Download as pdf or txt

You might also like

- Managerial Practices Survey 2012Document3 pagesManagerial Practices Survey 2012Leana Polston-Murdoch75% (4)

- 03 9609 22 MS Prov RmaDocument25 pages03 9609 22 MS Prov RmaKalsoom SoniNo ratings yet

- Introduction To Trusting Social - Client Edited2 - 190819V2 - SendDocument21 pagesIntroduction To Trusting Social - Client Edited2 - 190819V2 - SendDemson Natanael Sihaloho100% (1)

- English: Quarter 2 - Module 3Document21 pagesEnglish: Quarter 2 - Module 3Emer Perez100% (12)

- Bitmovin Developer Report 2020 Final V2 PDFDocument26 pagesBitmovin Developer Report 2020 Final V2 PDFBbaPbaNo ratings yet

- The Next Generation of Assessments: White PaperDocument11 pagesThe Next Generation of Assessments: White PaperJamey DAVIDSONNo ratings yet

- Navigating The CCAR Process With Increased InsightDocument3 pagesNavigating The CCAR Process With Increased InsightJamal EldebaisNo ratings yet

- VantageScore 4.0 Fact Sheet Aug 2023Document2 pagesVantageScore 4.0 Fact Sheet Aug 2023Ethan MooreNo ratings yet

- Challenges To Implementing CECLDocument20 pagesChallenges To Implementing CECLDudenNo ratings yet

- BNI Productsheet enDocument2 pagesBNI Productsheet enTonilleNo ratings yet

- GOVERNANCEDocument3 pagesGOVERNANCEma. gretchen pedroNo ratings yet

- Credit Scoring: Beyond The NumbersDocument34 pagesCredit Scoring: Beyond The NumbersramssravaniNo ratings yet

- Q1 2024 Quarterly Investor PresentationDocument39 pagesQ1 2024 Quarterly Investor PresentationTejalNo ratings yet

- Vibhu Agarwal CVDocument1 pageVibhu Agarwal CVrg24No ratings yet

- ERS 2.0 - Product SheetDocument2 pagesERS 2.0 - Product SheetTonilleNo ratings yet

- FICO® Debt Manager™ 7 Solution: Collections and RecoveryDocument2 pagesFICO® Debt Manager™ 7 Solution: Collections and RecoveryataktosNo ratings yet

- Sample - Global Accounting Software Market (2021-2026) - Mordor IntelligenceDocument32 pagesSample - Global Accounting Software Market (2021-2026) - Mordor IntelligenceChintya DefisaptariNo ratings yet

- Introduction To Predictive Analytics: FICO Solutions EducationDocument51 pagesIntroduction To Predictive Analytics: FICO Solutions EducationSumit RampuriaNo ratings yet

- Ilovepdf Merged PDFDocument141 pagesIlovepdf Merged PDFAswqNo ratings yet

- ForecastingDocument126 pagesForecastinghbf7rvqhgfNo ratings yet

- Samarth Mehta - Strategy & New Initiatives - AHEAD Internship 2020Document11 pagesSamarth Mehta - Strategy & New Initiatives - AHEAD Internship 2020Samarth MehtaNo ratings yet

- Account Aggregator - HyperVergeDocument13 pagesAccount Aggregator - HyperVergetestengine701921No ratings yet

- JM - Homefirst PDFDocument10 pagesJM - Homefirst PDFSanjay PatelNo ratings yet

- Developing Your Payor Contracting Strategy 103113 FINALDocument32 pagesDeveloping Your Payor Contracting Strategy 103113 FINALAnish RatnamNo ratings yet

- Assessment BriefDocument9 pagesAssessment BriefAli RanaNo ratings yet

- SPP GuidelinesDocument18 pagesSPP GuidelinesevansmutitiNo ratings yet

- BankConnect v2Document19 pagesBankConnect v2Apoorv KhannaNo ratings yet

- LEAP Mortgages Value PropositionDocument28 pagesLEAP Mortgages Value PropositionLy ThanhNo ratings yet

- Clicks Program - ENDocument29 pagesClicks Program - ENNicholas nichloasNo ratings yet

- Da Vinci - SIBM Pune-1Document7 pagesDa Vinci - SIBM Pune-1Anirban ChowdhuryNo ratings yet

- Cia - Financial ManagementDocument9 pagesCia - Financial Managementsattwikd77No ratings yet

- 2018 Investor Day SlidesDocument57 pages2018 Investor Day SlidesAhmed SayedNo ratings yet

- CIBI PresentationDocument29 pagesCIBI PresentationJune EpNo ratings yet

- Credit ScoreDocument16 pagesCredit ScoreSudheer Gurram100% (2)

