Download as docx, pdf, or txt

You might also like

- Auditing Theory Test BankDocument31 pagesAuditing Theory Test BankLyza96% (53)

- Auditing Theory Test BankDocument32 pagesAuditing Theory Test BankJane Estrada100% (2)

- Module Title: Combinational and Sequential Logic Topic Title: Sequential Logic Tutor Marked Assignment 3 (V1.1)Document11 pagesModule Title: Combinational and Sequential Logic Topic Title: Sequential Logic Tutor Marked Assignment 3 (V1.1)Khadija YasirNo ratings yet

- USALI 10th VS 11th EditionDocument7 pagesUSALI 10th VS 11th EditionvictoregomezNo ratings yet

- Auditing Theory 01Document30 pagesAuditing Theory 01ralphalonzoNo ratings yet

- CH 1 Quiz With AnswersDocument7 pagesCH 1 Quiz With AnswersBeverly Ann Caparoso100% (3)

- IC TroubleshootingDocument64 pagesIC TroubleshootingKriti TyagiNo ratings yet

- Renr1367 11 01 All PDFDocument412 pagesRenr1367 11 01 All PDFJonathan Luiz PolezaNo ratings yet

- Aud Theo Dept. MIDTERM EXAMDocument8 pagesAud Theo Dept. MIDTERM EXAMChristine Joy OriginalNo ratings yet

- GAAS and Quality ControlDocument6 pagesGAAS and Quality ControlJanica BerbaNo ratings yet

- C. A System of Quality ControlsDocument11 pagesC. A System of Quality ControlsMC ExtNo ratings yet

- Quality Controls CparDocument33 pagesQuality Controls CparBrian TorresNo ratings yet

- Internal Audit Group 1 Report-Class Quiz Plan Engagements & Performance Appraisal NAME: - SCORE: - SECTION: - DATEDocument2 pagesInternal Audit Group 1 Report-Class Quiz Plan Engagements & Performance Appraisal NAME: - SCORE: - SECTION: - DATEdeleonjaniene bsaNo ratings yet

- Auditing Notes - Chapter 2Document17 pagesAuditing Notes - Chapter 2Future CPA90% (10)

- Auditing Theory Test Bank 2020Document180 pagesAuditing Theory Test Bank 2020Gela ValesNo ratings yet

- Airplane NotesDocument1 pageAirplane NotesEmma Mariz GarciaNo ratings yet

- Audit MCQDocument16 pagesAudit MCQAlexandria SomethingNo ratings yet

- Auditing Theory Final ExamDocument9 pagesAuditing Theory Final ExamGarcia Alizsandra L.No ratings yet

- Auditing Theory Reviewer 2Document3 pagesAuditing Theory Reviewer 2Sheena ClataNo ratings yet

- Auditing Theory - Q1 GAASDocument7 pagesAuditing Theory - Q1 GAASKevin James Sedurifa Oledan100% (1)

- AUDTHEOMIDTERMDocument6 pagesAUDTHEOMIDTERMClaudine DelacruzNo ratings yet

- AT02 System of Quality ControlsDocument8 pagesAT02 System of Quality ControlsZatsumono YamamotoNo ratings yet

- Auditing Chapter 2Document7 pagesAuditing Chapter 2lopo100% (1)

- Quiz Answer KeyDocument5 pagesQuiz Answer KeyJo Marie BlancaverNo ratings yet

- AAP ReviewerDocument14 pagesAAP ReviewerJadon MejiaNo ratings yet

- Jose Rizal University: College Ob Business Administration and AccountancyDocument2 pagesJose Rizal University: College Ob Business Administration and AccountancyLorielyn AgoncilloNo ratings yet

- Audit Theory PreboardDocument6 pagesAudit Theory PreboardCM LanceNo ratings yet

- Auditing Theory-2018Document26 pagesAuditing Theory-2018Suzette VillalinoNo ratings yet

- Jose Rizal University: College Ob Business Administration and AccountancyDocument2 pagesJose Rizal University: College Ob Business Administration and AccountancykmarisseeNo ratings yet

