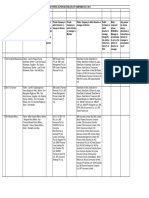

FR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 2

FR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 2

You might also like

- Coop Development Plan 2016 2018Document5 pagesCoop Development Plan 2016 2018Jefrey Gucela100% (1)

- Past Exam Answer Key (To Consol BS)Document53 pagesPast Exam Answer Key (To Consol BS)Huệ LêNo ratings yet

- List Qualified Person - SPANDocument87 pagesList Qualified Person - SPANAhmadFadhlanAbdHamid57% (7)

- Sample Wholesale Agreement TemplateDocument6 pagesSample Wholesale Agreement TemplateBảoBìnhMayMắnNo ratings yet

- Psak 19Document8 pagesPsak 19Nadia NathaniaNo ratings yet

- Module 4 - INTACC2 Intangible AssetsDocument20 pagesModule 4 - INTACC2 Intangible AssetsKhan TanNo ratings yet

- Accounting For Intangible Assets (LKAS 38) 2Document10 pagesAccounting For Intangible Assets (LKAS 38) 29gvsh2w7xyNo ratings yet

- F7 Summary Dec 2011Document30 pagesF7 Summary Dec 2011artkodis100% (1)

- Intangible Assets1Document22 pagesIntangible Assets1hamarshi2010No ratings yet

- Chapter 21 Intangible AssetsDocument10 pagesChapter 21 Intangible AssetsEllen MaskariñoNo ratings yet

- Module 7 IntangiblesDocument14 pagesModule 7 Intangiblestite ko'y malakeNo ratings yet

- Module 7 IntangiblesDocument14 pagesModule 7 IntangiblesEarl ENo ratings yet

- IAS 38 Intangible Assets: Technical SummaryDocument5 pagesIAS 38 Intangible Assets: Technical Summaryanon-553693100% (2)

- Intangible AssetsmarykellyDocument7 pagesIntangible AssetsmarykellyAshura ShaibNo ratings yet

- Accounting Standard 26 - Intangible Assets Issuing Authority: Status: Effective DateDocument6 pagesAccounting Standard 26 - Intangible Assets Issuing Authority: Status: Effective DatePiyush AgarwalNo ratings yet

- Chapter 7 Intangible AssetsDocument70 pagesChapter 7 Intangible AssetsLovely AbadianoNo ratings yet

- IAS 38 Intangible Assets: Technical SummaryDocument5 pagesIAS 38 Intangible Assets: Technical SummaryFoititika.net100% (2)

- Ind As 38Document14 pagesInd As 38Juthika Bora100% (1)

- Module 14 PAS 38Document5 pagesModule 14 PAS 38Jan JanNo ratings yet

- Intangible AssetsDocument87 pagesIntangible AssetsNoor fatimaNo ratings yet

- Pas 38 - Intangible AssetsDocument21 pagesPas 38 - Intangible AssetsMa. Franceska Loiz T. RiveraNo ratings yet

- Pas 38Document8 pagesPas 38AngelicaNo ratings yet

- Ias 38 Intangible Assets SummaryDocument8 pagesIas 38 Intangible Assets SummaryPandu WiratamaNo ratings yet

- Fac 302 ProjectDocument10 pagesFac 302 ProjectGrace GabrielNo ratings yet

- Summary of IAS 38Document5 pagesSummary of IAS 38Jaanu SanthiranNo ratings yet

- Chapter 20Document25 pagesChapter 20Crysta LeeNo ratings yet

- Intangible AssetsDocument10 pagesIntangible AssetsrmsghtuNo ratings yet

- Objective: o o o o oDocument5 pagesObjective: o o o o oShakeel AhmedNo ratings yet

- Intangible Asset: An: Identifiable Non-Monetary Asset Without Physical SubstanceDocument6 pagesIntangible Asset: An: Identifiable Non-Monetary Asset Without Physical SubstanceGianrie Gwyneth CabigonNo ratings yet

