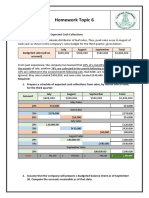

Topic 6 - Cash Budget

Topic 6 - Cash Budget

You might also like

- Group 3 - Master Budget-Earrings UnlimitedDocument8 pagesGroup 3 - Master Budget-Earrings UnlimitedLorena Mae LasquiteNo ratings yet

- Project Case 9-30 Master BudgetDocument6 pagesProject Case 9-30 Master Budgetleizalm29% (7)

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- Chapter 7 ProblemsDocument25 pagesChapter 7 ProblemsRhoda Claire M. Gansobin100% (1)

- Proof of Cash ProblemDocument3 pagesProof of Cash ProblemKathleen Frondozo71% (7)

- Includes $2,000 Depreciation Each MonthDocument3 pagesIncludes $2,000 Depreciation Each MonthLynnard Philip Panes100% (1)

- 08 TP 1-ArgDocument3 pages08 TP 1-ArgAlthea ObinaNo ratings yet

- Mas ReviewerDocument14 pagesMas ReviewerMichelle AvilesNo ratings yet

- Cash BudgetingDocument3 pagesCash Budgetingsunil.ctNo ratings yet

- 08 TP - Evangelista Angela - 501PDocument9 pages08 TP - Evangelista Angela - 501PBetchang AquinoNo ratings yet

- Geme CostDocument6 pagesGeme CostBiruk Chuchu NigusuNo ratings yet

- Case 8-31: April May June QuarterDocument2 pagesCase 8-31: April May June QuarterileviejoieNo ratings yet

- Budgeting and Budgetary ControlDocument13 pagesBudgeting and Budgetary ControlRenu PoddarNo ratings yet

- Earrings Suggested SolutionsDocument4 pagesEarrings Suggested Solutions9ry5gsghybNo ratings yet

- Chapter 4 Best Master Budget IllustrationDocument23 pagesChapter 4 Best Master Budget IllustrationLeykun GizealemNo ratings yet

- Asynchronous Statement of Financial Position XYZ CompanyDocument5 pagesAsynchronous Statement of Financial Position XYZ CompanyDiana Fernandez MagnoNo ratings yet

- Working Capital Suggested SolutionsDocument7 pagesWorking Capital Suggested SolutionsBulelwa HarrisNo ratings yet

- Cash Budget For January Thru July Based On Expected Sales Nov Dec Jan Feb MarDocument6 pagesCash Budget For January Thru July Based On Expected Sales Nov Dec Jan Feb MardanielkangNo ratings yet

- BudgetingDocument74 pagesBudgetingRevathi AnandNo ratings yet

- The Sharpe Corporation's ProjectedDocument3 pagesThe Sharpe Corporation's Projectedmadnansajid8765No ratings yet

- Corminal TPDocument7 pagesCorminal TPBetchang AquinoNo ratings yet

- Assignment 2Document3 pagesAssignment 2Joe MajchrzakNo ratings yet

- Proof of Cash123Document5 pagesProof of Cash123rufamaegarcia07No ratings yet

- Part 1: Reviewer#5: Midterm Quiz 9fundamentals of Accounting 1 & 2)Document5 pagesPart 1: Reviewer#5: Midterm Quiz 9fundamentals of Accounting 1 & 2)annedanyle acabadoNo ratings yet

- Llagas 10 Quiz 2Document6 pagesLlagas 10 Quiz 2Angela Fye LlagasNo ratings yet

- KALBARYONISHERLY2Document8 pagesKALBARYONISHERLY2De MarcusNo ratings yet

- BudgetingDocument130 pagesBudgetingRevathi AnandNo ratings yet

- Master BudgetDocument36 pagesMaster BudgetRafols AnnabelleNo ratings yet

- 60dac5585d719 Chapter 6 Supplementary Exercise Question With Answer KeyDocument7 pages60dac5585d719 Chapter 6 Supplementary Exercise Question With Answer KeyOvelia KayuzakiNo ratings yet

- AP 001 A.2 Proof of Cash Prob 2Document1 pageAP 001 A.2 Proof of Cash Prob 2joseph90865No ratings yet

- Audit of Cash and Cash Equivalents - Set BDocument5 pagesAudit of Cash and Cash Equivalents - Set BZyrah Mae SaezNo ratings yet

- Partnership LiquidationDocument10 pagesPartnership LiquidationAbc xyzNo ratings yet

