Download as pdf or txt

You might also like

- Perspectives On Personality 8th Edition Carver Test BankDocument22 pagesPerspectives On Personality 8th Edition Carver Test BankKimberlyWilliamsonepda100% (46)

- Lesson 1 Tax Planning & ManagementDocument35 pagesLesson 1 Tax Planning & ManagementkelvinNo ratings yet

- PR Week 5 CVPDocument3 pagesPR Week 5 CVPAyhuNo ratings yet

- A Proposed Business Plan For Tricycle (Keke), Buses For Transportation Business - Feasibility Study - Martins LibraryDocument15 pagesA Proposed Business Plan For Tricycle (Keke), Buses For Transportation Business - Feasibility Study - Martins LibraryFrankie50% (2)

- CH8 Practice-ProblemsDocument11 pagesCH8 Practice-ProblemsLuigi Enderez BalucanNo ratings yet

- Module 2 HWDocument5 pagesModule 2 HWdrgNo ratings yet

- 6-3B - High-Low Method, Scattergraph, Least-Squares RegressionDocument8 pages6-3B - High-Low Method, Scattergraph, Least-Squares RegressionDias AdhyaksaNo ratings yet

- Construction Documentation - AIADocument7 pagesConstruction Documentation - AIAameeri143No ratings yet

- RECENSEO 2020 Comprehensive Examination Reviewer Material PDFDocument124 pagesRECENSEO 2020 Comprehensive Examination Reviewer Material PDFCamille CastroNo ratings yet

- Chapter 4Document27 pagesChapter 4Manish SadhuNo ratings yet

- Answers Chapter 4 - ACCT5204Document16 pagesAnswers Chapter 4 - ACCT5204abdulraheem.eesNo ratings yet

- Afm Week 2 Assignments Summer 2016Document4 pagesAfm Week 2 Assignments Summer 2016lexfred55No ratings yet

- Adam Bataineh Ch5Document10 pagesAdam Bataineh Ch5Omar AssafNo ratings yet

- Cost, Volume, Profit Analysis - Ex. SoluDocument19 pagesCost, Volume, Profit Analysis - Ex. SoluHimadri DeyNo ratings yet

- Managerial Accounting Chapter 6 Homework: 4 Out of 4 PointsDocument10 pagesManagerial Accounting Chapter 6 Homework: 4 Out of 4 PointsReal Estate Golden TownNo ratings yet

- Cost-Volume-Profit Relationships: Solutions To QuestionsDocument79 pagesCost-Volume-Profit Relationships: Solutions To QuestionsMursalin HossainNo ratings yet

- A Chp6 TUTDocument11 pagesA Chp6 TUTYong Jing YinNo ratings yet

- 2014 Bep Analysis ExercisesDocument5 pages2014 Bep Analysis ExercisesaimeeNo ratings yet

- ACCT 3001 Chapter 5 Assigned Homework SolutionsDocument18 pagesACCT 3001 Chapter 5 Assigned Homework SolutionsPeter ParkNo ratings yet

- Question 1 Hatem MasriDocument5 pagesQuestion 1 Hatem Masrisurvivalofthepoly0% (1)

- Tutorial 3 - Student AnswerDocument7 pagesTutorial 3 - Student AnswerDâmDâmCôNươngNo ratings yet

- Solutions CH 04 Managerial Accounting 11th Edition GarrisonDocument24 pagesSolutions CH 04 Managerial Accounting 11th Edition GarrisonArina Kartika RizqiNo ratings yet

- Exercise 5-1: Total Per UnitDocument18 pagesExercise 5-1: Total Per UnitSaransh Chauhan 23No ratings yet

- Accounting QuestionsDocument18 pagesAccounting QuestionsashmitaNo ratings yet

- Strat Cost CVP Analysis PDFDocument14 pagesStrat Cost CVP Analysis PDFA. HanifahNo ratings yet

- MA Chap 5Document19 pagesMA Chap 5Lan Tran HoangNo ratings yet

- Ch17 - Guan CM - AISEDocument40 pagesCh17 - Guan CM - AISEIassa MarcelinaNo ratings yet

- Prepared by DR - Hassan Sweillam University of 6 of October, EgyptDocument18 pagesPrepared by DR - Hassan Sweillam University of 6 of October, EgyptjgjghNo ratings yet

- CVP - GitttDocument15 pagesCVP - GitttFarid RezaNo ratings yet

- (Done) Activity-Chapter 2Document8 pages(Done) Activity-Chapter 2bbrightvc 一ไบร์ทNo ratings yet

- Et - Manac - 2014 SolutionDocument5 pagesEt - Manac - 2014 SolutionAmna NashitNo ratings yet