- Intangible AssetsDocument6 pagesIntangible Assetsmark fernandezNo ratings yet

- Ias 38Document33 pagesIas 38Reever River100% (1)

- Ias 38 PP 2023Document41 pagesIas 38 PP 2023SaeedNo ratings yet

- Iap 1Document8 pagesIap 1adammorettoNo ratings yet

- Summary of IAS 38Document7 pagesSummary of IAS 38Cyhra Diane MabaoNo ratings yet

- INTANGIBLESDocument40 pagesINTANGIBLESPhoebe Dayrit CunananNo ratings yet

- IAS#38Document43 pagesIAS#38Shah KamalNo ratings yet

- IAS 38 - Intangible AssetsDocument27 pagesIAS 38 - Intangible AssetsArshad BhuttaNo ratings yet

- Al Fattaul Islam ReportDocument7 pagesAl Fattaul Islam Reportsaifullah.ais01No ratings yet

- FR - IAS 38 - CompleteDocument27 pagesFR - IAS 38 - CompleteahmadNo ratings yet

- Intangible Assets Under Pfrs ScopeDocument12 pagesIntangible Assets Under Pfrs ScopeYsabella ChenNo ratings yet

- IAS 36 - Class NotesDocument10 pagesIAS 36 - Class NotesShaheryar ShahidNo ratings yet

- Lkas 38Document28 pagesLkas 38SaneejNo ratings yet

- Ias 38Document7 pagesIas 38Researcher BrianNo ratings yet

- Intangible Assets NotesDocument11 pagesIntangible Assets NotesHayes HareNo ratings yet

- Ho1 Intangible Asset Definition and Initial MeasurementDocument1 pageHo1 Intangible Asset Definition and Initial Measurement21100257No ratings yet

- IAS 36 Chapter TextDocument10 pagesIAS 36 Chapter Textkashan.ahmed1985No ratings yet

- Ias 38-Intangible AssetDocument6 pagesIas 38-Intangible AssetTope JohnNo ratings yet

- CFAS Notes For FINALS PDFDocument26 pagesCFAS Notes For FINALS PDFMarife PangesbanNo ratings yet

- Summary Notes in Intangible Assets PDFDocument5 pagesSummary Notes in Intangible Assets PDFJohn Kenneth100% (1)

- 69256asb55316 As28Document62 pages69256asb55316 As28GybcNo ratings yet

- Ind AS-38: Intangible Assets: 1. ScopeDocument21 pagesInd AS-38: Intangible Assets: 1. ScopeRochak ShresthaNo ratings yet

- Inte Sta Ass Ernati Andard Sets Ional D 38 (Acco (IAS 3 Ountin 38), in NG Ntangi IbleDocument9 pagesInte Sta Ass Ernati Andard Sets Ional D 38 (Acco (IAS 3 Ountin 38), in NG Ntangi IbleVMRONo ratings yet

- Section 4 IDocument22 pagesSection 4 ISatish Ranjan PradhanNo ratings yet

- 74700bos60485 Inter p1 cp5 U6Document32 pages74700bos60485 Inter p1 cp5 U6Gurusaran SNo ratings yet

- Accounting Policies of DaburDocument10 pagesAccounting Policies of DaburMkNo ratings yet

- Chapter 12 PAS 38 INTANGIBLE ASSETSDocument4 pagesChapter 12 PAS 38 INTANGIBLE ASSETSJeanette LampitocNo ratings yet

- Summary of IAS 38Document6 pagesSummary of IAS 38Rey Jr AlipisNo ratings yet

- Indas 38Document6 pagesIndas 38SanjayNo ratings yet

- L6 Intangible AssetsDocument43 pagesL6 Intangible AssetsЛинкольн ХaйдаровNo ratings yet

- ICDS - 5 Fixed AssetsDocument14 pagesICDS - 5 Fixed Assetskavita.m.yadavNo ratings yet