- Production Budget: October NovemberDocument11 pagesProduction Budget: October NovemberKyle LapuzNo ratings yet

- Budgeting 30 NOvDocument8 pagesBudgeting 30 NOvHaris HasanNo ratings yet

- MAS ExerciseDocument9 pagesMAS ExerciseAlaine Milka GosycoNo ratings yet

- Acctg 202Document9 pagesAcctg 202Lore Desa CenizaNo ratings yet

- 2 Tutorial Question and Answer On Cash BudgetDocument4 pages2 Tutorial Question and Answer On Cash BudgetHasnita Hasan BudinNo ratings yet

- Problem 10-20: Month April May June QuarterDocument1 pageProblem 10-20: Month April May June QuarterIra PutriNo ratings yet

- Proof of Cash Syria CompanyDocument4 pagesProof of Cash Syria CompanyCJ alandy100% (1)

- HomeworkDocument3 pagesHomeworkZihao TangNo ratings yet

- Case Study 2022 FallDocument3 pagesCase Study 2022 FallAppleDugarNo ratings yet

- Lecture 2 - Practice QuestionsDocument2 pagesLecture 2 - Practice Questionsdonkhalif13No ratings yet

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- 2017 Fall Solution: Sales BudgetDocument3 pages2017 Fall Solution: Sales BudgetRaam Tha BossNo ratings yet

- Exercise 1Document3 pagesExercise 1ScribdTranslationsNo ratings yet

- Quiz in Safe Payment and Cash Priority Program With Answer Keys Part 2Document4 pagesQuiz in Safe Payment and Cash Priority Program With Answer Keys Part 2caraaatbongNo ratings yet

- Cash Management (Divya Jadi Booti)Document27 pagesCash Management (Divya Jadi Booti)Michael AdhikariNo ratings yet

- Mayes 8e CH04 SolutionsDocument48 pagesMayes 8e CH04 SolutionsRamez Ahmed0% (1)

- FFS - NumericalsDocument5 pagesFFS - NumericalsFunny ManNo ratings yet

- FAR Quiz 1 SolutionDocument16 pagesFAR Quiz 1 SolutiontruthNo ratings yet

- AC 41 Accounting Essentials PRACTICE DRILL Unit IIIDocument1 pageAC 41 Accounting Essentials PRACTICE DRILL Unit IIIAiahNo ratings yet

- Bigotry Company Proof of CashDocument4 pagesBigotry Company Proof of CashGee Lysa Pascua VilbarNo ratings yet

- Assignment 1Document12 pagesAssignment 1Ira YbanezNo ratings yet

- Treasury Management Vs Cash Management Answer To Warm Up ExercisesDocument8 pagesTreasury Management Vs Cash Management Answer To Warm Up Exercisesephraim0% (1)

- 1.1 Cce To Proof of Cash Discussion ProblemsDocument3 pages1.1 Cce To Proof of Cash Discussion ProblemsGiyah UsiNo ratings yet

- FALL Class 7 - Cash Budgeting - Ch9 - GDBA - Note # 7 - TEACHERDocument7 pagesFALL Class 7 - Cash Budgeting - Ch9 - GDBA - Note # 7 - TEACHERAkankshaNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Rundown Webinar 4 Juli 2020Document2 pagesRundown Webinar 4 Juli 2020michelle beyonceNo ratings yet

- Timeline Interview Commitee MGT Award 2020Document2 pagesTimeline Interview Commitee MGT Award 2020michelle beyonceNo ratings yet

- Evaluating A Company'S External Environment: Mcgraw-Hill/IrwinDocument21 pagesEvaluating A Company'S External Environment: Mcgraw-Hill/Irwinmichelle beyonceNo ratings yet

- Chapter # 1 Outline: Mcgraw-Hill/IrwinDocument15 pagesChapter # 1 Outline: Mcgraw-Hill/Irwinmichelle beyonceNo ratings yet

- Group D - Network Effects On Multi-Sided Platform (Gojek)Document7 pagesGroup D - Network Effects On Multi-Sided Platform (Gojek)michelle beyonceNo ratings yet

- Gojek Case Study Group 4Document2 pagesGojek Case Study Group 4michelle beyonceNo ratings yet

- Creative Content On The Digital Campaign Tokopedia "Seller Story"Document15 pagesCreative Content On The Digital Campaign Tokopedia "Seller Story"michelle beyonceNo ratings yet

- Group 6 Psak 51-60Document11 pagesGroup 6 Psak 51-60michelle beyonceNo ratings yet