- PitchBook - Pumping The Brakes 2Q2023Document43 pagesPitchBook - Pumping The Brakes 2Q2023Никита МузафаровNo ratings yet

- Jupiter India Select Factsheet PA Retail LU0329071053 en GB PDFDocument4 pagesJupiter India Select Factsheet PA Retail LU0329071053 en GB PDFAlly Bin AssadNo ratings yet

- PaceDocument12 pagesPacevishalvermaNo ratings yet

- JM IciciDocument18 pagesJM IciciSanjay PatelNo ratings yet

- 9.1 Week The Risk and Protective Factors of Using DrugsDocument20 pages9.1 Week The Risk and Protective Factors of Using DrugsYuri TsukkishimaNo ratings yet

- Persistent Ace The Case IIDocument6 pagesPersistent Ace The Case IIg23033No ratings yet

- Dixon Technologies Annual Report Analysis 18 September 2021Document12 pagesDixon Technologies Annual Report Analysis 18 September 2021Equity NestNo ratings yet

- V Vietnam Ietnam: Inf Informa Ormation T Tion Technology R Echnology Report EportDocument38 pagesV Vietnam Ietnam: Inf Informa Ormation T Tion Technology R Echnology Report EportK59 Tran Kha VyNo ratings yet

- Mike DSR Pro Report 2023 Oct 1Document16 pagesMike DSR Pro Report 2023 Oct 1Won Seok ChoeNo ratings yet

- Milestone 3 - Division 1 - Team 3 - Martinus WilmanDocument6 pagesMilestone 3 - Division 1 - Team 3 - Martinus WilmanWilmanNo ratings yet

- 9.1 Week The Risk and Protective Factors of Using DrugsDocument20 pages9.1 Week The Risk and Protective Factors of Using DrugsYuri TsukkishimaNo ratings yet

- COUR Presentation Q1-2024Document31 pagesCOUR Presentation Q1-2024Luiz Henrique AraujoNo ratings yet

- Ata Analytics - 5 Data Analytics Software: About Jim Kaplan, CIA, CFEDocument32 pagesAta Analytics - 5 Data Analytics Software: About Jim Kaplan, CIA, CFEMelissa MorgaNo ratings yet

- Loyalty Advisor BrochureDocument2 pagesLoyalty Advisor BrochureChinnakannan ENo ratings yet

- Annual Report For The Financial Year 2021-22Document390 pagesAnnual Report For The Financial Year 2021-22KiwinNo ratings yet

- Global Bond: Schroder International Selection FundDocument3 pagesGlobal Bond: Schroder International Selection FundAruma MuhamadNo ratings yet

- Approaches To Calculating Project Hurdle Rates: Thought Leadership SeriesDocument16 pagesApproaches To Calculating Project Hurdle Rates: Thought Leadership SeriesUmang AgarwalNo ratings yet

- Ibeta Quality Assurance Achieves Industry First in Biometrics TestingDocument2 pagesIbeta Quality Assurance Achieves Industry First in Biometrics TestingPR.comNo ratings yet

- Biometric Testing Report - Pad Algorithm - Template - FinanceDocument20 pagesBiometric Testing Report - Pad Algorithm - Template - FinancedeluxepowerNo ratings yet

- FNSACC414 Prepare Financial Statements For Non-Reporting EntitiesDocument4 pagesFNSACC414 Prepare Financial Statements For Non-Reporting EntitiesDagnachew WeldegebrielNo ratings yet

- (Eric Ries) The Lean Startup How Today's EntrepreDocument2 pages(Eric Ries) The Lean Startup How Today's EntrepremarcpitreNo ratings yet

- fICO resilienceIndexfromEquifaxDocument4 pagesfICO resilienceIndexfromEquifaxvijayambaNo ratings yet

- Equity Valuation Report - TwitterDocument3 pagesEquity Valuation Report - TwitterFEPFinanceClubNo ratings yet

- SyngeneDocument12 pagesSyngeneIndraneel MahantiNo ratings yet

- Case Study 2-Actuarial Valuation - ReportDocument8 pagesCase Study 2-Actuarial Valuation - Reportflávio guilhermeNo ratings yet

- The Henry FundDocument31 pagesThe Henry Fundhalbast87No ratings yet

- PDF The Forrester Wavetm Risk Based Authentication Q2 2020 1St Edition Andras Cser Ebook Full ChapterDocument40 pagesPDF The Forrester Wavetm Risk Based Authentication Q2 2020 1St Edition Andras Cser Ebook Full Chapterholly.nation790100% (1)