- Aurelia Anjani - 215154040 - 3B-AC - Tugas Latihan UTSDocument8 pagesAurelia Anjani - 215154040 - 3B-AC - Tugas Latihan UTS08AURELIA ANJANINo ratings yet

- Practice Questions Psa 210 Amp 300 PDF FreeDocument10 pagesPractice Questions Psa 210 Amp 300 PDF FreeAnna TaylorNo ratings yet

- (Roncal) at Midterms 2Document5 pages(Roncal) at Midterms 2Lorie RoncalNo ratings yet

- AT.2821 - Professional Standards Quality Control and Legal Liabilities PDFDocument6 pagesAT.2821 - Professional Standards Quality Control and Legal Liabilities PDFMaeNo ratings yet

- Practice Examination in Auditing TheoryDocument28 pagesPractice Examination in Auditing TheoryGabriel PonceNo ratings yet

- Seatwork For Professional Standards MCDocument5 pagesSeatwork For Professional Standards MCJoyce Ann CortezNo ratings yet

- Unit TestDocument6 pagesUnit TestMajoy BantocNo ratings yet

- Auditing Theory: C. Both I and IIDocument8 pagesAuditing Theory: C. Both I and IIKIM RAGANo ratings yet

- A. B. C. D. A. B. C. D.: ANSWER: Review Prior-Year Audit Documentation and The Permanent File For The ClientDocument7 pagesA. B. C. D. A. B. C. D.: ANSWER: Review Prior-Year Audit Documentation and The Permanent File For The ClientRenNo ratings yet

- Accntng 402 Module 1 MCQDocument21 pagesAccntng 402 Module 1 MCQRAY NICOLE MALINGINo ratings yet

- Practice Questions Psa 210 Amp 300Document10 pagesPractice Questions Psa 210 Amp 300Trixie Pearl TompongNo ratings yet

- At Quizzer 1 Fundamentals of Auditing and Assurance Services S2AY2122Document12 pagesAt Quizzer 1 Fundamentals of Auditing and Assurance Services S2AY2122GabNo ratings yet

- Auditing ReviewerDocument2 pagesAuditing Reviewerhannah3jane3amadNo ratings yet

- Audit Process and Audit Planning With AnswerDocument12 pagesAudit Process and Audit Planning With AnswerR100% (1)

- This Study Resource Was: Manila Central UniversityDocument5 pagesThis Study Resource Was: Manila Central UniversityMaryane AngelaNo ratings yet

- First ExamDocument11 pagesFirst ExamDiana BasarabaNo ratings yet

- 2 Multiple ChoiceDocument57 pages2 Multiple ChoiceMichael Brian TorresNo ratings yet

- ASUPRIN-testbank G. CosepDocument8 pagesASUPRIN-testbank G. CosepBelle RandrupNo ratings yet

- PSBA AT Quizzer 1 - Fundamentals of Auditing and Assurance Services 2SAY2021Document12 pagesPSBA AT Quizzer 1 - Fundamentals of Auditing and Assurance Services 2SAY2021Abdulmajed Unda MimbantasNo ratings yet

- Intermediate Accounting First ExamDocument9 pagesIntermediate Accounting First ExamJill morieNo ratings yet

- Department of Accountancy: Page - 1Document5 pagesDepartment of Accountancy: Page - 1NoroNo ratings yet

- Long Test Part 2 QuestionnaireDocument5 pagesLong Test Part 2 QuestionnaireNorman MoralesNo ratings yet

- PracExam On AudTheoDocument25 pagesPracExam On AudTheoPrancesNo ratings yet

- AT 3rdbatch 1stPBDocument12 pagesAT 3rdbatch 1stPBvangieolalia100% (2)

- ATDocument8 pagesATNoemi MacatangayNo ratings yet

- Preliminary Exam Reviewer1Document77 pagesPreliminary Exam Reviewer1Adam Smith0% (1)

- 2019 2020 501 ASSIGNMENT Audit ResponsibilitiesDocument2 pages2019 2020 501 ASSIGNMENT Audit ResponsibilitiesHeinie Joy PauleNo ratings yet

