Download as docx, pdf, or txt

You might also like

- Payment Assessment FormDocument1 pagePayment Assessment FormHanabishi RekkaNo ratings yet

- REMINDER LETTER Late Filing of Vat ReturnDocument2 pagesREMINDER LETTER Late Filing of Vat ReturnHanabishi Rekka100% (1)

- Ebook BRZ SAP LocalizationDocument62 pagesEbook BRZ SAP LocalizationSergio Monteiro Barros100% (3)

- Pea Applicationform PDFDocument1 pagePea Applicationform PDFChipNo ratings yet

- LOG-2-6-WAREHOUSE-TEMPLATE-Warehouse Rental Contract-RCRCS PDFDocument3 pagesLOG-2-6-WAREHOUSE-TEMPLATE-Warehouse Rental Contract-RCRCS PDFG Vishwanath ReddyNo ratings yet

- Bir Ruling Da 086 08Document5 pagesBir Ruling Da 086 08Orlando O. CalundanNo ratings yet

- Powerpoint-09.14.22-Smmc Vat Zero Rating PDFDocument92 pagesPowerpoint-09.14.22-Smmc Vat Zero Rating PDFGirlie BacaocoNo ratings yet

- Motion To Reset NEADocument3 pagesMotion To Reset NEANoreen AquinoNo ratings yet

- Motion For Postponement (Omayao) 2021Document2 pagesMotion For Postponement (Omayao) 2021James DecolongonNo ratings yet

- Tools Accountability Form To Return SAMPLEDocument1 pageTools Accountability Form To Return SAMPLEGau Callanga JrNo ratings yet

- Tax CaseDocument3 pagesTax CaseBethyl PorrasNo ratings yet

- Tax Bulletin by SGV As of Oct 2014Document18 pagesTax Bulletin by SGV As of Oct 2014adobopinikpikanNo ratings yet

- Moyer Agreement of SaleDocument4 pagesMoyer Agreement of SaleElizabeth ScheinbergNo ratings yet

- Certificate of MembershipDocument3 pagesCertificate of MembershipCM5I86Bharat KhalateNo ratings yet

- Aff of QuitclaimDocument3 pagesAff of QuitclaimAlmarius CadigalNo ratings yet

- CA 473 NaturalizationDocument7 pagesCA 473 NaturalizationAnthony H. TrinidadNo ratings yet

- Extension of Probationary Period LetterDocument1 pageExtension of Probationary Period LetterMichele McmillanNo ratings yet

- Borres Realty & Development Corporation Borres Realty & Development CorporationDocument12 pagesBorres Realty & Development Corporation Borres Realty & Development Corporation09303313316No ratings yet

- What Is A Corporate Secretary?Document1 pageWhat Is A Corporate Secretary?PhilNo ratings yet

- For Infringement of TrademarkDocument2 pagesFor Infringement of TrademarkJov May DimcoNo ratings yet

- CARA Spay Neuter Application FormDocument2 pagesCARA Spay Neuter Application FormAmanakeNo ratings yet

- Sample Membership Agreement: Rights As A Member of The Co-OperativeDocument2 pagesSample Membership Agreement: Rights As A Member of The Co-OperativeWeng R. JimenezNo ratings yet

- Affidavit of Loss or CRDocument2 pagesAffidavit of Loss or CRJubelee Anne PatanganNo ratings yet

- Sample RetainerDocument2 pagesSample RetainerMiko Caralde Dela CruzNo ratings yet

- Panoril PN Set-2Document2 pagesPanoril PN Set-2Aileen PuerinNo ratings yet

- Affidavit of UndertakingDocument1 pageAffidavit of UndertakingJhodessy Jane BrianNo ratings yet

- Authorization For Credit Investigation and AppraisalDocument1 pageAuthorization For Credit Investigation and AppraisalMarvin CeledioNo ratings yet

- Letter of Intent To BuyDocument1 pageLetter of Intent To BuyNai AccgNo ratings yet

- Ayala Corp Class B Preferred Shares - Preliminary ProspectusDocument387 pagesAyala Corp Class B Preferred Shares - Preliminary ProspectusEunjina MoNo ratings yet