- 2024 03 05 - Power The Core - Vision 2027Document97 pages2024 03 05 - Power The Core - Vision 2027sonNo ratings yet

- BNM Malaysia Ekyc StandardisedDocument3 pagesBNM Malaysia Ekyc Standardisedhudaishak87No ratings yet

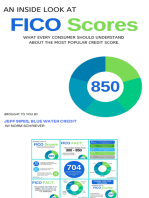

- An Inside Look at FICO Scores: What every consumer should understand about the most popular credit score.From EverandAn Inside Look at FICO Scores: What every consumer should understand about the most popular credit score.No ratings yet

- notesDocument2 pagesnotesJamey DAVIDSONNo ratings yet

- Save Money, Time and Effort Using Psychometrics: 1 © Test Partnership - Getting Started With Psychometrics 1Document14 pagesSave Money, Time and Effort Using Psychometrics: 1 © Test Partnership - Getting Started With Psychometrics 1Jamey DAVIDSONNo ratings yet

- RFP- 001 (HIMS)Document39 pagesRFP- 001 (HIMS)Jamey DAVIDSONNo ratings yet

- Recruitment & Onboarding Tools: Usage Trends REPORT - 2018-19Document21 pagesRecruitment & Onboarding Tools: Usage Trends REPORT - 2018-19Jamey DAVIDSONNo ratings yet

- The State of Pre-Hire Assessments: The Art of Finding and Hiring Quality CandidatesDocument21 pagesThe State of Pre-Hire Assessments: The Art of Finding and Hiring Quality CandidatesJamey DAVIDSONNo ratings yet

- Development Rationale: Mindmetriq Gamified AssessmentsDocument8 pagesDevelopment Rationale: Mindmetriq Gamified AssessmentsJamey DAVIDSONNo ratings yet

- The State of Psychometric Assessments in IndiaDocument8 pagesThe State of Psychometric Assessments in IndiaJamey DAVIDSONNo ratings yet

- How Game-Based Assessments Uncover Top TalentDocument10 pagesHow Game-Based Assessments Uncover Top TalentJamey DAVIDSONNo ratings yet

- Hello: Talented PeopleDocument26 pagesHello: Talented PeopleJamey DAVIDSONNo ratings yet

- GamifyingRecruitmentProcess PDFDocument22 pagesGamifyingRecruitmentProcess PDFJamey DAVIDSONNo ratings yet

- January: It's Okay If You Don't Like Me . Not Everyone Has Good Taste.Document12 pagesJanuary: It's Okay If You Don't Like Me . Not Everyone Has Good Taste.Jamey DAVIDSONNo ratings yet

- The Waterfall Model Template - Editable Flowchart Template On CreatelyDocument7 pagesThe Waterfall Model Template - Editable Flowchart Template On CreatelyJamey DAVIDSONNo ratings yet

- PWC Success Story: Gamification in RecruitmentDocument14 pagesPWC Success Story: Gamification in RecruitmentJamey DAVIDSONNo ratings yet

- Agile Project Management WhitepaperDocument23 pagesAgile Project Management WhitepaperJamey DAVIDSONNo ratings yet

- Strategy, Games, and The Mind: by Martin Reeves, Frida Polli, and Gerardo Gutiérrez-LópezDocument5 pagesStrategy, Games, and The Mind: by Martin Reeves, Frida Polli, and Gerardo Gutiérrez-LópezJamey DAVIDSONNo ratings yet

- Human-Centred Design in Global Health: A Scoping Review of Applications and ContextsDocument24 pagesHuman-Centred Design in Global Health: A Scoping Review of Applications and ContextsJamey DAVIDSONNo ratings yet

- TI Reference No.: 442221857 Title: Electronic Clinical Observations SystemDocument2 pagesTI Reference No.: 442221857 Title: Electronic Clinical Observations SystemJamey DAVIDSONNo ratings yet

- Solution Architect - CVDocument3 pagesSolution Architect - CVJamey DAVIDSONNo ratings yet

- DT Key Terms GlossaryDocument8 pagesDT Key Terms GlossaryJamey DAVIDSONNo ratings yet

- Gartner 2019 - Market Guide For Desktop As A ServiceDocument13 pagesGartner 2019 - Market Guide For Desktop As A ServiceJamey DAVIDSON100% (2)

- Drone Applications For Supporting Disaster Management: World Journal of Engineering and Technology January 2015Document7 pagesDrone Applications For Supporting Disaster Management: World Journal of Engineering and Technology January 2015Jamey DAVIDSONNo ratings yet