- ACG 2071, Test 2-Sample QuestionsDocument11 pagesACG 2071, Test 2-Sample QuestionsCresenciano MalabuyocNo ratings yet

- CVP AnalysisDocument7 pagesCVP AnalysisKat Lontok0% (1)

- AF2110 Management Accounting 1 Assignment 05 Suggested Solutions Exercise 6-13 (20 Minutes)Document12 pagesAF2110 Management Accounting 1 Assignment 05 Suggested Solutions Exercise 6-13 (20 Minutes)Shadow IpNo ratings yet

- Short Term Decision Making 2Document8 pagesShort Term Decision Making 2Pui YanNo ratings yet

- Chapter 4 Practice SolutionsDocument24 pagesChapter 4 Practice SolutionstolatillerNo ratings yet

- Chapter6 SolutionsDocument7 pagesChapter6 SolutionsCassandra Dianne Ferolino MacadoNo ratings yet

- Exercise C2Document13 pagesExercise C2Nhựt AnhNo ratings yet

- Traditional and Contribution Inc. Stat (TA)Document4 pagesTraditional and Contribution Inc. Stat (TA)Fatma AbdelnaemNo ratings yet

- $70) ÷ $150 53.33%) - This May Suggest That D. LawranceDocument1 page$70) ÷ $150 53.33%) - This May Suggest That D. LawrancejppjelNo ratings yet

- CVP Analysis QA AllDocument63 pagesCVP Analysis QA Allg8kd6r8np2No ratings yet

- Homework Chapter 5 EX 5-18Document9 pagesHomework Chapter 5 EX 5-18K59 Lai Hoang SonNo ratings yet

- Week 9 Suggested Solutions To Class QuestionsDocument8 pagesWeek 9 Suggested Solutions To Class QuestionspartyycrasherNo ratings yet

- Institute of Certified General Accountants of Bangladesh (ICGAB) Performance Management (P13) LC-3: CVP AnalysisDocument5 pagesInstitute of Certified General Accountants of Bangladesh (ICGAB) Performance Management (P13) LC-3: CVP AnalysisMozid RahmanNo ratings yet

- Hilton CH 8 Select SolutionsDocument9 pagesHilton CH 8 Select SolutionsDebashruti BiswasNo ratings yet

- 4 Lecture - CVP AnalysisDocument34 pages4 Lecture - CVP AnalysisDorothy Enid AguaNo ratings yet

- Answer - Case 1Document10 pagesAnswer - Case 1EVI MARIA SIBUEANo ratings yet

- Cost Volume Profit Relationships ExerciseDocument2 pagesCost Volume Profit Relationships ExerciseAvronil AnikNo ratings yet

- Revision Lecture With MADocument12 pagesRevision Lecture With MAMohamed ManoNo ratings yet

- Post Test 3Document5 pagesPost Test 3trixie manitoNo ratings yet

- 320C03Document33 pages320C03ArjelVajvoda100% (3)

- FMA Assg 1Document8 pagesFMA Assg 1Dagmawit NegussieNo ratings yet

- Managerial Accounting - 1Document4 pagesManagerial Accounting - 1Layla AfidatiNo ratings yet

- Cost II AssignmentDocument18 pagesCost II AssignmentAddisNo ratings yet

- Problem 7 39Document3 pagesProblem 7 39ninjai_thelittleninjaNo ratings yet

- AS5Document13 pagesAS5Andrea RobinsonNo ratings yet

- CVP ReportDocument11 pagesCVP Reportsyed danishNo ratings yet

- Additional Practice For MidtermDocument81 pagesAdditional Practice For MidtermMohmmad OmarNo ratings yet

- Tutorial 8Document6 pagesTutorial 8Steven CHONGNo ratings yet

- Review ch.6Document15 pagesReview ch.6LâmViên100% (9)

- Lecture 2 - CVP Analysis - QDocument6 pagesLecture 2 - CVP Analysis - Q1231402960No ratings yet

- Bài tập chương 13Document10 pagesBài tập chương 132021agl12.phamhoangdieumyNo ratings yet

- Assgment 1 (Chapter 1-4) : Agung Rizal / 2201827622Document10 pagesAssgment 1 (Chapter 1-4) : Agung Rizal / 2201827622Agung Rizal DewantoroNo ratings yet

- Hilton CH 7 Select SolutionsDocument25 pagesHilton CH 7 Select SolutionsParth ParthNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Optionals Syllbus BreakdownDocument6 pagesOptionals Syllbus BreakdownFajar KhanNo ratings yet

- PA XyzDocument20 pagesPA XyzFajar KhanNo ratings yet

- CSS-MPT Practice Paper 2023Document11 pagesCSS-MPT Practice Paper 2023Fajar KhanNo ratings yet