- Chapter 18Document6 pagesChapter 18michelle beyonceNo ratings yet

- The 73rd Constitutional Amendment ActDocument26 pagesThe 73rd Constitutional Amendment ActYasser ArfatNo ratings yet

- Resume Word OriginDocument5 pagesResume Word Originaflkvapnf100% (1)

- Abita Brand GuideDocument7 pagesAbita Brand GuideGabriel Bedini de JesusNo ratings yet

- Geometry AssignmentDocument2 pagesGeometry AssignmentAMIN BUHARI ABDUL KHADERNo ratings yet

- HIRARC FormDocument43 pagesHIRARC FormFachri Hidayat50% (2)

- CEDC Discl StatementDocument789 pagesCEDC Discl StatementChapter 11 DocketsNo ratings yet

- T5 B68 Craig Unger FDR - 5-21-04 Stull Email - Unger Saudi Flight Docs 616Document6 pagesT5 B68 Craig Unger FDR - 5-21-04 Stull Email - Unger Saudi Flight Docs 6169/11 Document ArchiveNo ratings yet

- Dodge Ram Truck 2006 2500 - 3500 BrochureDocument11 pagesDodge Ram Truck 2006 2500 - 3500 BrochureStephen RivettNo ratings yet

- 458-Radhika Polypack - Amd - xlsx1.Document2 pages458-Radhika Polypack - Amd - xlsx1.MUNINo ratings yet

- Dr. N. Kumarappan IE (I) Council Candidate - Electrical DivisionDocument1 pageDr. N. Kumarappan IE (I) Council Candidate - Electrical Divisionshanmugasundaram32No ratings yet

- Chem Project VDocument18 pagesChem Project Vmjvarun2006No ratings yet

- Programming Arduino Using Atmel Studio 6Document6 pagesProgramming Arduino Using Atmel Studio 6Carlos FerrarisNo ratings yet

- Astro-Logics Pub PDFDocument7 pagesAstro-Logics Pub PDFlbedar100% (1)

- Warman Slurry Correction Factors HR and ER Pump Power: MPC H S S L Q PDocument2 pagesWarman Slurry Correction Factors HR and ER Pump Power: MPC H S S L Q Pyoel cueva arquinigoNo ratings yet

- HX DG V 5.1.0 PDFDocument136 pagesHX DG V 5.1.0 PDFLyu SeyNo ratings yet

- Applied Physics On Spectros PDFDocument71 pagesApplied Physics On Spectros PDFKaskus FourusNo ratings yet

- Denim A New Export Item For BangladeshDocument2 pagesDenim A New Export Item For Bangladeshhabibun naharNo ratings yet

- PT English-6 Q2Document7 pagesPT English-6 Q2Elona Jane CapangpanganNo ratings yet

- Anand RathiDocument95 pagesAnand Rathivikramgupta195096% (25)

- Advanced Digital Controls Improve PFC PerformanceDocument18 pagesAdvanced Digital Controls Improve PFC Performancediablo diablolordNo ratings yet

- RecursionDocument9 pagesRecursionMada BaskoroNo ratings yet

- Learning Experiences Learning Outcome 3 - Install The Computer Application Software Learning Activities Special InstructionsDocument15 pagesLearning Experiences Learning Outcome 3 - Install The Computer Application Software Learning Activities Special InstructionsAlexandra FernandezNo ratings yet

- 9 Cir vs. Baier-Nickel DGSTDocument2 pages9 Cir vs. Baier-Nickel DGSTMiguelNo ratings yet

- Terraria Official Lore PDFDocument3 pagesTerraria Official Lore PDFCavalo SebosoNo ratings yet

- Ritishree Offer EztruckDocument4 pagesRitishree Offer EztruckKali RathNo ratings yet

- School - Guest Faculty Management SystemDocument1 pageSchool - Guest Faculty Management SystemSuraj BadholiyaNo ratings yet

- Topic:: SolidsDocument8 pagesTopic:: SolidsDhanBahadurNo ratings yet

- Final INTERNSHIP Report-AshishDocument66 pagesFinal INTERNSHIP Report-AshishAshish PantNo ratings yet

- Lecture Two: Theories of SLA: Input, Output and The Role of Noticing How Does SLA Take Place?Document4 pagesLecture Two: Theories of SLA: Input, Output and The Role of Noticing How Does SLA Take Place?Hollós DávidNo ratings yet