- Intacc Ass 7Document7 pagesIntacc Ass 7Pixie CanaveralNo ratings yet

- Chapter 17 IAS 36 Impairment of AssetsDocument13 pagesChapter 17 IAS 36 Impairment of AssetsKelvin Chu JYNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets - IAS16 - Part 2Document3 pagesFR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets - IAS16 - Part 2User Upload and downloadNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets - IAS16 - Part 3Document3 pagesFR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets - IAS16 - Part 3User Upload and downloadNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets IAS40 - Part 1Document2 pagesFR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets IAS40 - Part 1User Upload and downloadNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 3Document2 pagesFR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 3User Upload and downloadNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 4Document2 pagesFR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 4User Upload and downloadNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets IAS40 - Part 2Document3 pagesFR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets IAS40 - Part 2User Upload and downloadNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Borrowing Costs - IAS23Document2 pagesFR - Accounting For Transactions in Financial Statements: Borrowing Costs - IAS23User Upload and downloadNo ratings yet

- FR 03 Impairment of Assets - IAS36 - Part 3 NotesDocument2 pagesFR 03 Impairment of Assets - IAS36 - Part 3 NotesUser Upload and downloadNo ratings yet

- FR 02 Impairment of Assets - IAS36 - Part 2 NotesDocument2 pagesFR 02 Impairment of Assets - IAS36 - Part 2 NotesUser Upload and downloadNo ratings yet

- Full Download Advanced Accounting 12th Edition Fischer Solutions ManualDocument35 pagesFull Download Advanced Accounting 12th Edition Fischer Solutions Manualrojeroissy2232s100% (37)

- Samba Visa Platinum Credit Cardholders Airport LoungesDocument4 pagesSamba Visa Platinum Credit Cardholders Airport LoungesalbaraamehdarNo ratings yet

- Daily Report Smu Ods Sap-Ho Mei 2023Document40 pagesDaily Report Smu Ods Sap-Ho Mei 2023FEBRYAN RAMADHANNo ratings yet

- 15 Jan 2021 PWD SialkotDocument9 pages15 Jan 2021 PWD SialkotHasnain KhanNo ratings yet

- Scholarship Service Contract FormDocument3 pagesScholarship Service Contract FormFrancis Thomas LimNo ratings yet

- Delegate List For AttendeesDocument4 pagesDelegate List For Attendeesनरेश देसाईNo ratings yet

- Attorney Sam Randazzo's Response To Protective Order by Wind DeveloperDocument46 pagesAttorney Sam Randazzo's Response To Protective Order by Wind DeveloperDennis AlbertNo ratings yet

- Affiliated To The ICSE & ISC Board, New Delhi School Website: APPLICATION FORM FOR NURSERY 2022-23 (This Form Does Not Admission)Document2 pagesAffiliated To The ICSE & ISC Board, New Delhi School Website: APPLICATION FORM FOR NURSERY 2022-23 (This Form Does Not Admission)Shuvajoy ChakrabortyNo ratings yet

- Case Comment: The Kerala Law Academy Law CollegeDocument12 pagesCase Comment: The Kerala Law Academy Law CollegeAdv Aiswarya UnnithanNo ratings yet

- Related Party Transaction PolicyDocument5 pagesRelated Party Transaction PolicycreateriNo ratings yet

- 20210906-2021 GESP Application Form 03sept2021 CODED-fillableDocument2 pages20210906-2021 GESP Application Form 03sept2021 CODED-fillablearianeNo ratings yet

- Warranty Against EvictionDocument2 pagesWarranty Against EvictionartNo ratings yet

- Report SampleDocument2 pagesReport SampleKeembua xeneuNo ratings yet

- Yuvienco V DacuycuyDocument2 pagesYuvienco V DacuycuyRochelle Ann EstradaNo ratings yet

- Max WeberDocument17 pagesMax WeberYash KadamNo ratings yet

- Jefferson Parish Sheriff LegalsDocument3 pagesJefferson Parish Sheriff Legalstheadvocate.comNo ratings yet