- Write Off Policy FINALDocument5 pagesWrite Off Policy FINALHoward UntalanNo ratings yet

- RMC No 5-2014 - Clarifying The Provisions of RR 1-2014Document18 pagesRMC No 5-2014 - Clarifying The Provisions of RR 1-2014sj_adenipNo ratings yet

- Demand Letter UberasDocument3 pagesDemand Letter UberasfortunecNo ratings yet

- Authorization LetterDocument1 pageAuthorization LetterLeyyNo ratings yet

- RR 13-1998Document17 pagesRR 13-1998nikkaremullaNo ratings yet

- Refund of CWT and VAT Upon Dissolution of Company - ICN 9.11.14Document3 pagesRefund of CWT and VAT Upon Dissolution of Company - ICN 9.11.14JianSadakoNo ratings yet

- Revenue Audit Memorandum 1-98Document5 pagesRevenue Audit Memorandum 1-98Nikos CabreraNo ratings yet

- Written Board ResolutionDocument1 pageWritten Board ResolutionRegi PonferradaNo ratings yet

- Special Power of AttorneyDocument1 pageSpecial Power of AttorneyWics Marawi LanaoNo ratings yet

- SSS R3 Contribution Collection List in Excel FormatDocument2 pagesSSS R3 Contribution Collection List in Excel FormatChristopher Daniels0% (2)

- Law of Insurance in The PhilippinesDocument41 pagesLaw of Insurance in The PhilippinesAndrea NaquimenNo ratings yet

- RMC No. 77-2021Document38 pagesRMC No. 77-2021Mike Ferdinand SantosNo ratings yet

- Ffidavit: Republic of The Philippines) Province of Camarines Sur) Municipality of Ocampo) S.SDocument1 pageFfidavit: Republic of The Philippines) Province of Camarines Sur) Municipality of Ocampo) S.SMichael Mendoza MarpuriNo ratings yet

- Sec Cert With Pre TrialDocument2 pagesSec Cert With Pre TrialEmil AlviolaNo ratings yet

- Annex CDocument1 pageAnnex CAileen TeoNo ratings yet

- FDA Drugs Clearing Account FDA Drugs Clearing Account: Cashierposting@fda - Gov.ph Cashierposting@fda - Gov.phDocument6 pagesFDA Drugs Clearing Account FDA Drugs Clearing Account: Cashierposting@fda - Gov.ph Cashierposting@fda - Gov.phRFO REGION 5No ratings yet

- DL Mary Grace RamosDocument2 pagesDL Mary Grace RamosChandi LendNo ratings yet

- DOAS TemplateDocument2 pagesDOAS TemplateNoon VeryNo ratings yet

- Assocation of Water Districts Bylaws-AmendedDocument15 pagesAssocation of Water Districts Bylaws-AmendedLeyCodes LeyCodesNo ratings yet

- Revocation of Special Power of AttorneyDocument2 pagesRevocation of Special Power of AttorneyJasNo ratings yet

- Articles of IncorporationDocument4 pagesArticles of IncorporationPaul EspinosaNo ratings yet

- Acknowledgment Receipt - SampleDocument1 pageAcknowledgment Receipt - SampleRey ObnimagaNo ratings yet

- Department Circular Series of 2012Document81 pagesDepartment Circular Series of 2012Pyke LaygoNo ratings yet

- Branch Manager - JD - UpdatedDocument1 pageBranch Manager - JD - UpdatedAdam SNo ratings yet

- Affidavit of Loss - TaytayDocument2 pagesAffidavit of Loss - TaytayaldinNo ratings yet

- Revenue Memorandum Order No. 37-94: March 25, 1994Document8 pagesRevenue Memorandum Order No. 37-94: March 25, 1994Rufino Gerard Moreno IIINo ratings yet

- BIR Ruling (DA-335) 815-09Document5 pagesBIR Ruling (DA-335) 815-09Ren Mar CruzNo ratings yet