- TransferMoneyReceipt 1700828040388Document1 pageTransferMoneyReceipt 1700828040388Fajar KhanNo ratings yet

- Env SciencesDocument27 pagesEnv SciencesFajar KhanNo ratings yet

- Cost CHP 22Document75 pagesCost CHP 22Fajar KhanNo ratings yet

- Cost CH 7Document53 pagesCost CH 7Fajar KhanNo ratings yet

- Logic SolutionsDocument21 pagesLogic SolutionsFajar KhanNo ratings yet

- CHP 16 ..Cost ..Document23 pagesCHP 16 ..Cost ..Fajar KhanNo ratings yet

- Language Functions - IrvingDocument8 pagesLanguage Functions - IrvingFajar Khan100% (1)

- Return: Return What Is GST ReturnDocument3 pagesReturn: Return What Is GST ReturnNagarjuna ReddyNo ratings yet

- Case StudyDocument13 pagesCase StudyDamola LashNo ratings yet

- E-Commerce Website QuotationDocument4 pagesE-Commerce Website QuotationfasiloginNo ratings yet

- Improvement of Inventory System Using First in First Out (FIFO) MethodDocument6 pagesImprovement of Inventory System Using First in First Out (FIFO) MethodZillah KeruboNo ratings yet

- Sage ERP X3 DistributionDocument6 pagesSage ERP X3 Distributionyakob tsegaNo ratings yet

- CSR PolicyDocument1 pageCSR Policybhupendra1988No ratings yet

- Project CrashingDocument24 pagesProject CrashingVINITHA100% (1)

- Senior Business Analyst Resume ExampleDocument1 pageSenior Business Analyst Resume ExamplevidyapablaNo ratings yet

- KCB FormsDocument2 pagesKCB FormsNakhayo Juma67% (3)

- Section 3 of The NLRC Rules of Procedure, As Amended, ClearlyDocument5 pagesSection 3 of The NLRC Rules of Procedure, As Amended, ClearlyDe Lima RJNo ratings yet

- Business PlanDocument24 pagesBusiness PlanRoanne Mae Canedo-PelorianaNo ratings yet

- Tanada VS Angara Case DigestDocument2 pagesTanada VS Angara Case DigestVincent Rey BernardoNo ratings yet

- IGCSE Economics 1.2 The Factors of ProductionDocument4 pagesIGCSE Economics 1.2 The Factors of Productionyeweiwei0925No ratings yet

- Mittal Commerce Classes Intermediate - Mock Test (GI-1, GI-2, GI-3, VI-1, SI-1, VDI-1)Document6 pagesMittal Commerce Classes Intermediate - Mock Test (GI-1, GI-2, GI-3, VI-1, SI-1, VDI-1)Shubham KuberkarNo ratings yet

- Improving Software Quality With Agile TestingDocument7 pagesImproving Software Quality With Agile TestingAnika TahsinNo ratings yet

- SUSTAINABLE LogisticsDocument17 pagesSUSTAINABLE LogisticsLoubna BourkhaNo ratings yet

- To Close Your Team's Cloud Skills Gap: Learn-By-Doing TrainingDocument4 pagesTo Close Your Team's Cloud Skills Gap: Learn-By-Doing Trainingrahul tejNo ratings yet

- Early TQM Successes: - Nashua - Xerox - Motorola - Intel - Dayton-Hudson - Corning - Hewlett-PackardDocument31 pagesEarly TQM Successes: - Nashua - Xerox - Motorola - Intel - Dayton-Hudson - Corning - Hewlett-Packardrocks tusharNo ratings yet

- Nigel Slack Chapter 13 Supply Chain Planning and ControlDocument22 pagesNigel Slack Chapter 13 Supply Chain Planning and ControladisopNo ratings yet

- IMS Int Audit-Day 1Document40 pagesIMS Int Audit-Day 1info qtcNo ratings yet

- Union Budget 2023 - 2024: A Plenary DiscussionDocument17 pagesUnion Budget 2023 - 2024: A Plenary DiscussionKAVITHA K SNo ratings yet

- Flexible Manufacturing Systems (S1-15 - EAZC412) - CHDocument20 pagesFlexible Manufacturing Systems (S1-15 - EAZC412) - CHymsyaseenNo ratings yet

- Human Being in The Manmade WorldDocument1 pageHuman Being in The Manmade WorldAvipriyo KarNo ratings yet

- Berthing Policy and Tariff Structure Wef 01 APRIL 2021Document35 pagesBerthing Policy and Tariff Structure Wef 01 APRIL 2021jaya thawaniNo ratings yet

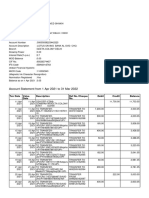

- Statement 22Document14 pagesStatement 22Saud ShaikhNo ratings yet