- LiabilitiesDocument6 pagesLiabilitiesBS Accoutancy St. SimonNo ratings yet

- Emerging Issuesin Construction Contract Administrationandtheir Significanceinthe Construction Industry 2Document20 pagesEmerging Issuesin Construction Contract Administrationandtheir Significanceinthe Construction Industry 2Boss VasNo ratings yet

- Datasonic - Presentation - 20230529 - Vfinal (4QFY23 Update)Document22 pagesDatasonic - Presentation - 20230529 - Vfinal (4QFY23 Update)phantom78No ratings yet

- Himalayan Gold Shilajit Business ReportDocument2 pagesHimalayan Gold Shilajit Business Reporthaseeb.asghar387No ratings yet

- Prof. Bhambwani'S Reliable Classes Syjc (Recording) Word File (Chapter Wise) Bills of ExchangeDocument2 pagesProf. Bhambwani'S Reliable Classes Syjc (Recording) Word File (Chapter Wise) Bills of ExchangekmrfromNo ratings yet

- ISO-CASCO - ISO-IEC 17020, Conformity Assessment - Requirements For The Operation of Various Types of Bodies Performing InspectionDocument37 pagesISO-CASCO - ISO-IEC 17020, Conformity Assessment - Requirements For The Operation of Various Types of Bodies Performing InspectionKatherine chirinosNo ratings yet

- Government Agencies (DOH, DSWD & DND)Document12 pagesGovernment Agencies (DOH, DSWD & DND)LEVY ALVAREZNo ratings yet

- Development Administration: VisionDocument6 pagesDevelopment Administration: VisionnathNo ratings yet

- Atlas Consolidated Mining and Development Corporation vs. Commissioner of Internal Revenue, RespondentDocument8 pagesAtlas Consolidated Mining and Development Corporation vs. Commissioner of Internal Revenue, RespondentJeorge VerbaNo ratings yet

- PMHPANYD23020003Document2 pagesPMHPANYD23020003ashishNo ratings yet

- GST 50th Council Press ReleaseDocument8 pagesGST 50th Council Press ReleaseDharma Krishnan RajaNo ratings yet

Download as pdf or txt

You might also like

- Coop Development Plan 2016 2018Document5 pagesCoop Development Plan 2016 2018Jefrey Gucela100% (1)

- Past Exam Answer Key (To Consol BS)Document53 pagesPast Exam Answer Key (To Consol BS)Huệ LêNo ratings yet

- List Qualified Person - SPANDocument87 pagesList Qualified Person - SPANAhmadFadhlanAbdHamid57% (7)

- Sample Wholesale Agreement TemplateDocument6 pagesSample Wholesale Agreement TemplateBảoBìnhMayMắnNo ratings yet

- Psak 19Document8 pagesPsak 19Nadia NathaniaNo ratings yet

- Module 4 - INTACC2 Intangible AssetsDocument20 pagesModule 4 - INTACC2 Intangible AssetsKhan TanNo ratings yet

- Accounting For Intangible Assets (LKAS 38) 2Document10 pagesAccounting For Intangible Assets (LKAS 38) 29gvsh2w7xyNo ratings yet

- F7 Summary Dec 2011Document30 pagesF7 Summary Dec 2011artkodis100% (1)

- Intangible Assets1Document22 pagesIntangible Assets1hamarshi2010No ratings yet

- Chapter 21 Intangible AssetsDocument10 pagesChapter 21 Intangible AssetsEllen MaskariñoNo ratings yet

- Module 7 IntangiblesDocument14 pagesModule 7 Intangiblestite ko'y malakeNo ratings yet

- Module 7 IntangiblesDocument14 pagesModule 7 IntangiblesEarl ENo ratings yet

- IAS 38 Intangible Assets: Technical SummaryDocument5 pagesIAS 38 Intangible Assets: Technical Summaryanon-553693100% (2)

- Intangible AssetsmarykellyDocument7 pagesIntangible AssetsmarykellyAshura ShaibNo ratings yet

- Accounting Standard 26 - Intangible Assets Issuing Authority: Status: Effective DateDocument6 pagesAccounting Standard 26 - Intangible Assets Issuing Authority: Status: Effective DatePiyush AgarwalNo ratings yet