- Notice of Non-Holding of Annual Meeting SECDocument1 pageNotice of Non-Holding of Annual Meeting SECBikoy EstoqueNo ratings yet

- TH ST RDDocument2 pagesTH ST RDVivo MayvelNo ratings yet

- Vat UpdatesDocument5 pagesVat Updatesprecy.calusaNo ratings yet

- Digest RR 13-2018Document9 pagesDigest RR 13-2018Maria Rose Ann BacilloteNo ratings yet

- Value Added Tax - Sale of GoodsDocument8 pagesValue Added Tax - Sale of Goods2071275No ratings yet

- Felipe, Emmyrose N. BSA-3 (Tax 2 MW 8:30-10:00am)Document5 pagesFelipe, Emmyrose N. BSA-3 (Tax 2 MW 8:30-10:00am)AustinNo ratings yet

- Reviewer BTTDocument14 pagesReviewer BTTAlthea Frances VasalloNo ratings yet

- 100% CompletedDocument1 page100% CompletedHanabishi RekkaNo ratings yet

- Destruction FormDocument2 pagesDestruction FormHanabishi RekkaNo ratings yet

- 49 PAID 2016Document12 pages49 PAID 2016Hanabishi RekkaNo ratings yet

- Law On Sales Final Exam First Sem 2020Document2 pagesLaw On Sales Final Exam First Sem 2020Hanabishi RekkaNo ratings yet

- Sub Contract Agreement TabukDocument7 pagesSub Contract Agreement TabukHanabishi RekkaNo ratings yet

- Land For The LandlessDocument1 pageLand For The LandlessHanabishi RekkaNo ratings yet

- Bid Disqualification LetterDocument1 pageBid Disqualification LetterHanabishi RekkaNo ratings yet

- VAT LATE FILING 1ST Q AND APRIL 2020 FilteredDocument13 pagesVAT LATE FILING 1ST Q AND APRIL 2020 FilteredHanabishi RekkaNo ratings yet

- RBR Builders & Ready Mix Concrete: Cell # 09228390603 / TELEFAX (044) 940-4005Document1 pageRBR Builders & Ready Mix Concrete: Cell # 09228390603 / TELEFAX (044) 940-4005Hanabishi RekkaNo ratings yet

- Sales Midterm ExamDocument2 pagesSales Midterm ExamHanabishi Rekka100% (1)

- Income Payee'S Sworn Declaration of Gross Receipts/SalesDocument2 pagesIncome Payee'S Sworn Declaration of Gross Receipts/SalesHanabishi RekkaNo ratings yet

- John Louie Esguerra Constitutional Law I Midterm (October 31, 2020)Document2 pagesJohn Louie Esguerra Constitutional Law I Midterm (October 31, 2020)Hanabishi RekkaNo ratings yet

- Land Titles and Deeds Module 1Document2 pagesLand Titles and Deeds Module 1Hanabishi RekkaNo ratings yet

- Wesleyan Law Course Guide For Negotiable Instruments LawDocument20 pagesWesleyan Law Course Guide For Negotiable Instruments LawHanabishi RekkaNo ratings yet

- Land Titles and DeedsDocument8 pagesLand Titles and DeedsHanabishi RekkaNo ratings yet

- Constitutional Law 2 Course Outline (Syllabus) John Wesley School of Law and GovernanceDocument17 pagesConstitutional Law 2 Course Outline (Syllabus) John Wesley School of Law and GovernanceHanabishi RekkaNo ratings yet

- Association of Small Landowners in The Philippines v. Honorable Secretary of Agrarian ReformDocument3 pagesAssociation of Small Landowners in The Philippines v. Honorable Secretary of Agrarian ReformHanabishi RekkaNo ratings yet

- General Rule: Potestas Delegata Non Delegari PotestDocument3 pagesGeneral Rule: Potestas Delegata Non Delegari PotestHanabishi RekkaNo ratings yet

- Jas PDFDocument34 pagesJas PDFJasenriNo ratings yet

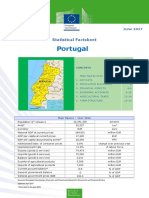

- Portugal: Statistical FactsheetDocument16 pagesPortugal: Statistical Factsheetmathavan_00No ratings yet