- AM Written Test PDFDocument6 pagesAM Written Test PDFJhaves AuzetinNo ratings yet

- Certified Construction Inspection OfficerFrom EverandCertified Construction Inspection OfficerRating: 5 out of 5 stars5/5 (1)

- Seatwork On Income Taxation NameDocument2 pagesSeatwork On Income Taxation NameVergel MartinezNo ratings yet

- Name of Student Task Performance (Quizzes) (50%)Document4 pagesName of Student Task Performance (Quizzes) (50%)Vergel MartinezNo ratings yet

- Final Midterm GradesDocument10 pagesFinal Midterm GradesVergel MartinezNo ratings yet

- Name of Student TASK PERFORMANCE (Quizzes) (50%) Class Participation (20%) Major Examination (30%)Document10 pagesName of Student TASK PERFORMANCE (Quizzes) (50%) Class Participation (20%) Major Examination (30%)Vergel MartinezNo ratings yet

- 2nd Term, SY 2019-2020 Quiz On Income Taxation Name: - Section: - Date: - Identification Identify The Following StatementsDocument2 pages2nd Term, SY 2019-2020 Quiz On Income Taxation Name: - Section: - Date: - Identification Identify The Following StatementsVergel MartinezNo ratings yet

- Time Value of MoneyDocument16 pagesTime Value of MoneyVergel MartinezNo ratings yet

- Quiz-Pre Engagement & Audit PlanningDocument5 pagesQuiz-Pre Engagement & Audit PlanningVergel MartinezNo ratings yet

- Quiz-FS AnalysisDocument3 pagesQuiz-FS AnalysisVergel MartinezNo ratings yet

- BondsDocument8 pagesBondsVergel MartinezNo ratings yet

- Marketable Securities + Receivable: Increase. IncreaseDocument4 pagesMarketable Securities + Receivable: Increase. IncreaseVergel MartinezNo ratings yet

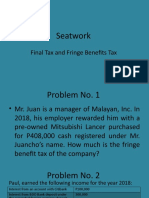

- Seatwork: Final Tax and Fringe Benefits TaxDocument6 pagesSeatwork: Final Tax and Fringe Benefits TaxVergel MartinezNo ratings yet

- 2nd Term, SY 2019-2020 Quiz On Income Taxation Name: - Section: - Date: - Identification Identify The Following StatementsDocument2 pages2nd Term, SY 2019-2020 Quiz On Income Taxation Name: - Section: - Date: - Identification Identify The Following StatementsVergel MartinezNo ratings yet

- Quiz-Pre Engagement & Audit PlanningDocument5 pagesQuiz-Pre Engagement & Audit PlanningVergel MartinezNo ratings yet

- Republic of The Philippines Department of Finance Bureau of Internal RevenueDocument20 pagesRepublic of The Philippines Department of Finance Bureau of Internal RevenueVergel MartinezNo ratings yet

- ListDocument5 pagesListVergel MartinezNo ratings yet

- Financial Statements AnalysisDocument9 pagesFinancial Statements AnalysisVergel MartinezNo ratings yet

- Quizzer-Donor's TaxDocument4 pagesQuizzer-Donor's TaxVergel Martinez33% (3)

- Cases) - Retrieved From: References Production ManagementDocument2 pagesCases) - Retrieved From: References Production ManagementVergel MartinezNo ratings yet

- RR 12 QuizDocument2 pagesRR 12 QuizVergel MartinezNo ratings yet

- Course Outline Example For BS AccountancyDocument5 pagesCourse Outline Example For BS AccountancyVergel MartinezNo ratings yet

- PILOsDocument2 pagesPILOsVergel MartinezNo ratings yet

- Nidec Philippines Corporation Company ProfileDocument35 pagesNidec Philippines Corporation Company ProfileVergel MartinezNo ratings yet

- Just in Time in Indian ContextDocument8 pagesJust in Time in Indian ContextLithin GeorgeNo ratings yet