- Chapter 7 Intangible AssetsDocument70 pagesChapter 7 Intangible AssetsLovely AbadianoNo ratings yet

- IAS 38 Intangible Assets: Technical SummaryDocument5 pagesIAS 38 Intangible Assets: Technical SummaryFoititika.net100% (2)

- Ind As 38Document14 pagesInd As 38Juthika Bora100% (1)

- Module 14 PAS 38Document5 pagesModule 14 PAS 38Jan JanNo ratings yet

- Intangible AssetsDocument87 pagesIntangible AssetsNoor fatimaNo ratings yet

- Pas 38 - Intangible AssetsDocument21 pagesPas 38 - Intangible AssetsMa. Franceska Loiz T. RiveraNo ratings yet

- Pas 38Document8 pagesPas 38AngelicaNo ratings yet

- Ias 38 Intangible Assets SummaryDocument8 pagesIas 38 Intangible Assets SummaryPandu WiratamaNo ratings yet

- Fac 302 ProjectDocument10 pagesFac 302 ProjectGrace GabrielNo ratings yet

- Summary of IAS 38Document5 pagesSummary of IAS 38Jaanu SanthiranNo ratings yet

- Chapter 20Document25 pagesChapter 20Crysta LeeNo ratings yet

- Intangible AssetsDocument10 pagesIntangible AssetsrmsghtuNo ratings yet

- Objective: o o o o oDocument5 pagesObjective: o o o o oShakeel AhmedNo ratings yet

- Intangible Asset: An: Identifiable Non-Monetary Asset Without Physical SubstanceDocument6 pagesIntangible Asset: An: Identifiable Non-Monetary Asset Without Physical SubstanceGianrie Gwyneth CabigonNo ratings yet

- Intangible AssetsDocument6 pagesIntangible Assetsmark fernandezNo ratings yet

- Ias 38Document33 pagesIas 38Reever River100% (1)

- Ias 38 PP 2023Document41 pagesIas 38 PP 2023SaeedNo ratings yet

- Iap 1Document8 pagesIap 1adammorettoNo ratings yet

- Summary of IAS 38Document7 pagesSummary of IAS 38Cyhra Diane MabaoNo ratings yet

- INTANGIBLESDocument40 pagesINTANGIBLESPhoebe Dayrit CunananNo ratings yet

- IAS#38Document43 pagesIAS#38Shah KamalNo ratings yet

- IAS 38 - Intangible AssetsDocument27 pagesIAS 38 - Intangible AssetsArshad BhuttaNo ratings yet

- Al Fattaul Islam ReportDocument7 pagesAl Fattaul Islam Reportsaifullah.ais01No ratings yet

- FR - IAS 38 - CompleteDocument27 pagesFR - IAS 38 - CompleteahmadNo ratings yet

- Intangible Assets Under Pfrs ScopeDocument12 pagesIntangible Assets Under Pfrs ScopeYsabella ChenNo ratings yet

- IAS 36 - Class NotesDocument10 pagesIAS 36 - Class NotesShaheryar ShahidNo ratings yet

- Lkas 38Document28 pagesLkas 38SaneejNo ratings yet

- Ias 38Document7 pagesIas 38Researcher BrianNo ratings yet

- Intangible Assets NotesDocument11 pagesIntangible Assets NotesHayes HareNo ratings yet

- Ho1 Intangible Asset Definition and Initial MeasurementDocument1 pageHo1 Intangible Asset Definition and Initial Measurement21100257No ratings yet

- IAS 36 Chapter TextDocument10 pagesIAS 36 Chapter Textkashan.ahmed1985No ratings yet

- Ias 38-Intangible AssetDocument6 pagesIas 38-Intangible AssetTope JohnNo ratings yet

- CFAS Notes For FINALS PDFDocument26 pagesCFAS Notes For FINALS PDFMarife PangesbanNo ratings yet

- Summary Notes in Intangible Assets PDFDocument5 pagesSummary Notes in Intangible Assets PDFJohn Kenneth100% (1)