- Ielts Reading Test 1Document7 pagesIelts Reading Test 1Bách XuânNo ratings yet

Download as doc, pdf, or txt

You might also like

- Group 3 - Master Budget-Earrings UnlimitedDocument8 pagesGroup 3 - Master Budget-Earrings UnlimitedLorena Mae LasquiteNo ratings yet

- Project Case 9-30 Master BudgetDocument6 pagesProject Case 9-30 Master Budgetleizalm29% (7)

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- Chapter 7 ProblemsDocument25 pagesChapter 7 ProblemsRhoda Claire M. Gansobin100% (1)

- Proof of Cash ProblemDocument3 pagesProof of Cash ProblemKathleen Frondozo71% (7)

- Includes $2,000 Depreciation Each MonthDocument3 pagesIncludes $2,000 Depreciation Each MonthLynnard Philip Panes100% (1)

- 08 TP 1-ArgDocument3 pages08 TP 1-ArgAlthea ObinaNo ratings yet

- Mas ReviewerDocument14 pagesMas ReviewerMichelle AvilesNo ratings yet

- Cash BudgetingDocument3 pagesCash Budgetingsunil.ctNo ratings yet

- 08 TP - Evangelista Angela - 501PDocument9 pages08 TP - Evangelista Angela - 501PBetchang AquinoNo ratings yet

- Geme CostDocument6 pagesGeme CostBiruk Chuchu NigusuNo ratings yet

- Case 8-31: April May June QuarterDocument2 pagesCase 8-31: April May June QuarterileviejoieNo ratings yet

- Budgeting and Budgetary ControlDocument13 pagesBudgeting and Budgetary ControlRenu PoddarNo ratings yet

- Earrings Suggested SolutionsDocument4 pagesEarrings Suggested Solutions9ry5gsghybNo ratings yet

- Chapter 4 Best Master Budget IllustrationDocument23 pagesChapter 4 Best Master Budget IllustrationLeykun GizealemNo ratings yet

- Asynchronous Statement of Financial Position XYZ CompanyDocument5 pagesAsynchronous Statement of Financial Position XYZ CompanyDiana Fernandez MagnoNo ratings yet

- Working Capital Suggested SolutionsDocument7 pagesWorking Capital Suggested SolutionsBulelwa HarrisNo ratings yet

- Cash Budget For January Thru July Based On Expected Sales Nov Dec Jan Feb MarDocument6 pagesCash Budget For January Thru July Based On Expected Sales Nov Dec Jan Feb MardanielkangNo ratings yet

- BudgetingDocument74 pagesBudgetingRevathi AnandNo ratings yet

- The Sharpe Corporation's ProjectedDocument3 pagesThe Sharpe Corporation's Projectedmadnansajid8765No ratings yet

- Corminal TPDocument7 pagesCorminal TPBetchang AquinoNo ratings yet

- Assignment 2Document3 pagesAssignment 2Joe MajchrzakNo ratings yet

- Proof of Cash123Document5 pagesProof of Cash123rufamaegarcia07No ratings yet

- Part 1: Reviewer#5: Midterm Quiz 9fundamentals of Accounting 1 & 2)Document5 pagesPart 1: Reviewer#5: Midterm Quiz 9fundamentals of Accounting 1 & 2)annedanyle acabadoNo ratings yet

- Llagas 10 Quiz 2Document6 pagesLlagas 10 Quiz 2Angela Fye LlagasNo ratings yet

- KALBARYONISHERLY2Document8 pagesKALBARYONISHERLY2De MarcusNo ratings yet

- BudgetingDocument130 pagesBudgetingRevathi AnandNo ratings yet

- Master BudgetDocument36 pagesMaster BudgetRafols AnnabelleNo ratings yet

- 60dac5585d719 Chapter 6 Supplementary Exercise Question With Answer KeyDocument7 pages60dac5585d719 Chapter 6 Supplementary Exercise Question With Answer KeyOvelia KayuzakiNo ratings yet

- AP 001 A.2 Proof of Cash Prob 2Document1 pageAP 001 A.2 Proof of Cash Prob 2joseph90865No ratings yet

- Audit of Cash and Cash Equivalents - Set BDocument5 pagesAudit of Cash and Cash Equivalents - Set BZyrah Mae SaezNo ratings yet

- Partnership LiquidationDocument10 pagesPartnership LiquidationAbc xyzNo ratings yet

- Production Budget: October NovemberDocument11 pagesProduction Budget: October NovemberKyle LapuzNo ratings yet