- Platinum Imaging Centre: Bill To Invoice Number Date Physician NameDocument1 pagePlatinum Imaging Centre: Bill To Invoice Number Date Physician NameJamey DAVIDSONNo ratings yet

- 6-18-7 Flow Meters and Pressure InstrumentsDocument9 pages6-18-7 Flow Meters and Pressure InstrumentssudokuNo ratings yet

- Pengembangan Lembar Kerja Siswa Berbasis Pendekatan Open-Ended Untuk Memfasilitasi Kemampuan Berpikir Kreatif Matematis Siswa Madrasah TsanawiyahDocument11 pagesPengembangan Lembar Kerja Siswa Berbasis Pendekatan Open-Ended Untuk Memfasilitasi Kemampuan Berpikir Kreatif Matematis Siswa Madrasah Tsanawiyaherdawati nurdinNo ratings yet

- G3 Success With Math TestsDocument58 pagesG3 Success With Math TestsNgoc Mai100% (2)

- Creating Customer Value Developing A Value Proposition and PositioningDocument3 pagesCreating Customer Value Developing A Value Proposition and PositioningЕmil KostovNo ratings yet

- Cad Wor X Field Pipe Users GuideDocument97 pagesCad Wor X Field Pipe Users GuidePetros IosifidisNo ratings yet

- Soft Ferrite Cores User Guide PDFDocument52 pagesSoft Ferrite Cores User Guide PDFPrithvi ScorpNo ratings yet

- Summer Issue of The Dirt 2021Document28 pagesSummer Issue of The Dirt 2021Vermont Nursery & Landscape AssociationNo ratings yet

- Teaching GrammarDocument22 pagesTeaching GrammarMUHAMMAD RAFFINo ratings yet

- Citation CJ4 - Checklist Working TitleDocument3 pagesCitation CJ4 - Checklist Working TitlePhilippe MagnoNo ratings yet

- Landscape and Urban Planning: Jie Su, Alexandros GasparatosDocument15 pagesLandscape and Urban Planning: Jie Su, Alexandros GasparatosMaria Claudia VergaraNo ratings yet

- Water Management Rules As MWELO in Los AngelesDocument2 pagesWater Management Rules As MWELO in Los AngelesPrecise Landscape Water ConservationNo ratings yet

- Real Time Characteristic Value CombinationDocument5 pagesReal Time Characteristic Value CombinationHari KrishnaNo ratings yet

- Bosch Motorsport - 2009Document341 pagesBosch Motorsport - 2009Андрей ТатаренковNo ratings yet

- E and M and Psychotherapy Coding AlgorithmDocument1 pageE and M and Psychotherapy Coding AlgorithmRashiden MadjalesNo ratings yet

- 41 Questions To Test Your Knowledge of Python StringsDocument14 pages41 Questions To Test Your Knowledge of Python StringsshanNo ratings yet

- Iit Hybrid ScheduleDocument3 pagesIit Hybrid ScheduleAdithyan CANo ratings yet

- CH 19 Cash and Liquidity Management Appendix Class WorkDocument4 pagesCH 19 Cash and Liquidity Management Appendix Class WorkMhmd KaramNo ratings yet

- 2-Tourism and CrimeDocument17 pages2-Tourism and CrimeJohn Melvin AbonitallaNo ratings yet

- C700D5 - SpecsDocument17 pagesC700D5 - SpecsElias Abou FakhrNo ratings yet

- Pipe Marking Guide: A Guide To Marking The Pipes in Your Facility According To OSHA/ANSI and Other StandardsDocument19 pagesPipe Marking Guide: A Guide To Marking The Pipes in Your Facility According To OSHA/ANSI and Other StandardsNaga ChaitanyaNo ratings yet

- Mortal Kombat X FatalitiesDocument3 pagesMortal Kombat X FatalitiessdfjsadNo ratings yet

- How To Teach SpeakingDocument4 pagesHow To Teach SpeakingKristabella RachelindhaNo ratings yet

- Ensemble Performance: Elaine GoodmanDocument10 pagesEnsemble Performance: Elaine GoodmanizzatbukhoriNo ratings yet

- Chapter One: What Is Econometrics?Document5 pagesChapter One: What Is Econometrics?Amanuel GenetNo ratings yet

- 1246 SP 4 Emm 24003 B2Document132 pages1246 SP 4 Emm 24003 B2Arash Aghagol100% (1)

- Basic General AptitudeDocument20 pagesBasic General AptitudesantoshNo ratings yet

- CPP QN 2019Document16 pagesCPP QN 2019kanishk vohraNo ratings yet