7 pagesQUIZ Bonds PayableKaren GarciaNo ratings yet

- Unit 5Document9 pagesUnit 5SowmiyaNo ratings yet

- Final Term Examination. Intermediate AccountingDocument8 pagesFinal Term Examination. Intermediate AccountingOrtiz, Trisha Mae S.No ratings yet

- Lending Exam May Utech 2013 SolutionsDocument12 pagesLending Exam May Utech 2013 SolutionsparkcesiaNo ratings yet

- FPQP Practice Question Workbook: 1,000 Comprehensive Practice Questions (2024 Edition)From EverandFPQP Practice Question Workbook: 1,000 Comprehensive Practice Questions (2024 Edition)No ratings yet

- Private Debt: Yield, Safety and the Emergence of Alternative LendingFrom EverandPrivate Debt: Yield, Safety and the Emergence of Alternative LendingNo ratings yet

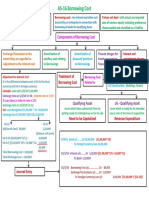

- AS 19 Leases: Bright LightsDocument7 pagesAS 19 Leases: Bright LightsRamNo ratings yet

- As 16 PDFDocument2 pagesAs 16 PDFRamNo ratings yet

- Materials For CA IPCCDocument5 pagesMaterials For CA IPCCRamNo ratings yet

- Introduction To Business: Process ManagementDocument37 pagesIntroduction To Business: Process ManagementRamNo ratings yet

- The Sirc of IcaiDocument1 pageThe Sirc of IcaiRamNo ratings yet

- Fiarlocks LTD: Invoice and Packing ListDocument1 pageFiarlocks LTD: Invoice and Packing ListDeelaka DheeraratneNo ratings yet

- Tutorial Set 2 - Key SolutionsDocument4 pagesTutorial Set 2 - Key SolutionsgregNo ratings yet

- CB & STPDocument20 pagesCB & STPPruthviraj RathoreNo ratings yet

- Municipal Council of Iloilo v. EvangelistaDocument4 pagesMunicipal Council of Iloilo v. EvangelistaJune Vincent Ferrer IIINo ratings yet

- Press Release Central U.P Gas Limited February 13, 2019: RatingsDocument5 pagesPress Release Central U.P Gas Limited February 13, 2019: RatingsSamrat DNo ratings yet

- Effects of Cash Management Practice On Financial Performance of Las Pinas Florita Trading 2Document82 pagesEffects of Cash Management Practice On Financial Performance of Las Pinas Florita Trading 2Rubie Grace ManaigNo ratings yet

- Saln CherryDocument3 pagesSaln CherryMARISSA MAMARILNo ratings yet

- M/s ABC LTD: Trading Profit & Loss Account Particulars Amount ParticularsDocument3 pagesM/s ABC LTD: Trading Profit & Loss Account Particulars Amount ParticularsSACHIN REVEKARNo ratings yet

- IRCTC IPO Description - IRCTC Limited (Indian Railway Catering and Tourism CorporationDocument6 pagesIRCTC IPO Description - IRCTC Limited (Indian Railway Catering and Tourism CorporationVinay KalraNo ratings yet

- TL9000Document18 pagesTL9000madan1981100% (1)

- TTC Package 3D2N Istanbul Bursa Winter 2023Document1 pageTTC Package 3D2N Istanbul Bursa Winter 2023Meiryza AstutiNo ratings yet

- Evaluating Opportunities in The Changing Marketing EnvironmentDocument26 pagesEvaluating Opportunities in The Changing Marketing Environmentbaongan3005No ratings yet

- Inventory Management FinalDocument32 pagesInventory Management Finaljessa rodene franciscoNo ratings yet

- PP On Fuel StationDocument20 pagesPP On Fuel StationGurraacha Abbayyaa100% (2)

- TorrentDocument8 pagesTorrentkaranbarmecha90No ratings yet

- New Resume 001Document1 pageNew Resume 001PhuongNo ratings yet

- Weekend Report: New Month, New Numbers: Gold Weekly With 3-Mo. AvgDocument7 pagesWeekend Report: New Month, New Numbers: Gold Weekly With 3-Mo. AvgSoren K. GroupNo ratings yet

- Dimla Selene S Assignment On Aggregate PlanningDocument3 pagesDimla Selene S Assignment On Aggregate PlanningJhaister Ashley LayugNo ratings yet

- Mcgraw Hill/IrwinDocument12 pagesMcgraw Hill/IrwinAhmed El KhateebNo ratings yet

- #3 Deferred Taxes PDFDocument3 pages#3 Deferred Taxes PDFjanus lopezNo ratings yet

- Be 20231208Document6 pagesBe 20231208jherwi.ocretoNo ratings yet

- Regional Economics Class NotesDocument21 pagesRegional Economics Class NotesCabletv10No ratings yet

- Analisis Negosiasi Bisnis Pada PT Allegrindo NusantaraDocument5 pagesAnalisis Negosiasi Bisnis Pada PT Allegrindo Nusantaramuhammad akmalulmazaya ChoiriNo ratings yet

- Hong KongDocument12 pagesHong KongThảo Nguyễn PhươngNo ratings yet

- Invoice: PTCL STN: PTCL NTNDocument1 pageInvoice: PTCL STN: PTCL NTNAmal EmaanNo ratings yet

- Livelihood Sustainability of Handloom Weavers: A Study in Sualkuchi, AssamDocument31 pagesLivelihood Sustainability of Handloom Weavers: A Study in Sualkuchi, AssamAbhishek VermaNo ratings yet

- Eco 310Document3 pagesEco 310LAIZA MARIE MANALONo ratings yet

- Check Stubs 3.0Document3 pagesCheck Stubs 3.0maliktaimoorsurahNo ratings yet