- Trade and Technology: The Ricardian ModelDocument74 pagesTrade and Technology: The Ricardian Modelnawab0403100% (1)

- Economics Practice Sheets N22Document101 pagesEconomics Practice Sheets N22joyboyishehereNo ratings yet

- Macro Eco Complete Ques+NotesDocument117 pagesMacro Eco Complete Ques+NotesPiyush ChhajerNo ratings yet

- 31.economic Contributions of Indian Film IndustryDocument3 pages31.economic Contributions of Indian Film IndustrymercatuzNo ratings yet

- MODULE 1 - Intro To Operations Mgt.Document4 pagesMODULE 1 - Intro To Operations Mgt.Samantha CruzNo ratings yet

- 2006 ArDocument176 pages2006 ArMoch Rifki HartantoNo ratings yet

- Activity-Based Management and Activity-Based Costing: Cost Accounting: Foundations & Evolutions, 9eDocument19 pagesActivity-Based Management and Activity-Based Costing: Cost Accounting: Foundations & Evolutions, 9eDonna Rose Sanchez FegiNo ratings yet

- Measurement of National Income Types Methods Benefits and Problems Associated E6766766Document9 pagesMeasurement of National Income Types Methods Benefits and Problems Associated E6766766RohanNo ratings yet

- 019 Problem Solving With Answer GuideDocument30 pages019 Problem Solving With Answer GuideRestie John UlipNo ratings yet

- 20200731-0100001646-SMCC-Mall North Wing-TECHNOMARINE ENTERPRISES PHILS INC PDFDocument6 pages20200731-0100001646-SMCC-Mall North Wing-TECHNOMARINE ENTERPRISES PHILS INC PDFEdjon AndalNo ratings yet

- National Income & Related ConceptsDocument75 pagesNational Income & Related ConceptsMukesh KumarNo ratings yet

- ProductivityDocument25 pagesProductivitysau1994No ratings yet

- 5.security Barracks B - DupaDocument405 pages5.security Barracks B - Dupa朱叶凡No ratings yet

- Evolution Indonesia Participation Global Value ChainsDocument135 pagesEvolution Indonesia Participation Global Value ChainsSulistyo HadiNo ratings yet

- Soal M. JurnalDocument36 pagesSoal M. JurnalDKTNo ratings yet

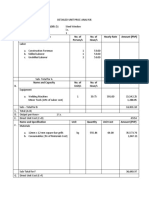

- DETAILED UNIT PRICE ANALYSIS CadDocument7 pagesDETAILED UNIT PRICE ANALYSIS CadIan Kirby RedondoNo ratings yet

- WDI11122021Document531 pagesWDI11122021Jawwad JaskaniNo ratings yet

- National Income AccountingDocument100 pagesNational Income AccountingreethuganiNo ratings yet

- Principle of VATDocument6 pagesPrinciple of VATtornadoindiaNo ratings yet

- Cost Accounting-St Chap001Document17 pagesCost Accounting-St Chap001Caliech Califa Jones-PennNo ratings yet

- Determination of National Income - Unit I - National Income AccountingDocument34 pagesDetermination of National Income - Unit I - National Income AccountingPriya chauhanNo ratings yet

- Namma Kalvi 12th Economics Unit 2 Surya Economics Guide emDocument28 pagesNamma Kalvi 12th Economics Unit 2 Surya Economics Guide emAakaash C.K.No ratings yet

- Macro EconDocument128 pagesMacro EconDawne BrownNo ratings yet

- Other Percentage TaxespdfDocument5 pagesOther Percentage TaxespdfAngeilyn RodaNo ratings yet

- Adam SugarDocument11 pagesAdam SugarshirazhaqNo ratings yet

- HHW12 PDFDocument37 pagesHHW12 PDFĂmåñ Śïńğh ŘăjpuťNo ratings yet

- Business Studies IgcseDocument115 pagesBusiness Studies IgcsexNo ratings yet