- 69256asb55316 As28Document62 pages69256asb55316 As28GybcNo ratings yet

- Ind AS-38: Intangible Assets: 1. ScopeDocument21 pagesInd AS-38: Intangible Assets: 1. ScopeRochak ShresthaNo ratings yet

- Inte Sta Ass Ernati Andard Sets Ional D 38 (Acco (IAS 3 Ountin 38), in NG Ntangi IbleDocument9 pagesInte Sta Ass Ernati Andard Sets Ional D 38 (Acco (IAS 3 Ountin 38), in NG Ntangi IbleVMRONo ratings yet

- Section 4 IDocument22 pagesSection 4 ISatish Ranjan PradhanNo ratings yet

- 74700bos60485 Inter p1 cp5 U6Document32 pages74700bos60485 Inter p1 cp5 U6Gurusaran SNo ratings yet

- Accounting Policies of DaburDocument10 pagesAccounting Policies of DaburMkNo ratings yet

- Chapter 12 PAS 38 INTANGIBLE ASSETSDocument4 pagesChapter 12 PAS 38 INTANGIBLE ASSETSJeanette LampitocNo ratings yet

- Summary of IAS 38Document6 pagesSummary of IAS 38Rey Jr AlipisNo ratings yet

- Indas 38Document6 pagesIndas 38SanjayNo ratings yet

- L6 Intangible AssetsDocument43 pagesL6 Intangible AssetsЛинкольн ХaйдаровNo ratings yet

- ICDS - 5 Fixed AssetsDocument14 pagesICDS - 5 Fixed Assetskavita.m.yadavNo ratings yet

- Intacc Ass 7Document7 pagesIntacc Ass 7Pixie CanaveralNo ratings yet

- Chapter 17 IAS 36 Impairment of AssetsDocument13 pagesChapter 17 IAS 36 Impairment of AssetsKelvin Chu JYNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets - IAS16 - Part 2Document3 pagesFR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets - IAS16 - Part 2User Upload and downloadNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets - IAS16 - Part 3Document3 pagesFR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets - IAS16 - Part 3User Upload and downloadNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets IAS40 - Part 1Document2 pagesFR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets IAS40 - Part 1User Upload and downloadNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 3Document2 pagesFR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 3User Upload and downloadNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 4Document2 pagesFR - Accounting For Transactions in Financial Statements: Intangible Assets - IAS 38 - Part 4User Upload and downloadNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets IAS40 - Part 2Document3 pagesFR - Accounting For Transactions in Financial Statements: Tangible Non-Current Assets IAS40 - Part 2User Upload and downloadNo ratings yet

- FR - Accounting For Transactions in Financial Statements: Borrowing Costs - IAS23Document2 pagesFR - Accounting For Transactions in Financial Statements: Borrowing Costs - IAS23User Upload and downloadNo ratings yet

- FR 03 Impairment of Assets - IAS36 - Part 3 NotesDocument2 pagesFR 03 Impairment of Assets - IAS36 - Part 3 NotesUser Upload and downloadNo ratings yet

- FR 02 Impairment of Assets - IAS36 - Part 2 NotesDocument2 pagesFR 02 Impairment of Assets - IAS36 - Part 2 NotesUser Upload and downloadNo ratings yet

- Full Download Advanced Accounting 12th Edition Fischer Solutions ManualDocument35 pagesFull Download Advanced Accounting 12th Edition Fischer Solutions Manualrojeroissy2232s100% (37)

- Samba Visa Platinum Credit Cardholders Airport LoungesDocument4 pagesSamba Visa Platinum Credit Cardholders Airport LoungesalbaraamehdarNo ratings yet

- Daily Report Smu Ods Sap-Ho Mei 2023Document40 pagesDaily Report Smu Ods Sap-Ho Mei 2023FEBRYAN RAMADHANNo ratings yet

- 15 Jan 2021 PWD SialkotDocument9 pages15 Jan 2021 PWD SialkotHasnain KhanNo ratings yet