- Budgeting 30 NOvDocument8 pagesBudgeting 30 NOvHaris HasanNo ratings yet

- MAS ExerciseDocument9 pagesMAS ExerciseAlaine Milka GosycoNo ratings yet

- Acctg 202Document9 pagesAcctg 202Lore Desa CenizaNo ratings yet

- 2 Tutorial Question and Answer On Cash BudgetDocument4 pages2 Tutorial Question and Answer On Cash BudgetHasnita Hasan BudinNo ratings yet

- Problem 10-20: Month April May June QuarterDocument1 pageProblem 10-20: Month April May June QuarterIra PutriNo ratings yet

- Proof of Cash Syria CompanyDocument4 pagesProof of Cash Syria CompanyCJ alandy100% (1)

- HomeworkDocument3 pagesHomeworkZihao TangNo ratings yet

- Case Study 2022 FallDocument3 pagesCase Study 2022 FallAppleDugarNo ratings yet

- Lecture 2 - Practice QuestionsDocument2 pagesLecture 2 - Practice Questionsdonkhalif13No ratings yet

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- 2017 Fall Solution: Sales BudgetDocument3 pages2017 Fall Solution: Sales BudgetRaam Tha BossNo ratings yet

- Exercise 1Document3 pagesExercise 1ScribdTranslationsNo ratings yet

- Quiz in Safe Payment and Cash Priority Program With Answer Keys Part 2Document4 pagesQuiz in Safe Payment and Cash Priority Program With Answer Keys Part 2caraaatbongNo ratings yet

- Cash Management (Divya Jadi Booti)Document27 pagesCash Management (Divya Jadi Booti)Michael AdhikariNo ratings yet

- Mayes 8e CH04 SolutionsDocument48 pagesMayes 8e CH04 SolutionsRamez Ahmed0% (1)

- FFS - NumericalsDocument5 pagesFFS - NumericalsFunny ManNo ratings yet

- FAR Quiz 1 SolutionDocument16 pagesFAR Quiz 1 SolutiontruthNo ratings yet

- AC 41 Accounting Essentials PRACTICE DRILL Unit IIIDocument1 pageAC 41 Accounting Essentials PRACTICE DRILL Unit IIIAiahNo ratings yet

- Bigotry Company Proof of CashDocument4 pagesBigotry Company Proof of CashGee Lysa Pascua VilbarNo ratings yet

- Assignment 1Document12 pagesAssignment 1Ira YbanezNo ratings yet

- Treasury Management Vs Cash Management Answer To Warm Up ExercisesDocument8 pagesTreasury Management Vs Cash Management Answer To Warm Up Exercisesephraim0% (1)

- 1.1 Cce To Proof of Cash Discussion ProblemsDocument3 pages1.1 Cce To Proof of Cash Discussion ProblemsGiyah UsiNo ratings yet

- FALL Class 7 - Cash Budgeting - Ch9 - GDBA - Note # 7 - TEACHERDocument7 pagesFALL Class 7 - Cash Budgeting - Ch9 - GDBA - Note # 7 - TEACHERAkankshaNo ratings yet

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020From EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020No ratings yet

- Rundown Webinar 4 Juli 2020Document2 pagesRundown Webinar 4 Juli 2020michelle beyonceNo ratings yet

- Timeline Interview Commitee MGT Award 2020Document2 pagesTimeline Interview Commitee MGT Award 2020michelle beyonceNo ratings yet

- Evaluating A Company'S External Environment: Mcgraw-Hill/IrwinDocument21 pagesEvaluating A Company'S External Environment: Mcgraw-Hill/Irwinmichelle beyonceNo ratings yet

- Chapter # 1 Outline: Mcgraw-Hill/IrwinDocument15 pagesChapter # 1 Outline: Mcgraw-Hill/Irwinmichelle beyonceNo ratings yet

- Group D - Network Effects On Multi-Sided Platform (Gojek)Document7 pagesGroup D - Network Effects On Multi-Sided Platform (Gojek)michelle beyonceNo ratings yet

- Gojek Case Study Group 4Document2 pagesGojek Case Study Group 4michelle beyonceNo ratings yet

- Creative Content On The Digital Campaign Tokopedia "Seller Story"Document15 pagesCreative Content On The Digital Campaign Tokopedia "Seller Story"michelle beyonceNo ratings yet

- Group 6 Psak 51-60Document11 pagesGroup 6 Psak 51-60michelle beyonceNo ratings yet