- 22 2019-03-07 UdemyforBusinessCourseList PDFDocument72 pages22 2019-03-07 UdemyforBusinessCourseList PDFisaacbombayNo ratings yet

- TechnopreneurshipDocument2 pagesTechnopreneurshipAin AfiqahNo ratings yet

- Listening Test: Directions: For Each Question in This Part, You Will Hear Four Statements About A Picture in YourDocument40 pagesListening Test: Directions: For Each Question in This Part, You Will Hear Four Statements About A Picture in YourTrương Hữu LộcNo ratings yet

- Different Types of Irrigation System Advantages and DisadvantagesDocument12 pagesDifferent Types of Irrigation System Advantages and DisadvantagesEngr.Iqbal Baig100% (2)

- Week 10 CorporationssDocument9 pagesWeek 10 CorporationssAdrian MontemayorNo ratings yet

- Mannuru Et Al 2023 Artificial Intelligence in Developing Countries The Impact of Generative Artificial Intelligence AiDocument20 pagesMannuru Et Al 2023 Artificial Intelligence in Developing Countries The Impact of Generative Artificial Intelligence AiDr. Muhammad Zaman ZahidNo ratings yet

- Article 19 (A) Freedom of Speech and ExpressionDocument4 pagesArticle 19 (A) Freedom of Speech and ExpressionEditor IJTSRDNo ratings yet

- LTBR (Bursa-Yenişehir)Document10 pagesLTBR (Bursa-Yenişehir)SadettinNo ratings yet

- Metaphor AgerosegelelectroforeseDocument2 pagesMetaphor AgerosegelelectroforeseSuus.veluwenkampNo ratings yet

- Example ReportDocument4 pagesExample ReportFirzanNo ratings yet

- PDU-G1, 2: UHF Sensor For Partial Discharge Monitoring of GIS/GILDocument2 pagesPDU-G1, 2: UHF Sensor For Partial Discharge Monitoring of GIS/GILHafiziAhmadNo ratings yet

- Klasa 7 English LanguageDocument17 pagesKlasa 7 English LanguageSami R. PalushiNo ratings yet

- Linux PracticalDocument18 pagesLinux PracticalAnonymous x6UDQVBHawNo ratings yet

- UPDATE YANG BELUM Mengerjakan Sertifikasi TCO Maret Update 0804 Jam 08.00 WIBDocument2 pagesUPDATE YANG BELUM Mengerjakan Sertifikasi TCO Maret Update 0804 Jam 08.00 WIBWendi ArtheaNo ratings yet

- D-5 Track Maintenance Activities - Part 4Document35 pagesD-5 Track Maintenance Activities - Part 4rajeshengasst89No ratings yet

- 2.classfication of ComputersDocument54 pages2.classfication of ComputersBiswajit BeheraNo ratings yet

- MA REV 1 Finals Dec 2017Document33 pagesMA REV 1 Finals Dec 2017Dale PonceNo ratings yet

- Maria Katticaran/ M.Arch II/ UCLA SuprastudioDocument19 pagesMaria Katticaran/ M.Arch II/ UCLA SuprastudioMaria KatticaranNo ratings yet

- L410 Flight ManualDocument722 pagesL410 Flight ManualTim Lin100% (1)

- Research Paper About Asian CuisineDocument8 pagesResearch Paper About Asian Cuisineikofdvbnd100% (1)

- Kore Wa Zombie Desuka Volume 01Document252 pagesKore Wa Zombie Desuka Volume 01randydodson1993No ratings yet

- Internal External Forces For ChangeDocument16 pagesInternal External Forces For ChangeRoo BiNo ratings yet

- Legal Hurdle in Gaming PaymentDocument9 pagesLegal Hurdle in Gaming Paymentanurag kumarNo ratings yet

- Apollo Over The Moon A View From OrbitDocument266 pagesApollo Over The Moon A View From OrbitBob Andrepont100% (3)

- Calligraphy Fonts - Calligraphy Font Generator 2Document1 pageCalligraphy Fonts - Calligraphy Font Generator 2STANCIUC ALEXANDRA-ALESIANo ratings yet