- Scholarship Service Contract FormDocument3 pagesScholarship Service Contract FormFrancis Thomas LimNo ratings yet

- Delegate List For AttendeesDocument4 pagesDelegate List For Attendeesनरेश देसाईNo ratings yet

- Attorney Sam Randazzo's Response To Protective Order by Wind DeveloperDocument46 pagesAttorney Sam Randazzo's Response To Protective Order by Wind DeveloperDennis AlbertNo ratings yet

- Affiliated To The ICSE & ISC Board, New Delhi School Website: APPLICATION FORM FOR NURSERY 2022-23 (This Form Does Not Admission)Document2 pagesAffiliated To The ICSE & ISC Board, New Delhi School Website: APPLICATION FORM FOR NURSERY 2022-23 (This Form Does Not Admission)Shuvajoy ChakrabortyNo ratings yet

- Case Comment: The Kerala Law Academy Law CollegeDocument12 pagesCase Comment: The Kerala Law Academy Law CollegeAdv Aiswarya UnnithanNo ratings yet

- Related Party Transaction PolicyDocument5 pagesRelated Party Transaction PolicycreateriNo ratings yet

- 20210906-2021 GESP Application Form 03sept2021 CODED-fillableDocument2 pages20210906-2021 GESP Application Form 03sept2021 CODED-fillablearianeNo ratings yet

- Warranty Against EvictionDocument2 pagesWarranty Against EvictionartNo ratings yet

- Report SampleDocument2 pagesReport SampleKeembua xeneuNo ratings yet

- Yuvienco V DacuycuyDocument2 pagesYuvienco V DacuycuyRochelle Ann EstradaNo ratings yet

- Max WeberDocument17 pagesMax WeberYash KadamNo ratings yet

- Jefferson Parish Sheriff LegalsDocument3 pagesJefferson Parish Sheriff Legalstheadvocate.comNo ratings yet

- LiabilitiesDocument6 pagesLiabilitiesBS Accoutancy St. SimonNo ratings yet

- Emerging Issuesin Construction Contract Administrationandtheir Significanceinthe Construction Industry 2Document20 pagesEmerging Issuesin Construction Contract Administrationandtheir Significanceinthe Construction Industry 2Boss VasNo ratings yet

- Datasonic - Presentation - 20230529 - Vfinal (4QFY23 Update)Document22 pagesDatasonic - Presentation - 20230529 - Vfinal (4QFY23 Update)phantom78No ratings yet

- Himalayan Gold Shilajit Business ReportDocument2 pagesHimalayan Gold Shilajit Business Reporthaseeb.asghar387No ratings yet

- Prof. Bhambwani'S Reliable Classes Syjc (Recording) Word File (Chapter Wise) Bills of ExchangeDocument2 pagesProf. Bhambwani'S Reliable Classes Syjc (Recording) Word File (Chapter Wise) Bills of ExchangekmrfromNo ratings yet

- ISO-CASCO - ISO-IEC 17020, Conformity Assessment - Requirements For The Operation of Various Types of Bodies Performing InspectionDocument37 pagesISO-CASCO - ISO-IEC 17020, Conformity Assessment - Requirements For The Operation of Various Types of Bodies Performing InspectionKatherine chirinosNo ratings yet

- Government Agencies (DOH, DSWD & DND)Document12 pagesGovernment Agencies (DOH, DSWD & DND)LEVY ALVAREZNo ratings yet

- Development Administration: VisionDocument6 pagesDevelopment Administration: VisionnathNo ratings yet

- Atlas Consolidated Mining and Development Corporation vs. Commissioner of Internal Revenue, RespondentDocument8 pagesAtlas Consolidated Mining and Development Corporation vs. Commissioner of Internal Revenue, RespondentJeorge VerbaNo ratings yet

- PMHPANYD23020003Document2 pagesPMHPANYD23020003ashishNo ratings yet

- GST 50th Council Press ReleaseDocument8 pagesGST 50th Council Press ReleaseDharma Krishnan RajaNo ratings yet