- Chapter 18Document6 pagesChapter 18michelle beyonceNo ratings yet

- The 73rd Constitutional Amendment ActDocument26 pagesThe 73rd Constitutional Amendment ActYasser ArfatNo ratings yet

- Resume Word OriginDocument5 pagesResume Word Originaflkvapnf100% (1)

- Abita Brand GuideDocument7 pagesAbita Brand GuideGabriel Bedini de JesusNo ratings yet

- Geometry AssignmentDocument2 pagesGeometry AssignmentAMIN BUHARI ABDUL KHADERNo ratings yet

- HIRARC FormDocument43 pagesHIRARC FormFachri Hidayat50% (2)

- CEDC Discl StatementDocument789 pagesCEDC Discl StatementChapter 11 DocketsNo ratings yet

- T5 B68 Craig Unger FDR - 5-21-04 Stull Email - Unger Saudi Flight Docs 616Document6 pagesT5 B68 Craig Unger FDR - 5-21-04 Stull Email - Unger Saudi Flight Docs 6169/11 Document ArchiveNo ratings yet

- Dodge Ram Truck 2006 2500 - 3500 BrochureDocument11 pagesDodge Ram Truck 2006 2500 - 3500 BrochureStephen RivettNo ratings yet

- 458-Radhika Polypack - Amd - xlsx1.Document2 pages458-Radhika Polypack - Amd - xlsx1.MUNINo ratings yet

- Dr. N. Kumarappan IE (I) Council Candidate - Electrical DivisionDocument1 pageDr. N. Kumarappan IE (I) Council Candidate - Electrical Divisionshanmugasundaram32No ratings yet

- Chem Project VDocument18 pagesChem Project Vmjvarun2006No ratings yet

- Programming Arduino Using Atmel Studio 6Document6 pagesProgramming Arduino Using Atmel Studio 6Carlos FerrarisNo ratings yet

- Astro-Logics Pub PDFDocument7 pagesAstro-Logics Pub PDFlbedar100% (1)

- Warman Slurry Correction Factors HR and ER Pump Power: MPC H S S L Q PDocument2 pagesWarman Slurry Correction Factors HR and ER Pump Power: MPC H S S L Q Pyoel cueva arquinigoNo ratings yet

- HX DG V 5.1.0 PDFDocument136 pagesHX DG V 5.1.0 PDFLyu SeyNo ratings yet

- Applied Physics On Spectros PDFDocument71 pagesApplied Physics On Spectros PDFKaskus FourusNo ratings yet

- Denim A New Export Item For BangladeshDocument2 pagesDenim A New Export Item For Bangladeshhabibun naharNo ratings yet

- PT English-6 Q2Document7 pagesPT English-6 Q2Elona Jane CapangpanganNo ratings yet

- Anand RathiDocument95 pagesAnand Rathivikramgupta195096% (25)

- Advanced Digital Controls Improve PFC PerformanceDocument18 pagesAdvanced Digital Controls Improve PFC Performancediablo diablolordNo ratings yet

- RecursionDocument9 pagesRecursionMada BaskoroNo ratings yet

- Learning Experiences Learning Outcome 3 - Install The Computer Application Software Learning Activities Special InstructionsDocument15 pagesLearning Experiences Learning Outcome 3 - Install The Computer Application Software Learning Activities Special InstructionsAlexandra FernandezNo ratings yet

- 9 Cir vs. Baier-Nickel DGSTDocument2 pages9 Cir vs. Baier-Nickel DGSTMiguelNo ratings yet

- Terraria Official Lore PDFDocument3 pagesTerraria Official Lore PDFCavalo SebosoNo ratings yet

- Ritishree Offer EztruckDocument4 pagesRitishree Offer EztruckKali RathNo ratings yet

- School - Guest Faculty Management SystemDocument1 pageSchool - Guest Faculty Management SystemSuraj BadholiyaNo ratings yet

- Topic:: SolidsDocument8 pagesTopic:: SolidsDhanBahadurNo ratings yet

- Final INTERNSHIP Report-AshishDocument66 pagesFinal INTERNSHIP Report-AshishAshish PantNo ratings yet

- Lecture Two: Theories of SLA: Input, Output and The Role of Noticing How Does SLA Take Place?Document4 pagesLecture Two: Theories of SLA: Input, Output and The Role of Noticing How Does SLA Take Place?Hollós DávidNo ratings yet

- Ielts Reading Test 1Document7 pagesIelts Reading Test 1Bách XuânNo ratings yet